FF - FutureFuel Corp.: Watching But Not Buying Here Just Yet

2023-11-27 16:57:33 ET

Summary

- FutureFuel Corp.'s stock price has declined steadily and is currently around $6 per share.

- The company operates in a growing market for biofuels, but strong top and bottom line expansion is needed for a more positive outlook.

- The company has shown improvement in net income, but challenges and risks remain, including potential policy changes and transportation obstacles.

Investment Rundown

The stock price for FutureFuel Corp. ( FF ) has been on quite the ride the last 12 months, especially after the Q2 report in August this year which resulted in the valuation dropping by almost 30% as the results were not that impressive to the market it seems. It has not managed to return to those levels again and has instead declined steadily to around $6 per share. I unfortunately think this will continue to be the case as the bottom line margins have been in the same trajectory reaching 5-year lows of 7.34% as opposed to an average of over 20%.

The market that the company operates in is quite appealing as it's expected to continue to expand at a double-digit rate over the next several years. I think that with the dividend the company has now as well, it's enough to make it a hold case but not more as I do think we need to see the strong top and bottom line expansion before such a thesis could be established. Last year the company had notable losses on marketable securities and other expenses which dragged down the net income. It's a positive trend that this seems to be reversing at least and that FF has nine months net income of $13 million in 2023 which is sufficient to support the $10.5 million distributed as dividends. For now, though I am rating FF a hold.

Company Segments

FF is involved in the production and sale of a diverse range of chemical products, bio-based fuels, and specialty chemicals within the United States. The company operates through two primary segments, namely Chemicals and Biofuels.

In the Chemicals segment, FutureFuel offers a wide array of custom chemicals utilized in applications such as coatings, chemical intermediates, and industrial and consumer cleaning. This diversified product portfolio positions the company to cater to various industries and adapt to market demands. The Biofuels segment reflects its commitment to sustainable solutions, emphasizing the production of bio-based fuels that contribute to the evolving landscape of renewable energy sources.

