GCI - Gannett: Extraordinarily Undervalued And On The Cusp Of Revenue Earnings Growth

2023-10-02 15:17:48 ET

Summary

- Gannett has undergone a four-year transformation into a digitally focused media and marketing solutions company.

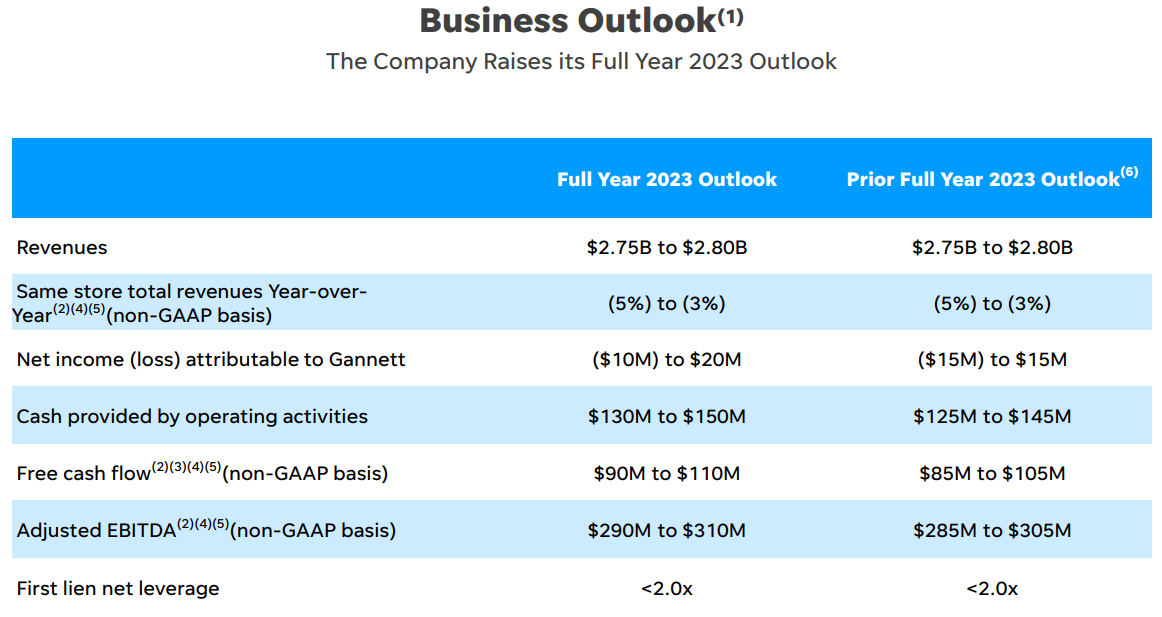

- The company has exceeded its own estimates and raised guidance for the full year in the first and second quarters, with a return to overall revenue growth expected in 2024.

- Gannett's Digital Marketing Solutions (DMS) business is a key driver of growth, with potential value estimated at $800 million to $1 billion.

- A new shareholder greatly reduces the risk profile of the company moving forward.

