USA - GAB And USA: The Results After Making A Swap

2023-08-01 14:28:33 ET

Summary

- The swap between Gabelli Equity and Liberty All-Star Equity funds has proven successful for investors, with USA significantly outperforming on a total return basis.

- Both funds are now trading at similar valuations, with the performance difference likely to come from the underlying portfolio rather than convergence in valuations.

- Despite the success of the swap, neither fund is considered a strong buy candidate at this time due to both still trading above their longer-term historical discount levels.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Just over a year ago , I presented the idea that a swap between Gabelli Equity ( GAB ) to Liberty All-Star Equity ( USA ) made a lot of sense. The main premise of the idea was that GAB was trading at an incredibly rich premium, and USA was at a much more logical valuation in terms of its premium. Well, the end result was incredibly successful for investors that took caution with GAB's premium and made such a swap.

USA, since that time, has significantly outperformed on a total return basis. Even on a total NAV return basis, the fund put up a bit of better results too. For a period, GAB was outperforming through the end of 2022 and heading into 2023, but USA caught back up. During this time, since the initial idea was presented, GAB provided essentially flat total returns despite the quite positive total NAV return results. This helps highlight the power of playing discounts/premiums and making swaps when they present themselves.

Ycharts

Going forward, the valuations between these funds are quite similar now and taking one over the other shouldn't lead to such a drastic outcome. Now, the performance difference could come from the underlying portfolio and not convergence in premiums.

Ycharts

Admittedly, both of these funds are still trading above their longer-term historical levels since going back to their inception, which have both on average traded at discounts. So I don't believe that either fund is necessarily a strong buy candidate at this time.

Both of these funds are quite old, with GAB being slightly older, with the inception on 8/21/1986 when USA launched a couple of months later on 10/31/1986. USA's valuation appears to have been more volatile during its life relative to GAB.

Ycharts

I would also note that in November, I made an update on GAB , where I revisited this same idea for an update. At that time, I had also noted that the idea had mostly played out too, and buying either at that time seemed okay. In fact, we are essentially in the same position now as we were then.

Now that GAB's premium has come down, this trade has played out and holding either is okay at this point. That being said, both are still trading at slight premiums, which doesn't necessarily seem warranted when you are getting some pretty plain equity exposure. So, I still can't apply a "Buy" rating outright.

Going forward, this will be my final update on this swap idea until the valuations provide a scenario where the same sort of opportunity can be made. I just wanted to do one final tie up piece for this idea.

GAB Basics

- 1-Year Z-score: -0.79

- Premium: 6.88%

- Distribution Yield: 10.43%

- Expense Ratio: 1.37%

- Leverage: 21.04%

- Managed Assets: $2.019 billion

- Structure: Perpetual

GAB's investment objective is "long-term growth of capital, with income as a secondary objective." Generally, we see that the investment objective for closed-end funds is often income or high income. In this case, GAB is looking for long-term growth of capital, which it technically hasn't been successful with. There has been very limited appreciation, and returns have only come from the distributions.

The fund is also leveraged, while USA is not. They've taken the approach of raising leverage primarily through fixed-rate preferred offerings. That has proven to be a good thing as interest rates have risen; the preferreds have kept their borrowing costs from rising significantly.

GAB Capital Structure (Gabelli)

These are publicly traded as well, making it easy access for investors to buy and sell these if interested; 5% Series G ( GAB.PG ), 5% Series H ( GAB.PH ) and 5% Series K ( GAB.PK ).

USA Basics

- 1-Year Z-score: 0.56

- Premium: 2.43%

- Distribution Yield: 9.48%

- Expense Ratio: 0.93%

- Leverage: N/A

- Managed Assets: $1.75 billion

- Structure: Perpetual

USA's investment objective is to "seek total investment return, comprised of long-term capital appreciation and current income. It seeks its investment objective through investment primarily in a diversified portfolio of equity securities."