{kind=link}

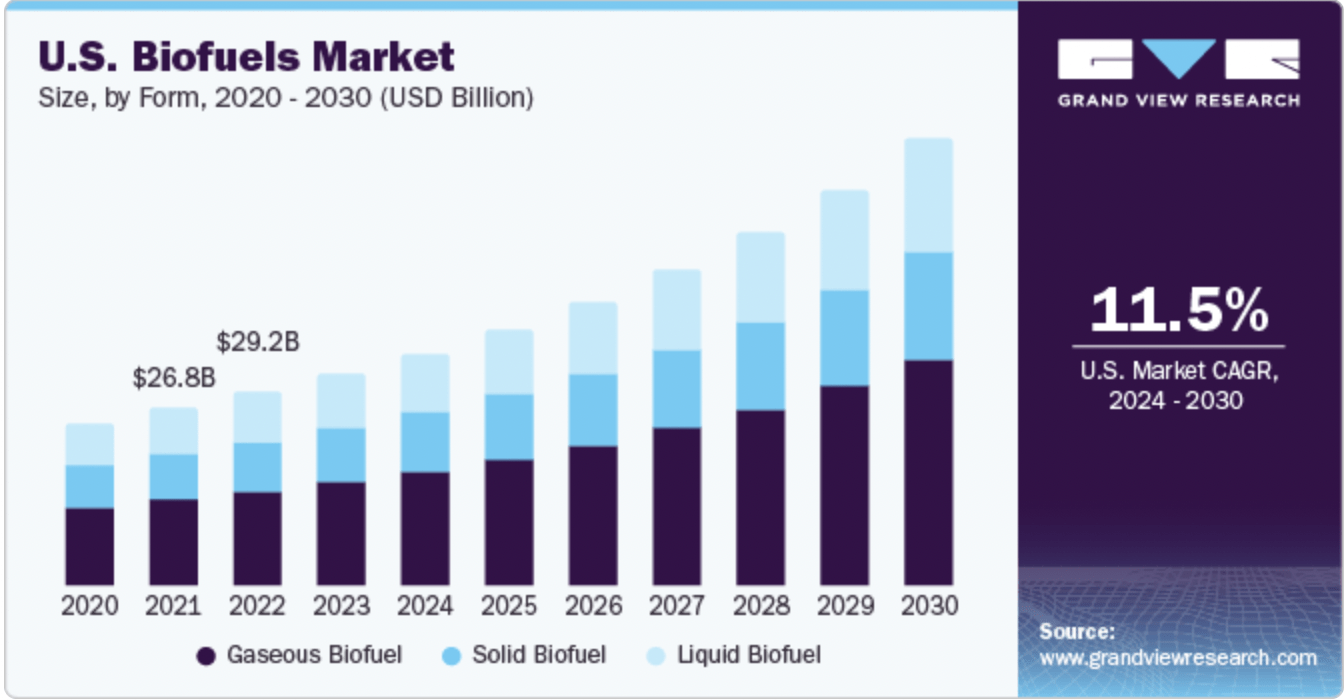

The company is a part of a growing market which in the US alone is expected to grow at a CAGR of 11.5% between 2020 and 2030. Looking at the results from FF the last 3 years going back to 2022 it has averaged an annual top-line expansion rate of 31.12% . This is beating out the market by a fair bit and could be a reason for the hype the stock has received since 2020. Peaking at nearly $15 per share it has since declined by over 50%.

Key trends in the biobased fuels market include advancements in biofuel production technologies, increased investment in research and development, and supportive government policies promoting the use of renewable energy. The demand for biobased fuels is expected to rise as industries and consumers prioritize eco-friendly options.

Germany Biofuel (BAFA)

The potential demand for biobased fuels is driven by their ability to lower greenhouse gas emissions, enhance energy security, and contribute to a circular economy. With a growing emphasis on decarbonization and the transition to cleaner energy sources, the biobased fuels market is likely to witness sustained growth in the coming years. The outlook remains positive, aligning with global efforts to achieve more sustainable and environmentally friendly energy solutions. Germany for example, which is a country pushing quite heavily for more green energy is seeing a steady climb in the usage of biobased fuels and this supports the current market outlook in my opinion.

Earnings Highlights

Looking at the last report from the company on November 9th it has produced some decent results as the bottom line has expanded exponentially compared to 2022.

