GAU - Galiano Gold: Reserves Reinstated And Cost Guidance Lowered

2023-05-26 01:57:28 ET

Summary

- Galiano Gold released its Q1 results earlier this month, reporting quarterly production of ~32,700 ounces of gold, a 23% decline from the year-ago period.

- However, this was an unusual quarter with a reliance on low-grade stockpiles, but despite the lower grades and recoveries, the AGM reported positive free cash flow in the period.

- Fortunately, 2024 should be a much better year as mining begins at Abore and Miradani North (Q4 2023, Q2 2024), with a return to a ~150,000+ ounce production profile.

- That said, while Galiano is doing a solid job of under-promising and over-delivering and the reinstatement of reserves has de-risked the story, I continue to see more attractive bets elsewhere in the sector.

The Q1 Earnings Season for the precious metals sector is nearly over and one of the first companies to report its results was Galiano Gold ( GAU ). And while several junior producers limped into the year with a disappointing performance like Americas Gold and Silver ( USAS ), Jaguar Mining ( OTCQX:JAGGF ), and Avino Silver & Gold ( ASM ), Galiano Gold had another solid quarter, continuing its trend of under-promising and over-delivering. Production of ~32,700 ounces evidenced this, which is tracking at ~30% of annual guidance and the company also lowered its cost guidance to $1,700/oz (down 12% at the mid-point), setting the company up for a better year as it prepares to mine its Abore deposit before year-end. Let's take a closer look at the Q1 results below.

{kind=link}

All figures are in United States Dollars unless otherwise noted. Production figures and financial metrics are on a 100% basis for the Asanko Gold Mine [AGM] where Galiano Gold holds a 45% interest, unless otherwise noted.

