NYT - Gannett's Digital Transformation Remains On Track

Summary

- The digital transformation of Gannett over the past three years continues, yet its stock price reflects none of the progress.

- The pandemic-induced recession in 2020 and surge in inflation during 2022 were both major headwinds for progress.

- Management continues to respond with steps that are putting the company back on track.

- Look at the transformation of the New York Times over the past ten years as a roadmap for where Gannett is headed.

- The stock is cheaper today than it was at the depths of the pandemic and bear market in 2020.

In the three years since New Media investment Group acquired Gannett ( GCI ) to form the largest newspaper company in the country, retaining the Gannett name, the combined enterprise has lost 78% of its market value. The share price has fallen from $6.70 to $1.44. Therein lies the initial investment opportunity, as the new Gannett has made huge strides in its transformation from a traditional print media operation into a subscription-led and digitally focused media and marketing solutions company. At a minimum these shares should be worth $6.70 today, which would account for management’s achievements over the past three years, as well as the far more challenging macroeconomic environment the company now faces. From my perspective, that is the easy money to be made. Yet a sum of the parts analysis reveals that these shares should garner a much higher valuation in the year ahead, as management continues to monetize non-core assets, deleverage, reduce costs, and return to profitability and free cash flow growth in 2023.

The Progress

In addition to gradually transforming the business from a print to digitally focused operation, management has made exceptional progress in strengthening the balance sheet and improving operational efficiencies since the acquisition.

- Achieved $325 million in annual expense reductions and initiated an additional $200-240 million in cost cuts last quarter to be completed by year end.

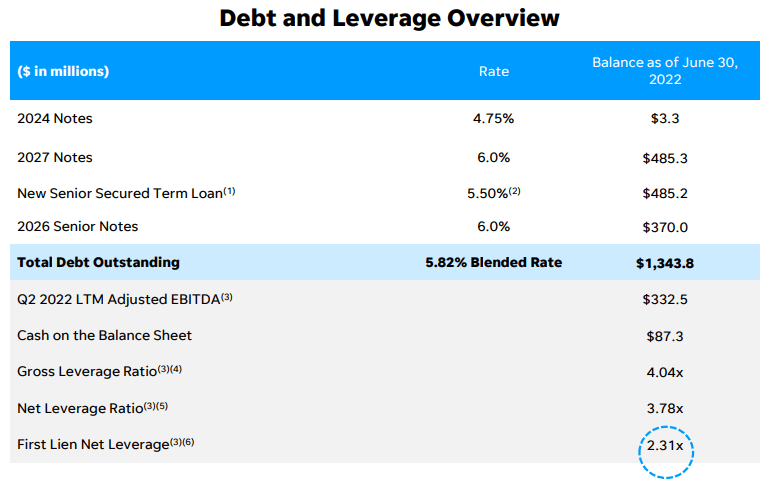

- Reduced debt outstanding by more than $585 million to approximately $1.3 billion.

- Refinanced the cost of the remaining debt from 11.5% to 5.8%.

- Increased digital revenue as a percentage of overall revenue from 22% to 35%.

The important thing to focus on is that debt and interest expense have declined every quarter since the acquisition, while digital revenues have consistently grown. That should continue moving forward in what I believe to be an inevitable recipe for success with timing as the only issue. The timeline has been interrupted twice by macroeconomic factors largely out of management’s control.

