ACRFF - Gambit

2023-09-19 16:01:14 ET

Summary

- Rising oil prices and commodity prices are causing inflationary pressures.

- The US is experiencing a shortage of diesel and crude stockpiles, leading to rising prices.

- The monetary regime may be changing, with a shift away from US Treasuries and towards gold and commodities.

“In poker, you want to play the weaker guys. In chess, it's the opposite” - Hikaru Nakamura

Looking at the most recent CPI print in the US coming at 3.7% in August from 3.2% in July and in conjunction with oil up by 35% in just three months with the US having drawn significantly on their strategic petroleum reserves when it came to selecting our title analogy and given our fondness for “chess game” analogies on many of our past musings, we decided to go for “Gambit”. A “Gambit” (from Italian gambetto, the act of tripping someone with the leg to make them fall) is a chess opening in which a player sacrifices material with the aim of achieving a subsequent positional advantage. As well it is also used to describe similar tactics used by politicians in a struggle with rivals in their respective fields, such as the US bans on semiconductor chips with the intention of crippling China's technology advance. This “Gambit” is starting in earnest to backfire on the likes of technology giant Apple, given its rival Huawei has risen like a phoenix with its new 7nm chips in its popular Mate 60 pro mobile phone. While in the game of chess, the broader sense of "opening move meant to gain advantage" and was first recorded in English in 1855. Gambits are said to be sound if it is capable of procuring adequate concessions from the opponent and as such there needs to be three general criteria to judge the soundness of a “Gambit”:

- Time gain: the player accepting the gambit must take time to procure the sacrificed material and possibly must use more time to reorganize their pieces after the material is taken.

- Generation of differential activity: often a player accepting a gambit will decentralize their pieces or pawns and their poorly placed pieces will allow the gambiteer to place their own pieces and pawns on squares that might otherwise have been inaccessible.

- Generation of positional weaknesses: finally, accepting a gambit may lead to a compromised pawn structure, holes or other positional deficiencies.

One can opine that the sacrifice of the strategic reserves of the United States ((SPR)) dipping below 800 million barrels, a level once seen in 1985, moving from a record 92-day supply three years ago to a 46-day supply low is akin to a “political gambit” and in terms of “soundness” is not only procuring zero time gain but, also leading to a positional weaknes s in light of the latest oil production cuts of both Saudi Arabia and Russia, but we ramble again.

In this conversation we would like to look at the inflationary implications of the significant rise in oil prices as well as the message coming from the significant rise of soft commodities from a “monetary” perspective.