Q1 Production & Sales

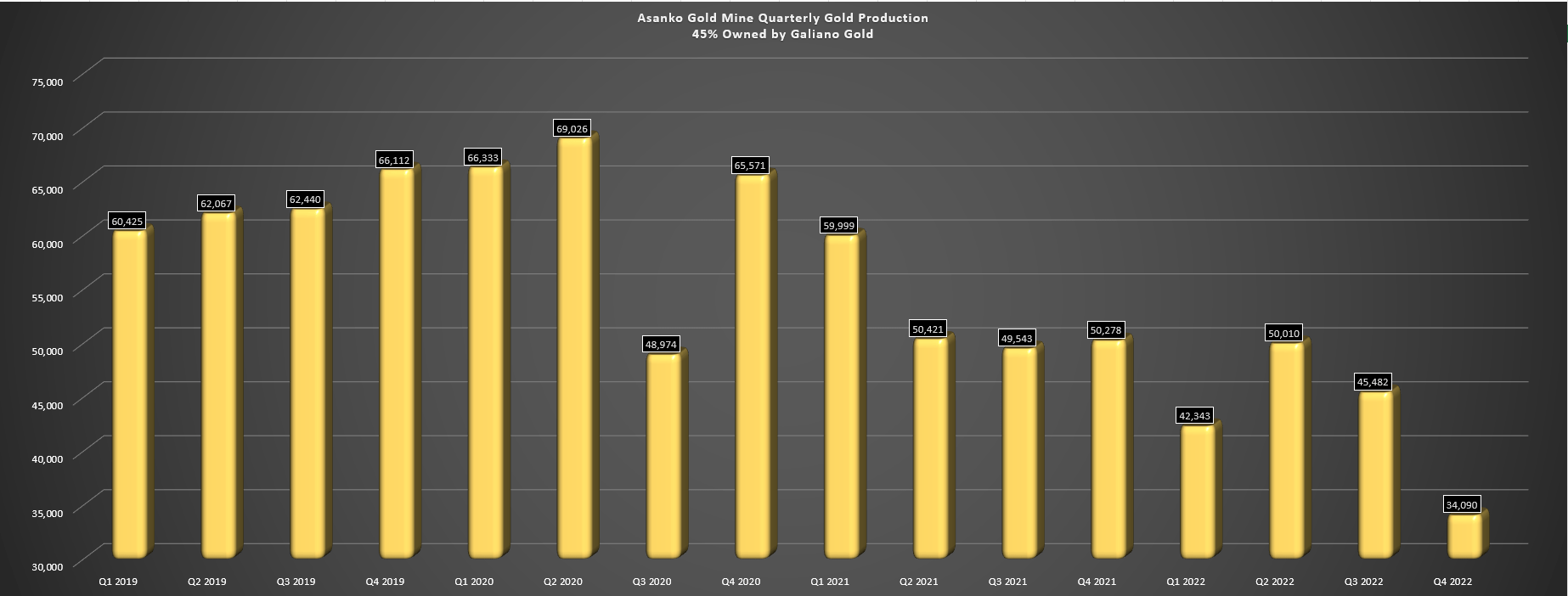

Galiano Gold ("Galiano") released its Q1 results earlier this month, reporting quarterly production from its Asanko Gold Mine of ~32,700 ounces (~14,700 ounces attributable), a sharp decline from the year-ago period where output came in at ~42,300 ounces. However, while this may have appeared to be an alarming drop, it's important to note that the two periods were not comparable, with current activities focused on stripping with no ore mined in the period, resulting in the mill relying on low-grade stockpiles. Hence, while mill throughput was higher at ~1.57 million tonnes, grades and recoveries more than offset the increased tonnes processed. The result was a 23% decline in production, and a significant decrease in revenue to $65.1 million (Q1 2022: $77.5 million).

Asanko Gold Mine - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

While the lower production and sales translated to lower revenue in the period despite a slightly higher gold price, it's important to note that this was expected based on a guidance midpoint of 110,000 ounces for FY2023. And while FY2023 will be a weaker year for the mine, annual production is expected to return to 200,000+ ounces (100% basis) starting in 2025 with a steady stream of mid-grade ore from Abore and Miradani North. However, despite the lower sales volumes, inflationary pressures year-over-year on some consumables/reagents and combination of lower grades and higher throughput, costs were actually down year-over-year, and the mine was free cash flow positive, reporting free cash flow of $12.0 million in Q1 2022: cash outflow of $3.4 million).

