GAU - Galiano Gold: More Solid Results In Q2

2023-08-14 04:54:24 ET

Summary

- Galiano Gold surprised with another quarter of solid results and raised its FY2023 production guidance.

- And while costs will increase in H2 on the back of elevated sustaining capital, 2024 will be a much better year, with AISC set to improve further post-2024.

- Given the company's ability to over-deliver on promises and its very reasonable valuation, I see GAU stock as a Speculative Buy below US$0.52.

It's been a mediocre Q2 Earnings Season with the Gold Miners Index ( GDX ) down over 5% since it began last month, and suffering a drawdown of nearly 10% at last week's lows. The mixed results can be attributed to one-time headwinds in some instances (severe weather, power outages, ongoing strike) but also to rising costs, even if inflationary pressures have eased a little from the double-digit inflation experienced last year. Unfortunately, this resulted in limited benefit from record gold prices from a margin standpoint, and some names like Coeur ( CDE ) saw even less benefit given that a portion of their gold production goes to streams (Palmarejo) or hedges. However, Galiano Gold ( GAU ) was one company that surprised yet again to the upside again in Q2, and has raised guidance for FY2023. Let's take a closer look below:

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

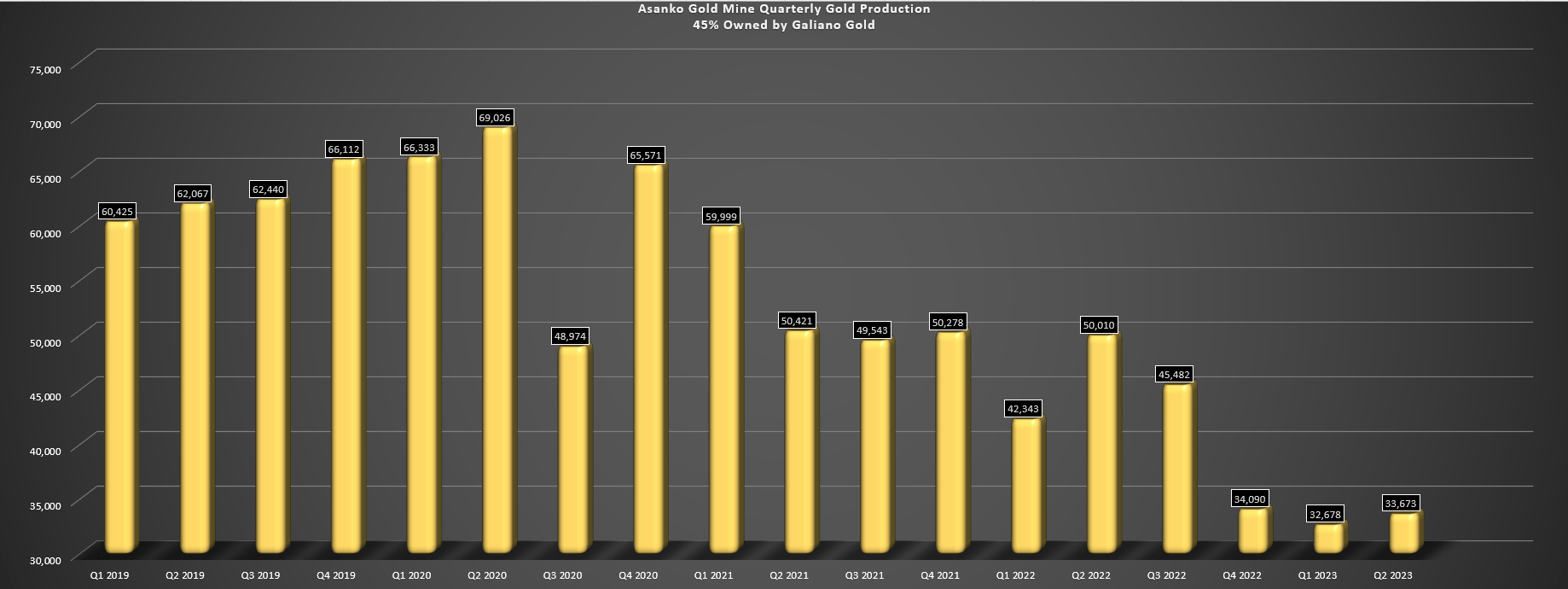