Oil “Gambit” and inflation

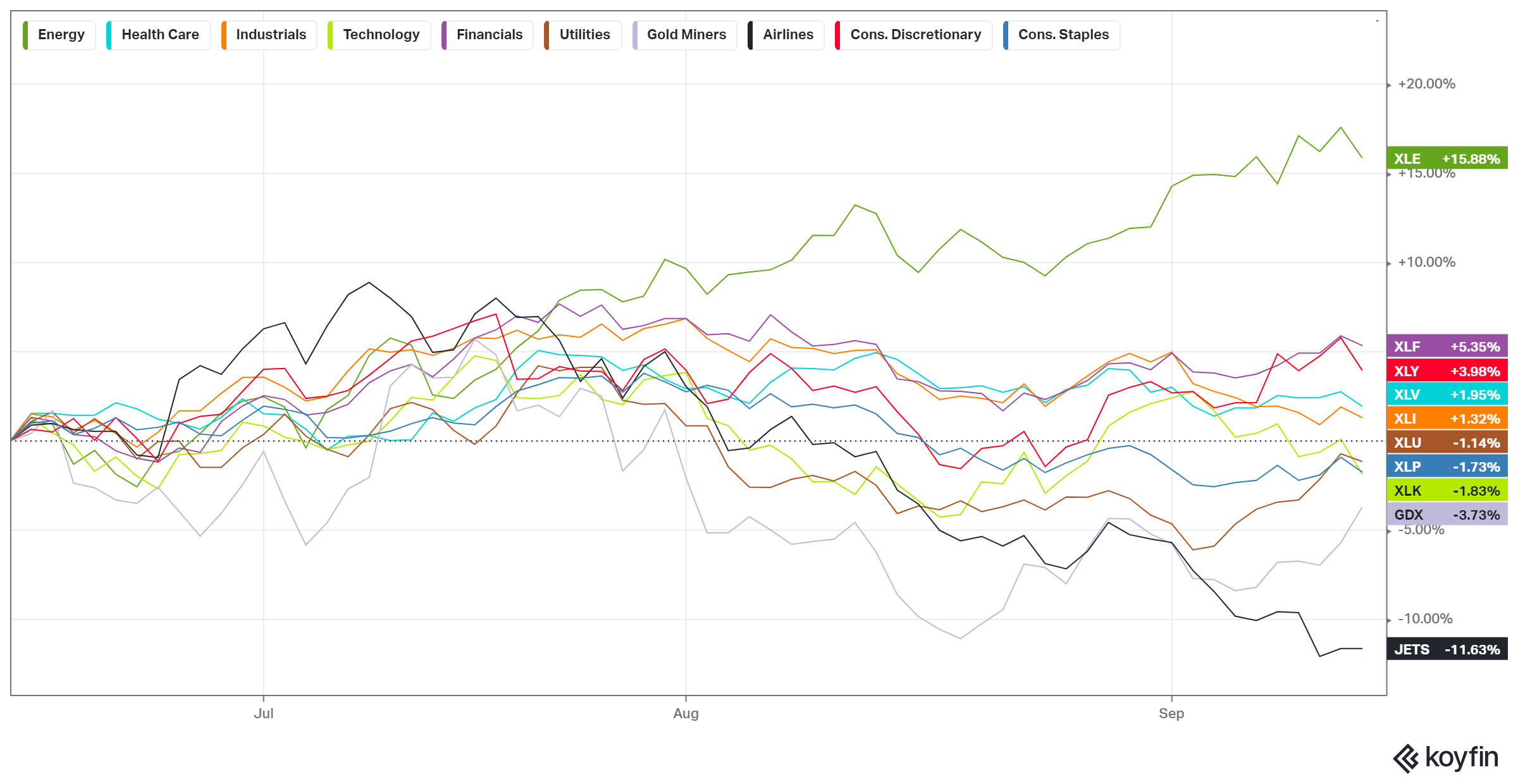

Back in early August in our conversation “ The Decoy effect ”, we pointed out our “Gambit” which was an upward acceleration of oil prices. As well in our June conversation “ Willful blindness ”, we indicated that the energy sector was currently being “neglected” flow wise and that for us it was indicative that it was getting cheap and therefore “enticing” (yet another allocation hint of ours from our musing). No wonder that our “Gambit” was vindicated (our contrarian stance) given Energy Select Sector SPDR ( XLE ) performance for the last three months has been significant:

{kind=link}

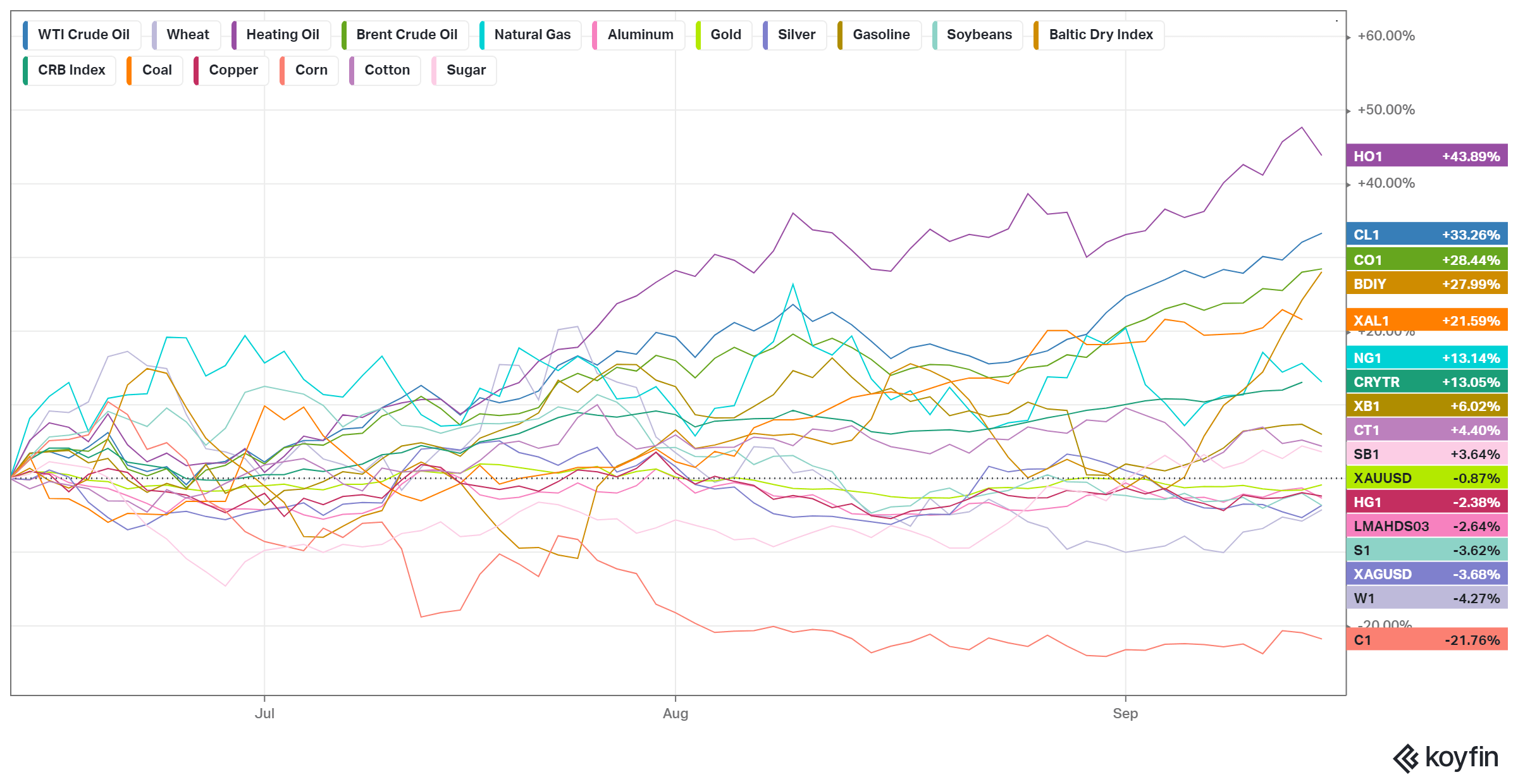

There is of course a similar picture when we look at various commodities in the last three months with oil prices racing ahead:

{kind=link}

At the time of our August musing, we put forward again a paper from the Bank of Israel we have quoted on numerous occasions “ Oil prices, inflation expectations, and monetary policy ”, Bank of Israel DP092015.). Since the Great Financial Crisis ((GFC)) of 2008, the paper argues that a 10% change in oil prices moves 5Y expected inflation by nearly 0.1% in the US and 0.05% in the Euro area.

