GLOP - GasLog Partners: I Know What I Have Don't Low Ball Me

Summary

- GasLog Partners LP staged a recovery during 2022 as their financial performance surged on the back of increased LNG demand from Europe.

- They recently received a takeover offer from their parent company for $7.70 per unit.

- I feel this is far too low given their immense free cash flow that, even in a bad year, would still see a massive circa 25% yield.

- Further strengthening my resolve is their continued deleveraging, which increases the prospects of higher distributions in 2023.

- Since this, nevertheless, helps put a floor beneath their unit price, I believe that maintaining my strong buy rating on GasLog Partners LP is appropriate.

Introduction

After GasLog Partners LP ( GLOP ) staged a recovery during 2022, it seemed that a big year was ahead in 2023, as my previous article discussed. Funnily enough, mere weeks into the year and they already have received a takeover bid, which is not necessarily what I envisioned. Despite this helping push their unit price higher, I will be holding out for a much better offer for GLOP, as this brings to mind the online marketplace meme of "I know what I have, don't low ball me."

Coverage Summary & Ratings

Since many readers are likely short on time, the table below provides a brief summary and ratings for the primary criteria assessed. If interested, this Google Document provides information regarding my rating system and, importantly, links to my library of equivalent analyses that share a comparable approach to enhance cross-investment comparability.

Author

Detailed Analysis

{kind=link}

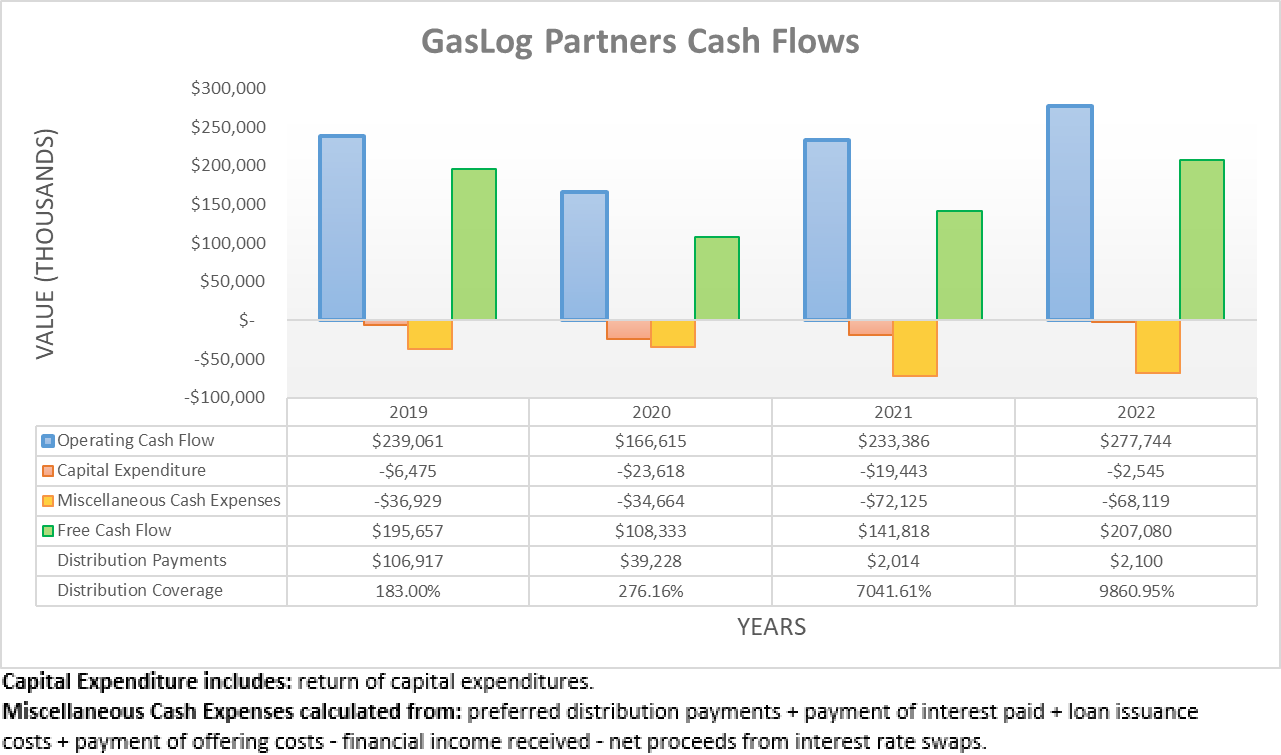

Thanks to charter rates for LNG vessels surging on the back of European LNG demand as my previous analysis expected, GasLog Partners LP's cash flow performance continued strengthening throughout the fourth quarter of 2022. As a result, their operating cash flow rounded out the year at $277.7m, which is the highest result since at least the beginning of 2019 and represents an impressive 19% improvement year-on-year versus their previous result of $233.4m during 2021.

