GAMB - Gambling.com Group's Q2 Results: Betting On The Future

2023-08-23 12:47:56 ET

Summary

- Gambling.com Group's Q2 performance exceeded expectations with a 63.10% YoY increase in revenue and a 60% surge in new depositors.

- The company's strong financials, strategic expansion, and promising market opportunities make it a compelling investment in the growing online gambling industry.

- Despite challenges such as rising operating expenses and evolving regulations, Gambling.com Group's outlook is positive, with adjusted revenue and EBITDA guidance for 2023 adjusted upwards.

Thesis

In the evolving landscape of the online gambling industry, projections indicate a potential doubling of market size within the forthcoming five years. Among the forefront contributors to this anticipated growth is the Gambling.com Group ( GAMB ). Their Q2 performance, as evidenced by a non-GAAP EPS of $0.17 and a revenue of $25.97 million—exceeding expectations by $4.22 million and marking a 63.10% year-over-year increase—suggests the firm's role not only as a participant but also as an influencer in the industry's trajectory. This analysis argues that Gambling.com Group's strong financials, savvy operational strategy, and promising market opportunities make it a compelling investment, even as it navigates the challenges of expansion and evolving regulations.

Company Overview

Gambling.com Group Limited, based in Saint Helier, Jersey since its 2006 inception, is a performance marketing firm serving the global online gambling sector. With a suite of branded websites like Gambling.com and Bookies.com, they cater to the iGaming and sports betting markets through digital marketing efforts that's exemplified in their corporate mission statement:

“At Gambling.com our mission is clear. We aim to provide every online gambler with a safe and fair place to play via independent reviews of the world’s best online gambling companies. We supplement this with expert writers, in depth analysis and data therefore ensuring that everything our audience needs to know is available right here before safely gambling online.”

Gambling.com Group's Q2 Earnings Highlights

The landscape of the online gambling industry is rapidly changing and on a trajectory to grow from a $105 billion market to $213 billion within the next five years, and at the heart of this metamorphosis is the remarkable financial performance of firms like the Gambling.com Group.

If you dig into their recent numbers, you'll see they’re doing something right as evidenced by their post-earnings' share price pop , which I think gives a pretty good snapshot of where the whole industry might be headed.

Seeking Alpha

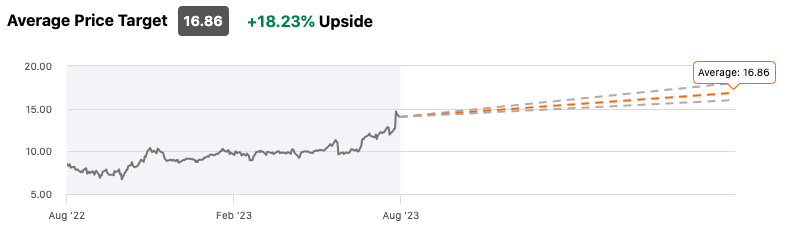

Evidently, Wall Street also loves Gambling.com, with seven analysts unanimously giving the stock a "Strong Buy" rating and an average projected price target of around 18% from here.

{kind=link}

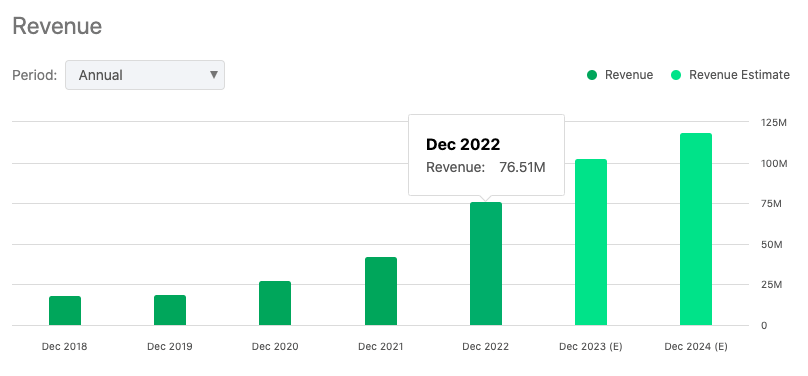

Diving into the firm's Q2, investors were welcomed with a substantial 63% increase in revenue, touching the $26 million mark in comparison to the previous year.