As such at the time of our writing back in early August we concluded that we were expecting a rise in inflation expectations in that context in the coming quarters.

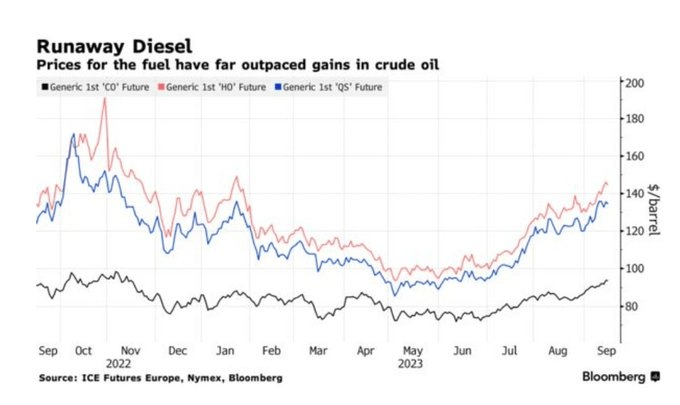

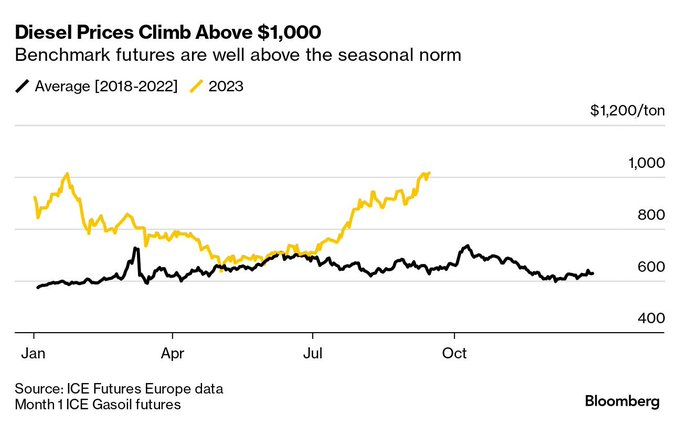

On top of that we are looking at the rising discrepancies between oil prices and Diesel prices:

{kind=link}

Both Saudi Arabia and Russia have reduced oil production which are “richer” in Diesel:

{kind=link}

With consumption rebounding, there is a “refining capacity” problem showing up in rising prices:

{kind=link}

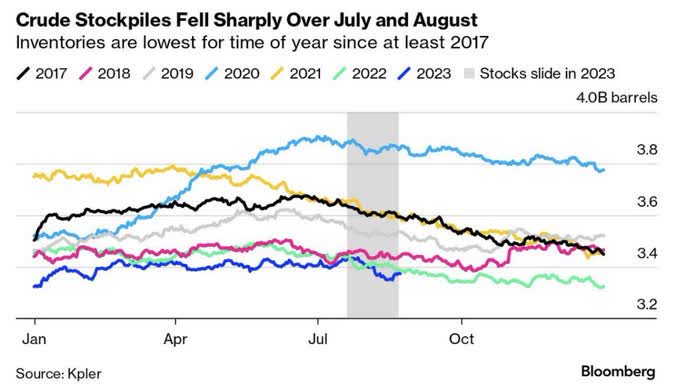

There is also an issue with Crude Stockpiles:

