GTX - Garrett Motion: Low Risk Bet On Commercial Overhaul

2023-12-04 07:38:44 ET

Summary

- GTX’s revenue has grown at a CAGR of 4%, while its margins have declined and debt has ticked up.

- The company is heavily negatively exposed to the EV transition, with the majority of its revenue relative to petrol/diesel cars and the use case of turbochargers in the future uncertain.

- The company is investing heavily in R&D but it is too early to say if GTX will be successful with its transition.

- GTX is performing reasonably well relative to peers but is materially lacking growth.

- GTX is trading at a substantial discount to its peers and at only 5x EBITDA. We believe this is an attractive level appreciating the present risks associated with the company.

Investment thesis

Our current investment thesis is:

- GTX is substantially exposed to the transition of production toward EVs. We expect demand for its existing products to begin declining near the end of the decade, although any further slippage in margins is unlikely.

- The key is whether its innovation can offset this through increased EV production, allowing Management to future-proof the company. We are not wholly sold yet, although we do not think the industry will be completely obsolete. Realistically, the demand and margin profile will be lower.

- At 5x EBITDA and 7x FCF, we believe the company represents a low-risk investment to gain the optionality for successful innovation. If this does not occur, lifetime FCF is a good downside in our view.

Company description

Garrett Motion Holdings Inc. (GTX) is a leading global technology company that specializes in providing advanced turbocharging technologies and solutions for the automotive and industrial sectors. Garrett Motion is headquartered in Rolle, Switzerland, and has a strong global presence, serving customers around the world. GTX is a spin-off of Honeywell International ( HON ).

Share price

GTX’s share price performance has been disastrous, losing over 50% of its value in a short period of time. This is a reflection of the company’s difficulty with achieving financial improvements, as well as concerns about its competitive positioning.