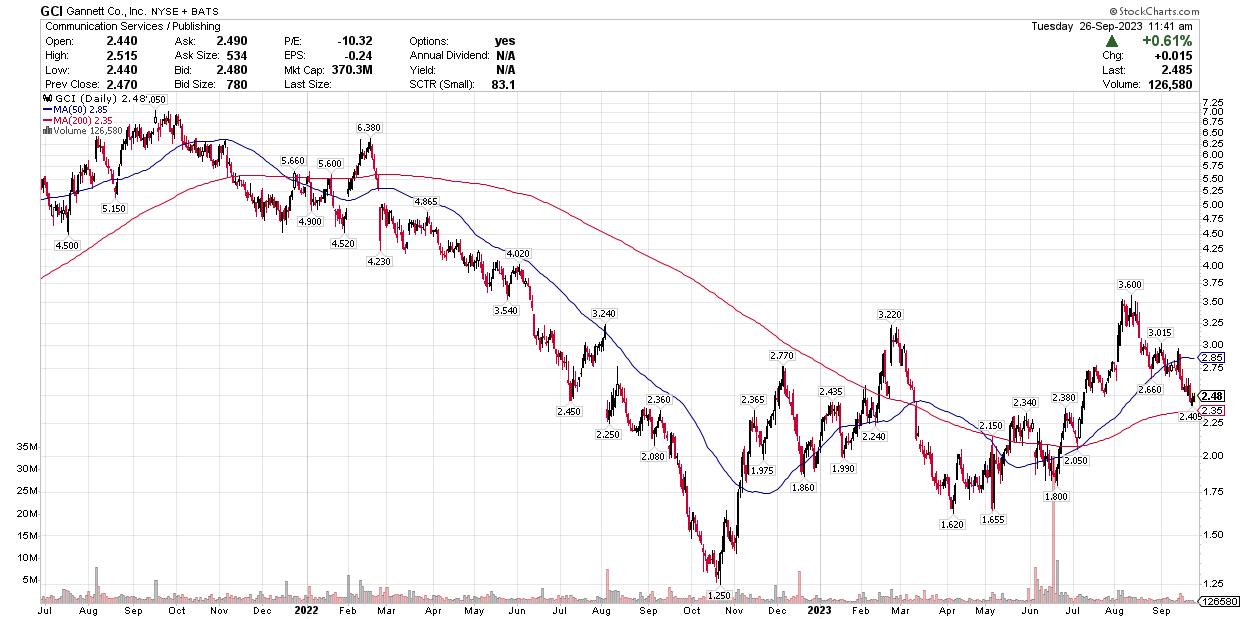

Since July 2021, I have chronicled Gannett's ( GCI ) transformation from the nation's largest newspaper operator into a digitally focused media and marketing solutions company, but very few investors have paid attention. The proof is in what has been abysmal stock price performance over the past two years, which begs the question, is this a classic value trap or an undiscovered gem with outsized growth potential that is waiting to be recognized?

{kind=link}

Following Gannett's merger with New Media in November 2019, CEO Mike Reed and his team were tasked with cutting costs, reducing debt, improving margins, and rebuilding a $3 billion revenue stream that was predominantly focused on the legacy print business. In that process, digital revenues have grown from 25% to what is now 39% of the total in an effort akin to turning around the Titanic.

Along the way, management navigated a pandemic, a recession, hyperinflation, negative sentiment, short sellers who now command 15% of the float, expulsion from several index funds in June, and some of the most short-sighted and misinformed Wall Street analysis I have ever seen. Despite this uphill battle, it looks like the company will soon reach two important milestones, which will make it more difficult to continue carrying a valuation that stokes fears of bankruptcy. The persistently depressed valuation in and of itself has become one of the greatest headwinds for shareholders and management, which needs to change very soon.

A Return To Growth

Gannett exceeded its own estimates and raised guidance for the full year after both the first and second quarter results, and I suspect we will see more of the same when third-quarter numbers are reported next month. It looks like the company will finish 2023 with positive net income, free cash flow of approximately $100 million, and adjusted EBITDA of $300 million. I think there is upside in these figures between now and year end.

{kind=link}

This sets the stage for a return to overall revenue growth in 2024 for the first time since the merger, which should be accompanied by positive net income and free cash flow growth on a more consistent quarterly basis. After four years, it looks like the Titanic has finally completed its 180-degree turn.