{kind=link}

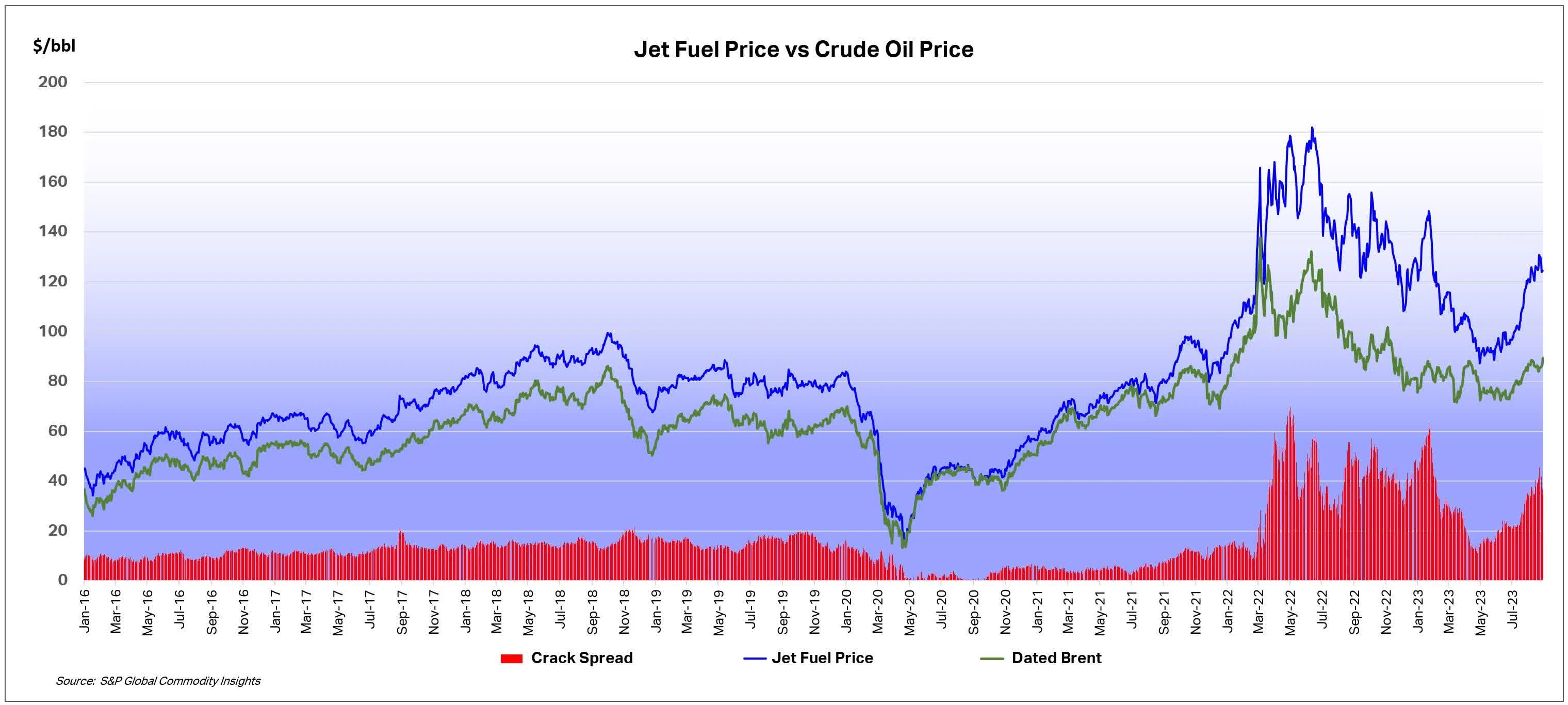

Another “broken” market has been in the Jet Fuel space relative to oil prices since the start of the conflict in Ukraine:

Jet fuel vs Crude oil prices (IATA – S&P Global Commodity Insights)

{kind=link}

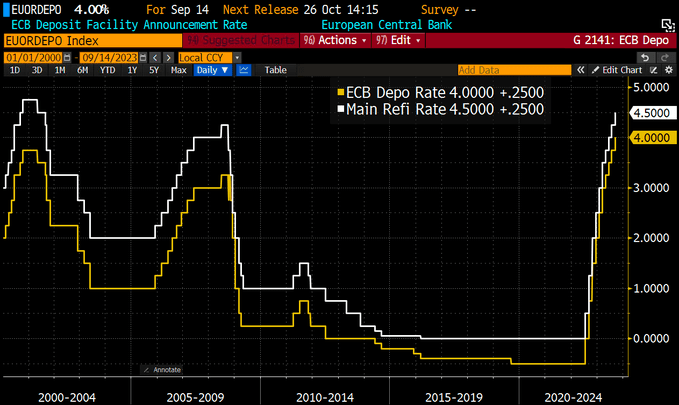

All in all, Christine Lagarde at the helm of the ECB is no “Le Chiffre” aka Mario Draghi when it comes to managing “expectations” even after the 25 bps latest rate hike. This is the ECB's tenth consecutive rate hike, putting rates at 4.5%, their highest since 2001:

{kind=link}

Inflation is becoming entrenched and the three consecutive months of rising oil prices represent a significant headwind for European economies in general and for the ECB in particular as shown by Banque de France February 2018 post entitled “The impact of oil prices on inflation in France and the euro area”:

“A EUR 10 rise in the price of oil results in a 0.4% increase in consumer prices in France and the euro area. A significant part of this rise can be attributed to the non-energy components of the consumer price index. This indirect effect amounts to 0.1 percentage point in the euro area and 0.15 percentage point in France.” – Banque de France

When it comes to the impact of global oil prices on domestic inflation, the IMF find out in their September 2022 paper entitled “ Second-Round Effects of Oil Price Shocks ”, that using data for 71 economies, a 10% increase in global oil inflation amounts to 0.4% impact:

“Estimating the impact of global oil prices on domestic inflation using annual data for 72 economies, Choi et. Al (2017) find that a 10 percent increase in global oil inflation increases domestic inflation by about 0.4 percentage point on impact, with the effects vanishing after two years. Conflitti and Luciani (2017) study the pass-through of oil prices to core inflation for the US and euro area. They find that an unexpected 10 percent increase in the real oil price raises core inflation by less than 0.1 percentage point, but with the effect remaining statistically significant for more than 4 years in the US. The effects are similarly small and persistent in the euro area.” – IMF, September 2022

Volatility in commodity prices, increases volatility in domestic inflation over the medium term.

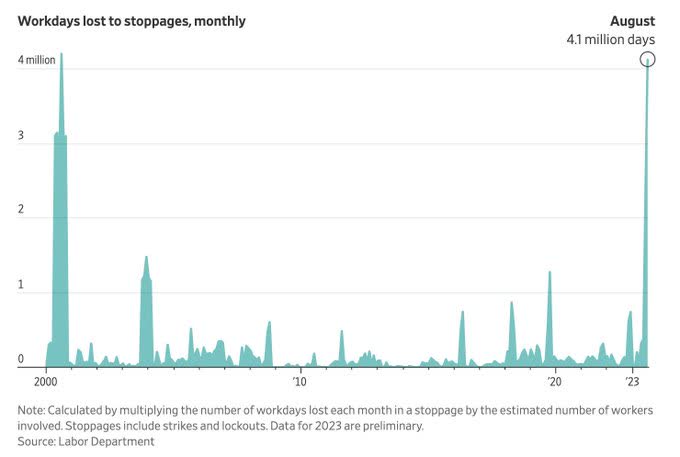

But when it comes to the United States, given the recent UAW strike there, is cause for concern inflation wise. Last month, large stoppages from strikes resulted in 4.1 million missed days of work, the biggest monthly total since August 2000 as per the Labor Department data:

{kind=link}

Why is it a cause for concern you may ask?