Financial analysis

{kind=link}

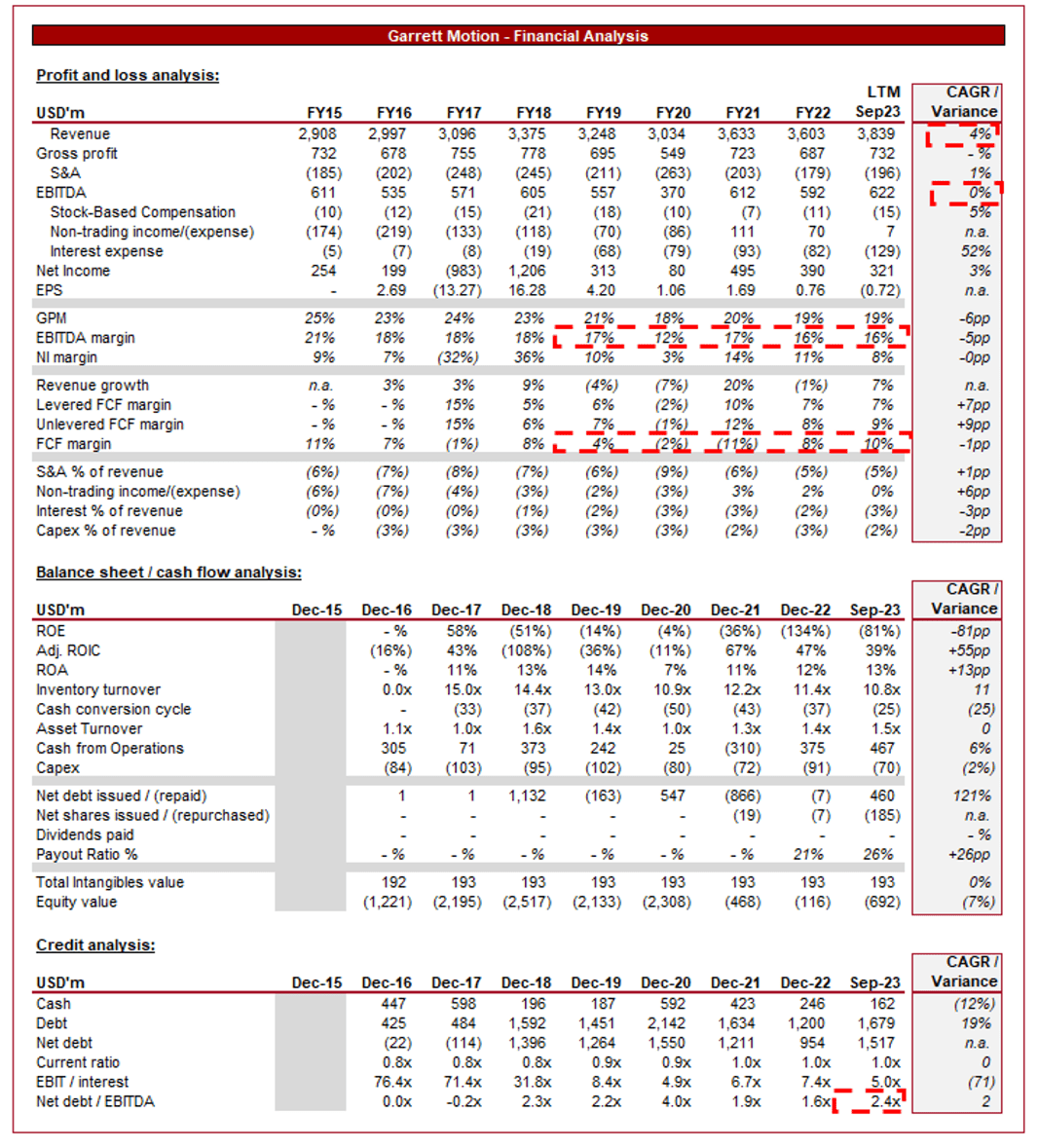

Presented above are GTX's financial results.

Revenue & Commercial Factors

GTX’s revenue has grown at a modest CAGR of 4% since FY15, representing a mild but consistent period for the business. The pandemic has arguably been beneficial, with revenue exceeding pre-pandemic levels substantially by FY21.

Business Model

GTX is a leading provider of turbocharging technologies. These systems are designed to improve the performance and efficiency of internal combustion engines (ICEs). Overly simplistically, by forcing more air into the engine's combustion chamber, turbochargers increase power output and reduce fuel consumption, which is crucial for efficiency and changing legislative demands.

The following illustrates a range of current products GTX offers, with solutions across vehicle types and “emission reduction” and “zero emission”. The zero-emission offering is part of the wider developments to future-proof the company’s product suite in the face of changing industry dynamics.

GTX

GTX is a market leader in the turbocharger segment, ranking #1 in the LV Gas segment, as well as LV Diesel and CV. The company has cornered the traditional ICE-powered segment, utilizing its strong brand and deep expertise to continually win new work.

GTX

Once won, there is little reason for automakers to switch, given that GTX is a leading player. This has allowed for sticky demand and incremental growth through new customer wins and inflationary price increases. As the following shows, this has given the company a bullet-proof pipeline for revenue, allowing Management to focus its efforts on product innovation and new customer wins.

GTX

GTX serves a diverse customer base, including leading automakers and manufacturers of commercial and off-highway vehicles. As the following illustrates, the company boasts a range of leading automakers as long-standing clients, reflecting the market position of GTX relative to its peers.

GTX

The company operates globally, with a presence in key automotive markets worldwide. Its global footprint allows GTX to tap into emerging opportunities and respond to regional market dynamics to maintain strong relationships with its customers. As the following reflects, no single region comprises more than 50% of revenue, with the same case for product segmentation. A slightly concerning observation, which we will discuss later, is the heavy weighting toward Gas and Diesel (c.67% of revenue) relative to emerging technologies (EV, etc.), with Aftermarket also exposed negatively to the EV trend (12%).

GTX

GTX has a significant presence in the aftermarket segment. They offer a range of replacement turbochargers and related components, ensuring ongoing revenue streams beyond initial OEM sales. This segment has provided the business with consistent recurring revenue, with less cyclicality that comes with car production cycles. This benefit is also the case for the Commercial segment, allowing for ~31% of revenue to be resilient.

GTX invests significantly in R&D to stay at the forefront of automotive technology. This commitment to innovation has enabled the company to develop cutting-edge solutions within the turbocharger segment, allowing it to maintain and develop its market-leading position.

This investment has now switched to the EV/electrification trend, with a substantial hiring spree and ~$100m annual spending.

GTX

In response to the shift towards electrification, GTX has expanded its portfolio to include electric boosting solutions. These systems are essential for enhancing the performance of hybrid and electric vehicles. GTX's electric boosting technologies improve efficiency, extend electric driving range, and enhance overall vehicle performance.

{kind=link}

GTX is already seeing good output from its development team, with preliminary progress toward winning customer contracts. Given its strong relationships within the existing business, GTX should have no trouble at least having conversations with the leading automakers. The question will be whether there is sufficient appetite for this technology and how the competition differs within this segment.