Deleveraging The Balance Sheet

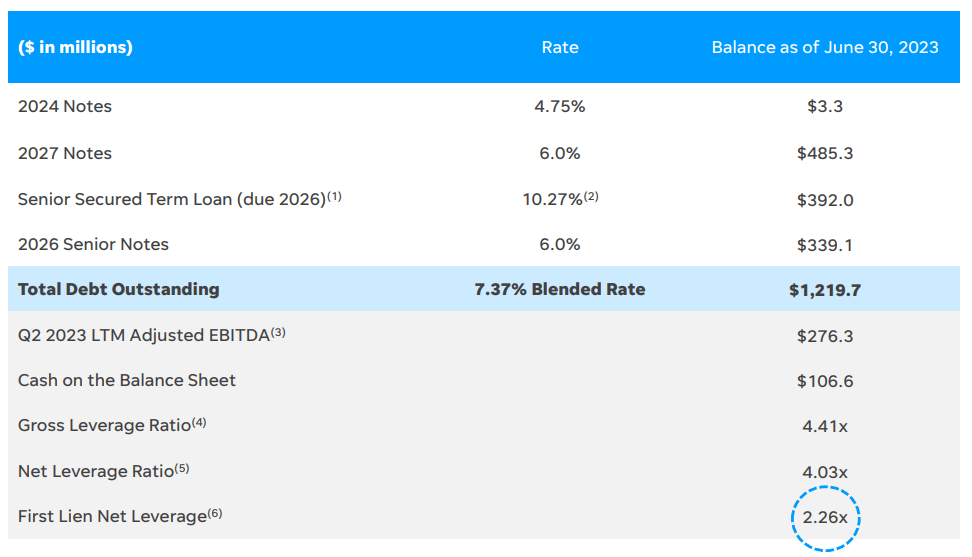

After two debt repayments made during the third quarter, it appears that another important milestone has been hit ahead of schedule. Gannett used real estate sale proceeds of $44.4 million to pay down $28.4 million of its senior secured term loan and repurchase $18.5 million of its 2026 senior notes at a discount to par with another $16 million. Weeks later it repurchased an additional $15 million of the same notes at a discount with $13.1 million it held in cash on its balance sheet. This brings the total debt reduction to nearly $62 million in the third quarter alone.

These actions take total debt outstanding down to $1.158 billion, and first lien debt (senior secured term loan + 2026 senior notes) down to $669 million. Assuming there is approximately $100 million in cash on the balance sheet as of the end of last week, first lien net debt falls to $559 million. I think this guarantees that management has achieved its year-end goal of reducing first lien net leverage below 2.0x a full three months ahead of schedule. I am assuming that trailing 12-month adjusted EBITDA will be greater than $280 million when the company reports third quarter results.