Because of what was highlighted in the IMF September 2022 paper:

“Both core and expected inflation respond more slowly to oil price shocks than wages do. Figures 17 and 18 show the impulse responses for core and expected inflation, respectively, along with the corresponding estimates for wages. In the first quarter after an oil price shock, the pass-through elasticity for core inflation is 0.002, which is much smaller than the estimate of 0.015 for wages”

Impulse responses of expected inflation (IMF)

As such, the inflation receding narrative touted by many financial “experts” is akin to a “Gambit” we think. We remain in the stagflationary camp regardless of the Jedi tricks from financial markets punditry.

Monetary regime change?

Before delving into the nitty gritty of what entails our second bullet point we would like to remind our readers that the most important monetary changes will certainly come from the Bank of Japan.

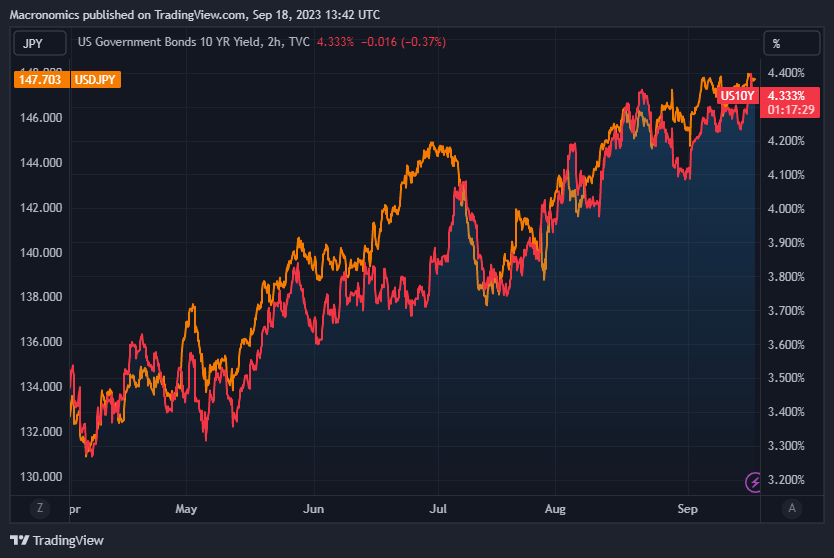

We have highlighted on numerous occasions that there has been a significant weakening of the Japanese yen in synch with the rise in US Treasury 10-year yields (6-month chart):

USTs 10 year yield vs USD/JPY 6 months (Macronomics - TradingView)

{kind=link}

As per our last conversation this is what we had to say:

“The weakening of the Japanese yield is the consequence of significant amount of bonds purchase by the Bank of Japan. As we pointed out in our March conversation “ The Cheshire Cat ”, Japan already owned 56% of the Japanese government bond market and given their willingness in boosting their defense spending and that Japanese are reluctant to accept tax hikes, the easiest way of course is therefore to issue more bonds and for the Bank of Japan to buy more of it.” – Macronomics, August 2023

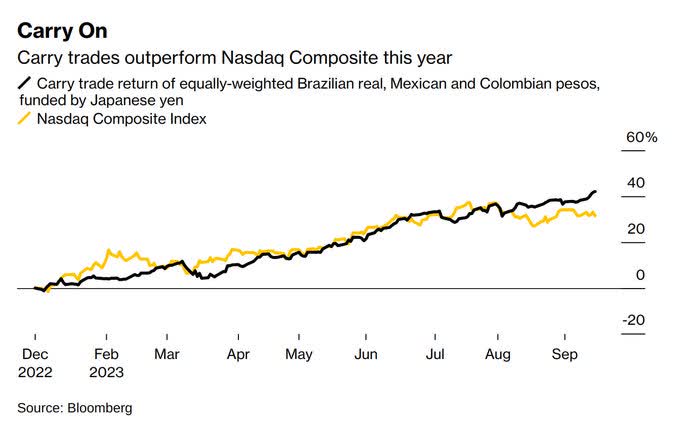

In early August in our conversation “The Decoy effect”, we mentioned that Mrs Watanabe and her “Double Deckers were back into play through Uridashi and Toshin funds via carry trades on both the Mexican peso and the Brazilian Real which used to be her favorite currency back in 2011. Sure for many the NASDAQ play has been the TINA trade (There Is No Alternative) of some sort in 2023, but, Mrs Watanabe knows a thing or two about “carry”:

{kind=link}

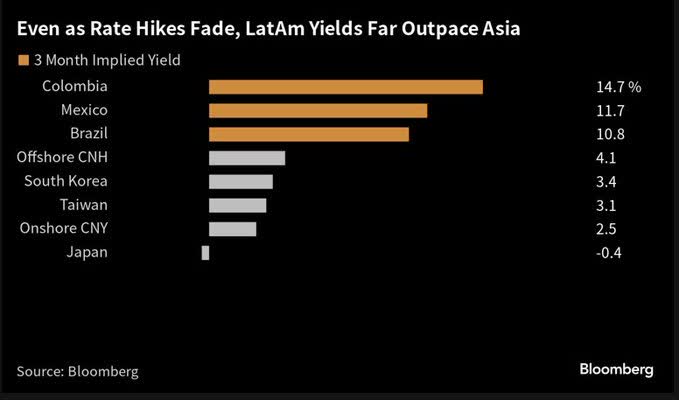

She also knows a thing or two about “Yields”:

{kind=link}

As you know from our regular musings, “Bondzilla” the fixed income allocator monster is “ Made in Japan ” with the significant role played via carry trades through Mrs Watanabe, GPIF and Japanese lifers and other financial players.