Costs & Margins

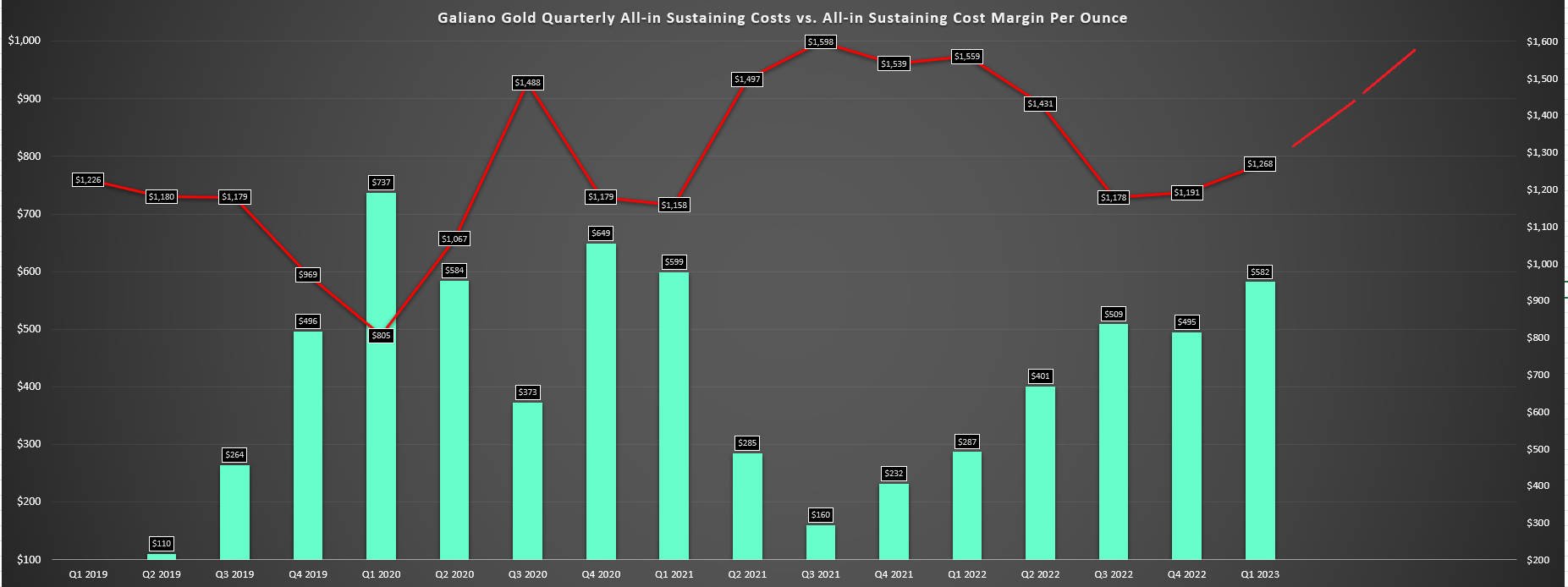

Digging into costs and margins, all-in sustaining costs came in below my estimates in Q1 at $1,268/oz, a significant decline year-over-year with the benefit of reduced labor costs from a rationalization of the workforce, no mining costs because of no ore being mined in the period, and despite inflationary pressures experienced sector-wide. This helped the mine to report significantly improved AISC margins of $582/oz (up 103% year-over-year), with a higher average realized gold price of $1,850/oz and ~19% lower costs. That said, sustaining capital came in at just ~$4.9 million in Q1 and is tracking at just ~13% of planned sustaining capital expenditures given the busy year ahead (Stage 7 TSF lift, plant infrastructure, and water management). So, while Q1 AISC was well below the guidance range, I would expect significantly higher costs and weaker margins in the upcoming quarters.

Galiano Gold - Quarterly AISC & AISC Margins (Company Filings, Author's Chart & Estimates)

{kind=link}

This isn't an issue from a long-term standpoint, but from a margin standpoint, I don't expect the higher gold price in Q2 to be much help relative to the higher sustaining capital, and I would expect to see AISC margins decline sharply sequentially (Q2 vs. Q1) to below $425/oz. Unfortunately, this should persist throughout the year, especially with production tracking well ahead of guidance and sustaining capital miles tracking well below budgeted spending. Therefore, I wouldn't expect a repeat of the strong Q1 results, which benefited from above-average production, suggesting that those investors that are banking on similar results in Q2 and Q3 are likely to be disappointed, even if the company can beat output guidance again this year because of the solid start to 2023.