{kind=link}

Digital Is The Engine Of Growth

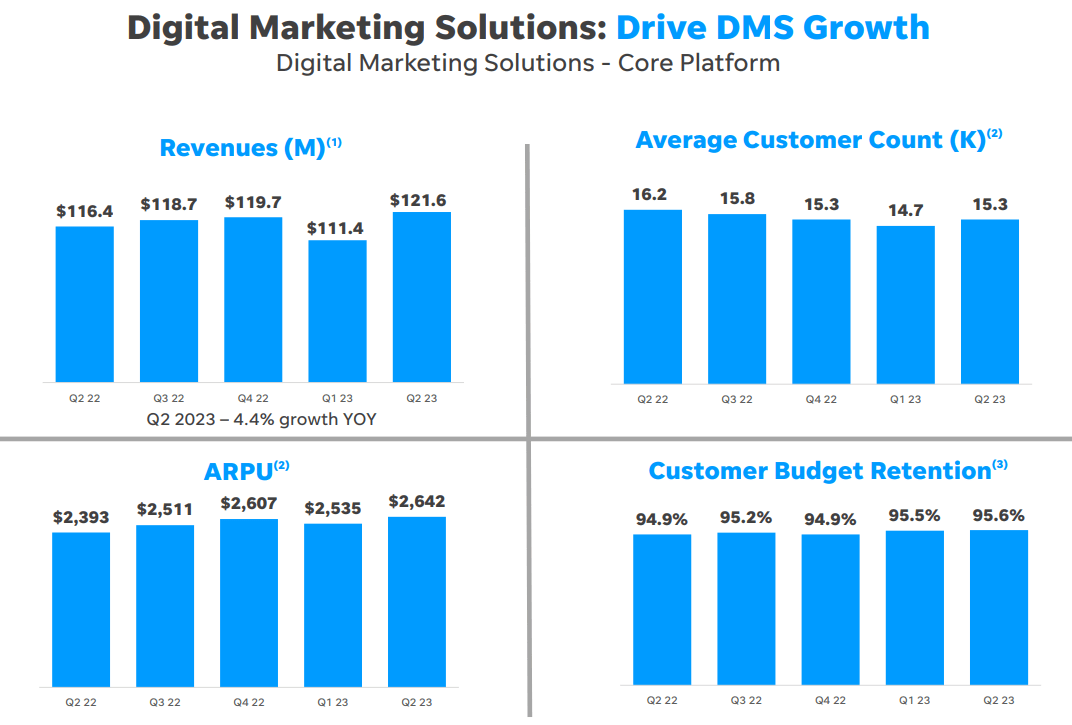

From an operational perspective, the crown jewel of the company continues to be its Digital Marketing Solutions (DMS) business, which offers a suite of cloud-based products and services on its LocaliQ platform to more than 15,300 small-to-medium size businesses. It operates as any other software-as-a-service (SaaS) company, whereby its customers license products and services from a menu on a subscription basis.

{kind=link}

DMS just achieved record quarterly revenue of $121.6 million, as well as record average revenue per user (ARPU) of $2,642 per month, which resulted in trailing 12-month revenue of $477 million and adjusted EBITDA of $59 million. What is DMS worth?

{kind=link}

To provide some context, consider another SaaS company called YEXT, Inc ( YEXT ), which is very similar to DMS in that it also offers a suite of cloud-based products and services on a subscription basis to corporate customers with a focus on improving the digital experiences consumers have with these corporations. YEXT has trailing 12-month revenues of approximately $400 million and adjusted EBITDA of $50 million. The share price has fallen significantly over the past two months during the market correction, but the company still commands a market cap of nearly $800 million.

DMS is not only a larger business, but it has a faster top-line growth rate and higher profit margins. Therefore, I think it is safe to assume that DMS is worth at least $800 million on a stand-alone basis. In fact, it deserves a market cap of at least $1 billion, based on this comparison, if it were a public company. Yet it is imprisoned inside Gannett's market cap of just $350 million.

Aside from DMS, revenues from some two million digital consumer subscriptions rose an annualized 17.3% in the second quarter to nearly $38 million, which was also record quarterly revenue. The combination of DMS and digital subscriptions provides Gannett with a more stable and predictable revenue base on which to build its digital advertising revenues, which are more cyclical. As digital becomes a larger percentage of overall revenues than the 39% achieved so far, we should see improving margins and profitability in 2024.

