GRMN - Garmin: Consumer Electronics Success Story

2023-06-27 22:00:45 ET

Summary

- Garmin has successfully developed a range of products, with a focus on premium products and diversification, resulting in healthy revenue growth and strong competitive positioning.

- The company has opportunities in the growing demand for smartwatches and subscription-based services as well as international market expansion, particularly in Asia.

- Garmin's impressive margins and FCF conversion will support continued distributions to shareholders.

- At its current price, we believe Garmin stock is undervalued.

Investment thesis

Our current investment thesis is:

- Garmin Ltd. ( GRMN ) is a high-quality business, with deep expertise in navigation and GPS, allowing the business to develop a range of market-leading products.

- Revenue growth and margins are strong, although Garmin has faced some erosion in recent periods. We suspect this will gradually subside over the coming years.

- The high free cash flow, lack of debt, and diversified revenue create an overarchingly attractive business, with upside at its current price.

Company description

Garmin is a Swiss company that designs, manufactures, and sells wireless devices globally. They have segments dedicated to fitness, outdoor activities, aviation, marine, and automotive.

Their products range from watches, trackers, and smartwatches to avionics solutions, marine electronics, and car navigation systems.

Share price

Garmin's share price has performed extremely well in the last decade, exceeding the returns of the S&P 500. This has been driven by a gradual improvement in financial performance, as well as a development of the company's capabilities.

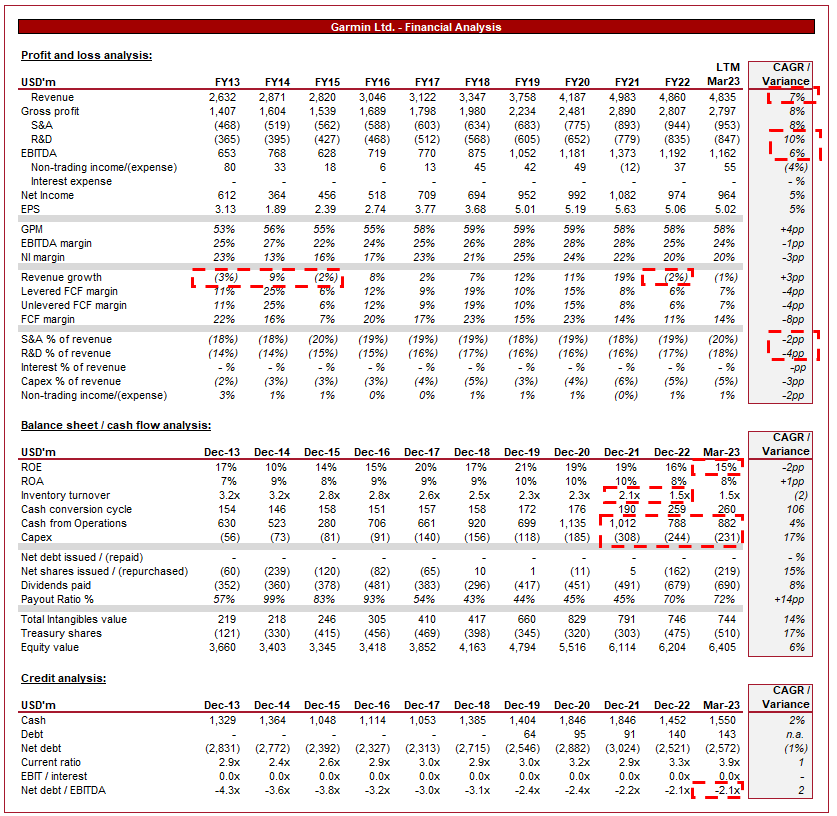

Financial analysis

{kind=link}

Garmin's financials ( TIKR Terminal )

Presented above is Garmin's financial performance for the last decade.

Revenue & Commercial Factors

Garmin's revenue has grown at a healthy CAGR of 7%, with only 3 fiscal years of negative growth, 2 of which were at the start of the period. This reflects a successful pivot by the business toward wearable fitness technology.

Business Model and Competitive Positioning

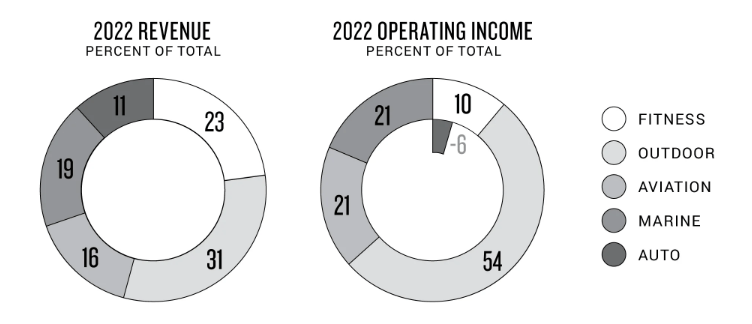

Garmin operates a highly diversified business, with no single segment comprising more than 31% of its revenue.