Galiano Gold released its Q2 results this week, reporting quarterly production of ~33,700 ounces of gold, a sharp decline from the year-ago period. However, this decline in production was above planned levels (~66,400 ounces produced year-to-date), and the lower production can be attributed to the processing of stockpiles with no ore tonnes mined. This is because the company was busy with a competitive tender process to award a new mining contract during the quarter, with this completed and a new mining contractor being selected by Gold Fields ( GFI ) and Galiano (partners at the Asanko Gold Mine). Assuming things go according to plan, mining will begin at Abore in Q4 of this year, with a major step up in feed grades without reliance on solely lower-grade stockpiles.

Asanko Gold Mine - Quarterly Gold Production (100% Basis) (Company Filings, Author's Chart)

{kind=link}

Looking at the above chart, investors may be a little alarmed by the production results, but it's important to note that it's been a year and a half of transition for the Asanko Gold Mine. This is because the mine saw alarmingly low recoveries from the Esaase deposit in Q1 2022, and increased gold grades were detected in tailings product leaving the facility. The negative news prompted Galiano to complete metallurgical test work and the company also worked to prepare a new resource/reserve estimate, with a new TR released earlier this year. Finally, mining was temporarily stopped last year, which has obviously affected production levels with a reliance on stockpiles vs. 1.0+ gram per tonne ore. Hence, the past three quarters are not indicative of the mine's actual production profile, and we should see a return to more normal production levels in 2024.

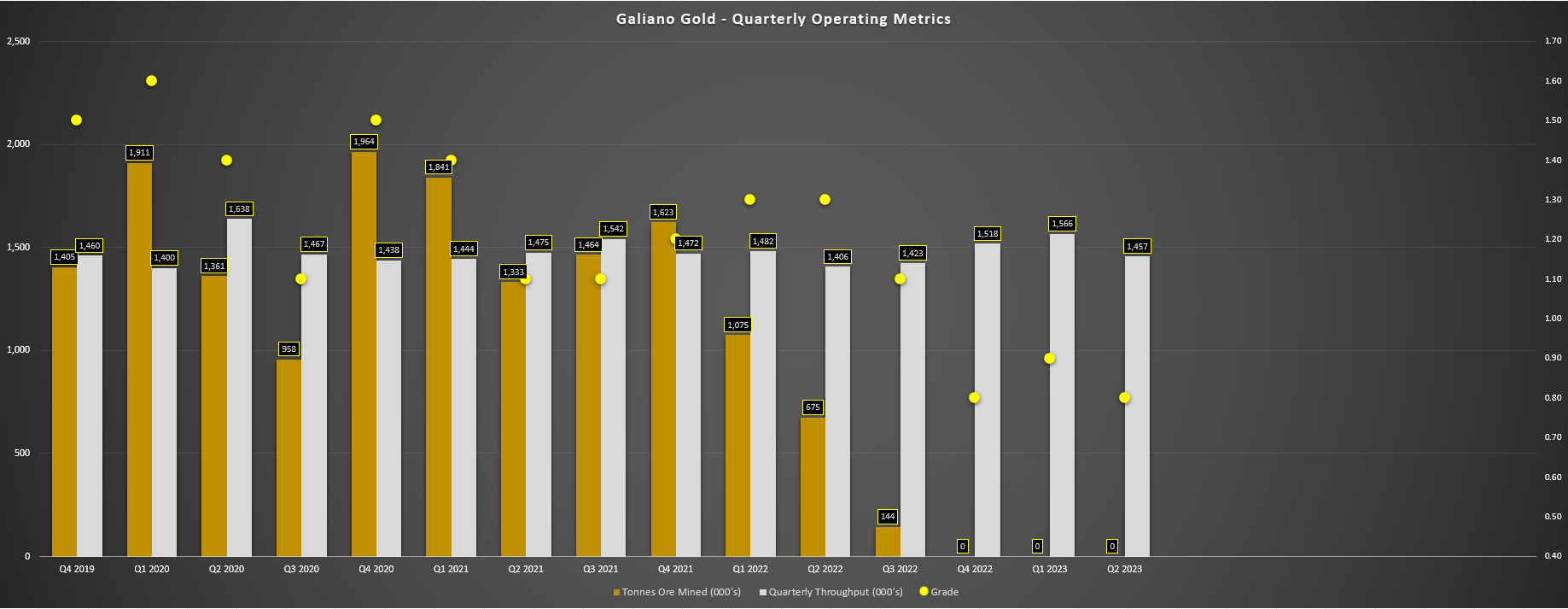

Asanko Gold Mine - Tonnes Mined, Throughput & Feed Grade (Company Filings, Author's Chart)