An Important New Shareholder

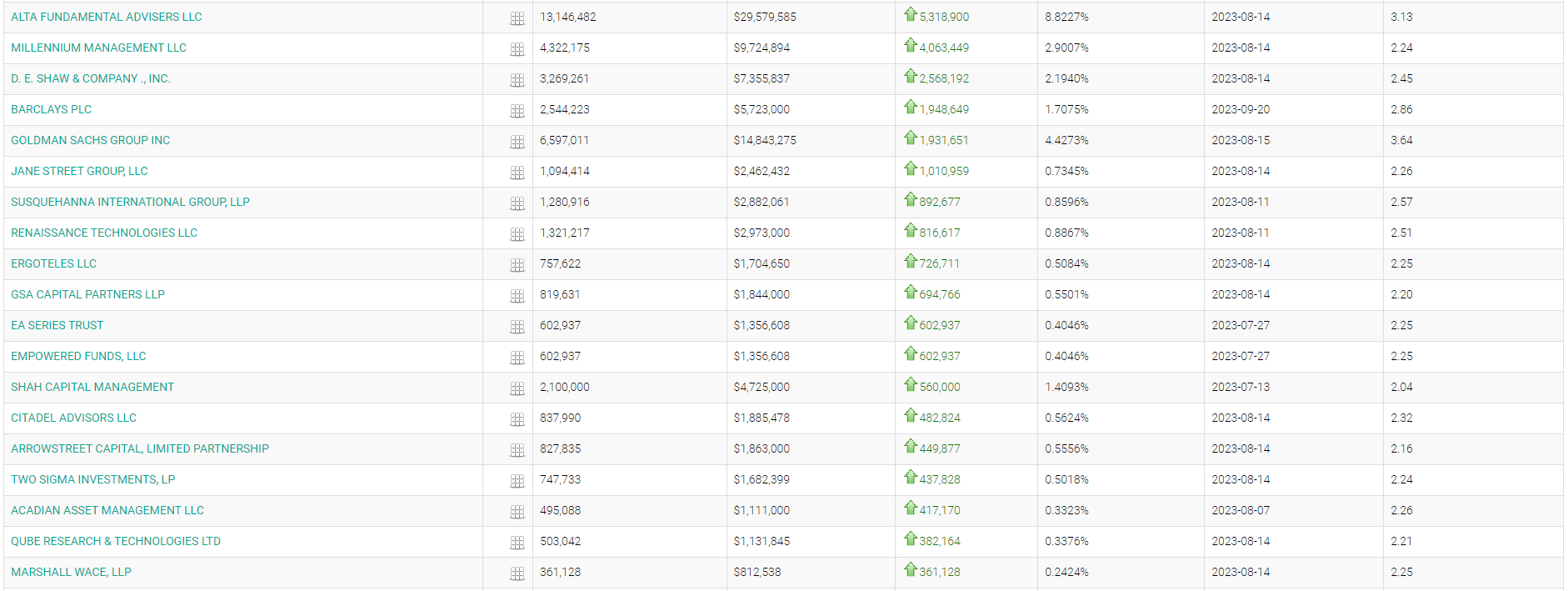

I think the most important development over the past few months for Gannett shareholders was the notification in a 13F filing on June 21 that Apollo Global Management ( APO ) is now the fifth largest shareholder after acquiring more than 7.5 million shares at an average price of $2.25. That amounts to 5% of the outstanding shares. Alta Fundamental Advisors, LLC added 5.3 million shares to its hedge fund's position as well, which could not have come at a better time, as index funds at Blackrock and Vanguard sold shares following Gannett's removal from the Russell 2000 index.

{kind=link}

Following Apollo's disclosure, additional 13F filings in August revealed six new institutional shareholders as of June 30 with more than a dozen existing ones significantly increasing their positions, some of which are shown below.

{kind=link}

Apollo Global Management is a rising financial powerhouse and considered one of the shrewdest investors on Wall Street. The firm is also Gannett's primary lender. Therefore, I suspect their newly announced involvement in the common stock is stoking interest from other institutions about the upside potential of Gannett, but the most important aspect of this development is the message it sends to shareholders about the primary risk of investing in the company-leverage.

Apollo provided $1.8 billion in debt financing at a whopping 11.5% interest rate to support New Media's acquisition of Gannett in late 2019, retaining the Gannett name. Since then, Apollo has refinanced and restructured that debt twice with far more favorable terms for Gannett, allowing the company to pay down more than $600 million of the original balance.

Today, the senior secured term loan has a variable rate, which has increased significantly with the rise in short-term rates, but the balance is down to approximately $363 million. Apollo restructured $500 million of the original loan balance into convertible notes that mature in 2027 with a 6% coupon, which can be exchanged for shares of common stock at $5. The convertible balance is down to $485 million. Lastly, there remains $305 million of the 2026 senior notes with a 6% coupon, which Apollo syndicated.

Therefore, Apollo remains the primary lender to Gannett, and it now stands as one of its largest shareholders. If Gannett was a credit risk, why would Apollo be buying the common stock? In other words, Apollo sees so little credit risk in Gannett, in addition to the deep value proposition, that it is buying the common stock. In my view, this takes credit risk off the table. There is one more reason why new institutional investors may be accumulating shares.