The Potholes

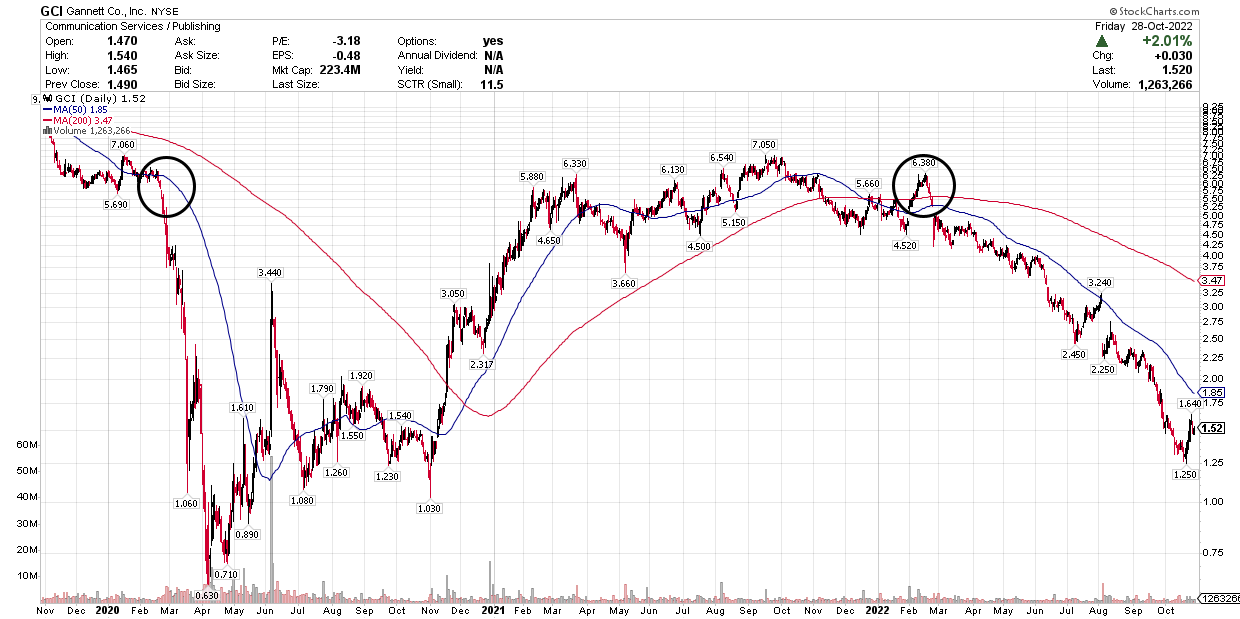

There were two enormous potholes over the past three years, which can be seen in the chart below. The first was the pandemic-induced recession that basically shut down the economy during the summer of 2020, sending the share price cascading to less than $1 at the height of the panic. That was a phenomenal investment opportunity in hindsight. As the economy reopened, the stock recovered rapidly over the subsequent 12 months to regain all it had lost. Significant progress was made during 2021 by achieving double-digit margins, positive net income, and strong free cash flow growth. That success prompted management to announce a $100 million share repurchase program in February of this year, which approximates nearly 50% of today's market value, but the stock buybacks came to end before they had time to start.

{kind=link}

Stockcharts

The second pothole, which we find ourselves in right now, came shortly after in the form of skyrocketing input costs primarily related to the print business. There was an abrupt surge in expenses for paper, ink, and fuel combined with wage pressures and a labor shortage that adversely impacted distribution. This resulted in a $23 million increase in costs during the second quarter alone. Management was forced to lower guidance for the year in August by reducing adjusted EBITDA from $380-400 million to $270-300 million and largely eliminating what was expected to be $170 million in free cash flow. CEO Mike Reed did not sit idle.

He responded during the third quarter with a new cost reduction initiative focused on the print business that is expected to produce $200-240 million in annualized savings by the end of this year. That means there should be meaningful results in the fourth quarter that puts the business back on track for growth in 2023, especially once the inflationary pressures ease. This is a far less severe situation than what the business faced during the pandemic, yet the shares are flirting with the same price level, which I think presents just as attractive an investment opportunity as we had during the pandemic.

I don’t see the potholes, which are temporary, as wiping out the progress, which continues, to the extent that this company should have lost 75% of its market value over the past three years. It is ridiculous. To further build my case, I will detail the developments in each segment of the business and the value each contributes to the overall enterprise. That will show how inefficient the market is in valuing this company today.

The Sum Of The Parts

Gannett recently surpassed $1 billion in annualized digital revenues, which is competing with approximately $2 billion in annualized revenues derived from the legacy print business. I say competing because print revenue has eroded by 8-10% per annum, while digital revenue has grown by 8-10%. Still, the print business generates a tremendous amount of cash that has helped to fund growth of the digital enterprise.

The objective with print is to slow its deterioration through enhanced product offerings, improved productivity, and the opportunistic divestiture of non-performing and non-core assets to pay down debt. Management has seen success on this front. The goal is to sustain this business, which accounted for 55% of the $750 million in revenue reported in the second quarter, until the digital business is holding the reins. That said, the reason to own Gannett is for the growth in its digital business.