The fund takes a bit of a different approach than other closed-end funds. They don't have just one advisor managing, but five different investment managers that take a sleeve of the fund to invest. They have three value-oriented managers and two growth managers. They put 60% of their portfolio in what is considered value and the other 40% in growth.

With no leverage, the fund can generally be seen as a relatively less volatile name. They don't have to deal with higher interest rates increasing borrowing costs either, simply because there are no borrowing costs to consider

Why They Are Decent Swap Candidates

What makes these funds so easy to compare is that they are fairly similar because they are pretty plain equity funds. They don't implement any sort of strategy that is too fancy.

However, the longer-term results of the funds have been quite different, with USA generally outperforming by a considerable level. So the longer period of time that goes by, the longer the chance for divergence in performance. This is the result of the funds over the last decade. USA's performance has been almost double GAB's on a total NAV return basis.

Ycharts

This is why some investors could clearly argue that a premium for USA over and above GAB would be justified. However, investors have chosen to value GAB at a higher valuation, with its average discount lower relative to USA's. Undoubtedly, there could be some merit to that, but I'd suggest that almost no premium is justified for a plain equity fund. Some alternatives trade at discounts or ETFs that trade at NAV if you aren't worried about a high distribution rate.

The shorter periods of time can see the correlation between these funds hold a bit more snugly - as we reflected around a year ago in the above chart showing results since the initial swap idea last year.

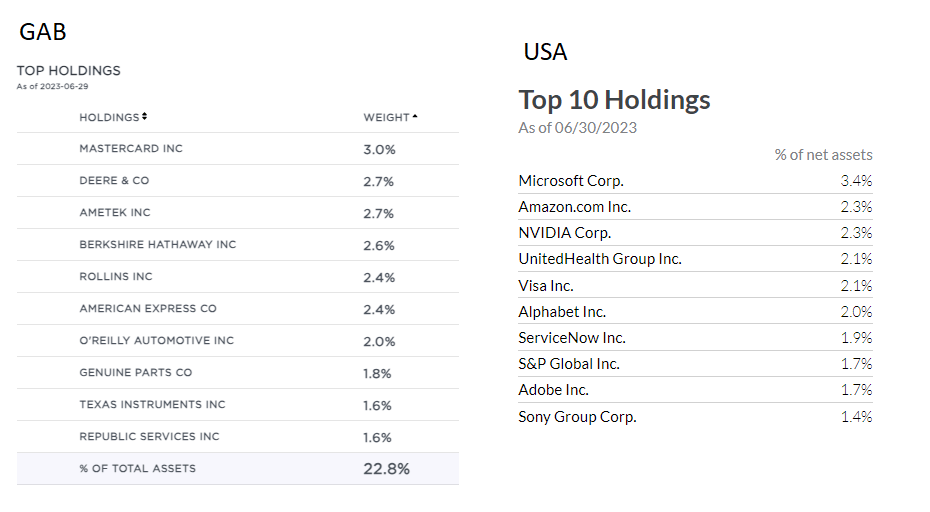

In looking at the top holdings, we can see differences between these names and why the longer-term results would diverge so materially.

{kind=link}

Despite USA's tilt toward a more value approach, GAB traditionally goes even heavier in value investing. This is a common characteristic of Gabelli Funds, as he's a known value-oriented investor.

USA's top holdings include some of the mega-cap growth names Microsoft ( MSFT ), Amazon ( AMZN ), Alphabet ( GOOG ) (GOOGL) and even NVIDIA ( NVDA ), which has been on an amazing run. Enough to make it push into the $1 trillion market cap club.

This isn't to say that GAB's holdings are bad, but they are definitely tilted more toward the older and usually slower growers. That is besides maybe Mastercard ( MA ), which has been on a faster pace of growth relative to other names.

