GAN - GAN's Potential Needs To Show Itself

2023-08-01 18:48:35 ET

Summary

- GAN Limited operates an online gambling provider, Coolbet, and provides B2B solutions for other providers.

- GAN has been unprofitable throughout its history and as revenues don't seem to grow, the company could be in for a hard time.

- If GAN manages to grow, the stock could be a fantastic investment opportunity at the current price.

GAN Limited ( GAN ) is a company that operates an online gambling provider, Coolbet, and provides software solutions for other providers. GAN’s turnkey solution currently generates heavy losses, of which part is offset by Coolbet’s profits. As the company’s market value reflects poor faith in the company’s future, I believe the company is worth to have on a watchlist. Before the company’s bottom line starts to improve significantly, though, I have the stock at a hold-rating.

The Company

GAN operates in the gambling industry as mentioned. The company has historically operated its B2B offering, which includes the following services for gambling providers:

{kind=link}

GAN's B2B Offering (gan.com)

As online gambling is becoming legal in more states in the United States, GAN could expand its customer base to create growth to its B2B segment.

In addition, the company bought Coolbet, a B2C gambling site and brand, in 2021. Coolbet has a geographical footprint that is based mostly in the Nordics, Canada, and a recent expansion to Mexico.

{kind=link}

Coolbet's Casino (mr-gamble.com)

The site has a wide offering of slots, a sportsbook and poker. The site offers lots of promotions around these offerings to draw in customers.

Financials

Historically GAN has grown its revenues both organically and through the acquisition of Coolbet, as growth started in 2015:

GAN's Revenues (Seeking Alpha)

The acquisition of Coolbet was made in 2021, explaining the huge jump in revenues. In their most recent quarter GAN’s revenues shrunk by six percent, as one of the company’s B2B clients contributed less in Q1 of 2023 compared to 2022. The B2C side of Coolbet also shrunk, as foreign exchange rates have been unfavorable for the company.

GAN has been unprofitable throughout its history, only generating an operating profit in 2019. Currently the company’s trailing EBIT margin stands at -20% - a heavy loss that the company needs to dig itself out of. GAN’s gross margin is above 70%, so growth would outgrow the company’s high fixed costs – for example, GAN has around $27 million in annual R&D expenses, representing over 19% of the company’s revenues. Other SG&A level is also high and growing, casting worries for the company’s future earnings.

The company holds almost $41 million in cash and $28 million in debt. The company is unprofitable and bleeds cash flow constantly, so in my opinion a larger cash balance would be healthy to secure GAN’s operations.

Valuation

Usually, my thesis relies heavily on a company’s valuation. As GAN is currently operating with heavy losses, and visibility into the future is quite weak, operative factors weigh more on the stock’s future; the company’s value relies on a potential scenario of a valuation.