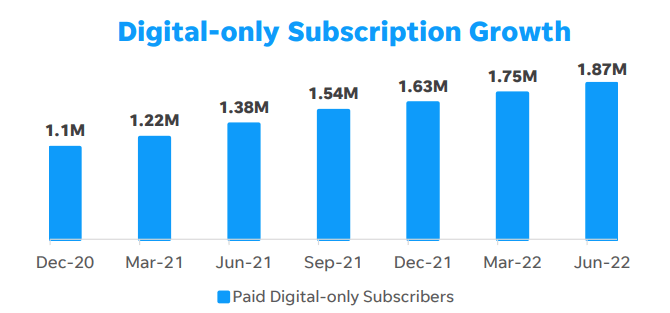

Digital subscriptions should come close to two million when the company reports third quarter results tomorrow, but the ramp in subscriber growth is still in front of us. Gannett’s flagship paper being the USA Today has only recently been launched as a digital product nationwide and commands just 5% of its overall subscription base. Gannett prospects for subscribers from the 165 million monthly visitors to its various sites by obtaining email contact information (8.5 million) and converting those contacts into registered users (4.9 million) who are more likely to become paying subscribers. Contact and registered user growth has been 40% over the past year. Digital circulation, which is in its infancy, is producing an annualized $130 million in revenue, while digital advertising is approaching $400 million. Management has a goal of 6 million digital subs by the end of 2025, which should be obtainable with its vast base of prospects and growing number of product offerings.

{kind=link}

Gannett

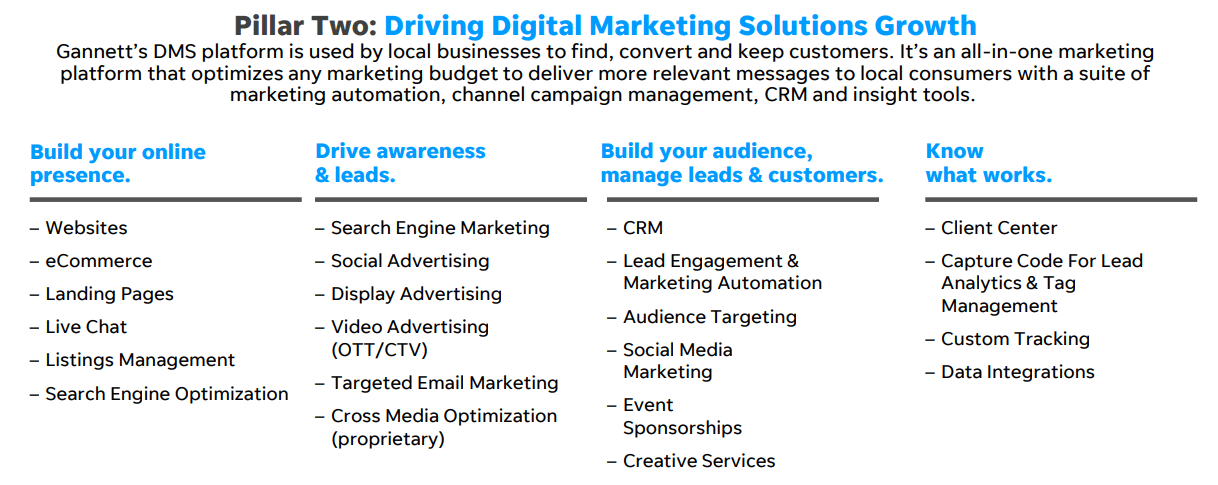

The other half of Gannett’s digital revenues come from its Digital Marketing Services business ('DMS'), which operates under the brand name LocaliQ. For those who were around in the late 1990s, I like to think of DMS as the Palm inside of Compaq Computer before it was spun off in an IPO. If DMS were a stand-alone publicly trading company today, its market cap would undoubtedly dwarf that of Gannett in my opinion.

DMS is a cloud-based suite of products serving more than 16,000 small-to-medium sized business customers (SMBs) in all the capacities you see below. It operates under a software-as-a-service model (SaaS) with sales and service reps helping business owners select from the suite of products.

{kind=link}

Gannett

It recently launched a “freemium product” in the second quarter, similar to other SaaS operators, whereby it offers do-it-yourself products for free to SMBs with marketing budgets of less than $12,000. This is a proven strategy to significantly increase new customers with minimal acquisition costs. Freemium had already generated more than 7,000 registered users by the end of June.

