GCI - Gannett: 4 Reasons Why I Am Cautious

2023-12-12 03:14:11 ET

Summary

- Gannett has struggled to adapt to the changing media landscape and has delivered weak shareholder returns over the past few years.

- The company recently reported weak Q3 results and cut FY 2023 guidance, leading to a sharp drop in the share price.

- GCI has a highly leveraged balance sheet and may struggle to refinance its existing debt if market and business conditions do not improve.

- GCI trades at a cheap valuation, but lacks any near-term catalyst.

- I am initiating GCI with a hold rating, but would consider upgrading my rating if a monetization catalyst emerges for the company's digital marketing services business.

Gannett Co Inc ( GCI ) has not proved a very good investment over the past few years as the company has struggled to adapt to a changing media landscape.

While other Seeking Alpha analysts are current bullish on the stock, there are four reasons why I am currently cautious:

1. Q3 results were disappointing and the company lowered FY 2023 guidance

2. The company has a highly leveraged balance sheet and may struggle to refinance its existing debt

3. Print media business continues to struggle and still accounts majority of revenue

4. Lack of any near-term catalyst

1. Q3 results were disappointing and the company lowered FY 2023 guidance

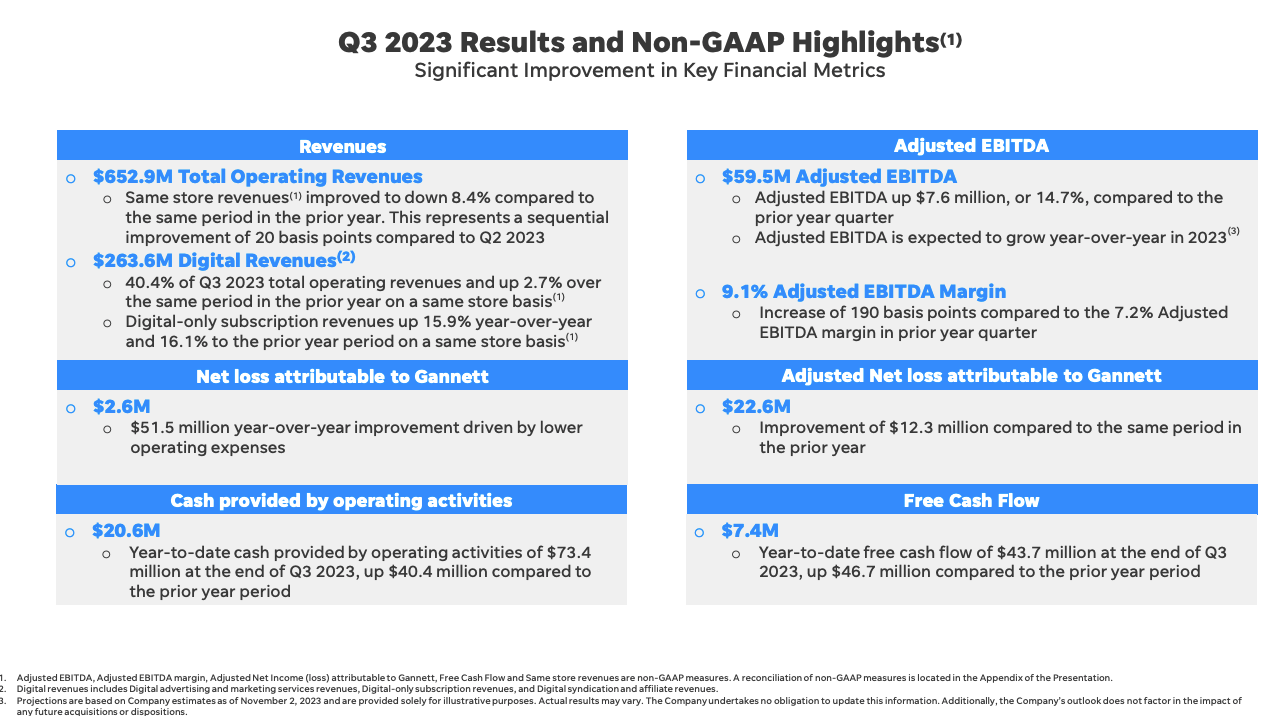

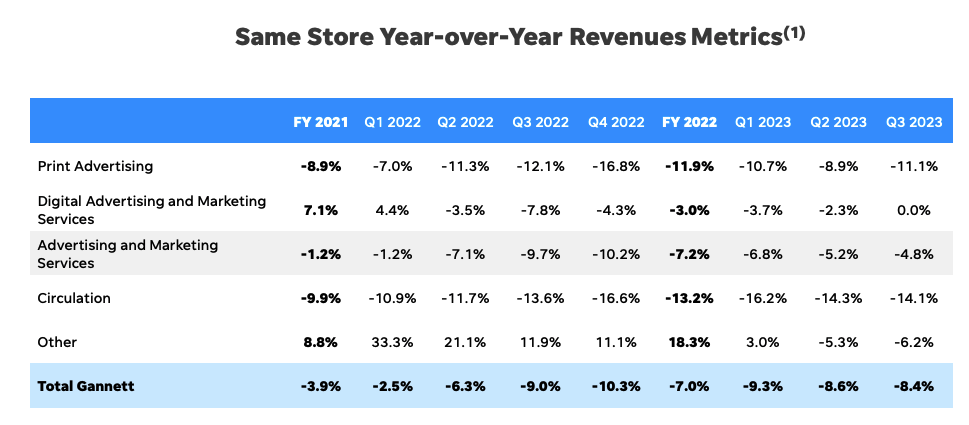

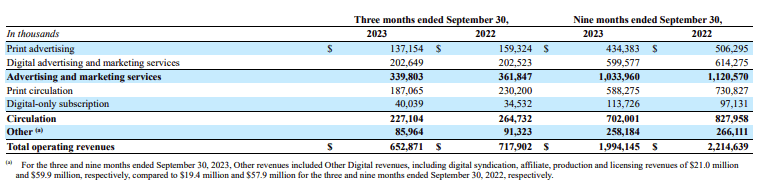

On November 2, 2023 GCI reported Q3 2023 results that disappointed investors. The company reported GAAP EPS of $0.02 per share which beat consensus estimates by $0.01 and compare favorably to a loss of $0.39 per share during the same period a year ago. GCI reported revenue of $652.9 million, missed consensus estimates by $7.53 million, and represents a 9.1% decline from the same period a year ago.

The most disappointing part of the Q3 report was the fact that GCI lowered its full year outlook. The company lowered its revenue outlook to a range of $2.65 - $2.67 billion down from a previous range of $2.75 - $2.8 billion. GCI also lowered its Adjusted EBITDA guidance to a range of $270 - $290 million down from a previous range of $290 - $310 million.