{kind=link}

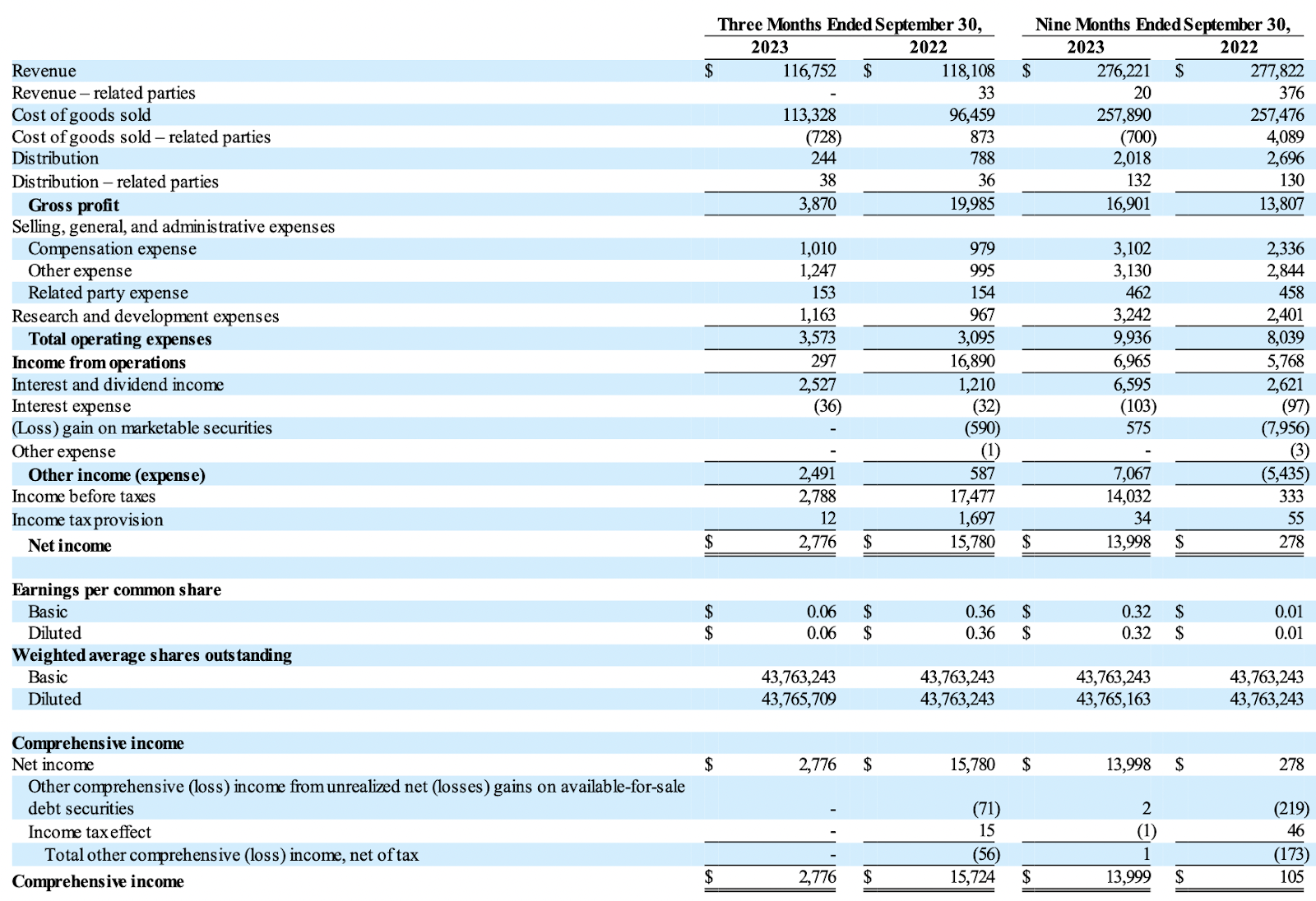

Some of the key drivers for the net income going from $ 278,000 in nine months during 2022 to over $13 million in 2023 have been gains from “other income” and also gains from marketable securities as opposed to over $7 million in losses last year. The company managed to sell 19 million gallons of biodiesel during the quarter and this increased the cashflows from operations by a decent amount. The company was however negatively affected by the rise of heating oil prices which generated a loss in the derivatives that the company holds. For the short term, the company sees margins under pressure as high feedstock prices and weak RIN values are key contributors. I think this is a reason for the share price unfortunately continuing to go lower in the coming quarters. But when we see a reversal then the stock price could rebound very fast.

{kind=link}

Should the net incomes return to pre-pandemic of around $88 million then we are looking at a p/e of around 3. This is incredibly low in comparison to the sector's average of close to 15. On a 5-year average FF has also traded closer to 8 which is 41% higher than right now. I think these are factors that contribute to my perhaps slightly more positive outlook on the business. I still want to see strong margin expansion and market trends continuing before suggesting a higher rating for FF, but in the meantime, I think they can adequately support their dividend, and should prices improve they might even be able to raise it too. What is very positive is the low amount of debt the company has and the small effect higher interest rates have had. The interest expenses are just around $100 000 which is easily manageable by the company.

Risks

FCF at FF has faced challenges in recent years but is showing signs of recovery. Despite the positive trend, there's a need for sustained improvement before confidently recommending FF as more than a hold at the moment. Investors are eagerly anticipating a return to the pre-pandemic levels of consistency in FCF.

{kind=link}

The market's response to FF's Q2 report suggests that if FCF doesn't continue to improve, the share price may face ongoing pressure. Paying a 24x multiple for FCF seems unreasonable unless there's clear evidence of expanding profitability. A cautious approach is warranted until there's more certainty about the persistence of FCF improvement and its alignment with market expectations.

{kind=link}

The company faces additional risks, notably the potential impact of losing governmental mandates and incentives, including the Biomass-Based Diesel Tax Credit, which could adversely affect its business. Moreover, obstacles to reliable and cost-effective transportation through various channels, such as rail, truck, and pipelines for both raw materials and finished goods, have the potential to significantly diminish the company's profit margins. These challenges underline the importance of monitoring policy changes and addressing transportation-related hindrances to ensure sustained profitability. With inflation seemingly going lower after peaking in 2022 I think that investors will be looking at how the cost of revenues grow for FF. After materials have inflated in price FF needs to adequately grow their margins too and if they do not have a strong enough MOAT then they may not be capable of passing down some of the costs to customers. This would be a drag on the bottom line margins ultimately and something that will be a key factor in my opinion for the stock price continuing its downward trend.