{kind=link}

Gannett

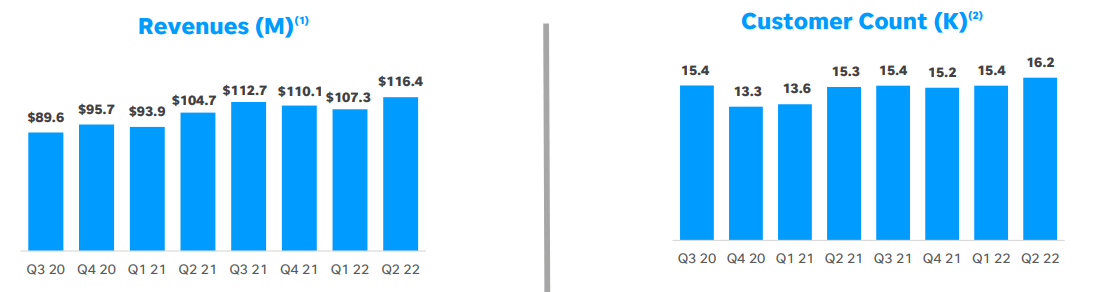

Over the past 12 months DMS has generated $458 million in revenue and $55 million in adjusted EBITDA, growing both at double-digit rates with margins of better than 12%. Customer retention has held steady at approximately 95%, and recurring revenue is 63% of the total. The most attractive aspect of this business, unlike advertising, is that it has shown minimal cyclicality, which is extremely important for consistent overall growth in digital revenues.

What is DMS worth? Consider that Zendesk was acquired in June by a group of buyout firms for more than 6 times sales. Zendesk offers a suite of software products for companies under a similar SaaS model as DMS, growing its top and bottom line by better than 20% in 2022. If we cut the multiple in half to account for what is still a double-digit rate of top and bottom line growth, DMS would have a market value of approximately $1.5 billion. This value is obviously nonexistent in Gannett’s $205 million market cap, similar to what Compaq Computer experienced with its Palm division until the IPO. Again, it is an emerging growth stock trapped inside one that is deep value.

The remaining 10% of Gannett’s revenues come from its commercial print and distribution business and its events business, which operates under USA Today Network Ventures, hosting a variety of special events and endurance races nationwide for hundreds of thousands of participants each year. Those two businesses combined have shown impressive growth over the past 18 months alongside the digital business at a time when advertising revenues have suffered. Therefore, a more equitable split between that which is growing and that which is eroding is 45% and 55%, respectively.

I see the sum of these parts being worth a lot more than the $205 million market cap that Gannett commands today. Critical to realizing greater value will be a further deleveraging of the balance sheet, especially considering the revised guidance for adjusted EBITDA and free cash flow. Prior to the revised guidance, management was forecasting a 40% compounding annual growth rate in free cash flow from the $88 million generated last year through 2025. That would have produced $960 million in cash, which is more than enough to retire all of the company’s outstanding debt ($855 million), assuming the $485.3 million in 6% notes due in 2027 convert to approximately 97 million common shares at $5. This does not account for the nearly $40 million in debt retired earlier this month or the additional $35-85 million expected before the end of the year.

{kind=link}

Gannett

With management’s new cost cutting initiative, it is highly probable that Gannett returns to positive free cash flow in 2023, putting it back on track to being debt free over the coming 3-4 years. Additional asset sales, which I expect, would accelerate the time line.

Consider that Gannett had net debt of $1.256 billion ($1.343B debt minus $87M cash) at the end of the second quarter, which combined with its market cap of $205 million results in an enterprise value (EV) of $1.46 billion. Trailing 12-month EBITDA of $332 million gives the company an EV/EBITDA multiple of 4.4 times. The New York Times ( NYT ) trades at an EV/EBITDA multiple of more than 15 times, which is after a near-50% decline in its share price over the past year.