{kind=link}

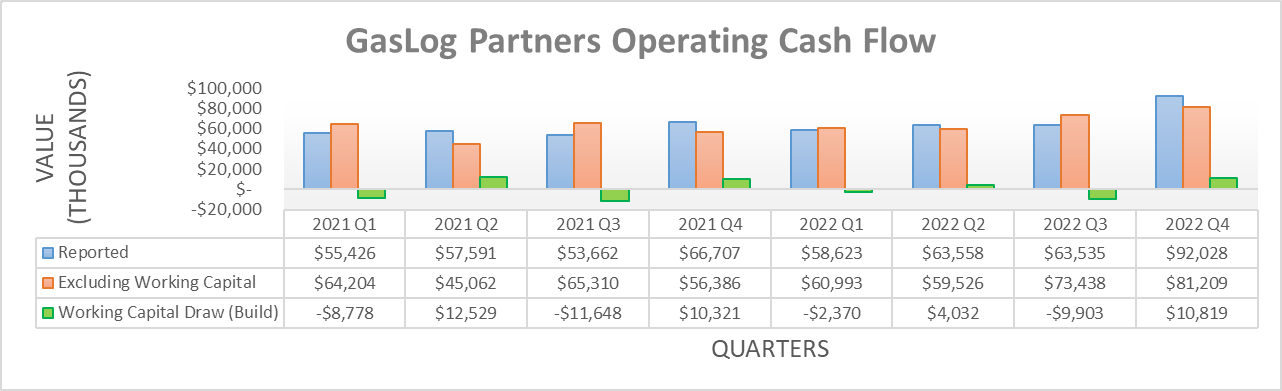

If zooming into the fourth quarter of 2022 in isolation, their reported operating cash flow was $92m and thus represents the highest result in recent history since at least the beginning of 2021, and far ahead of their next highest result of $66.7m during the fourth quarter of 2021. Even if excluding working capital movements, their underlying result of $81.2m during the fourth quarter of 2022 still easily beats their previous highest result of $73.4m during the third quarter.

To make their full-year results during 2022 even more favorable, GasLog Partners LP was not materially helped by working capital movements, nor were they materially hindered. To this point, their various draws and build each quarter netted out to an immaterial draw of $2.6m, whereas their results during full-year 2021 saw an equivalent draw of $2.4m.

Whilst this was positive and created a strong base heading into 2023, right now the big news is the takeover offer GasLog Partners LP recently received from the partner company, GasLog Limited. Judging by their unit price of $8.18 already trading above this offer of $7.70 as of the time of writing, it seems many in the market suspect a better offer is likely inbound, especially as this is only a non-binding proposal and not an officially accepted takeover offer.

In my eyes, GasLog Partners LP unitholders should hold out for a much better offer, especially given the positive outlook for 2023 detailed within my previous analysis. Although, even if we ignore this consideration and instead just focus on the numbers as they stand right now, there is far better value laying within GasLog Partners LP units. To especially drive this point home, I will ignore their record-setting results during 2022 and even their solid results during 2021, but instead, utilize their beaten-down results during 2020 that were hindered by the severe downturn caused by the Covid-19 pandemic.

In the face of this once-in-a-generation event, they still generated $108.3m of free cash flow that, even after their recent unit price rally, would see a massive free cash flow yield of 25%+ against their current market capitalization of approximately $420m. This is a tremendous yield, especially for the low point of their financial performance that is easily replicable in the future. In fact, their free cash flow during 2022 was $207.1m, and thus almost twice as high, which in turn would see a near unthinkably high 50% free cash flow yield.

To phrase this another way for new investors, this means they could potentially provide a distribution yield anywhere up to a massive circa 25% at their current unit price, even if solely relying upon their beaten-down results during 2020. So thinking about their offer in this light, it should be clear why I will not be selling my units GasLog Partners LP anywhere near these prices, especially as their financial position continues improving and moving closer to unlocking this immense value via higher distributions.