{kind=link}

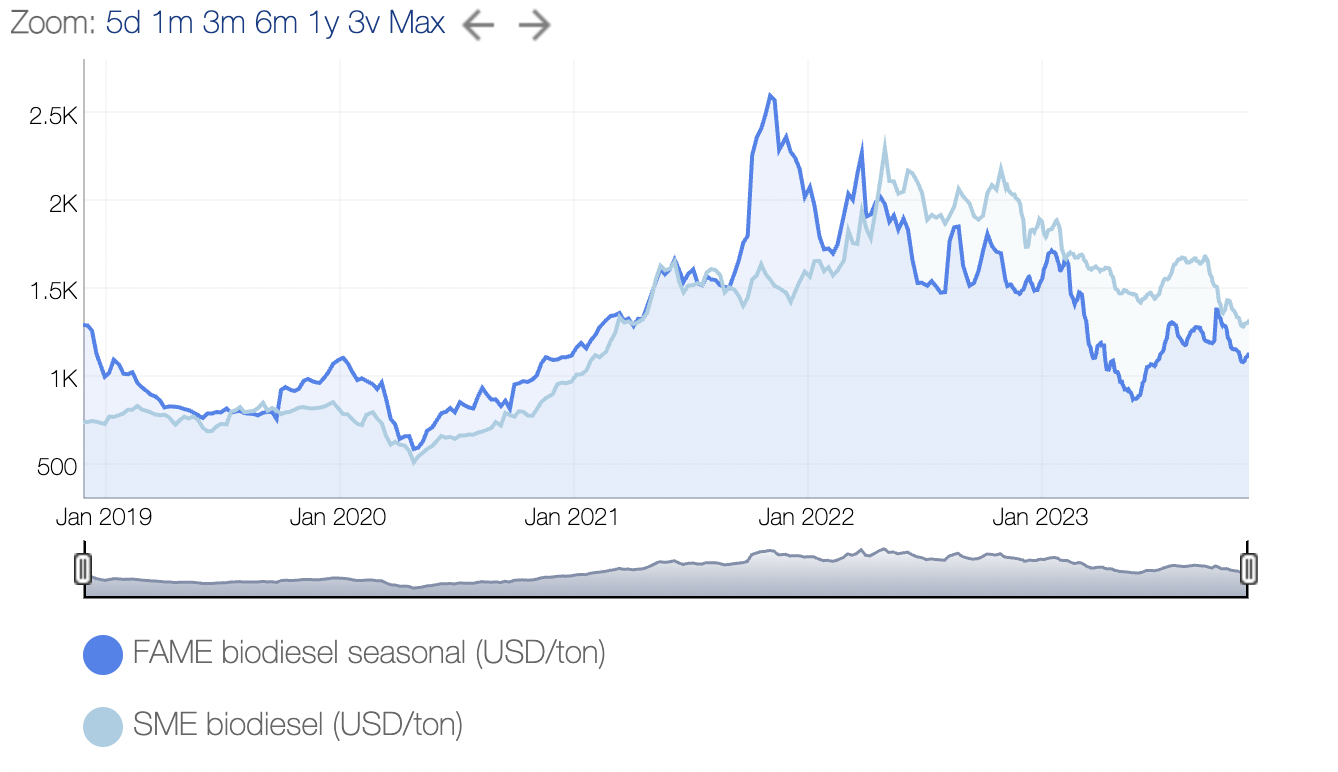

What could be a disruption though to the positive is if the biodiesel prices surge and cause FF to see even higher revenues and as a result stronger earnings too. I think that could be a justifiable reason for raising the valuation as the potential value investors could extract would likely improve in the shape of dividend raises or the announces of a special dividend too.

Final Words

FF has seen its valuation slashed since its peak back in 2021. It continues to post quite strong results in my opinion but the short term is still under pressure I think as margins could be pressed by various external factors noted by the management. These are things that likely will contribute to the stock price going lower. Selling shares I don't think is reasonable here as FF is a long-term play seeing as they are in the biofuels market, one that is expected to see double-digit growth over the next 7 years at least. FF has proved to be able to outperform this and this concludes to me rating it a hold.

For further details see:

FutureFuel Corp.: Watching But Not Buying Here Just Yet