GRTX - Galera Therapeutics: A Possible Solution To Severe Oral Mucositis In Head And Neck Cancer Patients

2023-04-24 18:33:13 ET

Summary

- Pivotal Phase 3 results were erroneously reported as missing both the primary and secondary endpoints causing a 70% share price drop in 2021.

- Phase 3 results actually hit both primary & a key secondary endpoint.

- The share price has not recovered and is still 80% less than the all time high.

- The company’s PDUFA date of Aug 9, this year for Avasopasem will be a significant catalyst.

- Avasopasem has Breakthrough Therapy Designation, Fast Track & priority review designations which bodes well for the upcoming PDUFA decision.

Investment Thesis

Galera Therapeutics ( GRTX ) lead asset, Avasopasem, completed a successful Phase 3 trial, has Breakthrough therapy designation (BTD), Fast Track Designation, and Priority Review with an upcoming PDUFA date on Aug 9, 2023. The FDA did not request an advisory committee (Adcom) for Avasopasem's NDA. Its primary market is an unmet medical need for radiation-induced Severe Oral Mucositis (SOM). The share price sits at less than $3 which is less than 20% from its all-time high. The company has adequate cash until 4th Q 2023 and we expect the share price to continue to rise as the PDUFA date gets closer.

Article Focus

GRTX has 2 primary drugs (Avasopasem & Rucosopasem). Avasopasem has finished its testing for SOM for Head & Neck Cancer (HNC). Rucosopasem is in Phase 2 clinical testing for pancreatic and lung cancer. This article will only highlight Avasopasem and the SOM market. We recommend reading other Seeking Alpha articles for analysis on Rucosopasem.

This article will primarily focus on 4 parts: the likelihood of Avasopasem gaining NDA approval from the FDA this August, the current share price relative to its historical price, the potential market for the drug, and the risks of investing in GRTX. All four will support our case for a Strong Buy recommendation.

Company Summary

Galera Therapeutics went public in late 2019 with the goal of advancing drugs to be used in the radiotherapy cancer setting. Their lead drug is Avasopasem which is designed to reduce the incidence of SOM in patients with HNC. Oral mucositis is a side effect of radiation treatment. It is characterized by severe pain, inflammation, bleeding in the mouth, and ulcers in the mouth. There are no approved drugs for SOM. Current treatments are designed to address the symptoms, but not the underlying cause. SOM in HNC is an unmet medical need, which is important for understanding the potential for the drug to receive an NDA, market adoption & potential sales.