{kind=link}

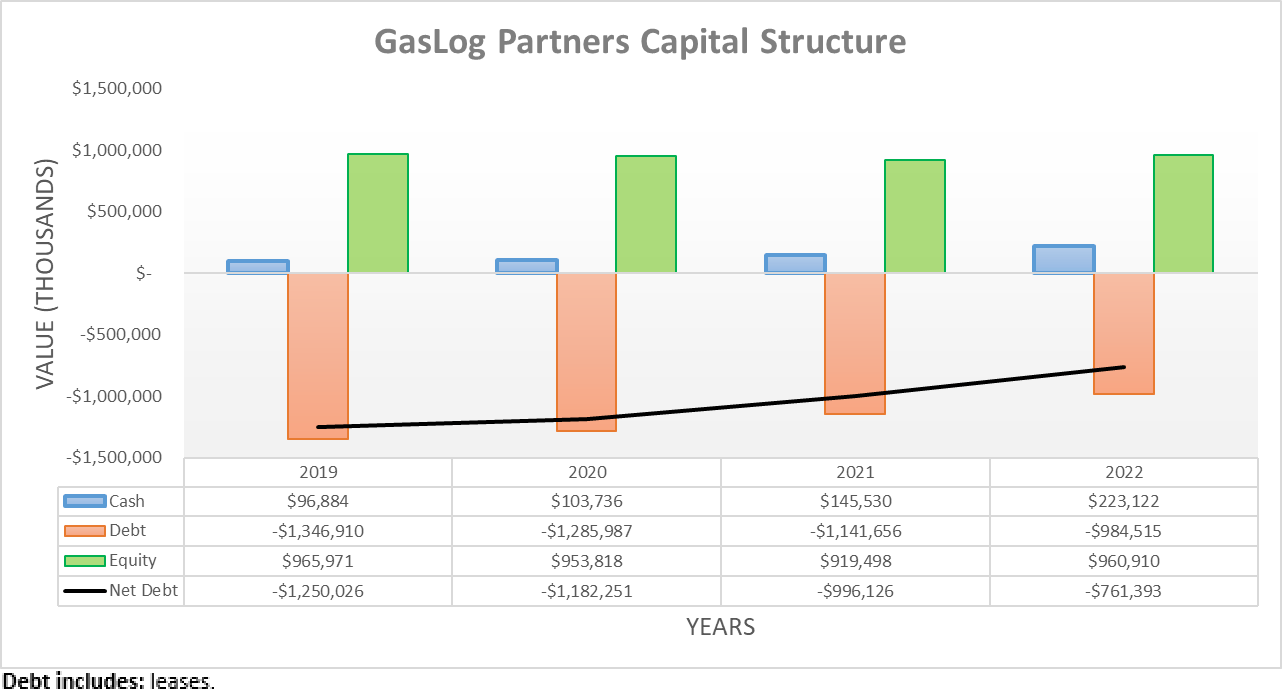

Quite unsurprisingly, their deleveraging continued during the fourth quarter of 2022, with their net debt remaining on its downward trajectory to $761.4m versus its previous level of $806.9m following the third quarter. Whilst already solid, it was accompanied by a further $10.5m of preferred unit buybacks that will help boost their free cash flow slightly going forwards.

Until such time as their barebones distributions are lifted higher, their deleveraging mission will continue unabated as they move to complete the second of their two targets, as discussed in detail within my previously linked article. Namely, this remaining target requires getting their debt-to-capitalization down to sub-40%, which was 50.30% following the third quarter of 2022 and subsequently dropped to 48.70% following the fourth quarter, as per slide thirteen of their fourth quarter of 2022 results presentation . This further helps push GasLog Partners LP closer to completing its leverage mission, which as my previously linked article outlined in detail, should be achieved during 2023 to mark the beginning of a new era of higher distributions. This, therefore, strengthens my resolve to wait for a higher unit price instead of what I view as a lowball takeover offer.