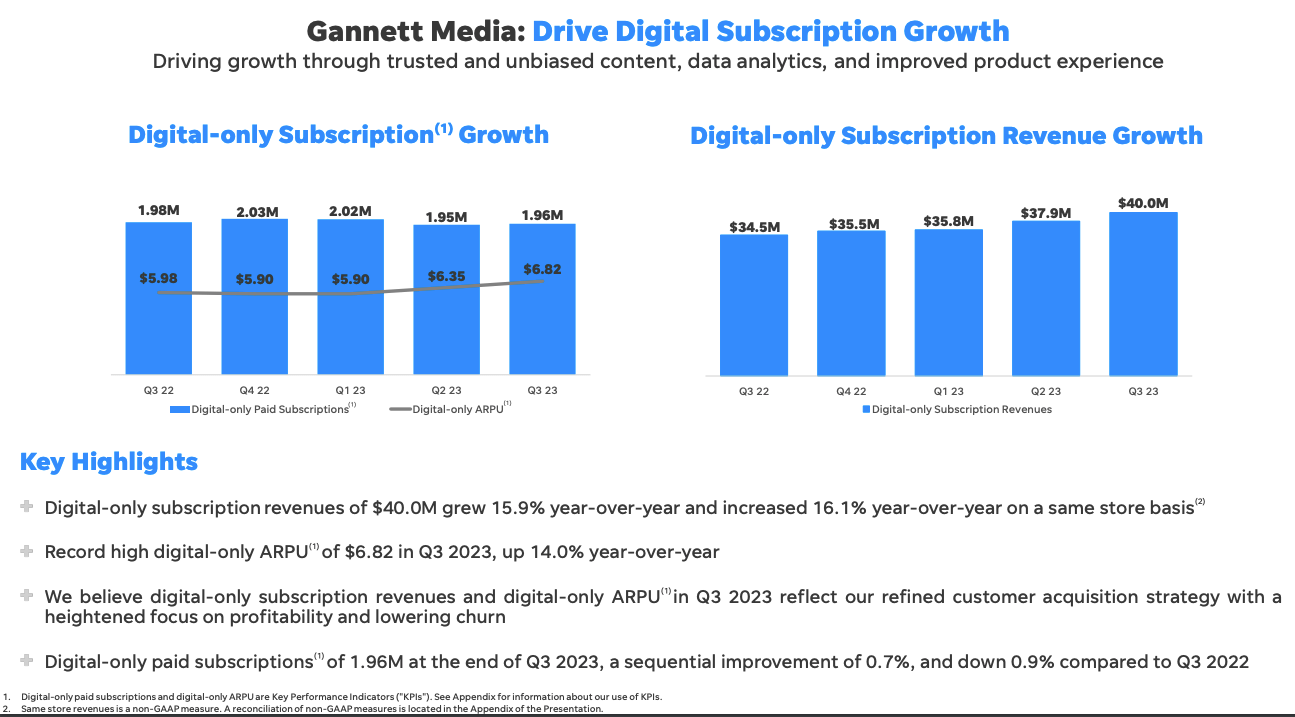

Another relatively disappointing part of the Q3 earnings release was the fact that digital revenues increased just 2.7% compared to the same period a year ago on a same store basis. Digital paid subscriptions for the quarter came in at 1.96 million representing a 0.7% increase from Q2 2023 but down 0.9% compared to Q3 2023.

In response to this development, GCI shares plunged by 25%. During the Q3 earnings call the company blamed the its guidance cut on macroeconomic headwinds:

While we made great strides on our strategic priorities, we must acknowledge the complex economic environment in which we are operating. We believe there are signs that consumers are beginning to feel the cumulative impact of higher interest rates and continued inflation which has led to an overall reduction in consumer confidence. As a result, the small and medium-sized businesses we serve have become more cautious in their approach to advertising expenditures than we had previously seen.

These results are particularly disappointing as peers have reported better results. For example, The New York Times ( NYT ) reported a 9.3% increase in revenue, a 13.7% increase in digital revenue, and a 9.5% increase in digital subscribers all on a year-over-year basis.

Given this, the difference in relatively trajectory I am concerned that GCI may be experiencing company specific issues and not simply advertising softness due to a weaker economy.