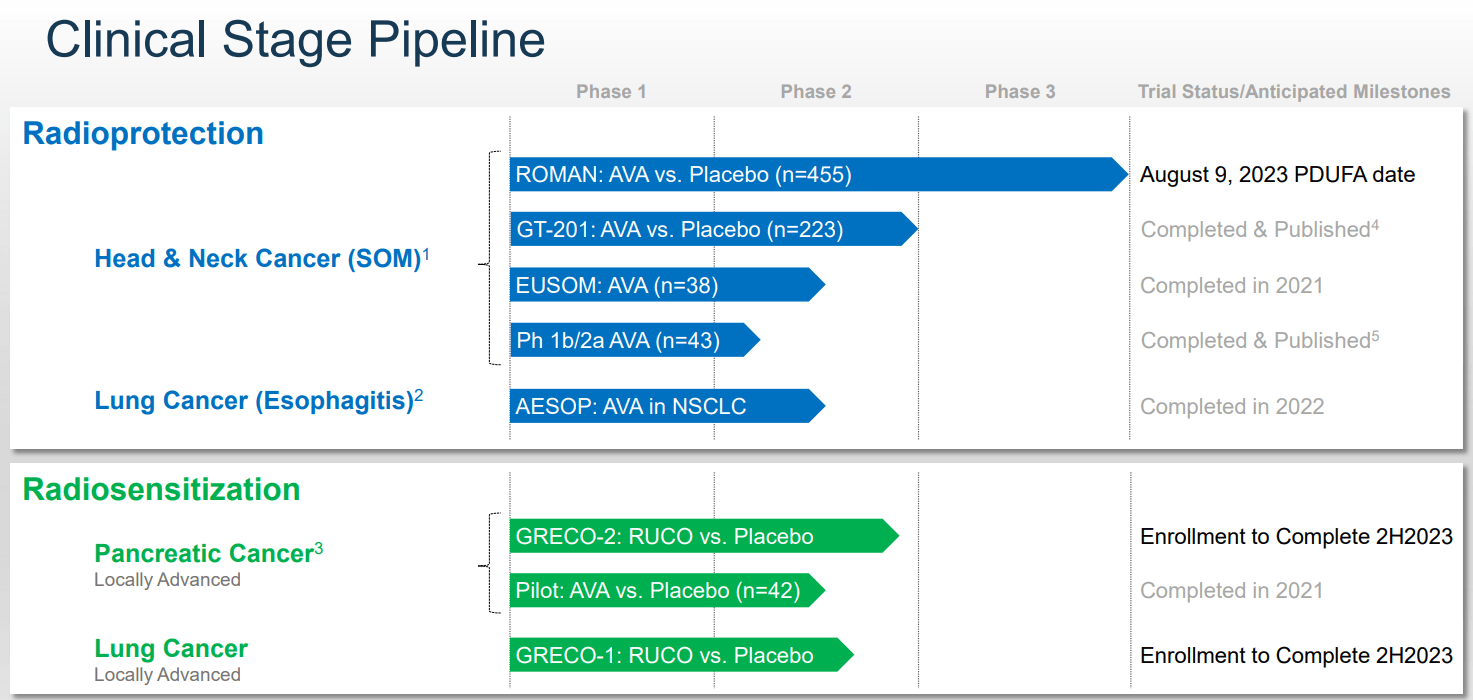

Below is a graphic from GRTX presentation on the pipeline along with anticipated milestones.

Clinical State Pipeline & Anticipated Milestone Dates (Company Presentation)