{kind=link}

Despite no mining being completed in Q2 2023 (with it set to start in Q4 as communicated earlier this year), Galiano Gold processed ~1.46 million tonnes at 0.80 grams per tonne of gold at an 85% recovery rate. This throughput rate was up slightly from the year-ago period, but down on a full year basis because of the impact of lower grades (reliance on stockpiles vs. ore from the Akwasiso Pit). Fortunately, the near record gold price ($1,944/oz) in the period helped to pick up some of the slack. Hence, revenues were down less than expected at $64.1 million (Q2 2022: $84.9 million), and production is tracking well ahead of plans, sitting at ~57.7% of its guidance mid-point (115,000 ounces).

Given the impressive operating results year-to-date, Galiano has revised its guidance higher by ~9% at the mid-point, increasing its FY2023 outlook from 115,000 ounces to 125,000 ounces. And assuming the company is able to deliver on this, it will be the second year in a row of guidance beats for the company under its new CEO, Matt Badylak, an impressive feat. And while costs will remain elevated in 2023, they would be much lower if not for the increase in planned sustaining capital flagged in the Q2 report. That said, while H2 will be higher-cost from an operating cost standpoint, we will see a significant improvement in costs in 2024 and post-2024 once production levels increase and the company gets past this year of elevated sustaining capital ($43 million this year alone excluding sustaining stripping costs vs. ~$100 million over life of mine).