{kind=link}

Automotive industry

Stricter emissions regulations worldwide and the demand for fuel-efficient vehicles have driven automakers to adopt turbocharging and other advanced technologies to reduce greenhouse gas emissions. For this reason, the ability to produce a highly efficient solution will garner strong demand, which is the case for GTX, as illustrated by its strong margins. This should ensure healthy demand (not necessarily growth) for its products so long as traditional ICE-powered vehicles are being sold. The concern is that based on current legislative action by global governments, this market is expected to materially shrink during the 2030-2040 decade.

The key trend within the industry, and the reason for the company’s disappointing share price performance, is the EV transition. Traditional ICE-powered vehicles are on the way out and the future, at least in the next 2 decades, is likely EVs. EVs do not need turbochargers in the traditional sense as there is no engine that needs improving. For this reason, as each year passes, production will inevitably move toward EVs and thus GTX will experience reduced demand over time.

This does not mean the segment will be obsolete, as there is scope for innovation to modernize the technology. This will involve improving range and performance. The issue is that the product is far less important to the overall production of the vehicle, which likely means reduced demand and lower margins.

GTX's response has been to expand into electric boosting technologies. As automakers produce more hybrid and electric vehicles, GTX has the potential to offset the weakness in the coming years, although it is difficult to assess this today given the lack of material contract wins thus far. Further, we are concerned that GTX’s peers may exploit this opportunity to leapfrog it. As an example,

Mitsubishi Turbocharger and Engine Europe (MTEE) has developed power generators capable of charging the batteries of an electric vehicle while driving, repositioning the value proposition of a turbocharger. GTX believes the industry will be worth double the existing one, but is based on strong assumptions regarding the value proposition of the solutions developed. GTX

{kind=link}

Compounding this concern is the risk of weakness within the aftermarket industry. This is a consistent source of revenue for the business but with reduced parts within an EV and the reduced importance of GTX’s products, this segment will likely also suffer.

Economic & External Consideration

Current economic circumstances pose a challenge to GTX’s short-term growth prospects. The prolonged period of high inflation and current elevated interest rates are causing consumers to scale back on significant expenditures because of increased living expenses.

The automotive industry is particularly vulnerable in this situation, as new vehicle purchases tend to be sensitive to consumer choices, including the option of buying used cars or exploring alternative transportation methods. Additionally, limited financing choices further restrict the number of new purchases. This reduced demand will inevitably impact production, contributing to a reduced need for turbochargers and other parts.

The benefit for GTX is that its industrials (and Aftermarket) exposure has the potential to offset this impact, partially (~31% of revenue), allowing for a robust performance relative to its automotive-focused peers. Industrials generally have a longer time horizon, contributing to less volatile demand based on the current environment.