{kind=link}

{kind=link}

2. The company has a highly leveraged balance sheet and may struggle to refinance its existing debt

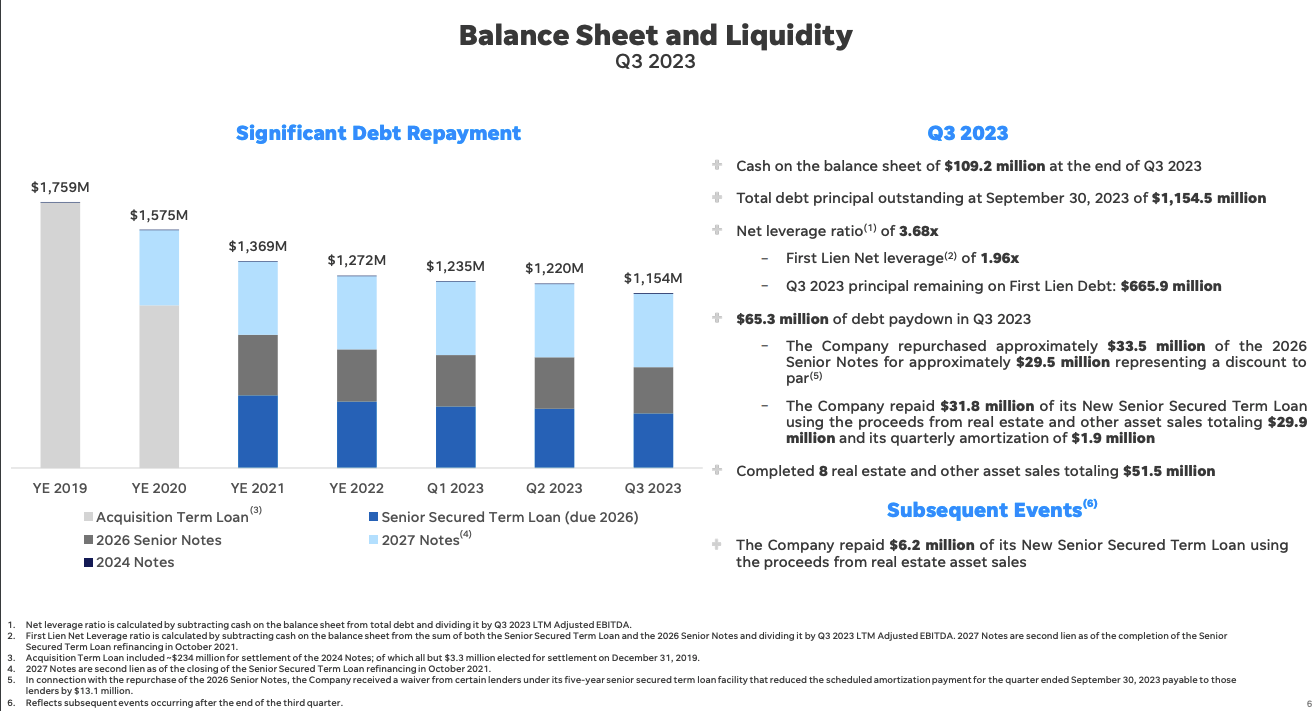

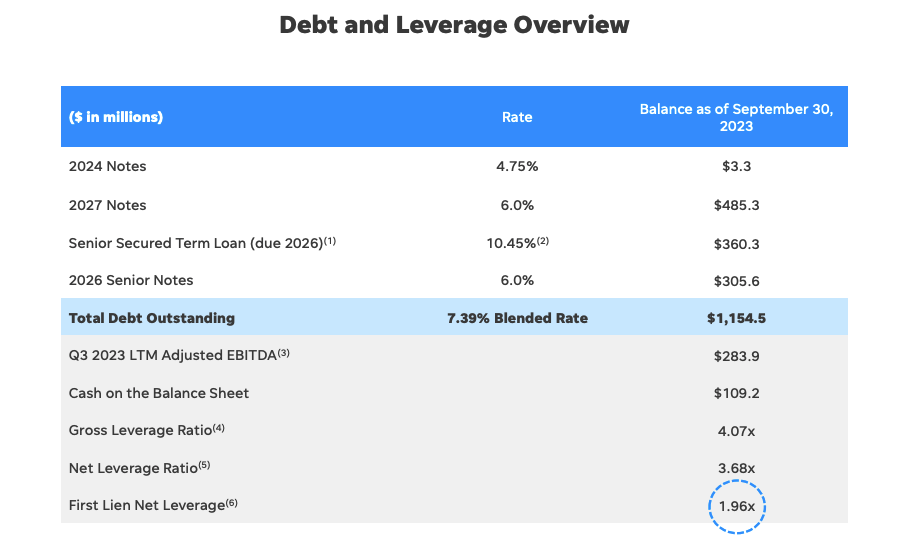

While GCI has made considerable progress improving its balance sheet over the past few years, the company remains highly levered. As of Q3 2023, GCI had a total net leverage ratio of 3.68x and a gross leverage ratio of 4.07x. I view this as a fairly high level of leverage for any company let alone one that has struggled to achieve profitability.

Currently, GCI has a blended cost of debt of 7.39%. While this rate is very attractive given the current level of interest rates it is likely that GCI will experience a significant increase in its blended cost of debt once it is forced to refinance the $305.6 million in 2026 Notes and $485.3 million 2027 Notes.

Given the current level of interest rates and risk associated with a highly levered relatively cyclical company I believe GCI would be forced to pay at least 12% to refinance these notes. The result of this would be an additional ~$47.5 million in annual interest expense.