Costs & Margins

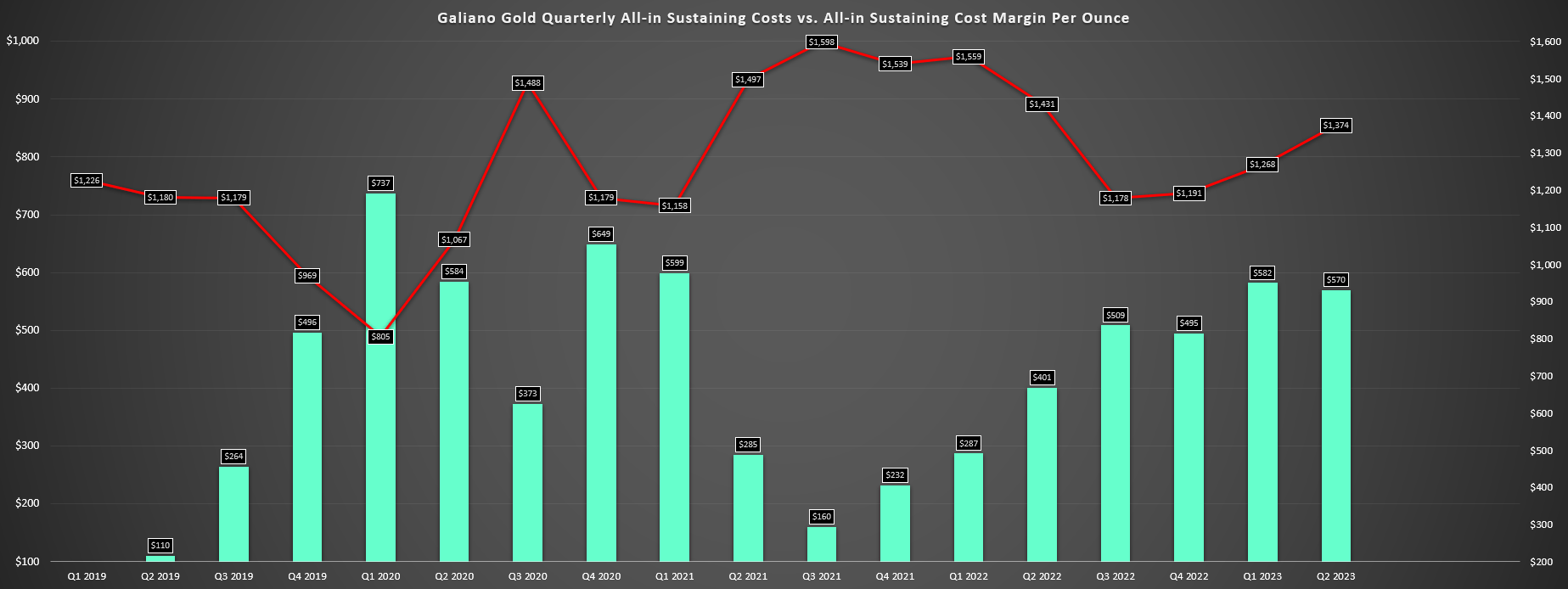

Moving over to costs and margins, Galiano Gold reported all-in sustaining costs of $1,374/oz in Q2 2023, an improvement from the $1,431/oz costs in the year-ago period. The company noted that it continues to work to identify additional optimization opportunities (workforce was rationalized last year leading to cost savings), in hopes to further reduce operating costs, and noted that the mining fleet at Abore and Miradani North will utilize 100-ton haul trucks vs. the 40 ton CAT 740's that were previously expected to be used in the 2023 TR. In other positive news, the sector continues to see low single-digit inflation, but many producers have reporting an easing of inflationary pressures, a positive sign for Galiano which is a mid-cost miner and sensitive to changes in the gold price (LOM AISC: ~$1,200/oz when adjusting for inflationary pressures).

Galiano Gold - Quarterly AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

Given the higher gold price in the period and solid cost controls, Galiano reported improved all-in sustaining cost margins of $570/oz, a 43% increase from the year-ago period. This partially benefited from being up against easy year-over-year comps with a much lower gold price in Q2 2022 ($1,832/oz), but this was still a solid result with AISC margins coming in near the industry average (~$600/oz) despite the Asanko Gold Mine not operating at anywhere near its potential (reliance on stockpiles). As for its financial results, the mine generated $18.0 million in operating cash flow on a 100% basis ($10.1 million in free cash flow), and Galiano exited the period with ~$55 million in cash, making it one of the more well financed junior producers.

