GLPI - Gaming and Leisure Properties: Play With House Money

2023-11-14 08:10:00 ET

Summary

- Gaming and Leisure Properties offers opportunity due to its pricing power, efficient cost structure, and attractive dividend yield.

- GLPI owns 61 properties across the US, with 88% of rent coming from premier, publicly-traded gaming companies.

- GLPI has demonstrated resilient results, with strong profitability and potential for growth through rent resets and development pipeline.

Being a REIT investor hasn't been easy as of late, with plenty of risks baked into the sector due to higher interest rates. While I'm wary of certain REIT segments that are more economically vulnerable, I see opportunity in net lease REITs like Gaming and Leisure Properties ( GLPI ) due to their pricing power and efficient cost structures.

I last visited GLPI here back in November of last year and the stock has declined by 9.6% since then (-4.3% total return when including dividends), due in part to higher interest rates. In this article, I provide an update and discuss why income and value investors may want to revisit this stock for potentially strong returns from income and growth down the line.

Why GLPI?

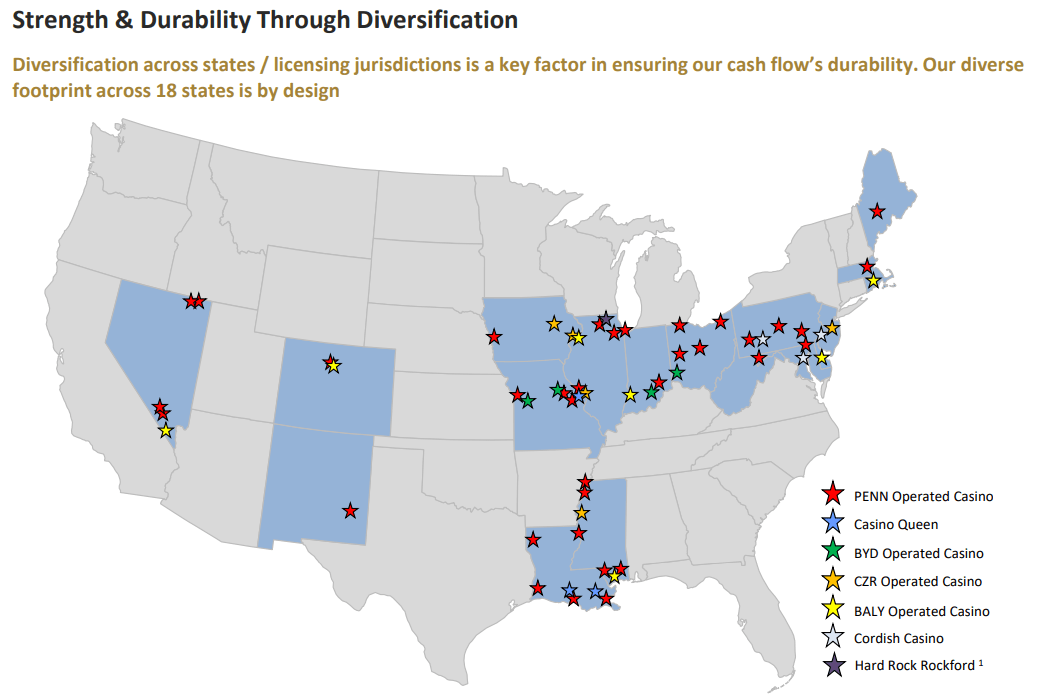

Gaming and Leisure Properties is one of just 2 triple-net lease REITs that are focused on gaming property ownership across the U.S., with the other one being VICI Properties ( VICI ). At present, it owns 61 properties covering 30 million square feet, with 14,800 hotel rooms across 18 states.

Notably, 88% of GLPI's rent comes from premier publicly traded gaming companies PENN Entertainment ( PENN ), Boyd Gaming ( BYD ), Caesars Entertainment ( CZR ), and Bally's ( BALY ). To get a sense of the durability of GLPI's business model, it collected 100% of its rents during the COVID, at a time when many Shopping Center REITs faced rent collection issues.

Unlike VICI, whose iconic properties are concentrated around Las Vegas, GLPI's properties are diversified across regional gaming markets in the Midwest, Mid-Atlantic, South, and Vegas, as shown below.

