GTX - Garrett Motion: The Massive Discount Is Fair Given The Risks

2023-07-17 06:00:00 ET

Summary

- Garrett Motion stock might look massively undervalued, but my analysis suggests the discount is fair.

- The turbocharger industry is expected to grow slowly, and Garrett is in a substantial net debt position.

- The company faces risks such as vulnerability to cycles in the automotive industry, fierce competition, and the emergence of electric vehicles.

Investment thesis

Garrett Motion ( GTX ) is massively undervalued based on valuation multiples and the discounted cash flow model. But I consider this substantial undervaluation fair because the company demonstrates almost no revenue growth, and its gross margin has declined notably over the long term. The turbocharger industry is expected to continue demonstrating a low growth pace, and I see no good prospects for the company's top line in the near term. Moreover, the company is in a substantial net debt position. To sum up, I assign the stock a "Hold" rating.

Company information

Garrett designs, manufactures, and sells highly engineered turbocharger and electric-boosting technologies for light and commercial vehicle original equipment manufacturers and automotive software solutions.

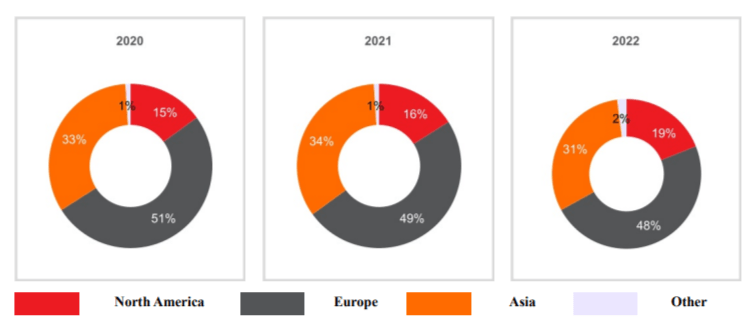

The company's fiscal year ends on December 31. About half of the company's sales were generated in Europe in FY 2022.

{kind=link}

Financials

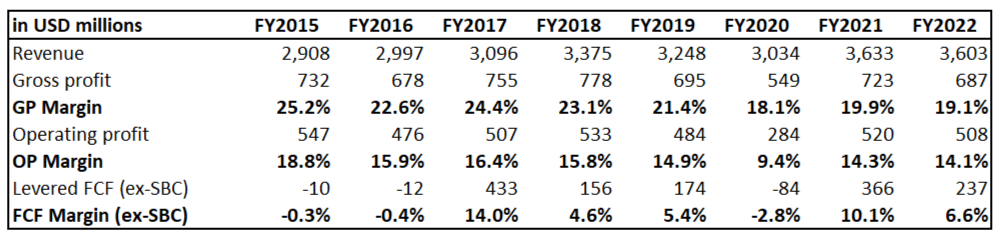

The company delivered a 3.1% revenue CAGR since FY 2015, which looks good compared to the global automotive market size volatility in the last few years. The problem is that GTX's gross and operating margins softened despite the increasing business scale. On the other hand, the good news is that the free cash flow [FCF] margin improved notably but is currently substantially lower than all-time highs.

{kind=link}

I like the company's meager SG&A-to-revenue ratio of about 5%, meaning the business is managed efficiently and that the business scaling up will expand the operating margin.

The company employs a rather aggressive capital allocation strategy with an above 100% leverage ratio. On the other hand, I am comfortable with the covered ratio of about 6. Liquidity metrics also look healthy.

Seeking Alpha

The latest quarterly earnings were announced on April 17, with higher-than-consensus revenue and a miss in EPS. Revenue grew 7.7% YoY and 13% on a constant currency basis. At the same time, the EPS shrank by two cents. The gross and operating margins were almost flat YoY. A solid bullish sign is that the adjusted EBITDA increased from $146 million to $168 million. The expanded EBITDA led to a substantial improvement in the adjusted FCF, which was up from $38 million to $88 million. During the Q1 earnings call , the management expressed its confidence in the near term by increasing the full FY2023 outlook.

The momentum for the business is strong, and the upcoming quarter's earnings are expected to be solid by consensus estimates. Revenue is forecasted at $982 million, which is 14% higher on a YoY basis. The EPS is expected to expand notably from $0.15 to $0.23.

