FUTU - Futu Holdings: Still A Speculative Buy

2023-04-11 11:27:14 ET

Summary

- Futu delivered a solid December 2022 quarter, beating analyst estimates with regard to both topline and earnings.

- For FY 2022, Futu's topline expanded by about 7% YoY, to $976 million, and Non-GAAP net income increased 4.2% YoY, to $401.4 million.

- As compared to a $7.5 billion market cap, Futu's FY 2022 net income pegs Futu stock valuation at below x20 P/E.

- Post Q4 and FY 2022, I update my EPS expectations for Futu through 2025, and I now calculate a fair implied share price of $62.01.

- My reiterated 'Buy' recommendation continues to be accompanied by a 'speculative' tag, due to unresolved regulatory risks.

Thesis

Quite some time has passed since I initiated coverage on Futu Holdings (FUTU) with a Buy recommendation--and the stock is up close to 35% as compared to a loss of about 1% for the S&P 500 ( SP500 ). Now, reflecting on Futu's strong Q4 and FY 2022 result s, I am confident to reiterate my bullish thesis: I continue to believe that Futu is excellently positioned to capture market share in the large and fast-growing Chinese/ APAC brokerage market, and broader fintech ecosystem (e.g., wealth management)

Post Q4 and FY 2022, I update my EPS expectations for Futu through 2025, and I now calculate a fair implied share price of $62.01.

Strong FY 2022 Support Bullish Thesis

Despite a challenging macroeconomic backdrop (trading volume around the world has been materially lower in Q4 2022 vs Q4 2021), Futu delivered a solid December 2022 quarter, beating analyst estimates with regards to both topline and earnings. During the period from September to end of December, Futu generated $292.3 million of revenues, as compared to about $182.2 million for the same period one year earlier (up 42.3% YoY) and compared to $260 million estimated by analyst consensus ($30 million beat). Futu's Non-GAAP net income came in at $130 million, a 90.2% YoY increase and a $32 million consensus beat respectively.

In Q4 2022, Futu's number of paying clients increased 19.5% year over year, to 1,486,980 as of end of December 2022 (adding about 240 thousand paying clients in 2022). That said, the strong growth in user base offset a contraction in (i) total trading volume, (ii) daily average revenue trades, and (iii) margin financing and securities lending, which fell year over year by (i) 10.9%, ((II)) 8.1% and ((III)) 12.2% respectively.

For the full year 2022, Futu's topline expanded by about 7% YoY, to $976 million. With regards to profitability, gross profit increased by approximately 12% YoY, to $850 million, and Non-GAAP net income increased 4.2% YoY, to $401.4 million.

The Long View - Expecting More Growth

As compared to a $7.5 billion market cap, Futu's FY 2022 net income of slightly more than $400 million pegs Futu stock valuation at below x20 P/E. Such a multiple is, in my opinion, too cheap to ignore considering that Futu has grown and is likely to continue to grow at an attractive double-digit CAGR. For reference, investors should consider that the fintech ecosystem in China is estimated to expand at a >18% CAGR through 2028, according to insights collected from Mordor Intelligence. And Futu is working to aggressively capture opportunities outside of China, including Singapore, United States, Australia and Japan, while also investing heavily in R&D to expand its product portfolio across fintech services (wealth management, ECM, etc.). That said, Futu is notoriously competitive with regards to tech capabilities and user-friendliness; so, I believe Futu is well positioned to capture an attractive slice of these target market growth opportunities.

While Futu management did not give formal guidance, I estimate that on the backdrop of a more favorable market sentiment, Futu will add about 200,000 - 220,000 new paying clients in FY 2023 (approximately 18% YoY growth), and push revenues towards about $1.1 billion (13% YoY growth; approximately in line with analyst consensus estimates).

Regulatory Risk Appears Manageable

Admittedly, Futu's near/-mid term commercial outlook remains clouded by regulatory uncertainty, after the CSRC ordered Futu and UP Fintech (TIGR) to not accept new China-based customers on the platform, citing concerns of illegal cross-border money flows. However, Futu may continue to serve existing clients.

During the post-earnings analyst conference, Futu management said that the company has not received any further regulatory guidance since the CSRC's announcements in December. Moreover, the company said the impacts of said announcement have been manageable: According to the company, net assets outflow in the first half of January 2023 only being about 1% to 2% of total client assets, while assets outflow reversed back to net asset inflows starting from February.

