GTX - Garrett Motion Is A Low Risk Stock With High Potential

2023-05-01 13:40:00 ET

Summary

- The company capital structure will be simplified by July with the conversion of series A preferred.

- Garrett will be buying back $570 million of preferred shares before conversion and approved a buyback plan of common shares of $250 million.

- The business execution since the emergence from bankruptcy has been excellent even against supply chain setbacks and inflation.

Garrett Motion (GTX) continues to be an investment with the odds on our side, and the business execution has been outstanding. Since my first article in September 2021 the company advanced its business plan and removed all barriers to appeal a broader range of investors.

Brief Story

GTX filed for bankruptcy in November 2020 to fight Honeywell and negotiate a fairer agreement on their legacy costs post spin off. The company emerged from Chapter 11 in 2021 with two classes of preferred shares, A and B. While B shares were repaid in 2022, shares A have the right to convert into common stock if certain milestones are achieved:

- Series B obligations are less or equal to $125 million.

- If the common stock trades 150% above the conversion price of $5.25, which means that it must trade above $7.88.

- LTM EBITDA has to be $600 million or higher for two consecutive quarters.

Series A shares will convert into common equity by July.

Business update

GTX business in 2022 was in line with the company April guidance, with sales of $3.6 billion, which was -1% from 2021 levels but +8% in constant currency. The company generated around $570 million in Adjusted EBITDA with a margin of 15.8%, which is 90 bps below the 2021 Adjusted EBITDA margin. Moreover, 80 bps of the 90 bps difference in margins is explained by FX impact and inflation. Garrett was able to offset inflationary pressures with inflation pass-through and productivity measures. In my first article , I argued that GTX had a moat around its turbo business and their ability to pass inflation pressures to their clients is another proof of that. In 2022 the company repaid all the series B and started paying cash dividends on the series A shares.

The company already reported is 1st quarter 2023 results and revised its guidance upwards. The company now expects to have sales in 2023 between $3.79 and $3.98 billion and achieve an adjusted EBITDA of $585 to $635 million. Nevertheless, the highlight for 2023 is the normalizing of the capital structure and the agreement to buy back some of the series A stock.

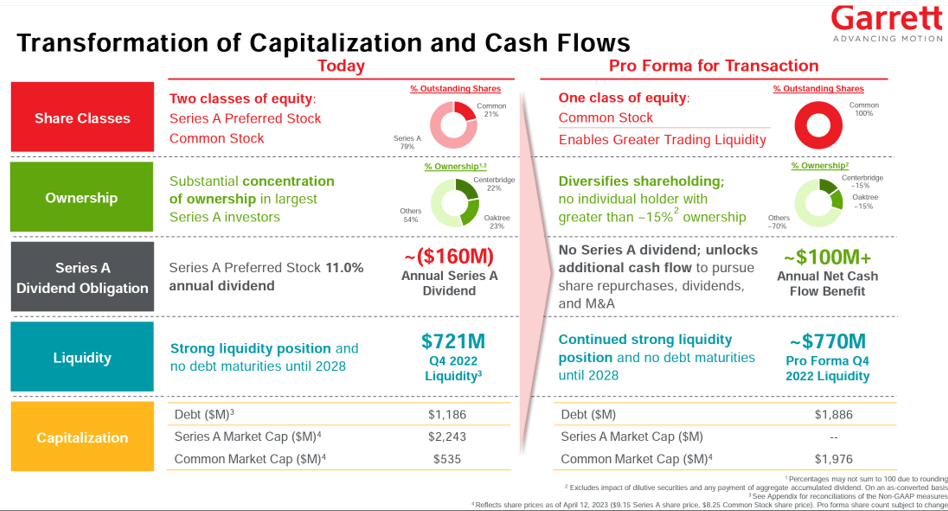

Series A Transaction

Garrett management has been pursuing the normalization of the capital structure since the emergency from bankruptcy which left the company with 3 types of stock, series A and B and its common shares. It also left the company with two big shareholders, Centerbridge and Oaktree. On the 13th of April the company announced that its A shares would convert into common equity by the 3rd July and that it achieved an agreement with Centerbridge and Oaktree to buyback a combined value of $570 million for its series A shares. The repurchase price will be around $8.1 per preferred share with a minimum price of $7.875 and a maximum of $8.5 per share. The immediate benefit of this transaction will be Garrett's ability to save $160 million in cash by not paying the 11% dividend rate on its A shares. The other benefits will be a more diverse set of investors, higher liquidity on its shares and more cash to compensate common shareholders. The company also announced that increased its current buyback plan of common shares from $100 million to $250 million.