The Opportunity

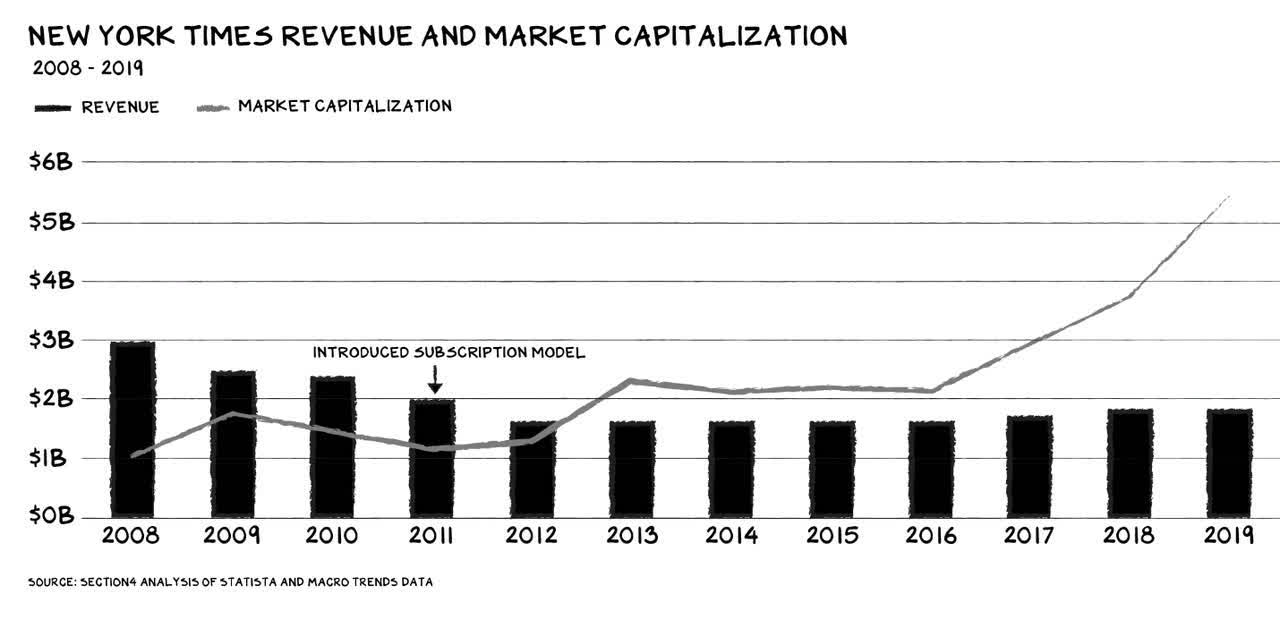

To understand the long-term opportunity in Gannett shares, look no further than the playbook at the New York Times one decade ago when it launched its digital subscription model in 2011 with 400,000 subscribers. It took the New York Times six years to surpass 2 million in 2017, while Gannett will reach that milestone in three. Revenue remained relatively flat as its digital business grew, but it managed to retire all of its nearly $700 million in debt by 2017, at which point margins expanded, net income soared, and its stock price followed, rising more than tenfold by 2021 from its low in 2011. Today, the Times has more than 10 million digital subscribers, but with digital revenues at approximately 55% of its total, it still depends on a print circulation and advertising business. Gannett is not that far behind.

{kind=link}

Section 4

Gannett is following the same playbook, but on an accelerated time line. We don’t need meaningful revenue growth to realize outsized gains in valuation. We need an improved business mix with a more variable cost structure that results in margin increases, which management is back on track to deliver. At the same time, we need to see continued progress on deleveraging the balance sheet, which management has already proven it is executing exceptionally well.

David Einhorn of Greenlight Capital recently opined that “value investing might never come back.” I share his frustration with an investment style that has been out of favor for nearly 15 years but disagree with his conclusion. Inevitably, investors will refocus on low-multiple stocks that are strengthening balance sheets, enhancing operational efficiencies, and improving profit margins to the extent that their share prices are rerated with higher multiples. It is simply a matter of when this happens for Gannett, and with just $1.44 in share price left to work with I see nowhere for this stock to go but up from here.

A significant near-term catalyst for these shares could be the expiration of a poison pill in mid-November that the company executed shortly after the acquisition in late 2019. It was designed to preserve some $435 million in tax loss carry forwards from a change in control, preventing any new investors or groups from acquiring more than 4.99% of the outstanding shares without a waiver. I think this pill limited demand for these shares over the past three years at times when the price was extremely depressed, as it is today. Its expiration should provide those institutions with a significantly higher cost basis the opportunity to capitalize on today’s extremely depressed valuation. I hope to hear more about this during the company’s earnings conference call tomorrow morning.

For further details see:

Gannett's Digital Transformation Remains On Track