{kind=link}

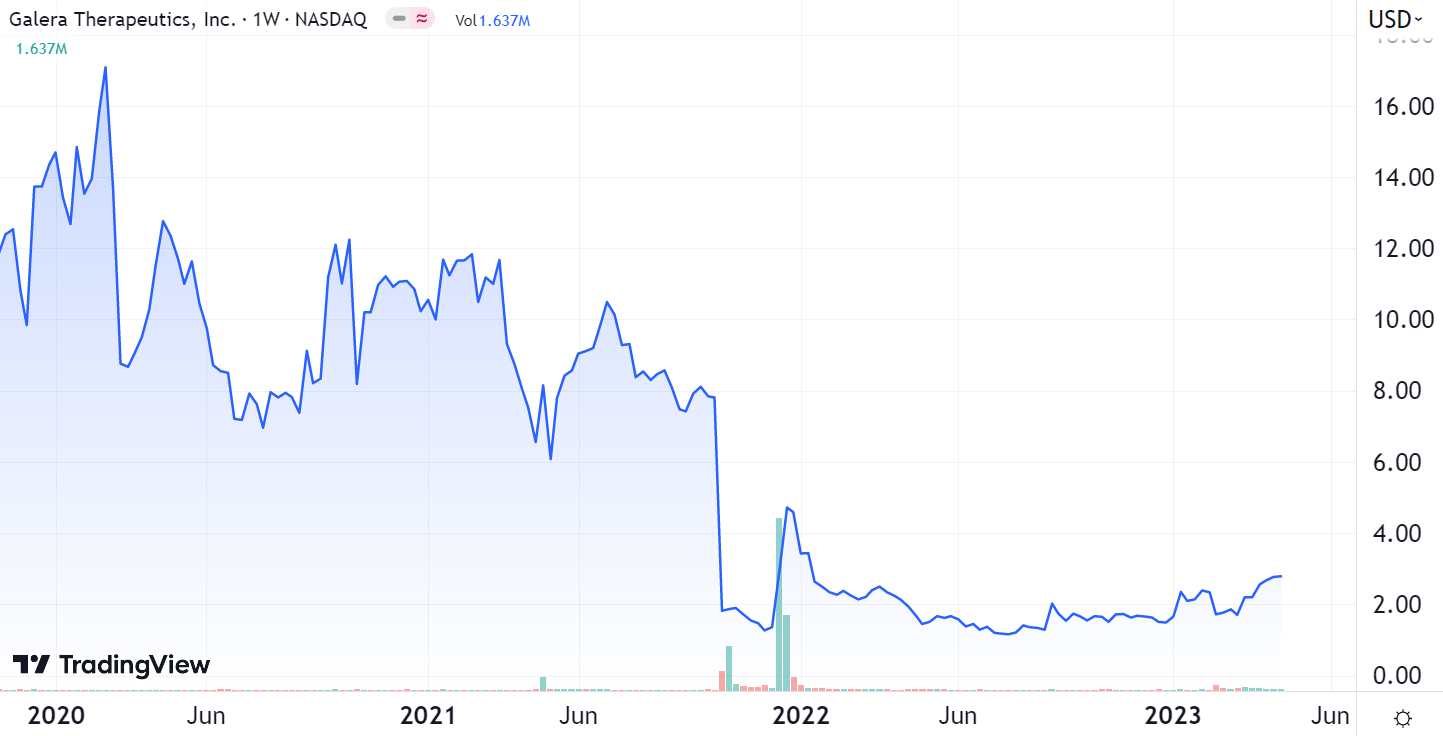

Share Price History

Below is a chart showing the share price history since GRTX IPO at the end of 2019.

As you can see, it hasn't been kind to early investors.

3.5 year share price chart (TradingView)

{kind=link}

But an extremely rare event happened in the last Quarter of 2021, which is shown by the U-shape in the chart. Understanding these events is key to de-risking our investment in GRTX.

In Oct 2021 the company reported that Avasopasem failed its 455 patient Phase 3 trial for SOM in HNC. This was devastating news and sent the share price down 70% in one day. The stock dropped from around $8 to less than $2 over the course of a week. And it kept dropping to around $1.25 at the end of November. This was a shock to management as the Phase 3 trial was designed very similar to their successful Phase 2b trial. The Phase 3 results were disconnected from the Phase 2b results so the company investigated. It didn't take long before they found a problem.

It turns out the clinical research organization (( CRO )) misinterpreted the results since there was an error in the statistical program. After fixing the error the company actually met its primary and a key secondary endpoint. After reporting correct results the share price rocketed over 100% to around $2.80 approximately 2 months after supposedly missing the endpoints. But the damage had been done. The company had good Phase 3 results, but a dismal share price due to the CRO error.

A CRO making a statistical reporting error is very rare. But when it happens, it can produce outsized returns for shareholders willing to take the risk.