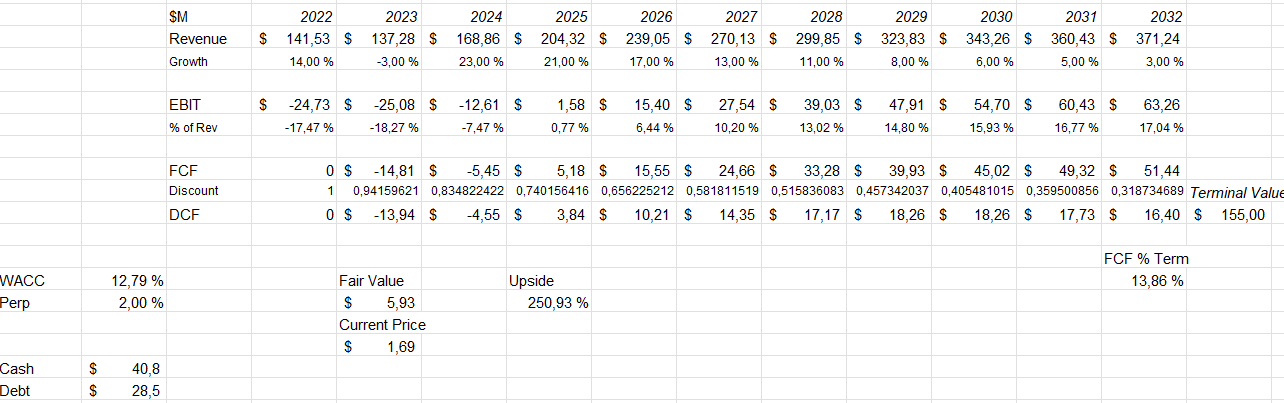

To evaluate the company’s value, I think using a two-way scenario analysis is the proper way to approach GAN. Simply put into a two-way scenario to simplify the case, I expect the company to either stay unprofitable giving a fair value of $0 for the stock, or to grow into a profitable territory giving a higher value for the stock. To approximate such a scenario, I constructed a DCF model for the company.

Analysts expect GAN to shrink around 3 percent in revenues for the current year but expect the company’s operation to turn around beginning in 2024 as growth estimates are over 20% for both 2024 and 2025, with a slightly positive EBIT in the latter year. I have my DCF estimates modified for these figures. Going further into the future, I estimate GAN’s growth to slow down gradually into a 2% terminal growth rate. The expectations have a well scaling EBIT-margin, as GAN has a good gross margin and as a SaaS business’ cost structure is quite solid – in 2032 I forecast their EBIT-margin to be around 17%.

GAN has depreciation and amortization that is somewhat above their capex and capitalized cost level, at least in historical terms - I believe the company should convert its earnings into free cash flow well. These expectations craft the following scenario for the company:

{kind=link}

The scenario would have an upside of 251% to the stock’s fair value estimate – GAN could be a fantastic investment opportunity. It is important to remember, though, that this scenario is a bullish one as GAN showed slightly decreasing revenues in Q1 and doesn’t have much to show for potential growth except the management’s words. A further analysis into the company's growth potential is written in a following paragraph.

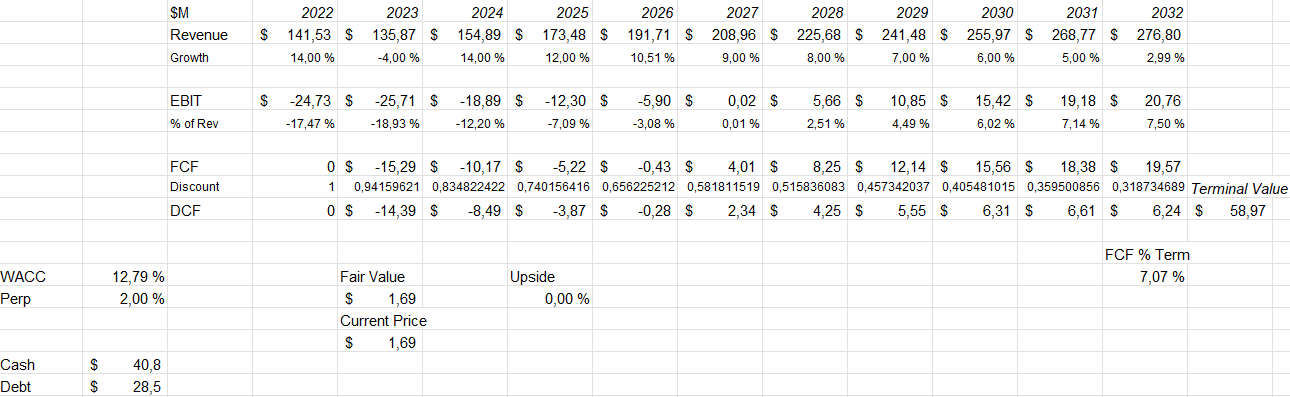

Other than looking at a bear/bull -scenario split, I constructed a reverse DCF to show the market's current base scenario expectations:

{kind=link}

This scenario would imply that GAN could grow revenues quite well, although not with a very high rate. The scaling margins would also imply a moderately good cost control from the company, although the company would only reach an EBIT margin of 7.5% - I believe the investment is very bipolar in its nature, as the company's value entirely depends on their future growth.