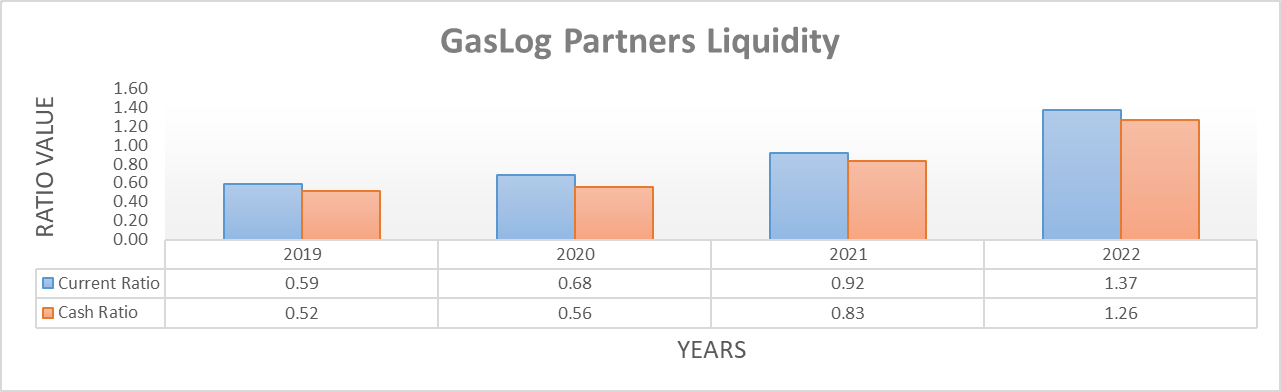

Whilst these improvements are positive, they are only modest and thus, it would still be redundant to reassess their leverage or debt serviceability in detail, as this was done when conducting the previous analysis. Furthermore, as their cash balance grew modestly higher during the fourth quarter of 2022 to $223.1m versus its previous level of $164m following the third quarter, this also applies to their liquidity since it was already not problematic.