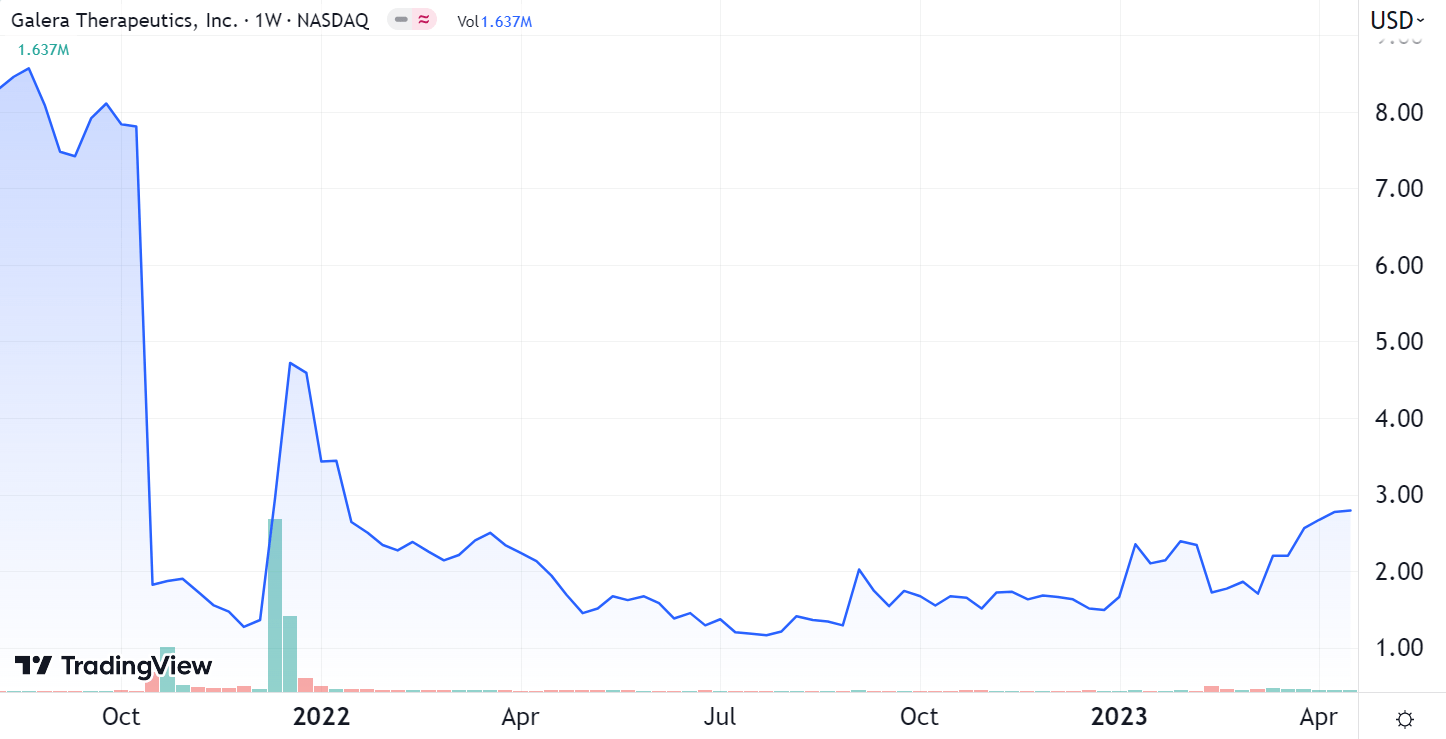

The Opportunity

Before erroneously reporting a failed trial, the share price was around $8. (See chart below.) Had GRTX reported a successful trial, we believe the share price would have risen due to SOM being an unmet medical need, the drug receiving breakthrough therapy designation (BTD) and Fast Track Designation from the FDA for the same indication. This would possibly have incentivized the company to quickly do a capital raise and fill their coffers at a much higher share price before applying for an NDA. Had this CRO error not occurred, we believe the share price should be hovering around $8-$10 this far out (~4 months) from its PDUFA date, in our estimation.

18-month share price chart (TradingView)

{kind=link}

Instead the share price now sits at slightly less than $3. Granted the share price has risen by 80% in the last 2 months, but we believe it has plenty of room to run.

As a bonus, on Feb 15, 2023, the company garnered Priority Review when it received notice from the FDA of acceptance of its Avasopasem NDA for SOM. This reduces the standard 10-month review time to around 6 months. In addition the FDA did not request an Adcom. The FDA requests an Adcom when there might be confusing data or potential safety issues discovered in the Phase 3 trial. All signs seem to be pointing to a favorable PDUFA decision from the FDA.