GAMB's growing revenues. (Seeking Alpha)

{kind=link}

What makes this figure more intriguing is the engine behind this growth: the exponential rise in New Deposit Customers (NDC) from a diverse array of regions. North America, the UK, Ireland, and various other global regions have contributed massively, revealing a significant shift in user behavior and preferences. This surge in new depositors, which grew by 60% to over 91,000 in this quarter, underscores the burgeoning market demand and its potential for further expansion.

However, growth often comes at a cost. The company’s operating expenses have risen. But instead of reckless spending, think of it more as smart investing. The company has strategically expanded its foothold across sectors, from marketing and sales to technology and finance. This proactive approach is indicative of a larger growth strategy. The emphasis on optimizing their business model to ensure a strong free cash flow conversion, which stood strikingly at about 90% of adjusted EBITDA for this quarter, bears testimony to this strategy.

With a net income of $0.3 million and an adjusted net income of $6.5 million for the quarter, and with their adjusted EBITDA skyrocketing by 161% for Q2, it’s clear they’re raking in money faster than they’re spending it. This fiscal prudence ensures a healthy cash reserve of $31.3 million as of June 30th, 2023, positioning the company to fuel its organic growth initiatives.

Peering into the future, management's outlook is promising as they anticipate regular seasonality patterns in Q3 including major sporting events. Given their impressive performance in the second quarter, it's hardly surprising that their revenue and EBITDA guidance for 2023 have been adjusted upwards, targeting an ambitious growth rate of 31% to 36%.

But there’s more on the horizon. The expected launch in Kentucky and the impending online sports betting arena in North Carolina point towards a North American market brimming with opportunities. And globally, the stage is set with promising markets like Brazil and Japan opening up, offering untapped reservoirs of opportunities.

Performance

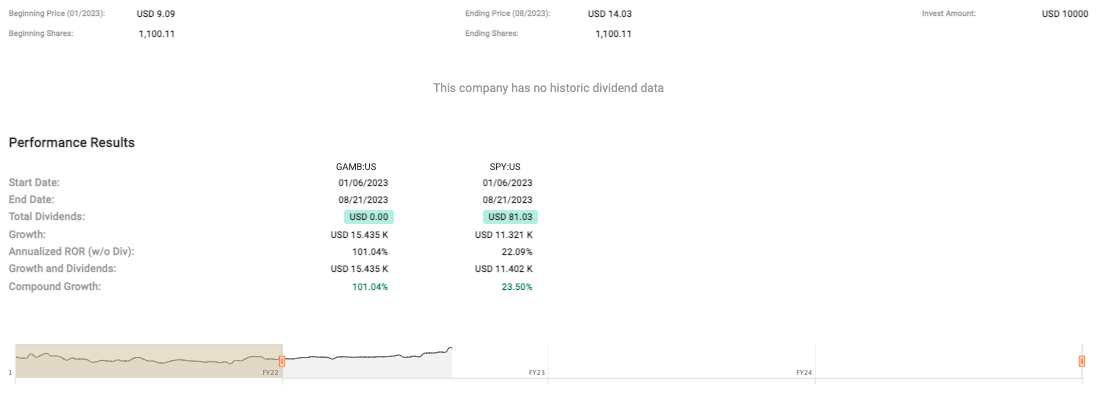

Looking at GAMB's performance, starting at a price of $10.15 in December 2021 and rising to $14.03 by August 2023, the firm exhibited a commendable upward trajectory in its stock price, signaling strong capital appreciation of 38.23% in less than two years.

{kind=link}

Contrast this with the S&P 500 Index , and Gambling.com clearly outshines. While S&P investors would have been compensated with dividends, the growth in the primary investment itself is quite underwhelming.