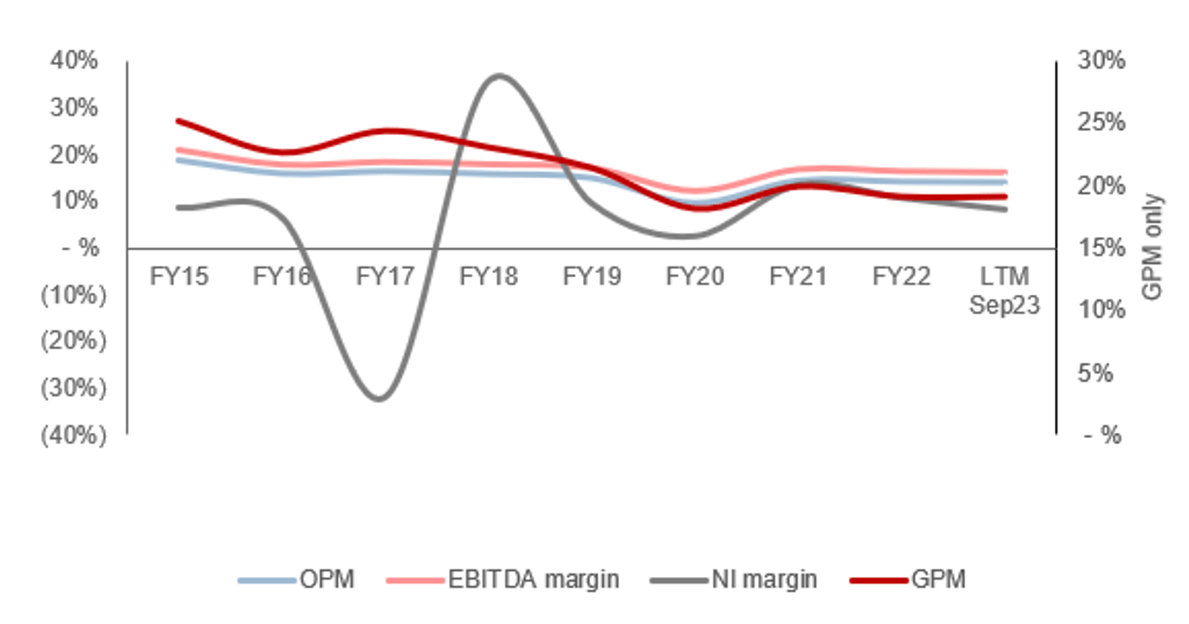

Margins

{kind=link}

GTX’s margins have gradually declined since it was listed, falling from an EBITDA-M of 21% to 16%. This is a disappointing development and reflective of both a decline in its commercial positioning and supply chain issues associated with the pandemic period.

Given the challenges its business model faces with the EV transition, we are not overly confident that GTX is positioned well to win back the margin it has lost. This will only occur if its product development is sufficient to create a strong EV product suite.

Quarterly results

The following are key takeaways from GTX’s most recent quarterly result:

- Net sales growth of +2%, driven by new product ramp-ups, strong demand from OEMs, and improved demand from China following the end of its zero-covid policy. This was offset by a broader softening of applications due to the macroeconomic environment.

- Management believes the outlook for light vehicle production will remain robust, with customer demand volatility declining. This bucks the trend observed with many automakers and the market as a whole, suggesting the demand from the end user is sufficient for OEMs to maintain current production levels.

- Improvement in adj. EBITDA-M from 15.4% to 15.8%. This solidifies its strong performance in the prior quarters, although does not represent a material improvement toward its FY18 levels. Much of the supply-side issues have broadly subsided, making this a concerning result.

We consider this a moderate quarter for the business following a strong Q2. Management has slightly lower expectations due to FX concerns, although we suspect there is a hint of demand fears. We are surprised to see demand remain robust (following our analysis of a number of players within the automotive and parts industry) and so we expect a continued downward trend in growth.

Balance sheet & Cash Flows

GTX has incrementally increased its debt usage, reaching a ND/EBITDA of 2.4x. This is a comfortable level, although we are slightly concerned that interest already comprises 3% of revenue (5x interest coverage). We do not believe this should be allowed to increase further, potentially restricting the company’s ability to invest in growth.

Distributions have been non-existent to any material level for ordinary shareholders, with cash utilized to repurchase preferred stock, as well as pay dividends to these shareholders. The expectation is for this to shift to the common shares following the Capital Transformation exercise.

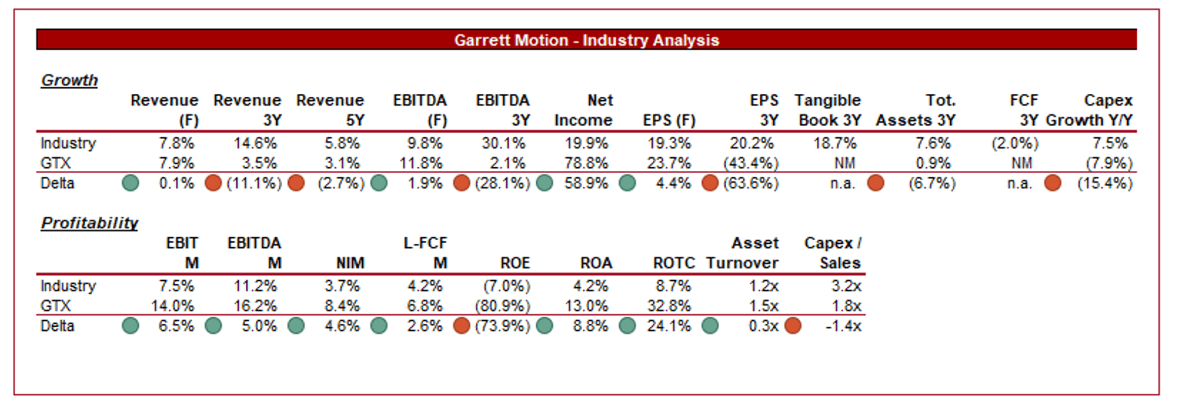

Industry analysis

Auto Parts and Equipment Stocks (Seeking Alpha)

{kind=link}

Presented above is a comparison of GTX's growth and profitability to the average of its industry, as defined by Seeking Alpha (26 companies).