Valuation

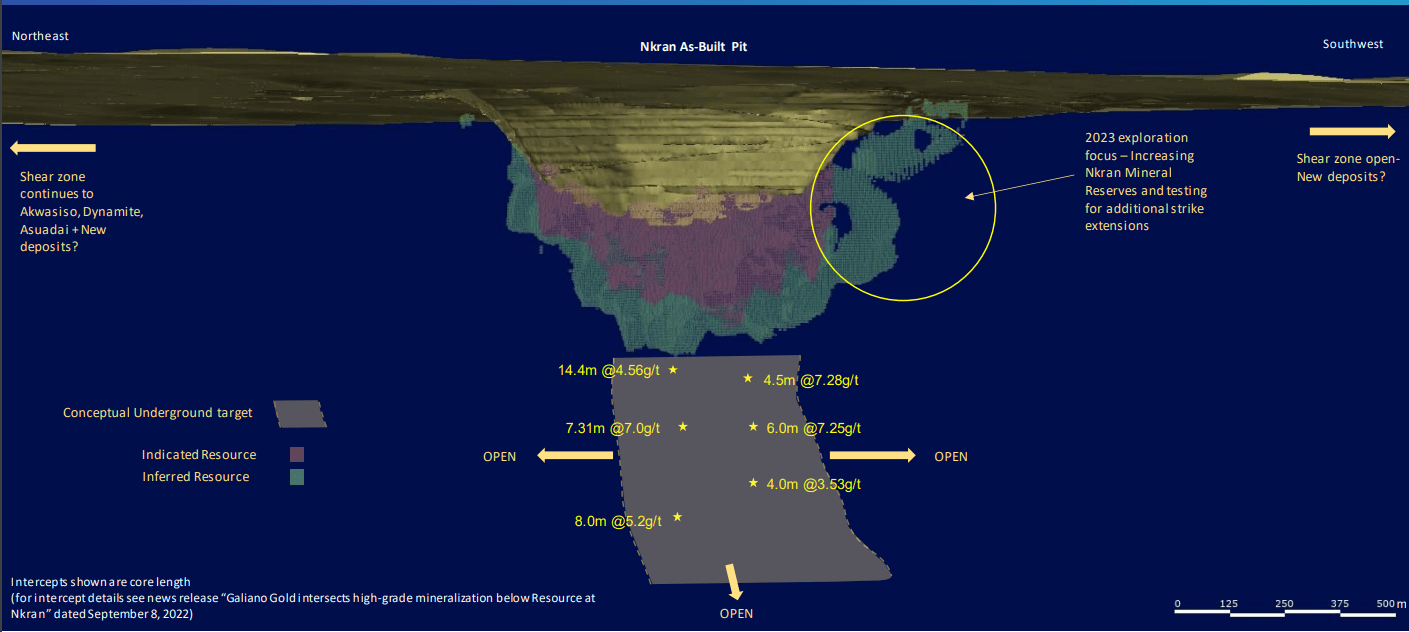

Based on ~238 million fully diluted shares and a share price of US$0.63, Galiano Gold trades at a market cap of ~$150 million. This is a very reasonable valuation for a company with 45% ownership of a ~220,000-ounce gold mine in Ghana with a greenfields project on the neighboring Sefwi Gold Belt, home to Newmont's ( NEM ) massive Ahafo Mine (and in-construction Ahafo North Project) and the Chirano Mine previously owned by Kinross ( KGC ) and Red Back Mining. In fact, if we compare Galiano's market cap to the estimated After-Tax NPV (5%) at the Asanko Gold Mine of ~$450 million ($1,825/oz gold) which bakes in inflationary pressures, the company would appear to be significantly undervalued, especially if upside can be surfaced from underground targets existing pits, with impressive hits from its higher-grade Nkran deposit at depth.

Nkran - Drilling Highlights (Company Presentation)

{kind=link}

That said, it's important to remember that Galiano Gold has a 45% interest in the asset, equating to ~$202 million in value vs. the estimated After-Tax NPV (5%) of ~$450 million. Meanwhile, even diversified West African producers with scale like Endeavour Mining ( OTCQX:EDVMF ) and Perseus Mining ( OTCPK:PMNXF ) typically trade at less than 0.90x P/NAV, suggesting small-scale single-asset producers like Galiano (~100,000 attributable ounces per annum) should trade at 0.80x P/NAV or less. After adjusting for this discount and adding $60 million in exploration upside [$0.25], I see a fair value for Galiano Gold of $222 million [$0.93]. This points to a 48% upside from current levels, suggesting meaningful undervaluation today despite the stock's outperformance year-to-date.

Although this points to a meaningful upside to fair value, I am looking for a minimum 45% discount to fair value for buying micro-cap names, and especially those operating in Tier-3 ranked jurisdictions. The reason is that single-asset producers carry higher risk if anything negative occurs to sideline operations temporarily or indefinitely because of their one mine being their only source of cash flow. In addition, micro-cap stocks ($250 million or lower) are far more volatile and have less institutional support, leading to sharp drawdowns if one doesn't buy them correctly, an additional risk from a trading standpoint. If we apply this discount to Galiano's estimated fair value of US$0.93, this translates to a low-risk buy zone of US$0.52 or lower. Obviously, this doesn't mean that the stock must drop to this level, but I prefer to pay the right price or pass entirely in a sector where many things can go wrong even with solid management at the helm.

Summary

Galiano Gold had another solid quarter in Q2 and has done a much better job of delivering on promises since new CEO Matt Badylak took over as CEO in mid-2021 after previously spending time as COO and in roles such as GM at Kisladag, and Director of Operational Support at Eldorado Gold ( EGO ). Given the company's solid execution to date under new management, Galiano has morphed into one name that can be trusted among the junior producer group and a name that can be bought on sharp pullbacks. That said, with negative sentiment surrounding African weighing on West African miners and Galiano not being in a low-risk buy zone yet, I don't see the reward/risk being attractive enough to pay up for the stock at US$0.64. So, given that I continue to see larger margins of safety elsewhere in the sector, I remain on the sidelines for now with GAU.

For further details see:

Galiano Gold: More Solid Results In Q2