According to the company's latest 10-K report , in the next couple of years, the turbocharger industry is expected to grow slowly from 46 million units in FY 2022 to 48 million units in FY 2024. The turbocharger industry growth will be mainly driven in the short and medium term by an expected increase in the penetration of hybrid vehicles.

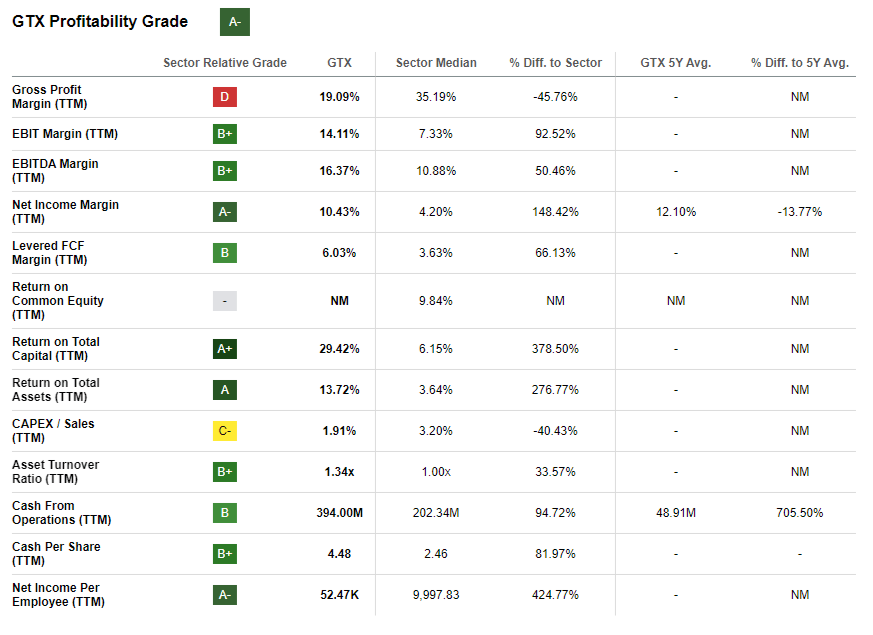

Let me also conduct a peer analysis to understand whether the company is well-positioned in the market. GTX has a relatively low 11th place out of 35 in the Automotive Parts & Equipment industry from Seeking Alpha Quant. A weak position in the industry rank is mainly due to the weak revenue growth compared to the sector median. On the other hand, GTX looks like a very effective business compared to its peers because of its high profitability grade. The company demonstrates a stellar return on capital of about 30%. The gross margin is the only profitability metric where Garrett significantly lags behind peers.

{kind=link}

Overall, I think that the management is effectively controlling operating expenses. Still, the critical point here looks like vast improvement is needed to the core operations, which directly affects the cost of revenue. We also see that the company lacks growth drivers, and expanding profitability with slow revenue growth is difficult.