Series A Transaction (Company presentation)

{kind=link}

The transaction will be financed with a new loan of $700 million and will buyback between 67 to 72 million series A shares that in the end will not convert into common stock.

| Series A buyback |

| Repurchase amount ($ millions) |

| 570 |

| Price per share $ |

| 7.88 |

| 8.10 |

| 8.50 |

| # of shares repurchased (millions) |

| 72 |

| 70 |

| 67 |

At the announced price the company will buyback around 70 million shares, or around 28% of the series A outstanding.

Valuation

Obviously, this transaction has an impact on the company future value. In previous articles I found the company intrinsic value by treating the A shares on a fully diluted basis since I believed the company would want to get rid them as soon as possible.

| Earnings Power Value ($ millions) |

| Worst Case |

| Base Case |

| Best Case |

| Expansion (2024E) |

| Sustainable revenues |

| 3.822 |

| 3.900 |

| 3.978 |

| 4.376 |

| Sustainable EBITDA MG |

| 15.4% |

| 15.7% |

| 16.7% |

| 16.7% |

| Sustainable EBITDA |

| 588 |

| 616 |

| 664 |

| 730 |

| Depreciation |

| 115 |

| 117 |

| 119 |

| 131 |

| Implied EBIT |

| 474 |

| 499 |

| 545 |

| 599 |

| Implied EBIT MG |

| 12.4% |

| 12.8% |

| 13.7% |

| 13.7% |

| Taxes @ 21% |

| 99 |

| 105 |

| 114 |

| 126 |

| Maintenance Capex |

| 115 |

| 117 |

| 119 |

| 131 |

| Earnings Power |

| 374 |

| 394 |

| 430 |

| 473 |

| EPV Multiple |

| 12 |

| 12 |

| 12 |

| 12 |

| EPV |

| 4.490 |

| 4.729 |

| 5.163 |

| 5.680 |

| Debt (with repurchase) |

| 1.886 |

| 1.886 |

| 1.886 |

| 1.886 |

| Cash (with repurchase) |

| 421 |

| 421 |

| 421 |

| 421 |

| Unpaid dividends on series A |

| 245 |

| 245 |

| 245 |

| 245 |

| Intrinsic Value |

| 2.780 |

| 2.019 |

| 3.453 |

| 3.969 |

| Shares outstanding (millions) |

| 65 |

| 65 |

| 65 |

| 65 |

| Series A converted shares (millions) |

| 175 |

| 175 |

| 175 |

| 175 |

| Fully diluted shares outstanding |

| 240 |

| 240 |

| 240 |

| 240 |

| Intrinsic value per share |

| 11.59 |

| 12.59 |

| 14.40 |

| 16.55 |

| Upside |

| 40% |

| 52% |

| 74% |

| 100% |

Garrett on a base case scenario still has an upside of +50%, with some conservative assumptions. Revenues equal to the mid-range guidance and adjusted EBITDA margin equal to 15.8% which was the 2022 value but far from the company long term margin of 16.7%. Comparing to 1st Quarter 2023 numbers debt will increase by $700 million to pay for the $570 million buyback of series A shares and cash will increase by $130 million. The value of the company for common shareholders will also decrease by the dividends accrued and unpaid to shareholders of series A shares. In this case the common shareholders will have a onetime loss of $245 million but in the future the company will have more cash to compensate common shareholders. The transaction does not put the company in any financial distress since the total level of debt will be more than manageable at around 3x EBITDA and the company does not have any significant maturities until 2028. Furthermore, 80% of its long-term debt has fixed rates.

Conclusion

Garrett Motion has a compelling set up! The company has a sticky business, great management and lower headwinds going forward. The conversion and the transaction agreement with Centerbridge and Oaktree will act as catalyst for the stock price since it will allow the company to have a broader base of investors and higher liquidity. It will also allow the company to focus on rewarding common shareholders with buybacks and probably some dividends. The most interesting part is that the risk is low for a company with this kind of undervaluation and business. The moat around its business and its execution allowed the company to repay more than $600 million in series B in over less than a year. At current prices the investors receive an asset with a 50% discount to its intrinsic value on a normalized earnings basis and its future growth for free. This seems almost a sure bet, let's go!

For further details see:

Garrett Motion Is A Low Risk Stock With High Potential