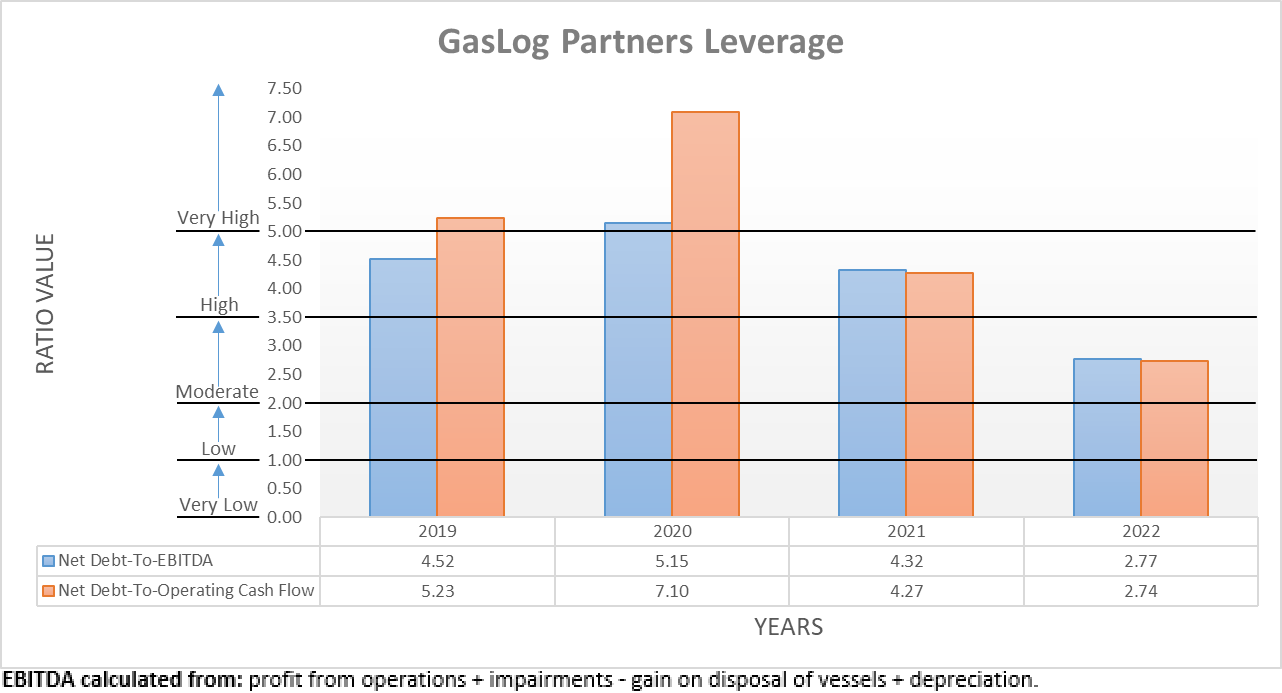

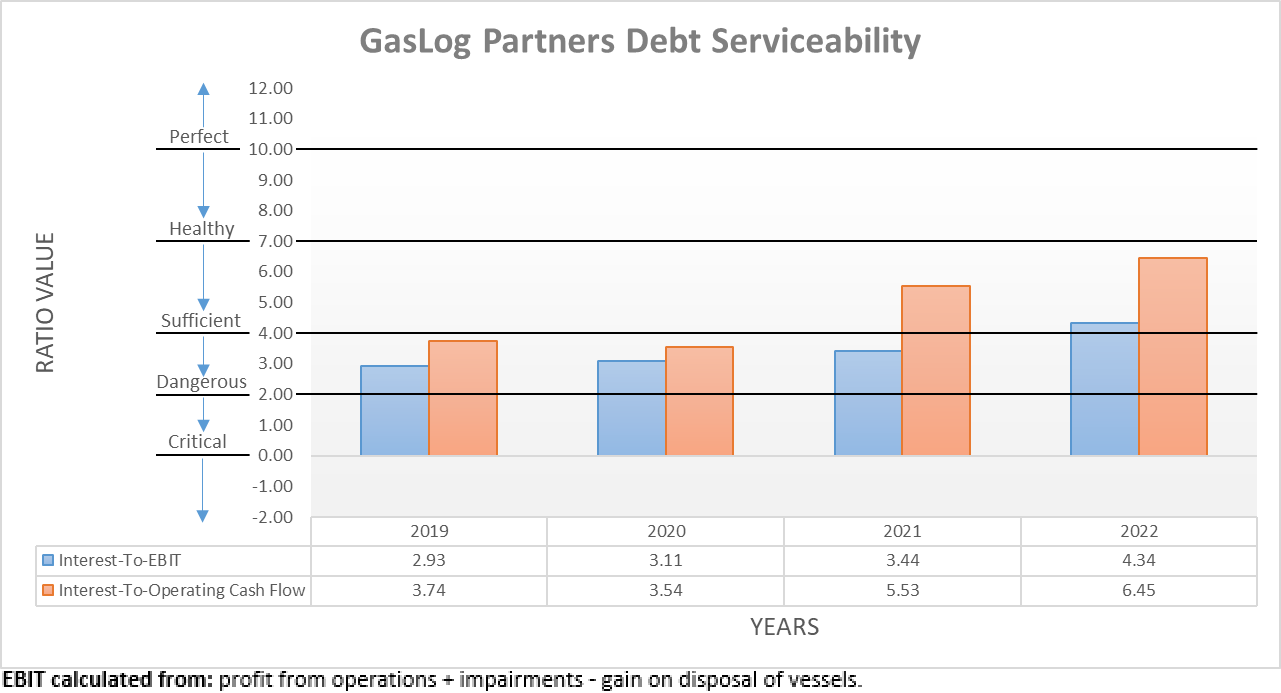

The three relevant graphs are still included below to provide context for any new readers, which to zero surprise shows their leverage continued plummeting with their respective net debt-to-EBITDA and net debt-to-operating cash flow down to 2.77 and 2.74. Apart from being within the moderate territory of between 2.01 and 3.50, these are quite possibly their lowest points ever in the history of the partnership. Concurrently, their debt serviceability also improved in tandem with their interest coverage hitting a healthy 4.34 and 6.45 when compared against their respective EBIT and operating cash flow. Finally, GasLog Partners LP's already strong liquidity also improved thanks to their higher cash balance, with their current and cash ratios now seeing respective results of 1.37 and 1.26. If interested in further details regarding these topics, please refer to my previously linked article.

{kind=link}

{kind=link}

{kind=link}

Conclusion

Despite awaiting a much better offer for GasLog Partners LP, I would actually prefer to see this takeover completely dropped with no higher offer forthcoming, so the immense value within the GLOP units has a chance to be fully realized across the coming years. That said, this is obviously outside of my control, but alas, I will not willingly sell my GLOP units for a massive 25%+ free cash flow yield right now, as they are pushing towards the end of their deleveraging mission. If nothing else, this takeover offer should help put a floor beneath the GasLog Partners LP unit price and, thus, I believe that maintaining my strong buy rating is appropriate.

Notes: Unless specified otherwise, all figures in this article were taken from GasLog Partners' SEC Filings , all calculated figures were performed by the author.

For further details see:

GasLog Partners: I Know What I Have, Don't Low Ball Me