MA Growth Grade Relative to Sector (Seeking Alpha)

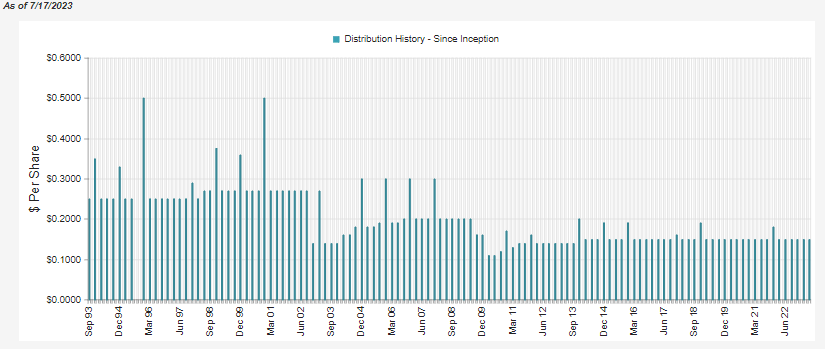

Additionally, both funds boast a high distribution yield. This is because they have managed distribution policies where they target 10% payouts annually. GAB's current distribution rate is 10.43%, with a NAV rate of 11.15%. This is above their managed target, but they use their managed target more as a minimum. In years where the 10% isn't met (or regulations result in them needing to distribute out more or face excise tax), they'll top it off with a year-end special.

Over time, the fund has cut its distribution in the periods where we would expect it to. That is the Dotcom bubble and the Global Financial Crisis.

{kind=link}

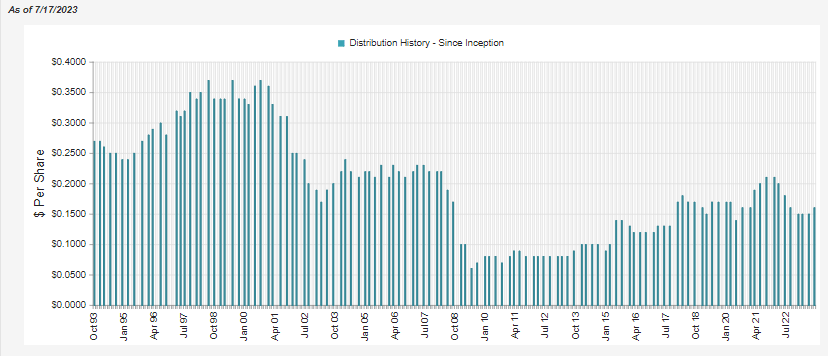

With USA, the approach is a bit different in that they take an approach of a 10% managed distribution plan annually. However, it is adjusted with each quarterly payment at a rate of 2.5%.

The current policy is to pay distributions on its common shares totaling approximately 10 percent of its net asset value per year, payable in four quarterly installments of 2.5 percent of the Fund's net asset value at the close of the New York Stock Exchange on the Friday prior to each quarterly declaration date.

This means that the distribution will generally be in a different amount every quarter. It also means the payout rate is going to be closer to 10% at any given time. Currently, the latest distribution rate works out to a 9.48% payout, and on a NAV basis, it comes to 9.71%. If the fund can continue an upward trajectory, we would expect an increased distribution again for the next one.

The overall trend is the same, lower distributions during the Dotcom bubble crash and then reductions during the GFC as NAV came crashing down.

{kind=link}

For some investors, this argument would favor GAB, which provides a generally more level distribution policy over USA's essentially variable (but predictable) rate.

Of course, as the share prices and NAVs have fallen since inception, we know these funds haven't entirely covered their distributions through income and gains. Despite that, total returns can still be respectable when factoring in the distributions. In fact, USA has performed so well in the last decade now that it actually topped the SPDR S&P 500 ETF ( SPY ) results. GAB has lagged considerably, which goes back to the more value-oriented approach we touched on above.

Ycharts

Conclusion

GAB and USA can present swap opportunities in the shorter term when their discount and premium levels diverge significantly. Over the longer term, the results between the funds have been quite different, so that is one of the main risks. That said, both funds are pretty straightforward vanilla equity funds that boast managed 10% distribution plans. The way these plans are implemented takes different approaches, but the end result is that both offer higher distribution rates than other equity peers.

For further details see:

GAB And USA: The Results After Making A Swap