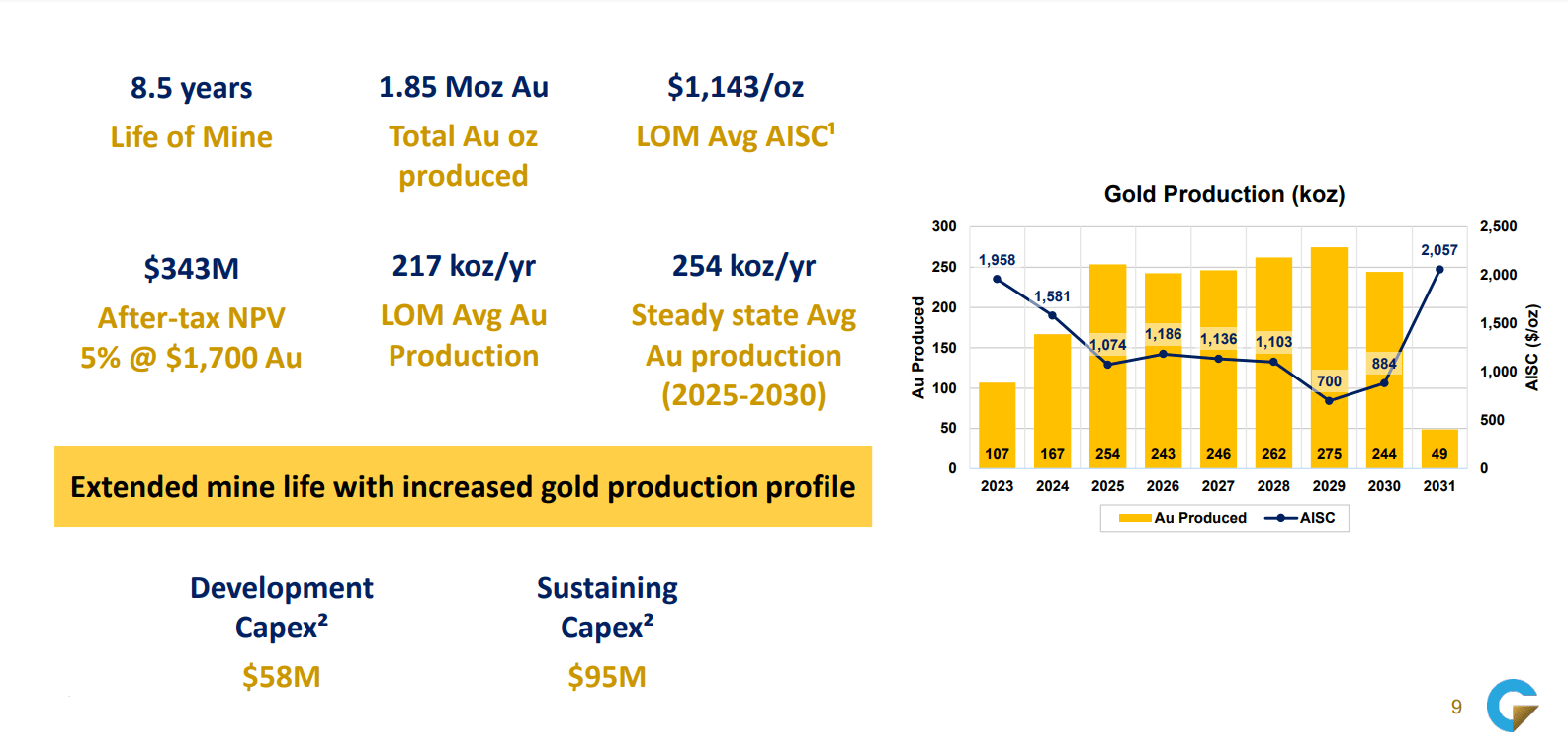

AGM - Updated Technical Report (Company Website)

{kind=link}

So, what's the good news?

Galiano Gold restated its reserves earlier this year and released an updated Technical Report, with its new mine plan having an 8-year mine life, with average production of ~217,000 ounces (~97,000 attributable ounces) at all-in sustaining costs of $1,143/oz. These costs are well below the current industry average of $1,300/oz and operating costs are expected to decline materially starting next year, with AISC expected to average just ~$1,014/oz from 2025 to 2030. So, while 2023 and 2024 will be much higher costs with lower free cash flow generation, Galiano will be back to pre-COVID-19 like production and cost levels by 2025, and the After-Tax NPV (5%) for the project stands at $343 million even using a conservative gold price. Plus, there looks to be upside to this figure and potential mine life extensions with high-grade intercepts below the Nkran Pit and the potential to head underground.

To summarize, with a new mine plan and the metallurgical worries resolved, the Galiano Gold thesis has been de-risked, and the company is well-funded to aggressively drill targets on its shared Asanko tenements, as well as its Asamura Project on the Sefwi Gold Belt southwest of Newmont's massive Ahafo Gold Mine. Hence, investors should be able to look forward to a steady stream of drill results from both projects this year, even if this won't be a year to write home about from a production and cost standpoint while the company churns through low-grade stockpiles and works on stripping at the Abore Pit. Let's take a look and see if the stock is offering an adequate margin of safety following its recent 20% correction.