The Lottery Ticket

Gannett announced its lawsuit against Google in June, claiming it violated antitrust and consumer protection laws, which resulted in billions of dollars in lost advertising revenue for the company. This lawsuit is piggy backing the one filed by the Department of Justice and a coalition of 34 states, which has a trial date set for this coming March. Gannett is being represented by Kellogg Hansen, which is a highly recognized and successful antitrust law firm. I suspect that Google may settle their case with the DOJ before it goes to trial, which should establish some liability. That would greatly increase the probability of a settlement with Gannett, which could amount to as much as $1 billion. Even a third of that amount would be a gamechanger for the balance sheet of Gannett. I suspect we will have a lot more information over the coming six months, especially if Google wants to avoid a trial.

The Upside

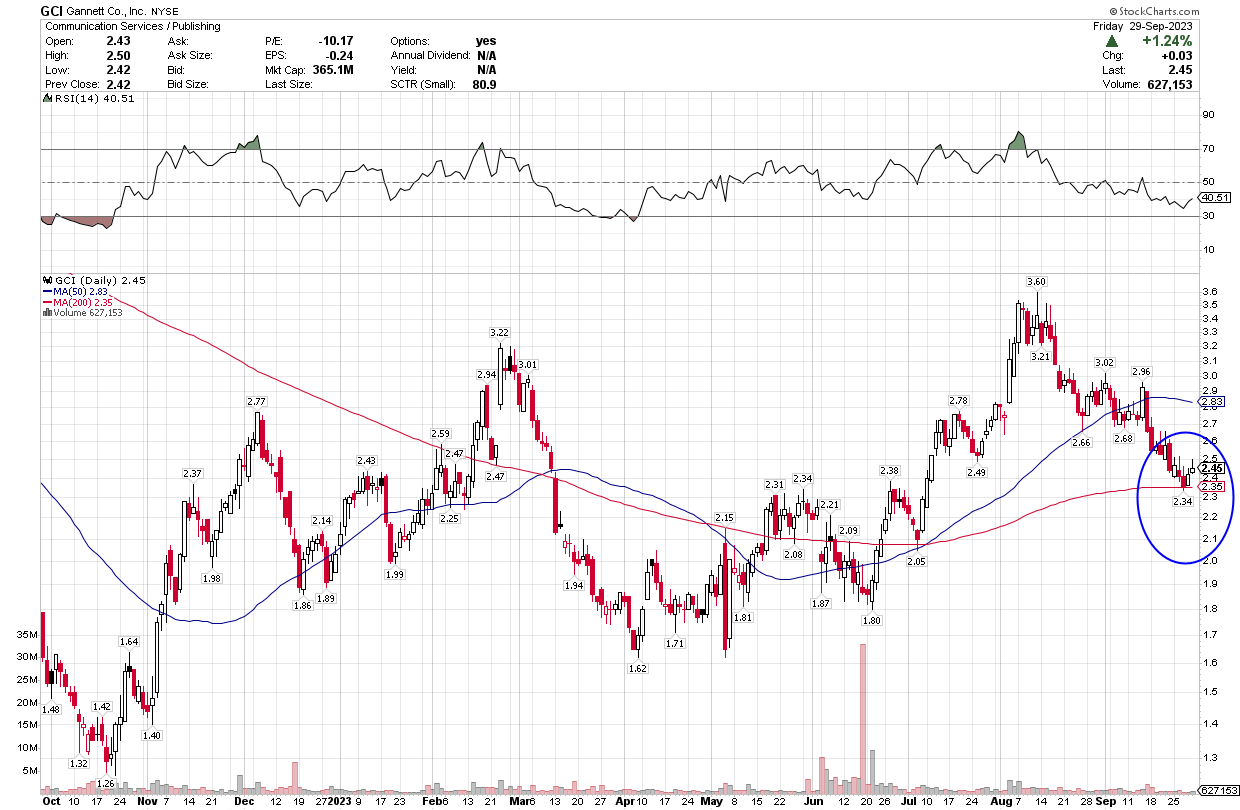

Sadly, Gannett's stock at $2.45 has been reduced to a call option with no expiration date, which is why I think its primary lender, holding all the purse strings, is buying shares. On that basis, the downside from current levels seems to be minimal in my opinion. Additionally, in the process of turning over some 30 million shares when index funds were forced to sell, the dozens of institutional investors who built positions did so in the $2.25 to $2.50 range, which is approximately where the 200-day moving average is at $2.35. This certainly seems like the floor.