Valuation

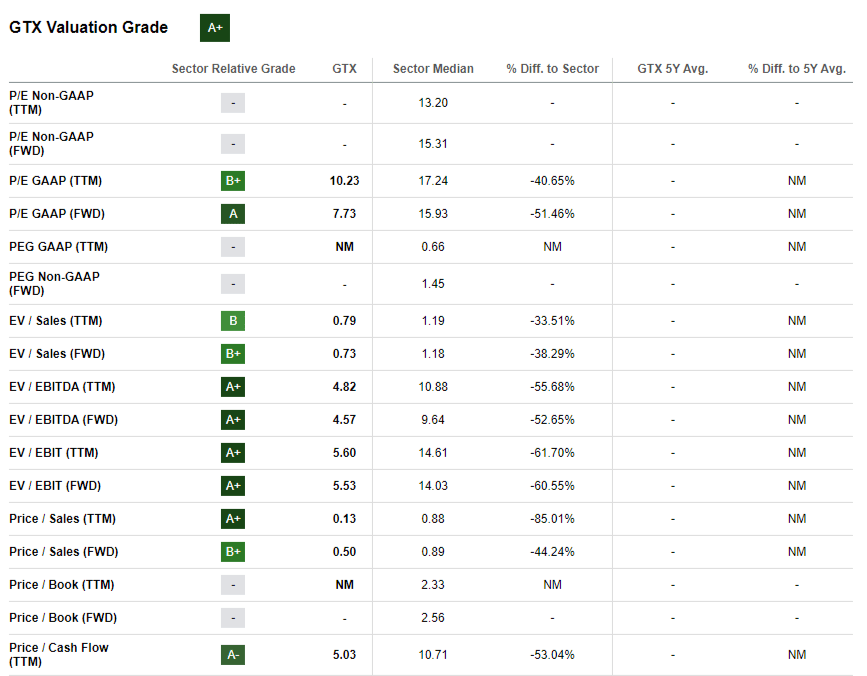

The stock underperformed the broader market with a 6% year-to-date share price decline. Seeking Alpha Quant assigns GTX the highest possible "A+" grade. This is due to very low multiples, substantially lower than the sector medial levels.

{kind=link}

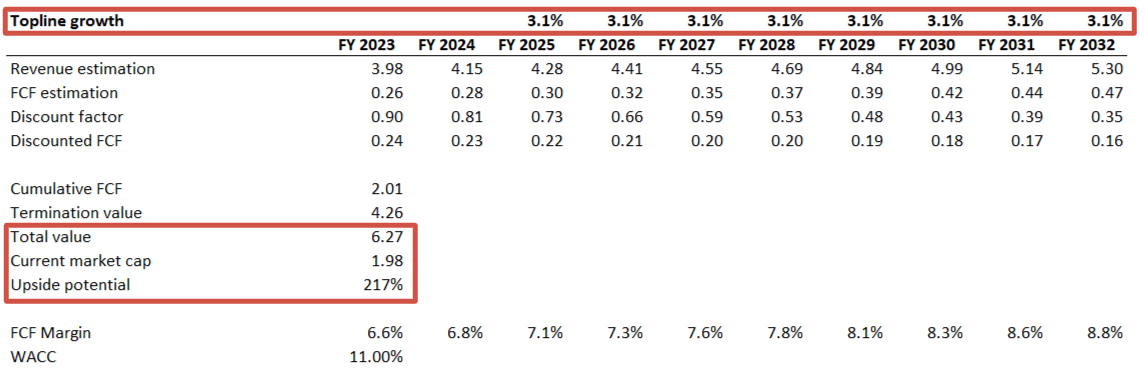

Now I want to continue my valuation analysis with the discounted cash flow [DCF] approach. I use an 11% WACC as a discount rate. I have revenue consensus estimates available for the nearest two fiscal years, and for the years beyond, I implement a historical 3.1% revenue CAGR. For FY 2023 I use a 6.6% FCF margin and expect it to expand by 25 basis points yearly as the business scales up.

{kind=link}

The upside potential looks immense since the DCF suggests the company's fair value is $6.3 billion, three times higher than the current market capitalization. Even if I subtract the current net debt position of $918 million from the fair value, the upside potential still might look very attractive. To decide whether it is actually attractive or not, let me proceed with the risk analysis.

Risks to consider

Investing in stocks is substantially risky, especially in companies of smaller capitalization, like GTX.

The business is closely related to the automotive industry, which makes the company vulnerable to cycles in the sector. The macro-environment for the automotive industry is harsh in the current high-interest rates reality.

Garrett Motion faces fierce competition from major turbochargers and automotive technology industry players. Companies of grander scale can offer similar products and technologies at lower prices thanks to the scale. That could lead to pricing pressure and loss of market share.

The automotive industry currently experiences a major disruption in the form of the emergence of electric vehicles and alternative propulsion systems. It is highly likely that the demand for internal combustion engines [ICE] may decline over the long term. The company needs to adapt and innovate in order not to go out of business.

The concentration risk is also high. The company's sales are highly dependent on a few key customers including major automotive manufacturers. This leads to customer-specific risks like financial instability or loss of major contracts. A substantial reduction in orders from primary customers will adversely affect Garrett's earnings.

Bottom line

To conclude, I would recommend staying away from the stock. After conducting my in-depth analysis, I do not see any potential positive catalysts which can fuel the stock price massive rally. The stock has been trading with substantial discounts over a long time, and I believe the market was fair. I am not investing and assign GTX stock a neutral "Hold" rating because the upside potential does not outweigh the risks.

For further details see:

Garrett Motion: The Massive Discount Is Fair, Given The Risks