Valuation

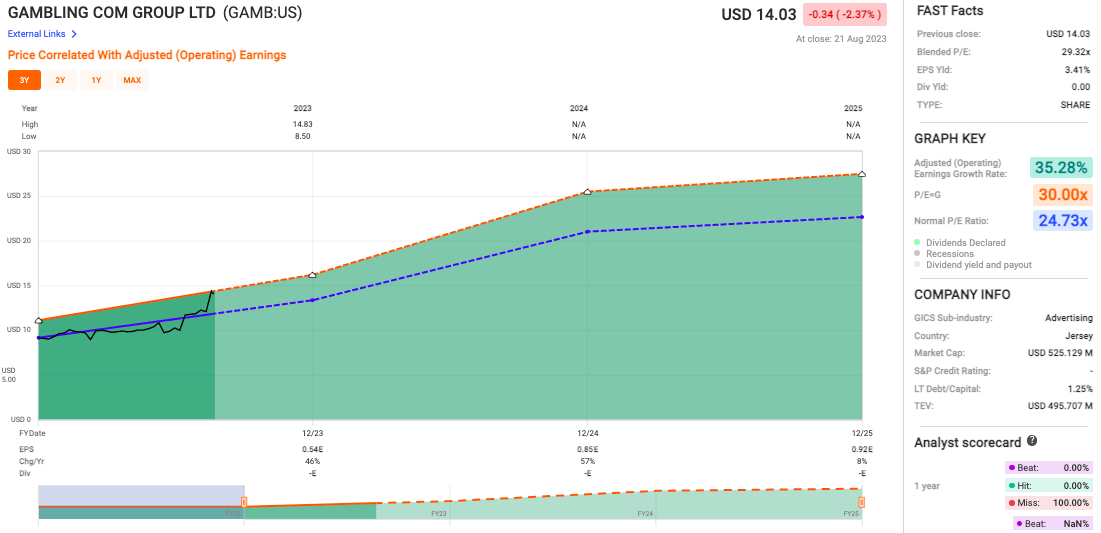

Gambling.com's blended P/E of 29.32x (see chart below) isn't what you'd call 'cheap' by any standard, especially when you consider the historical norms in the gaming and online gambling industry. In comparison to its 'normal P/E ratio' of 24.73x, an investor could argue the stock is overvalued. An inflated P/E is often justified if there's rapid growth, but even with an Adjusted (Operating) Earnings Growth Rate of 35.28%, the current valuation makes me pause. Investors are obviously pricing in not just growth, but exceptionally strong growth.

{kind=link}

But with a 35.28% earnings growth rate, the company is doing something right and naturally, the question is, can they sustain it? And even if they can, is it enough to justify the premium valuation?

Risks & Headwinds

Circling back to the company's Q2 , let's begin with the uptick in operating expenses. They have ascended to a noteworthy $24.3 million, showcasing a leap of $6.7 million. At first glance, this might sound alarm bells for any discerning investor. However, understanding the driving forces behind this surge offers clarity. Expansionary efforts across various departments, as well as costs associated with acquisitions, largely account for this increment. The big question here is whether this kind of spending can keep up and if it's giving us a good bang for our buck in the long run.

Looking forward, the company's predictions for the next quarter seem pretty upbeat. But there’s a catch. The company has cautiously refrained from carrying forward the seasonality-boosted performance from Q2 into their Q3 forecasts. This tempered anticipation possibly underscores a brand of circumspect optimism. So, if you're an optimist, you can view this as the company's way of playing it safe and managing expectations.

Now, when we talk cash – it seems there's been a dip. A sequential quarterly decrease of $2.3 million is on the ledger, largely imputed to payments tethered to acquisitions. If we keep seeing this kind of drop without a matching rise in revenue, well, it’s something we'll have to keep a close eye on.

Lastly, when it comes to expanding, especially in North America, it's not exactly smooth sailing and just to give you an idea: 43 states are still trying to figure out the iCasino rules, and 21 states are still on the fence about online sports betting. And when we think globally – places like Brazil and Japan, they're kind of like the wild west in terms of regulations. In other words, it's all still up in the air.

Rating: Strong Buy

Based on the presented analysis, I rate Gambling.com Group's stock a "Strong Buy". The online gambling industry is forecasted to double in the next five years, and Gambling.com Group is positioned favorably, showing a substantial 63% increase in Q2 revenue and a remarkable 60% surge in new depositors. Their strong financials, underscored by a 90% free cash flow conversion from adjusted EBITDA and a healthy cash reserve, combined with promising future expansions in lucrative markets, solidify my rating.

For further details see:

Gambling.com Group's Q2 Results: Betting On The Future