When it comes to Monetary regime change we read with interest Bloomberg article entitled “ Carry Trade Mints 42% Profit and Sparks Push Into New Market ”:

“Central banks in Brazil, Mexico and Chile have also started to lower rates, reducing the “carry” (which is finance jargon for the return on an investment) on some of the most lucrative trades.

Despite the risks, a growing number of traders still see value in the yuan as a means to spread out the funding risk on their carry trades.

While yen carry trades boomed the past two years as just about every central bank outside Japan aggressively raised rates, the worry now is that the BOJ will join in, especially as inflation has topped its 2% target for over a year. Traders recently priced in expectations the bank will raise rates in January.” - Bloomberg

As well from the same article we are reading that Goldman Sachs has been recommending funding purchases of Latin America currencies such as the Colombian pesos borrowing Yuan rather than Japanese yen:

Latam currencies correlation to Yuan (Bloomberg - Twitter)

The yuan apparently is becoming an attractive funding currency thanks to its low inflation and low volatility, making it an attractive “Gambit” for global Macro players hence our monetary regime change reference.

But we think there is more to it. If demography is destiny, then indeed Japan is turning more and more from the land of the rising sun towards “Sunset”:

{kind=link}

Also in continuation from our last missive rebuking the Chinese “Doom and Gloom” narrative we would like to point out that China is turning towards internal consumption hence the push of Hospitality Accor Group on track to sign 125 hotels projects in China as Chinese consumers splash out on leisure and Hilton betting on China’s middle class as it eyes about 730 hotels in the next 10 years. China continues to organize the “controlled demolition of financial instability from the likes of “Evergrande” and WMPs (Wealth Management Product).

As well in our June conversation “Willful blindness” we indicated the following:

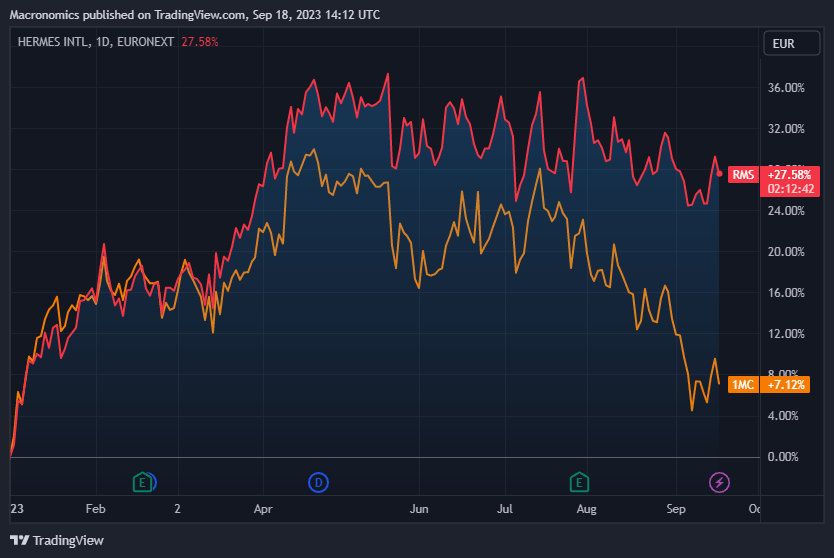

“Back in November last year we hinted that the Chinese “recovery” story would favor the French luxury sector and as such there has been a significant bounce in the sector which is a significant weight in the European Consumer Discretionary sector. We also pointed out in our December conversation “ Illusory trust effect ” that French luxury house Hermès has a stronger margin than LVMH and continues to have our preference ”- Macronomics – June 2023

(Hermès vs LVMH YTD below chart):

{kind=link}

As a reminder, the luxury sector represents more than a third of the weight of the CAC 40 French index (LVMH + L’Oréal + Hermès + Kering). The weight of the luxury sector in the French sector has tripled since 2007.

The CAC 40 is not a true reflection of the French economy as such given some sectors such as the luxury sector are over-represented. In the US, the Tech sector as well is over-represented in some indices.

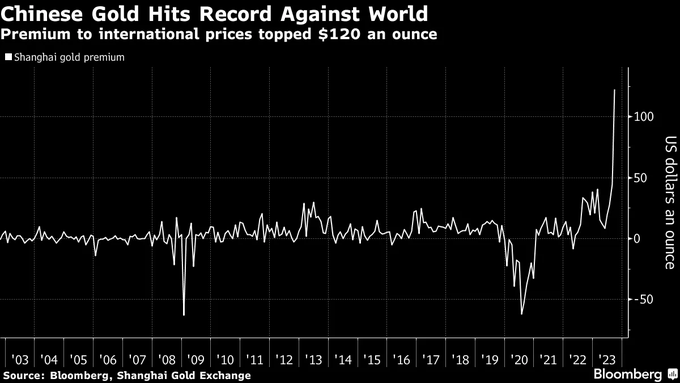

Another very important point we think when it comes to the “monetary regime change” is the growing premium of Chinese gold to international prices:

{kind=link}

We also raised our concerns again in our last musing about the US fiscal trajectory.