{kind=link}

As for the upside, I think the simplest way to value Gannett is to assume that it eventually trades at an enterprise value (EV) to EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) multiple equal to the industry average, which is approximately nine times. Note that the New York Times ( NYT ) trades at a multiple of 18, while New Corp ( NWS ) trades at more than 12 times.

If we use net debt of $1.060 billion, which is where I think Gannett finished the third quarter, and add the market cap of $350 million, we arrive at an enterprise value of $1.410 billion. If we divide $1.410 billion by this year's projected EBITDA of $300 million, we come to a multiple of 4.7 times, which is the lowest I can find among publishers. Expanding the multiple to nine times results in an enterprise value of $2.7 billion, which necessitates increasing the market cap by nearly $1.3 billion. Therefore, divide $1.65 billion by 140 million shares and you have a $11.78 stock price.

Perhaps Gannett does not deserve the average multiple, so let's reduce it to just six times, which is just below the multiple awarded to its much smaller competitor in Lee Enterprises ( LEE ). Using the same calculation, we arrive at a stock price of $5.28, which is still more than a 100% return from today's price. Apollo may be on to something buying stock at $2 and change. These valuation estimates do not account for anything other than a more modest discount to the industry average multiple. Therefore, when are investors (and an analyst or two) going to wake up and get it?

Something Has To Change

Gannett is clearly not a value trap, because its financial stability continues to improve, as the digital side of the business expands with increasing growth potential. Most importantly, Gannett's primary lender is now one of its largest shareholders, which speaks volumes about the upside in the stock price. That said, more aggressive steps need to be taken by management to awaken investors to this fact. The Titanic needs to turn into more of a speed boat.

Four years into its digital transformation, as we have seen over the past 12 months, merely inching its way towards revenue growth and profitability is not going to revalue the stock. In other words, nickel-and-diming the $1.158 billion debt balance with paydowns of $10-25 million and raising guidance for the year by $5 million each quarter is not generating a lot of investor interest. Otherwise, the stock would not still be a plaything for short sellers and day traders, whereby every meaningful rally is sold on light volume, evaporating the gains. Nor would the enterprise value continue to shrink, as the stock price declines alongside its gradually shrinking balance of debt.

I would like to see management buy back stock in a meaningful way to notify short sellers and investors that the stock is absurdly cheap. CEO Mike Reed seems to be the only one who thinks so with his own outsized purchases over the past year. With free cash flow of $100 million or more in 2023 and expectations that it will grow moving forward, it makes no sense to not complement debt reduction with a repurchase program of 10% ($35 million) of the float up to at least $4/share. That would excite and broaden the investor base and give short sellers second thoughts.

In terms of building that base, I still find it staggering that Gannett cannot garner a single buy recommendation from the analyst community on Wall Street, much less convince the few who have been assigned the task of following the stock, but clearly do not, to remove their sell recommendations. We need reputable and realistic coverage that will expand the shareholder base, increase daily volume, and reduce volatility in the stock price.

Lastly, the most significant catalyst would be the spin-off of DMS, which would unlock a valuation that could be worth more than Gannett is today. DMS already operates as a separate business unit, and a spin-off would not limit the upside in capital appreciation for shareholders as would an outright sale of the business. The bottom line is that something must change. Time is money, and the clock is ticking.

For further details see:

Gannett: Extraordinarily Undervalued And On The Cusp Of Revenue, Earnings Growth