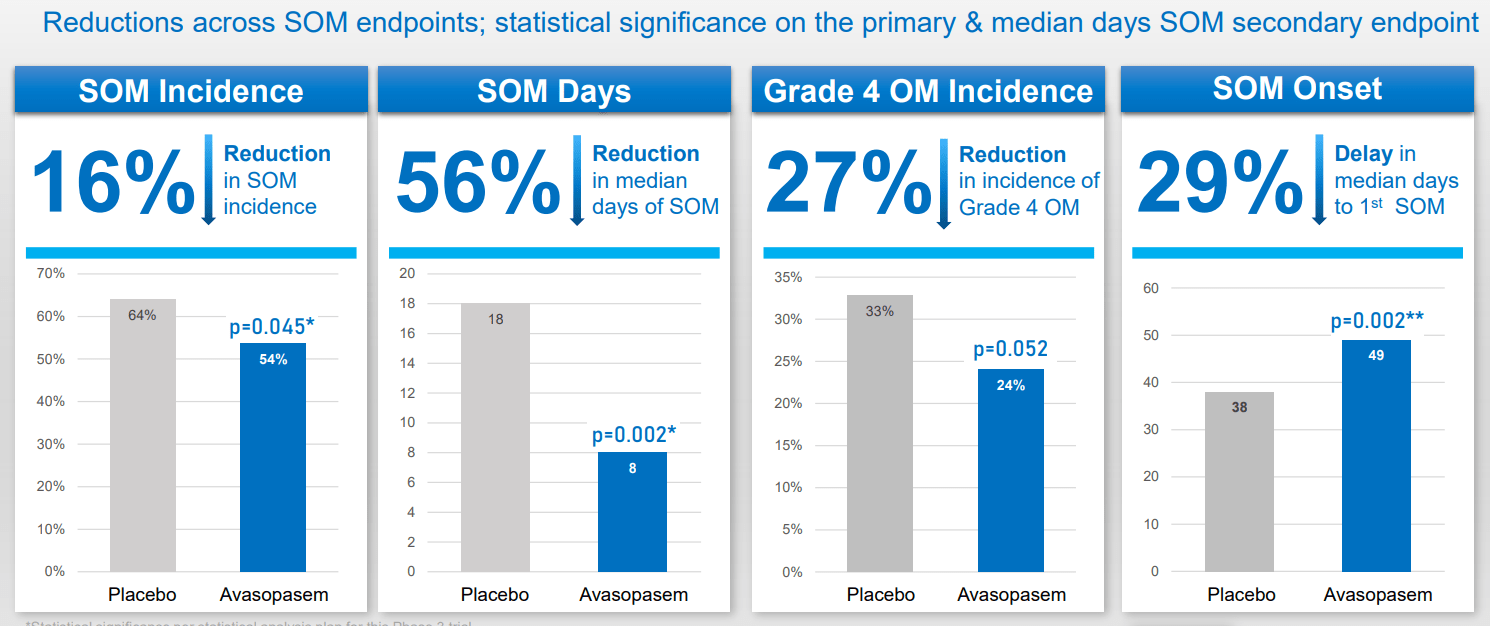

Phase 3 Results

As stated earlier the Phase 3 results met the primary and median days SOM secondary endpoint. Here is a summary of the trial endpoints as stated in the company PR on Dec 14, 2021.

-

16% relative reduction in the incidence of SOM in the Avasopasem treatment group (54%) vs. placebo group (64%) (p=0.045) (primary endpoint)

-

56% relative reduction in the number of days of SOM in the Avasopasem treatment group (8 days) vs. placebo group (18 days) (p=0.002*) (secondary endpoint)

-

27% relative reduction in the severity (incidence of Grade 4 OM) of SOM in the Avasopasem treatment group (24%) vs. placebo group (33%) (p=0.052) (secondary endpoint)

Below is a graphic of those endpoints and corresponding p-value.