{kind=link}

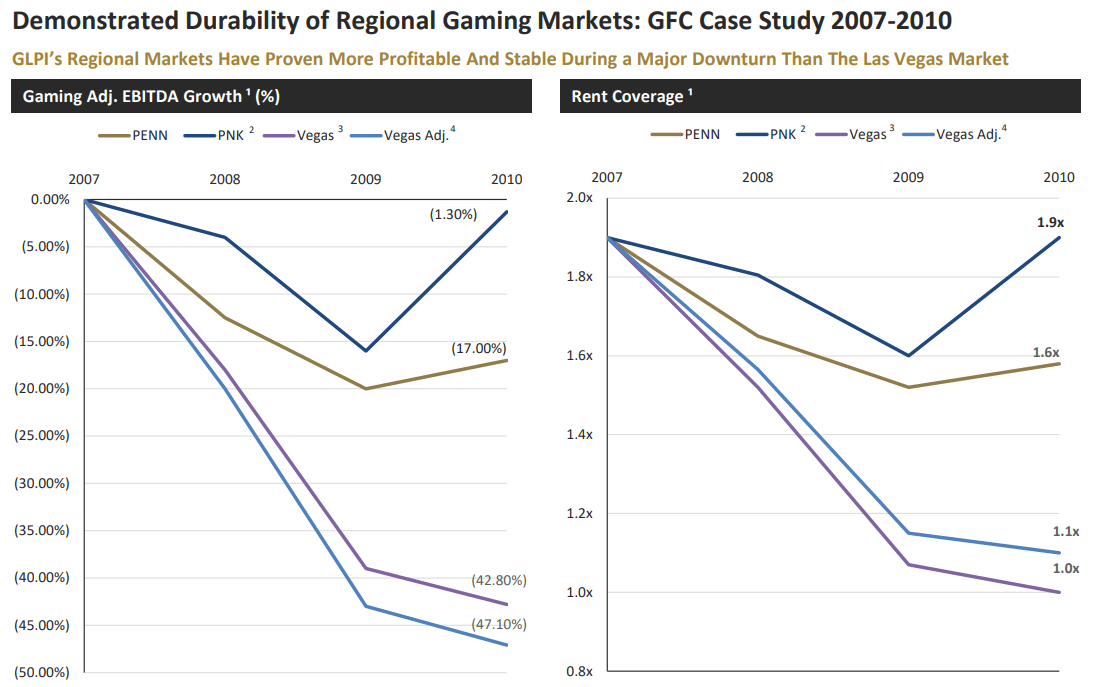

While GLPI's limited exposure to Vegas doesn't give it the same name recognition as VICI, much can be said about the durability of regional markets. That's because regional gaming markets cater to surrounding clientele that make them an affordable destination compared to Vegas. This is something worth considering as risks of the U.S. economy heading into a recession next year are now elevated due to high interest rates. As shown below, PENN's assets as a representation of the regional gaming market demonstrated less of a downturn and a faster recovery compared to Las Vegas during the Great Financial Crisis.

{kind=link}

Meanwhile, GLPI has demonstrated resilient results, with the most recent third quarter FFO/share growing by 7% YoY from $0.88 in the prior year period to $0.94. This was driven by rent escalators and percentage rent adjustments on GLPI's leases, adding $2.9 million of cash rent. Plus, the combination of higher noncash revenue gross-ups, investment in leases, and straight-line rent adjustments drove a collective $6.6 million YoY increase in cash rents.

Plus, GLPI continues to demonstrate strong profitability that's fitting for a triple net lease REIT. This is reflected by GLPI's TTM Operating Margin (with depreciation addback) of 92.9%, comparing favorably to the 91.5% for VICI and 88.4% of net lease bellwether, Realty Income Corporation ( O ) over the same time period. Having higher margins makes GLPI less vulnerable to a revenue downturn, as it has less overhead costs to consider. This is analogous to a person who lives below their means being more financially protected from adverse economic events compared to a person who does not.

Looking ahead, GLPI is positioned to benefit from 10 amended Pinnacle and Boyd master leases that have rent resets occurring in May of next year, with the expectation that there will be an upward percentage rent (percentage of gross tenant income) adjustment. GLPI could also benefit from its development pipeline, which includes its $78 million development in Louisiana that's expected to produce a healthy 8.5% initial cash yield, as described during the recent earnings call :

And as you recall, we sold our Hollywood facility in Baton Rouge to Casino Queen. And as part of that sale, we retained the right to design, build and construct the landside facility, eliminating our old boat. Our $78 million spend will produce a yield of 8.5%. The new casino is doing spectacularly well. And I must say, for the money invested there, to say this is an issue of personal pride, it's a terrific facility, and it's kicking butt.

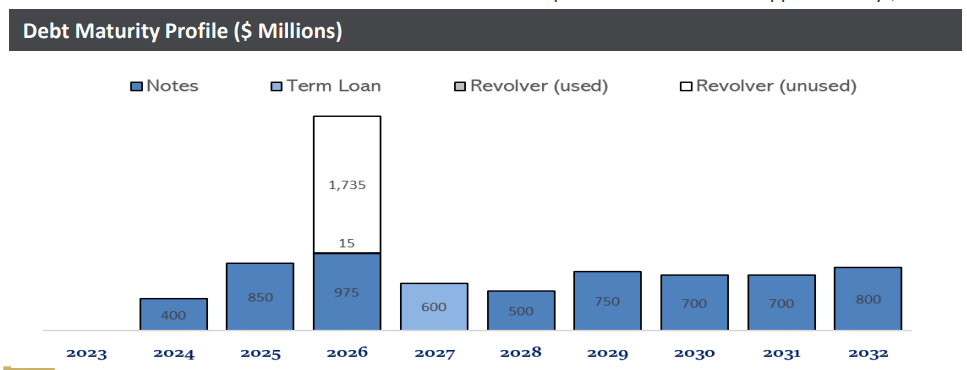

Importantly, GLPI is well-positioned with a strong balance sheet with a BBB- investment grade credit rating from S&P and a net debt to proforma EBITDA ratio of 4.7x. As shown below, GLPI has no remaining debt maturities this year and a well-staggered debt maturity profile over the next 10 years.