The used weighed average cost of capital of 12.79% is derived from a capital asset pricing model:

CAPM of GAN (Author's Calculation)

In their most recent quarter GAN paid $1.4 million in interest payments, an annualized amount of $5.6 million – the company has $28.5 million in debt, so the interest rate seems to be a mesmerizing rate of 19.6 percent. In the painted DCF scenarios I believe the company should be able to refinance its debt, or pay it off, get a cheaper interest rate – I believe a rate of 8.5% represents a long-term rate better. As GAN would improve its cash flows, the company's likelihood to pay back debts should increase dramatically lowering lendors' risk. A 8.5% expectation still leaves room for quite a high margin.

Currently the company's interest-bearing debt is entirely in long-term debt. I believe the company's credit facility should have a flexible payment schedule. Close to the company’s current state, I expect the company to have a debt-to-equity ratio of around 20%.

On the cost of equity side, the risk-free rate is taken from the United States’ 10-year bond yield that at the time of writing stands at 3.96% . The estimated equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate. Tikr estimates GAN’s beta to be 1.30 , a quite high rate as gambling operators are often perceived as recession-proof. The stock is quite illiquid, so I’m adding a 0.75% liquidity premium. Finally, as markets value low-ethic companies with higher required rates of return, I’m adding an ESG-addon of two percent to the cost of equity. These expectations craft the cost of equity of 14.39% and the WACC of 12.79%.

Can the company turn itself around?

As seen in the DCF model scenario, the company could have tremendous upside if it can improve operations with growth. Currently the stock market values a small chance of such a turnaround happening – for example, if there’s a 50/50 chance of either a $0 fair value scenario or my $5.93 DCF model estimated scenario, the company’s hypothetical fair value would be $2.97 – still a big upside from the current stock price: looking at the two scenarios, the market prices in a 28.5% chance for the latter scenario.

GAN has potential to grow B2B revenues, as the gross operator revenue of GAN’s clients seems to grow – for example, in Q1 the growth in the mentioned KPI was 40% as explained in the company’s Q1 earnings call. Revenues continue to trail as GAN’s take rate of the operators’ revenues seems to be declining quite sharply. If the shrinking take rate can be addressed and gross operator revenue continues to grow at current rates, the company could grow into profitability in a scenario like the DCF model I estimated.

The current reason to B2B's trailing revenues seems to be that GAN's take rate from gross operator revenue is collapsing. GAN's management has communicated that the company expects its take rate to grow, as in their Q1 earnings call CEO Dermot Smurfit told investors:

"With respect to our take rate, we do expect this trend to trend upwards in the coming quarters as we roll out GAN Sports across the United States. Our sports betting technology capability and particularly our retail sports betting technology carries a favorable economic model."

The CEO further states his belief in the company's growth in the same earnings call:

To wrap up, I'm confident in our go-forward strategy to drive revenue growth with B2B sports and B2C growth in LatAm. We are taking a more simplified and focused approach to how we allocate our capital and resources.

GAN’s management has promised growing sales and shrinking losses for a long while in their earnings calls – the company has a revenue guidance of $500-600 million for 2026, with the middlepoint representing a CAGR of 40% from 2022; I'm unable to take the management's words at face value. I believe investors should be cautious and look for signals of growth in the company's coming quarters.

Takeaway

GAN is a turbulent investment. An investor must take a stance on the chance of a turnaround in the company’s earnings – if B2B would turn into a growth machine, the stock would in my opinion be a fantastic investment. As the company is yet to prove such growth, I believe it’s reasonable to stand on the sidelines for the time being.

For further details see:

GAN's Potential Needs To Show Itself