Phase 3 Trial Results (TradingView)

{kind=link}

In summary Avasopasem reduced incidence, severity and duration of SOM for HNC patients. This should be welcome news for doctors who administer & patients who suffer from SOM, should the drug be approved.

Note that one of the secondary endpoints (Grade 4 OM Incidence Reduction) has a p-value of 0.052. This is above the 0.05 threshold the FDA needs to rule out a random result. However, we do not see this as being a blocking issue to receiving approval of the NDA, as long as there are no other issues.

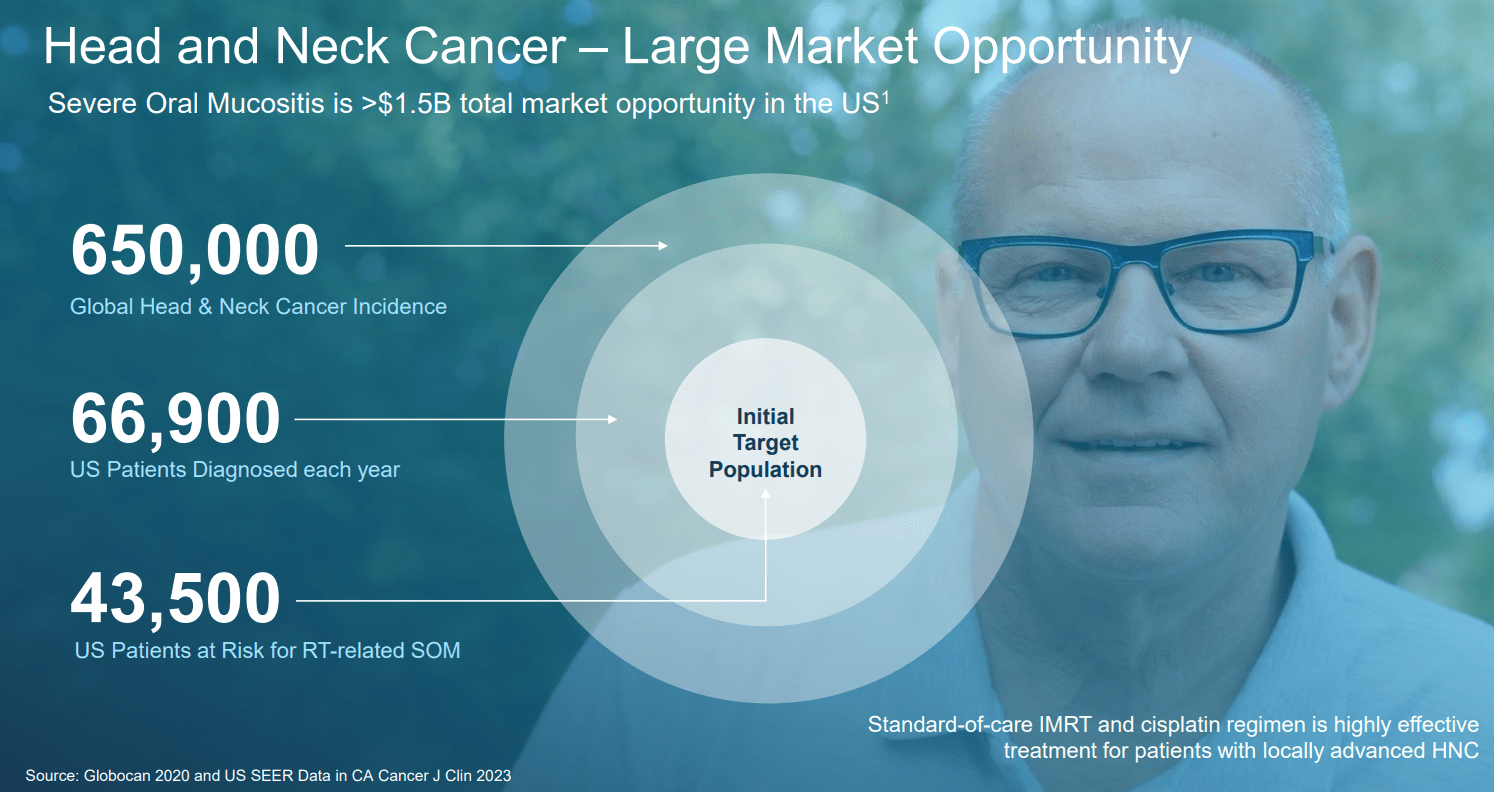

Total Addressable Market

The total addressable market for Avasopasem is large with 43,500 patients in the US. GRTX sees this as a billion dollar total market opportunity in the US alone.

Below is a graphic from the company presentation (Page 24).

HNC Total Addressable Market (Company Presentation)

{kind=link}

Also the company's recent 10K states that the five largest European countries have 68,000 people diagnosed annually with HNC, with an additional 28,000 in Japan. The company estimates that 65% of these patients (62,500 patients) will be treated with radiotherapy which makes them susceptible to SOM, and; therefore, potential candidates for Avasopasem treatment. The global SOM market for HNC is significant.

Cash

GRTX reported that they have ~$31M of cash, cash equivalents and short term investments as of Dec 31, 2022. On Feb 15, 2023 the company did a $30M secondary . This secondary included 14.3M warrants with an exercise price of $1.97/share. These warrants are now in the money and when exercised will add additional cash to their coffers. They are burning through cash at a rate of about $15M per quarter . When you subtract the spending from available cash, their cash should last until Dec 2023.

According to the 10K, the company stated "we believe that our existing cash, cash equivalents and short-term investments as of December 31, 2022, together with the net proceeds from our February 2023 registered direct offering, will be sufficient to enable us to fund our operating expenses and capital expenditure requirements into the fourth quarter of 2023".

This is good news as the PDUFA date is Aug 9, 2023. However, do not be surprised if the company chooses to do another secondary before the PDUFA date. Companies are in constant need of funds and never want to get too close to zero before doing a secondary.