Garmin's segments provide the following:

- Fitness segment - Garmin offers products such as running and multi-sport watches, cycling devices, activity trackers, and smartwatches.

- Outdoor segment - focuses on adventure watches, outdoor handhelds, golf devices and apps, and dog tracking and training devices.

- Aviation segment - Garmin designs, manufactures, and markets various avionics solutions for aircraft.

- Marine segment - provides marine electronics.

- Auto segment - offers embedded domain controllers and infotainment systems, personal navigation devices, and cameras.

{kind=link}

Revenue split (Garmin)

Garmin's focus revolves around the development of GPS/navigation solutions, seeking to exploit its expertise in the technology to create valuable products for a wide range of consumers. This has been the unwavered focus of the business for several decades, allowing Garmin to develop deep expertise and a strong brand. The company is known for its high-quality and reliable products.

The diversification of its target market has been critical to the continued success of the business, and resilience against changing industry dynamics. Garmin was a leader in the "sat nav" industry, which was subsequently made obsolete by the development of smartphones. That could have been the end of the company had it not continued to develop its breadth of customers/products.

Garmin has emphasized vertical integration as part of its operational capabilities, including in-house design, manufacturing, and distribution capabilities. This has contributed to reduced costs but importantly, illustrates a continued focus on innovation and the pursuit of new solutions.

Garmin's competitive position revolves around its strong brand, broad product base (and intellectual property), scale, and expertise. We believe these factors provide Garmin with a defensible position in its core markets.

Garmin's Industries

In recent years, we have seen a rapid increase in the demand for wearable smart devices, namely smartwatches. This has been driven by technological development creating the feasibility of the product, as well as the development of smartphones to support integration. Garmin has invested heavily in this technology, focusing on its core capabilities, and marrying it with premium components to build a range of high-quality products.

Unlike others, Garmin's focus has always been on the premium segment, ensuring its products had the best of what consumers desire, namely reliability, battery life, and ruggedness. This has protected the business against the recent trend of cheap wearables imported from the far east, significantly disrupting the "fashion smartwatch" segment.

Covid-19 and a greater awareness of a healthy lifestyle have contributed to a growing interest in outdoor recreational activities such as hiking, biking, and camping. We believe this is a natural tailwind that will support the justification for an investment in wearable technology, encouraging purchases.

Various Garmin products target the outdoor segment, although are focused primarily on professionals. The approach allows for the development of its brand in the sticky segment of the market, although makes winning over casuals more difficult (justifying price).

The continued development of smartwatches by leading mobile manufacturers such as Apple ( AAPL ) and Google ( GOOG ) is a threat, but we believe the inherent target market is different. Garmin's target care more about health and GPS, whereas Apple's market is focused on eco-system integration. Not to mention a Garmin measures its battery life in months but days. This said, the gap is certainly closing. If Apple remains committed to the continued development of the Apple Watch Ultra, it could quickly become an issue.

We expect the demand for smartwatches to continue, as although purchases have been high in recent years, the level of penetration in society remains low globally.

The Marine and Aviation industries represent resilient demand for Garmin. Garmin's deep expertise has allowed the business to create market-leading support solutions, supporting both corporates and consumers. As an example, Garmin received multiple supplier awards (8th consecutive year) from Embraer ( ERJ ), the leading aerospace business. These are both industries that should continue to grow well over the long term, generating sustained demand for Garmin, so long as product development is maintained.

Many industries have experienced a shift toward subscription-based services and cloud solutions, as part of the overall product package. The value proposition for Garmin is simple, recurring revenue that can increase periodically with price hikes. Across Garmin's various business units, it has 13 subscriptions. We expect continued focus on this revenue stream in order to develop the value proposition; however, the scope for upselling is seemingly high given the complexity of the services provided.

Emerging markets, especially in Asia, represent key growth markets, as continued economic development contributes to a growing middle class. We believe demand from these regions should support the smartwatch segment, although Garmin must ensure it develops its brand accordingly.

Economic & External Consideration

Current economic conditions represent a key near-term risk to the business. With high inflation and heightened rates, consumers' finances are being squeezed, contributing to reduced discretionary spending. Further, during such times, even those not financially struggling are emotionally encouraged to defer large spending, awaiting an improvement in conditions.

Given the pricing of Garmin's products, we suspect the business could face slowing demand, in the near-term, until conditions begin to normalize.