As commented by our friend Geoffrey, the “bond vigilantes” are in control of the long-end and do not care about “massaged” inflation numbers but care about the fiscal position of the United States. The US fiscal trajectory is unsustainable because of Quasi Fiscal Deficit in the US. (For more on QFD issues we highly recommend watching Geoffrey Fouvry quick take on Graph Financials, part 1 and part 2 ). US Treasuries seems to be more and more trading like Emerging Market bonds when it comes to “volatility”.

But there is according to him a more profound change: the biggest monetary change in the last 100 years. The end of FX used as reserves. This process started with the 9th recommendation from the Genoa Convention of the Leagues of Nation forcing countries to accept the US currency and the British currency as reserves. Before that only national currency claims and Gold would qualify as reserves. That started in 1922. This led to a double counting of reserves and a boom. This is where we got the idea of “currency as reserves”, with a repeat in Bretton Woods I, also known as the Triffin Dilemma. Evidently double counting without flow of Gold but “in fine convertibility” is totally impossible. In the end, double counting is a turbo charger for booms, and the convertibility is like actioning the hand brake while driving at 200 mph, while gold flow without currency reserve double counting is like using a pedal brake early in the cycle without the risk of “overspeeding”.

A system of floating currencies without the parasitizing of FX in central banks is perfectly possible, it would be achievable with bilateral swaps with the balance settled in Gold, and it does not require currencies to be pegged to Gold. The UK was under such system during the 1797-1821 period and the US between 1861 to 1879. The currencies were floating with no foreign currency reserves parasitizing / forced into seigniorage collection, while trade was settled in Gold.

He believes that is what China is doing now.

WATCH the Graph in Augmented Media.

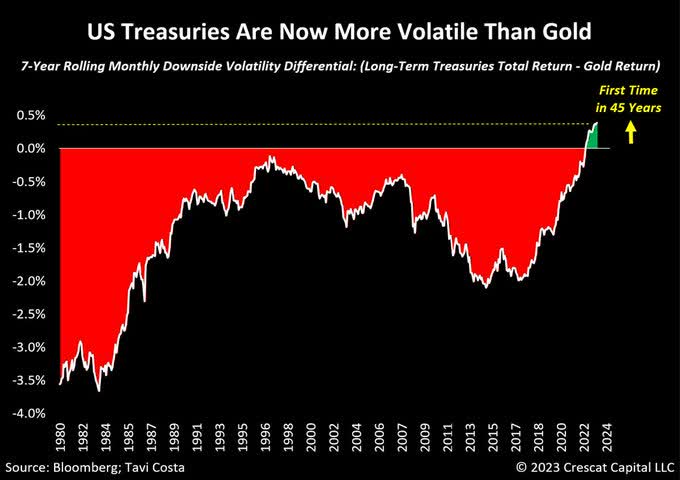

USTs more volatile than gold (Tavi Costa - Bloomberg - Twitter)

{kind=link}

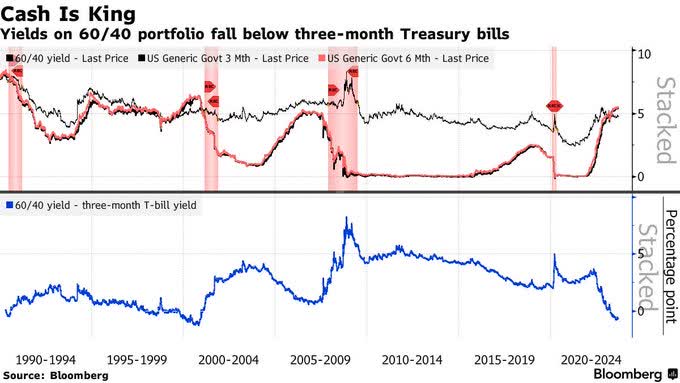

“Treasuries are no longer the safest alternative.

In fact:

For the first time in 45 years, US Treasuries now have higher downside volatility than gold.

This is undeniably crucial.

The shifting dynamics of capital moving away from crowded equity and fixed-income holdings, as investors seek new investment opportunities, could have profound implications in financial markets.

This is where gold, commodities, and overall hard assets are poised to play a significant role during this transitional phase from traditional 60/40 portfolios.” – Tavi Costa - Twitter

As such the much vaunted “balanced” portfolio 60/40 is getting “unbalanced”:

{kind=link}

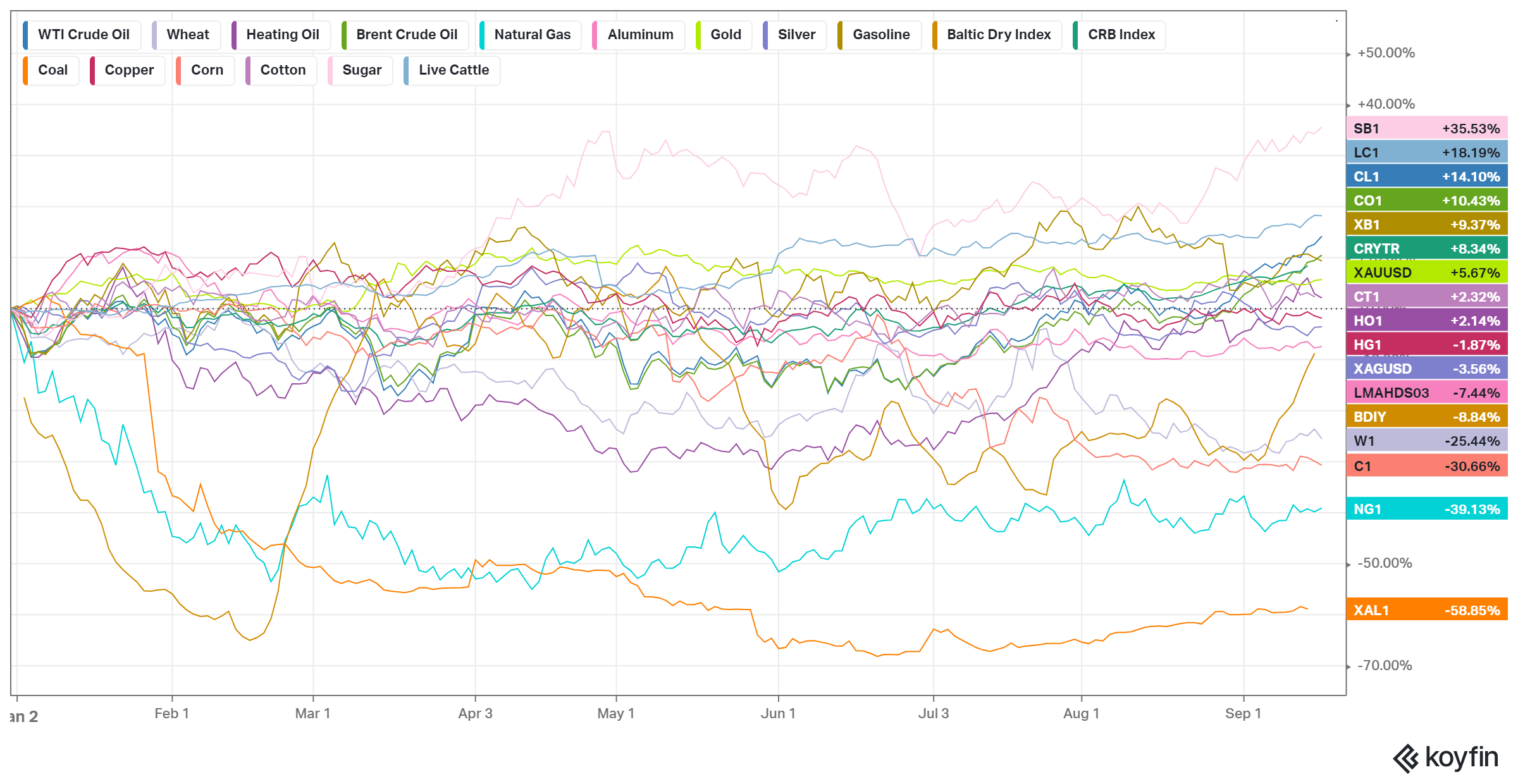

There is also a monetary message coming from “soft commodities” with Cattle Futures closing at an all-time high again in conjunction with Orange Juice and Sugar and this is not only thanks to poor harvest.

In our February conversation “ Tantalean Punishment ” we mentioned that back in 1933 a group of young investors in Boston started to worry about inflation and how it would affect bonds and stocks value and after two years of study they set up the first commodity investment trust in the world called Commodity Corp. in 1935.

We also pointed out the work of Professor Edwin Walter Kemmerer he was a professor of economics at Princeton University. He became famous as a "money doctor" or economic adviser to foreign governments all around the world, promoting plans based on strong currencies and balanced budgets. He also helped in the design of the US Federal Reserve System in 1911:

“A price is the value of a particular commodity in terms of the value of the monetary unit. It is an expression of the number of units of money for which a commodity is bought and sold. The price level represents a composite of individual prices. Prices fluctuate, therefore, with the changing value of goods and also with the changing value of money.” – Edwin Walter Kemmerer – The Prospect of Rising Prices from the Monetary Angle

If the only satisfactory hedge against inflation is commodities as thought by investors in 1933, we are not surprised to have seen such a rally in commodities overall and soft commodities in particular:

{kind=link}

Geoffrey Fouvry also added a quote from Henry Thornton modern central banking according to the Fed. it is a mistake to seize assets during a conflict:

“The idea that foreign property might be seized in England, as an act of retaliation for the British property seized in the north of Europe, may also have had some influence. The expectation of seizures on each would prejudice the exchange of whichever country was in debt, and the country in debt happened to be Great Britain” The seizure of assets for the benefit of Ukraine is illegal under US law – the 1977 International Emergency Economic Powers Act ( IEEPA )

WATCH the Graph in Augmented Media

When it comes to “Gambits”, it seems to us that Russia knows a thing or two when it comes to “chess games”. As such, Russia has sacrificed its FX reserves with the aim of achieving a subsequent positional advantage thanks to its commodity trading position which has led to an acceleration in the monetary and geopolitical grand chess:

“The player accepting the gambit must take time to procure the sacrificed material and possibly must use more time to reorganize their pieces after the material is taken”

Scarcity and commodities do not mix well when it comes to inflation expectations. You’ve been warned.

“The ability to deal with people is as purchasable a commodity as sugar or coffee and I will pay more for that ability than for any other under the sun.” - John D. Rockefeller

For further details see:

Gambit