Risks

The biggest risk is that the FDA rejects approval of Avasopasem and replies with a complete response letter . This event would send the share price crashing as it would result in another 12-18 months to fix deficiencies in the application and reapply. This assumes that the deficiencies are fixable. In this scenario the company would be forced to do multiple secondary raises resulting in significant dilution until another NDA can be filed. It would be doing this while the share price would be hovering around $1, in our estimation.

We see this non-approval scenario as unlikely since the Phase 3 trial achieved the primary, and a key secondary endpoint, and there were no safety issues. In addition the FDA did not request an Adcom. Lastly the FDA gave priority review upon application acceptance signifying the FDA sees the value of this drug on the market as quickly as possible.

Another risk is the FDA needing more time to review the Avasopasem application. This would also hurt the share price b/c it would nearly guarantee a secondary raise is needed before hearing back from the FDA again. If the FDA says they need more time, we may take some profits off the table.

Another risk is that a capital raise is needed before the upcoming PDUFA date. Even though the company has cash to fund operations through the end of the year, we see a capital raise as a remote possibility since clinical biotech companies often raise funds several months before they need it. This is not a risk to BLA acceptance/denial, but can put downward pressure on the share price since the secondary offering price is often lower than the current share price. In addition, it results in dilution which investors don't like.

Conclusion

GRTX share price is still recovering from the CRO erroneously reporting the company did not hit their primary and secondary end points in Sept 2021. They did, in fact, hit the primary endpoint and a key secondary endpoint for their novel drug for the SOM market. The company has a PDUFA date In August 2023, which will be a significant catalyst if their NDA is approved. Since SOM is a potential billion dollar market, we expect the share price to continue to gradually rise as the PDUFA date approaches.

For further details see:

Galera Therapeutics: A Possible Solution To Severe Oral Mucositis In Head And Neck Cancer Patients