Valuation & Technical Picture

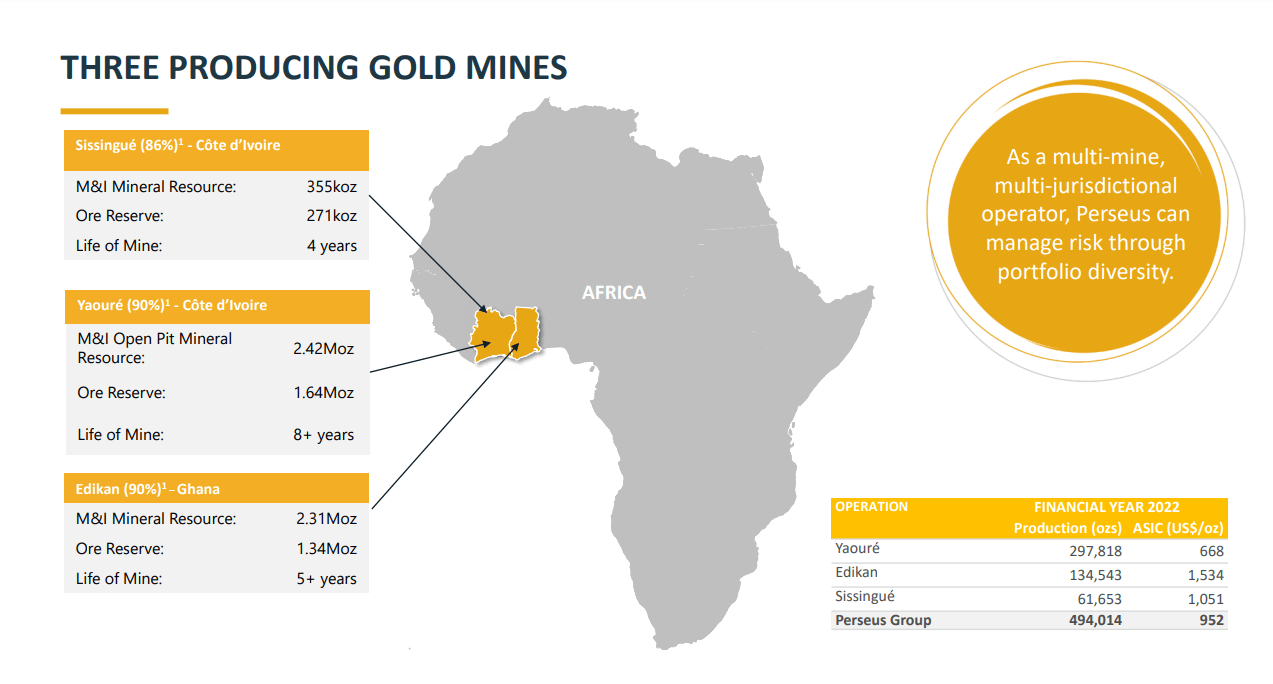

Based on ~238 million fully diluted shares and a share price of US$0.59, Galiano trades at a market cap of $140 million, making it one of the lowest-valued junior gold producers. However, while this may pale compared to the Asanko Gold Mine's After Tax NPV (5%) of ~$439 million at an $1,800/oz gold price, it's important to note that Galiano's ownership of this asset is 45% (attributable valuation: ~$198 million). And while some investors might believe that Galiano Gold should trade at 1.0x P/NAV, I don't see this as realistic, with single-asset producers with sub 100,000-ounce production profiles in Tier-3 ranked jurisdictions typically trading below 0.80x P/NAV. In fact, Perseus Mining ( OTCPK:PMNXF ) is a multi-asset producer operating out of Ghana/Cote d'Ivoire with lower operating costs than Galiano and regularly trades below 0.90x P/NAV, and so does Endeavour ( OTCQX:EDVMF ), a senior producer.

Perseus Mining - Production Profile & Costs (Perseus Mining Presentation)

{kind=link}

Using what I believe to be a conservative multiple of 0.80x for Galiano Gold, this translates to a fair value of ~$158 million. And if we add $60 million in combined value for the company's 100% Asamura Project and exploration upside at Nkran Deeps, this translates to a fair value of $218 million. If we divide this figure by 238 million fully diluted shares, this points to a fair value for Galiano of US$0.91. From a current share price of US$0.59, this points to a 53% upside from current levels, which might suggest the stock is a Buy. However, for micro-cap companies, I want a minimum 45% discount to fair value to justify starting new positions to account for the higher risk. So, while GAU may be undervalued, the stock would need to decline below US$0.51 to move into a low-risk buy zone.