GTX’s growth has been disappointing, with the company underperforming on a revenue basis across both a 3Y and 5Y basis. A portion of this is GTX’s lack of M&A activity, with many of its peers regularly acquiring smaller peers. This said, we also believe this also reflects the inherent weakness in the business model.

Conversely, GTX’s profitability is where the company shines. It is noticeably outperforming its peers across all key metrics, especially in FCF and ROTC. This is a reflection of its historical market strength, allowing for operational excellence and consistent demand to drive leading margins.

Given the disruption the industry is facing, we have a preference toward growth, particularly as GTX could face pressures on its margins if growth continues to be low.

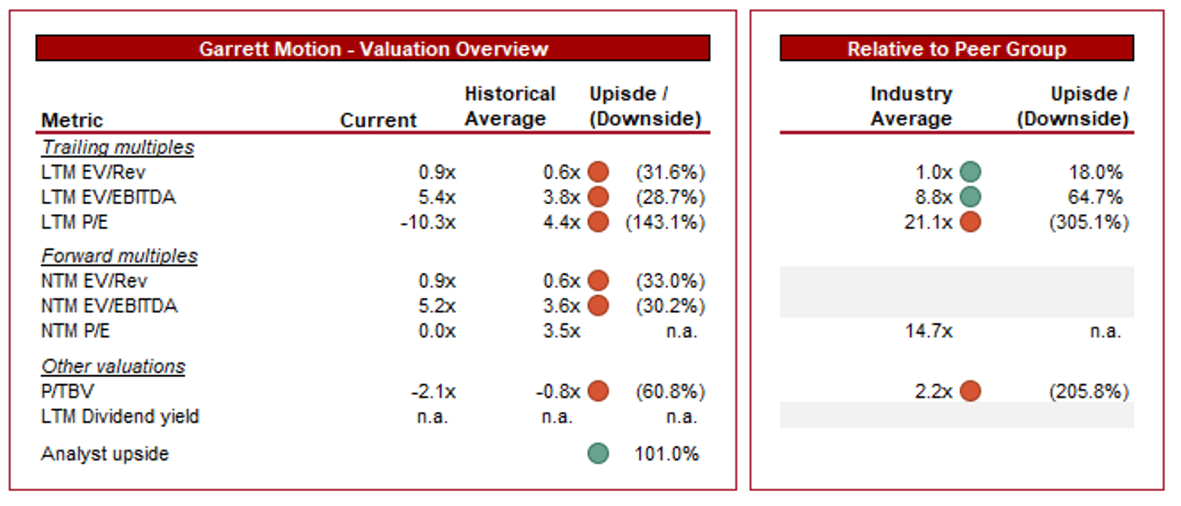

Valuation

{kind=link}

GTX is currently trading at 5x LTM EBITDA and 5x NTM EBITDA. This is a premium to its historical average.

Given the short trading history of the business, we will not consider this an appropriate benchmark. This said, the company has traded at extremely low multiples, with its current level not materially above its average. This implies real fear among investors that GTX will be left in the dust as the EV transition contributes to the extinction of its industry.

Further, the company is trading at a steep discount to its peer group on an EBITDA basis, substantially above what would be reasonable on a financial performance basis alone. This implies again that the discount is primarily a reflection of investor concerns around its commercial positioning and how this results in financial deterioration.

Our view is that the company is undervalued. Most of our analysis has been critical of GTX and we are seriously concerned about obsolescence. This said, it will be a long time until revenue begins to decline and an even longer time until the company is materially financially impacted (2030-2035). Until then, investors can own this stock at 5x EBITDA and hope Management can innovate its way to a lucrative future, in which case a 10x EBITDA multiple in line with its industry appears reasonable at a high level. If this does not occur, investors will buy GTX at a 8.4x FCF multiple to its market cap, giving sufficient returns until the end of the decade.

Key risks with our thesis

The key risks, which we have extensively detailed above, are the future of the turbocharger industry and how the unit economics shake out. Further, there are risks associated with how the existing turbocharger industry is positioned and how (and when) the transition is materially felt.

Final thoughts

GTX is a solid company. The business has developed a strong market position within a resilient segment of the automotive industry. Its profitability is attractive and partially offsets its limited growth. This said, GTX is the opposite of future-proof and this is likely the reason Honeywell spun the company off. The EV revolution represents a significant risk to the future of GTX and it feels inevitable that this will be a very different company in 10 years time. This said, at a >50% discount to its IPO price and a 5x EBITDA multiple, we believe it represents a low-risk option.

For further details see:

Garrett Motion: Low Risk Bet On Commercial Overhaul