In the most recent quarter, Garmin experienced a (2)% decline in sales, although the performance was fairly good in our view. 4 of its 5 BUs experienced double-digit growth, offset by a decline in the outdoor BU. This was due to a slowdown in the sale of adventure watches YoY, which we suspect is evidence of a slowdown. The resilience of other BUs is on full display, however, with aviation up 22% and Marine up 10%.

Margins

Garmin currently boasts a GPM of 58%, EBITDA of 24%, and a NIM of 20%. During the historical period, margins have remained relatively flat, as GPM gains have been offset by increased S&A spending.

The movement in margins is driven by overarching operational factors, such as scale economies and, more recently, inflationary pressures, as well as a change in product mix.

Garmin's business units have varying margins, contributing to a change based on growth. As the following illustrates, wearables and Automotive are currently eroding the impressive performance from the others.

| Q1 |

| OPM |

| Growth |

| Fitness |

| 4% |

| 11% |

| Outdoor |

| 23% |

| (27%) |

| Aviation |

| 27% |

| 22% |

| Marine |

| 26% |

| 10% |

| Auto OEM |

| (24)% |

| 11% |

We suspect margin improvement should occur, as demand for Outdoor returns, supplemented by an improvement in Auto OEM. This said, Fitness will continue to represent a downward pressure on margins.

Balance sheet & Cash Flows

Garmin's inventory turnover noticeably declined in FY22 and this has not been subsequently improved. This reflects weaker demand for its product beyond Management's expectations, contributing to a drag on cash.

This said, Garmin's cash flow generation has generally been extremely strong and consistent, allowing the business to fund operations and distribution sustainably, without the use of debt.

Garmin's ND/EBITDA position is currently (2)x, providing the business with scope for raising if required. Management should consider whether M&A could supplement its current strategy, given the ability.

Distributions in the last year have come in the form of dividends and buybacks, although the sustainability of this is lacking given the size of the dividend payments. The average FCF in the last 3 years was ~$730m, which implies further dividend growth is possible.

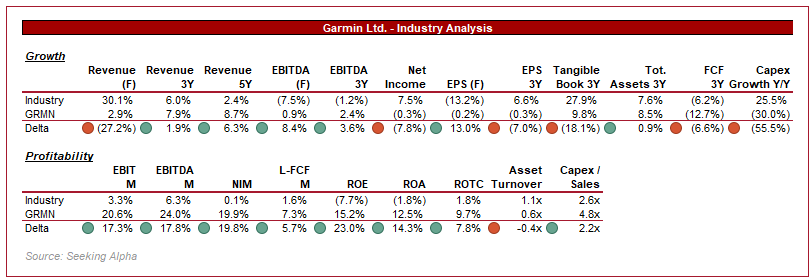

Industry analysis

{kind=link}

Consumer electronics (Seeking Alpha)

Presented above is a comparison of Garmin's growth and profitability to the average of its industry, as defined by Seeking Alpha (11 companies ).

Garmin performs incredibly well on a relative basis, generating superior margins and growth. The Consumer electronics industry is notoriously incredibly competitive, firstly due to the larger tech conglomerates operating across several sub-sectors, and secondly due to the sensitivity of demand to economic conditions.

Garmin's superiority illustrates that it is one of the few that is able to operate on a standalone basis and succeed. If anything, this suggests the company is a fantastic takeover target, amongst a sea of underperformers.

Valuation

Valuation ( TIKR Terminal )

Garmin is currently trading at 15x LTM EBITDA and 14x NTM EBITDA. This is a premium to its 10Y historical average.

Our view is that Garmin justifies this current premium, primarily due to the following factors:

- Growth improvement in the latter half of the last 10Y.

- Underlying strong margins that were improving and will likely continue to do so.

- Impressive FCF conversion, funding distributions, and growth investment.

- Consistent dividend growth.

Key risks with our thesis

The risks to our current thesis are:

- Although we expect continued economic weakness to weigh on the Fitness and Outdoor BUs, we are not expecting further large-scale declines. A continuation could rapidly deteriorate, leading to a bad year. Currently, Garmin expects to trade flat / slightly up, which we are expecting.

- Further margin deterioration. We are expecting an improvement over the next several years. Every bp of margin loss will be difficult to win back.

Final thoughts

Garmin is a solid business operating in a niche specialty. It has utilized its core competencies to develop a suite of products in a range of industries. This has created a robust business, tethered to its highly regarded brand.

We expected a continuation of its current trend, and at its current share price, we see further value. An interesting development would be if Garmin becomes a takeover target. With its current margins, it would be accretive to most.

For further details see:

Garmin: Consumer Electronics Success Story