{kind=link}

Risks to GLPI include the aforementioned elevated risk for a recession next year, which could hurt tenant profitability and GLPI's percentage rents. In addition, gaming is considered to be a 'sin' industry, and local zoning restrictions could inhibit GLPI's future development potential. It's worth noting that GLPI is not as diversified as VICI as far as VICI's investments in non-gaming sectors are concerned. Lastly, higher interest rates could also hurt GLPI's profitability, although some investment banks such as UBS ( UBS ) expect rate cuts to happen as early as next year.

Meanwhile, investors get paid an appealing 6.5% dividend yield that's covered by a 79% AFFO payout ratio. In addition, while many REITs have had to hold their dividends steady, GLPI actually grew its dividend rate by 3.5% compared to the prior year period.

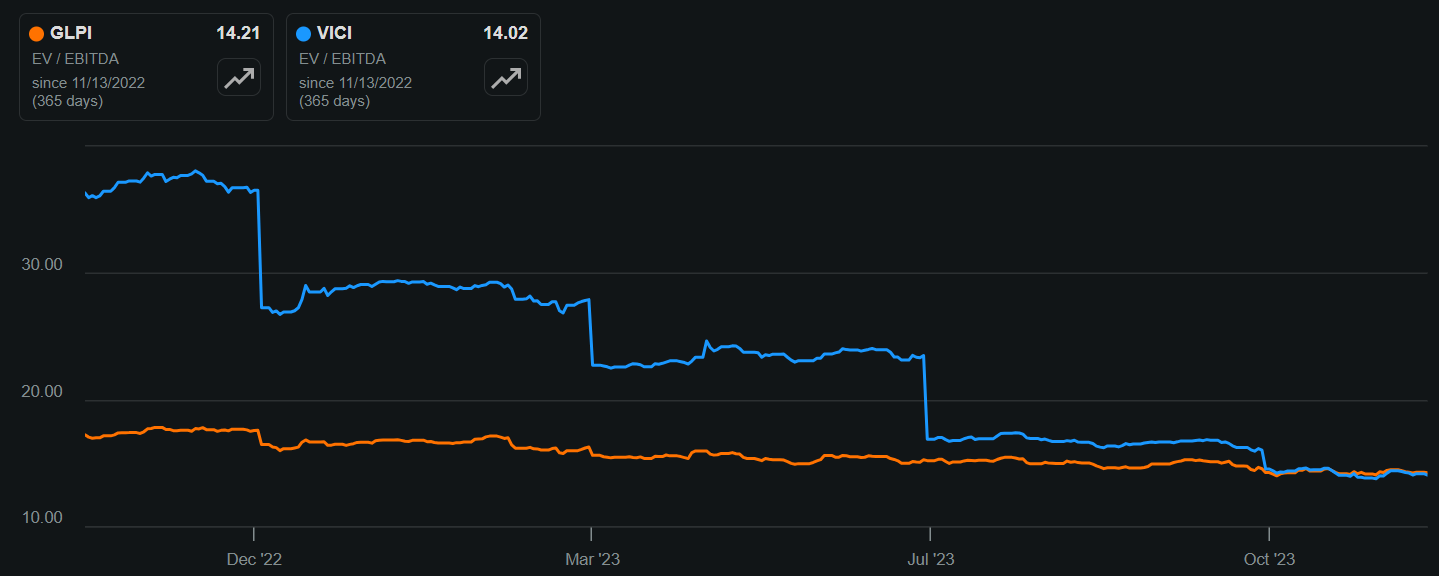

Lastly, I see value in GLPI at the current price of $45.05 with a forward P/FFO of 12.4. This makes GLPI reasonably attractive considering that analysts expect 3-8% annual FFO/share growth over the next 3 years, which combined with the dividend could translate to 10-14% annual total returns. While GLPI currently trades at a slight premium to peer VICI with an EV/EBITDA of 14.2, compared to VICI's 14.0, I don't see the two as being an 'either or' investment decision, as GLPI can be attractive for its higher starting yield compared to VICI's 5.9% yield, and for its diversification in economically resilient regional operators.

{kind=link}

Investor Takeaway

GLPI offers investors exposure to a resilient regional gaming market with a strong balance sheet, solid profitability, and potential for growth through rent resets and its development pipeline. With an attractive dividend yield and prospects for total returns in the double digits, investors get to "play with house money" through ownership in GLPI's valuable gaming real estate.

While GLPI isn't necessarily cheaper than its peer VICI Properties, investors who are interested in owning both may find GLPI appealing for its higher starting yield and higher exposure to regional tenants. As such, I reiterate my 'Buy' rating on GLPI.

For further details see:

Gaming and Leisure Properties: Play With House Money