To put this number into context consider the fact that GCI expects to generate free cash flow of $65 - $85 million for FY 2023.

In a best case scenario, GCI may be able to generate enough cash flow over the next two years to reduce the amount of debt it needs to refinance. In a worst case scenario, GCI may experience cash burn and EBITDA deterioration in the event of a recession which has the potential to make refinancing at any level of rates challenging or impossible.

GCI may be able to manage its balance sheet but there is very little margin of error.

{kind=link}

{kind=link}

3. Print media business continues to struggle and still accounts majority of revenue

Digital revenue accounts for just 40.4% of total revenue and thus print related revenue remains GCI's primary revenue driver. The print business continues to experience sharp declines due to a secular shift towards online media.

During Q3 2023, GCI reported an 11.1% decline in print advertising revenue compared to the same period a year ago on a same store basis. Print circulation revenues, which account for 28.7% of the company's total revenue, fell by ~19% during Q3 2023 compared to the same period a year ago. These declines are staggering and represent a key headwind for GCI. Comparably, The New York Times reported just a 1.8% decline in print subscription revenues for Q3 2023. Similarly, New Corp ( NWSA ) reported that circulation revenue at Dow Jones, publisher of T he Wall Street Journal, fell by ~1% during Q3 2023 compared to the same period a year ago.

These results suggests that the USA Today and other key print properties owned by GCI are performing considerably worse than other print publications. This is a major negative given the company's continued reliance on the print media business.

{kind=link}

{kind=link}

4. Lack of any near-term catalyst

Some might argue that GCI is a cheap stock based on the fact that it trades at forward EV/ EBITDA of just 5.3x compared to peers such as NYT and NWSA which trade at 18.5x and 10.4x forward EV / EBITDA multiples. While GCI is a weaker business, it could be argued that the valuation discount should be smaller than is currently the case given GCI's strong digital marketing services business.

However, I do not currently see any catalyst which suggests that GCI is set to close this valuation gap anytime soon. The company has a $96.9 million share repurchase authorization but it appears highly unlikely that the company will repurchase any shares in the near-term given balance sheet challenges.

It also seems highly unlikely that the company would be acquired by another media company given its high debt load.

The Bull Case

The bullish case for GCI centers around the potential value of its Digital Marketing Solutions ("DMS") business which offers a cloud-based platform of products to enable small and medium-sized businesses to accomplish marketing objectives.

During Q3 2023, DMS achieved LTM Revenues of $479 million and LTM Adjusted EBITDA of $57mm. Some have argued that DMS may be conservatively worth ~$800 million. However, I do not see a near-term path to monetization of that asset. That said, the potential value of this asset does keep me from rating GCI as a sell.

The bulls also believe that GCI will be able to experience significant growth in its digital business. While this may be possible, recent results have been highly disappointing compared to other platforms which leads me to question the long-term earnings potential of GCI's digital offerings.

Conclusion

GCI has delivered weak results for shareholders over the past few years and is trading at depressed levels.

Other Seeking Alpha analysts are bullish on the stock but I am more cautious. Weak Q3 results compared to peers suggest the company may be facing company specific issues related to its print and digital media publication offerings.

GCI has improved its balance sheet over the past few years but remains highly levered. The company is likely to experience a significant increase in interest expense over the next few years as existing fixed rate debt will need to be refinanced at much higher rates. However, I believe GCI could manage to refinance its debt at a reasonable cost if it is able to pay down a significant portion of its debt using free cash flow over the next two years. That said, the balance sheet will prove difficult to manage through even a moderate economic decline.

The company's near-term revenues remain primarily driven by print advertising and circulation revenue. GCI's print business has performed very poorly both on an absolute basis and vs peers suggesting company specific issues have played a role in the sharp decline of the business.

GCI trades at a very cheap valuation vs peers but lacks any near-term catalyst. One potential catalyst would be some form of monetization of GCI's DMS business.

I am initiating GCI with a hold rating but would consider upgrading the stock to buy if a monetization catalyst emerged surrounding its DMS business or if the company were to substantially improve its balance sheet.

For further details see:

Gannett: 4 Reasons Why I Am Cautious