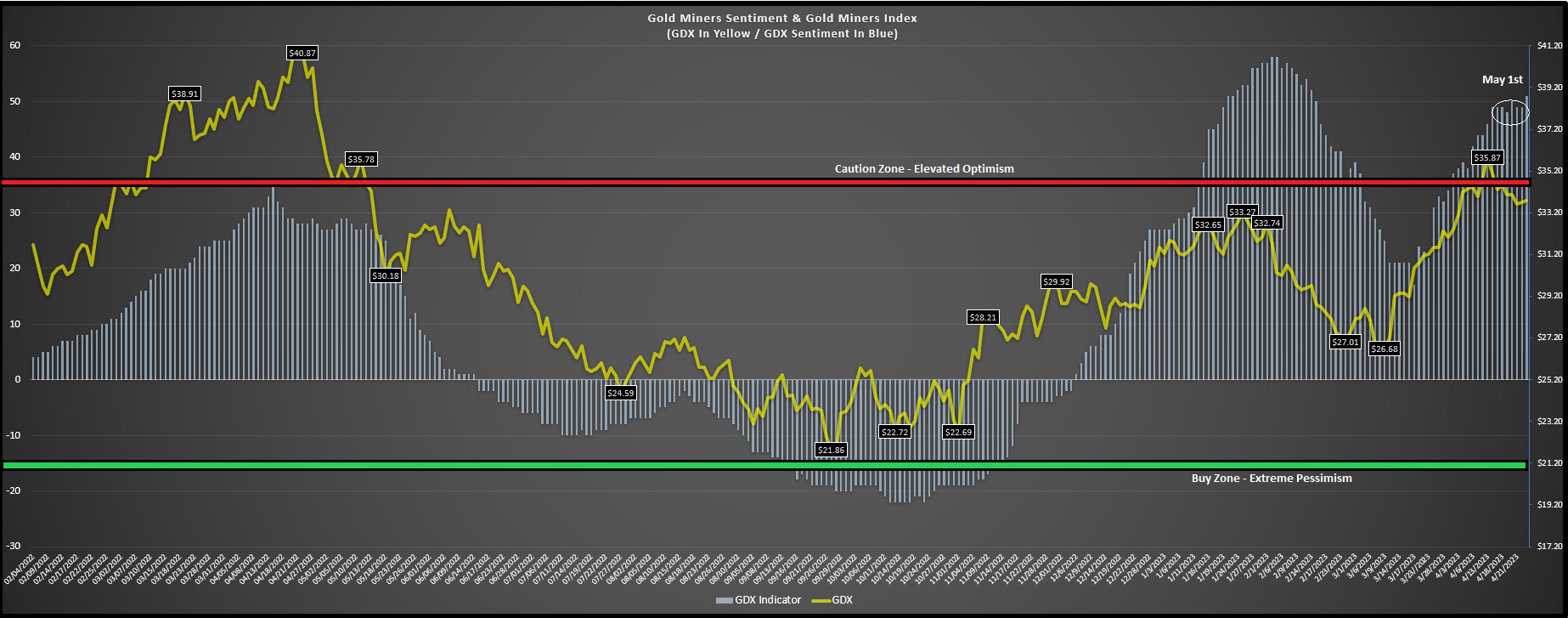

Gold Miners Sentiment - April 2022 to April 2023 (Author's Data & Chart )

{kind=link}

While a pullback of this magnitude may not occur and waiting for these levels could result in a missed opportunity, I do not believe in paying up for micro-cap stocks, and if I'm going to invest in these names, I want the right price or prefer to pass entirely. And from a sentiment standpoint, it's hard to rule out further weakness in the Gold Juniors Index ( GDXJ ) with sentiment moving to levels of elevated optimism earlier this month, which typically leads to a minimum 20% correction in the GDXJ (current correction: 14%). So, with GAU trading well above its next support level of US$0.49 and optimism significantly outweighing pessimism sector-wide, I see patience as the best course of action, and I would need to see lower prices to become interested in GAU as an investment.

Summary

Galiano Gold is tracking ahead of its FY2023 guidance and recently lowered cost guidance substantially, continuing a pattern that began since its new CEO Matt Badylak took over where it guides conservatively and over-delivers on promises. And while this will be a high-cost year with mostly low-grade stockpiles being fed to the plant, the higher gold price has certainly helped, and Galiano is set up for a solid 2024 if the yellow metal can hold on to its gains. That said, while GAU is undervalued, I continue to see more attractive bets elsewhere in the sector, and I don't see enough margin of safety. So, while I would view pullbacks below US$0.51 as buying opportunities, I have no plans to go long just yet.

For further details see:

Galiano Gold: Reserves Reinstated And Cost Guidance Lowered