Target Price Update

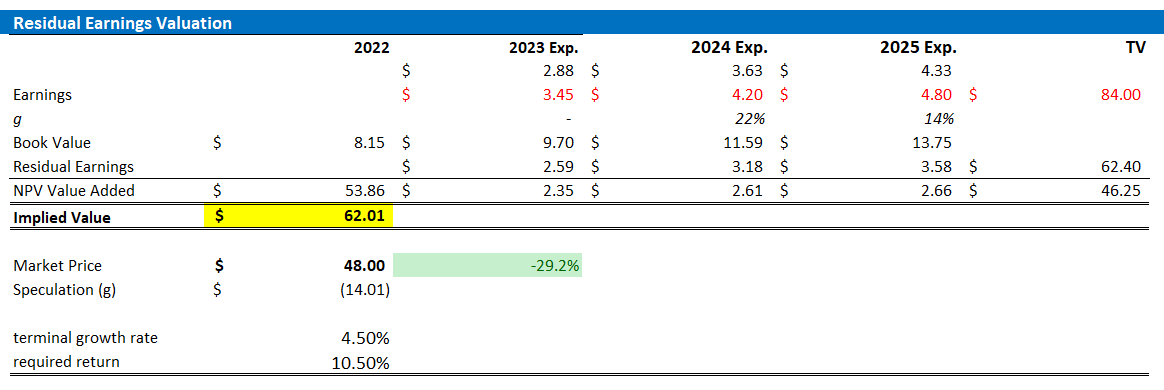

Expecting that trading volume will likely pick-up again in 2023 and beyond, as compared to a depressed environment throughout 2022, I estimate that Futu's FY 2023 earnings will likely expand to somewhere between $3.3 and $3.6. Moreover, I also lower my EPS expectations for 2024 and 2025, to $4.2 and $4.8, respectively.

I continue to anchor on a 4.5% terminal growth rate (about 1-2 percentage point higher than estimated nominal global GDP growth), as well as on a 10.5% cost of equity.

Given the EPS updates as highlighted below, I now calculate a fair implied share price of $62.01, as compared to my previous target price of $41.6 earlier .

{kind=link}

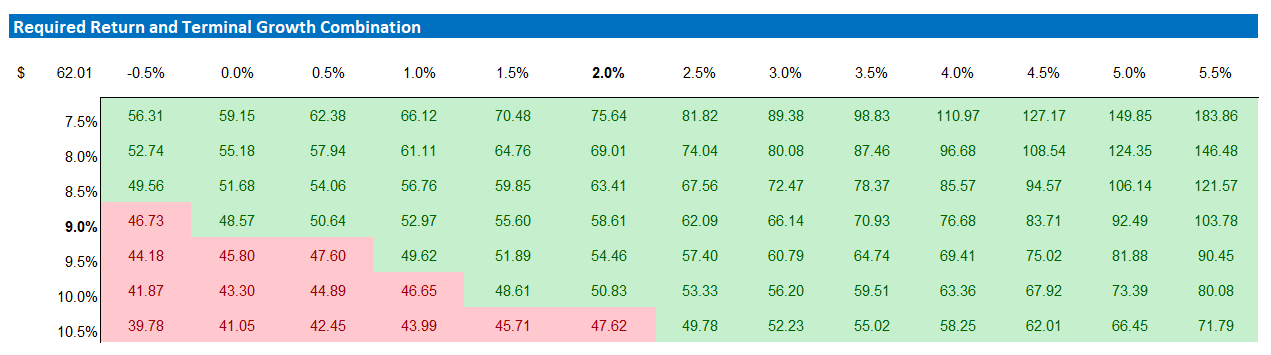

Below is also the updated sensitivity table.

{kind=link}

Conclusion

I continue to be bullish on Futu Holdings; In my opinion Futu's digital-first brokerage business model--focused on innovation and user experience-- positions the company to capture an attractive e-brokerage/ fintech market opportunity in China and broader APAC. However, the bullish thesis also continues to be accompanied by a 'speculative' tag, as unresolved regulatory risk clouds commercial opportunities.

Following Futu's Q4 and FY 2022 results, I update my EPS expectations for Futu through 2025, and I now calculate a fair implied share price of $62.01.

For further details see:

Futu Holdings: Still A Speculative Buy