GATX - GATX: Railcar Leasing Firm Is An Overlooked Capital Gains Candidate

Summary

- GATX has paid an uninterrupted quarterly dividend since 1918, 105 years, and has raised its dividend consecutively for the past 14 years.

- GATX offers exposure to a diverse portfolio of railcars. GATX's main markets are in North America, Europe, and India, and is partners with Rolls-Royce in spare aircraft engine leasing.

- Even though GATX could be considered a “Steady Eddie” selection, management has voiced concerns with short-term outlooks. My recommendation is to nibble here and to add during market weakness.

- GATX's major competitors are either privately held (Union), or part of a much larger firm (Wells Fargo, Trinity, CIT).

- GATX provides investors exposure to the largest "pure" publicly traded railcar leasing company.

GATX Corporation ( GATX ), previously known as General American Transportation, was founded as the Atlantic Seaboard Dispatch Co. in Chicago, Illinois in 1898 to ship beer in refrigerated railcars for the Duquesne Brewing Company. Today, GATX is one of the largest tank car leasing company with assets in North America, Europe, and India. In addition, GATX has a joint venture with Rolls-Royce (RYCEF), known as Rolls-Royce & Partners Finance RRPF. RRPF manages a portfolio of leased spare aircraft engines. Along the same business lines, GATX began purchasing its own stable of spare aircraft engines, with RRPF as the managing partner for leasing these assets. Railcar leasing is often an overlooked specialty finance industry which is controlled by a few big players, including GATX.

The Company leases tank cars, various freight car configurations, such as flat bed, box, and auto carriers, in addition to locomotives in North America. GATX focuses on tank and freight cars in Europe, and freight cars in India. Also, GATX owns Trifleet and its portfolio of 18,000 uniquely specialized tank containers combining the advantages of rail tank shipping with intermodal transportation. The company owns a fleet of ~147,000 railcars and 570 locomotives. The Company's rail customers primarily operate in the petroleum, chemical, food/agriculture, and transportation industries.

The company operates through four segments: Rail North America (67% of 2022 revenues), Rail International (22%), Portfolio Management (3%), and Other (8%). Portfolio Management includes its interest in RRPF, company-owned spare aircraft engines, and Trifleet. Other includes railcar maintenance and repair services for railcar leasing customers from company-owned repair facilities.

Factmr.com estimates the US railcar leasing market generates revenue of ~$6 billion a year. Page 26 of the 2022 GATX Corporate Overview presentation outlines railcar leasing market share by the top firms, based on a market size of 921,000 railcars. The presentation also outlines market share by tank cars and by freight cars. Management estimates GATX has a 17% market share for tanks cars and 10% market share for freight cars, for an average North American market share of 13%. The top tier railcar lessors include GATX, CIT group, a subsidiary of First Citizens Bancshares ( FCNCA ) with 13% share, privately held Union Tank Car also with 13%, Wells Fargo ( WFC ) with 15%, and Trinity ( TRN ) with 14%. The presentation implies these five companies control almost 70% of the North American railcar leasing business. Industry annual growth has slowed a bit from its 2015 to 2019 rate of 8% with annual growth expected to be 6.5% from 2021 to 2025.

Driving this growth in the US is the cost advantage of rail transportation over truck. Also, rail shipping offers an improved ESG profile with its smaller carbon footprint. Cost factors play a large role in leasing over purchasing considerations for shippers. A decade ago, “standard” tank railcars cost under $50,000 each, but currently exceed $150,000. With an average useful life span of 20 years and most scrapped after 35 yrs, and the higher financing expense from increasing interest rates, the cost advantage is moving towards leasing. GATX annually refreshes its portfolio by selling a portion of their assets, termed remarketing, and scraping other. In 2021, GATX remarketed 2,500 railcars and scrapped another 3,500, generating revenues of $97 million. Over the years, management has sold and scrapped an average of 6,000 to 7,000 railcars annually, and replaced the retired assets with updated and safer product. In 2022, GATX placed orders for new assets totally over $1 billion to be delivered over the next 5 years. Over the past few years, GATX has increased its fleet size by about 1% a year.

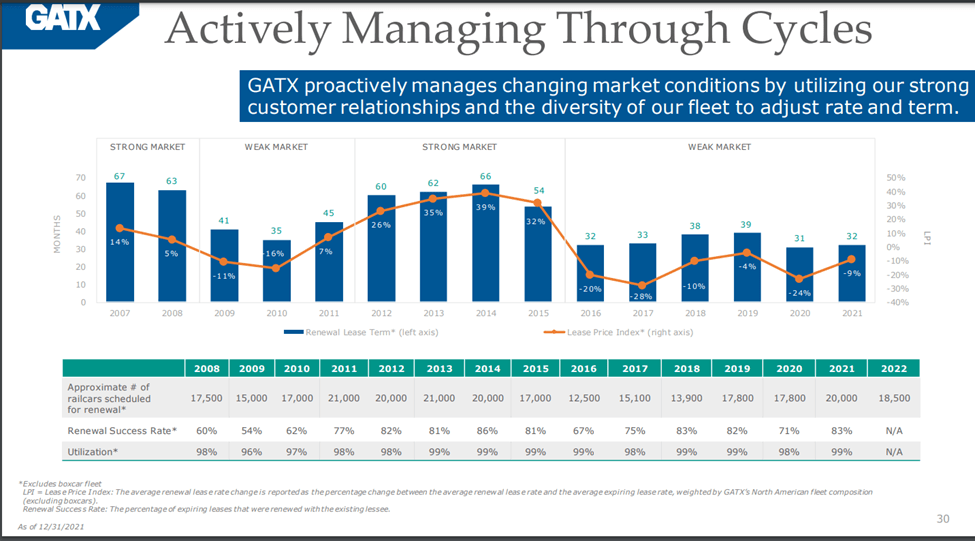

GATX recently issued its 2022 year-end results press release with the usual conference call and it seems to be rather upbeat. Even in the face of a pending economic slowdown, GATX customers were focused on retaining and renewing their railcar leases. Renewal rates were high at 85.6%, vs a 10-yr average renewal success rates of 79.1%, and is the highest since 2014. Average contract lengths also inched upwards in 2022 to 33 months, increasing from 31 months in 2020 and 32 months in 2022. It is interesting to note the 31 months contract length of 2020 was the lowest in 15 years, with a range of 31 months to 67 months. The high renewal rate led to higher lease price rates. For the year, renewal lease rates increased by 23%, after falling -9% in 2021 and -24% in 2020.

Management expects these positive trends to continue into 2023 and 2024. Utilization rates for their assets remains extremely high at 99.5%. GATX has an extraordinary history of high utilization rates, with readings above 98% since 2011. However, it is important to note management still considers the overall current market conditions to be “weak” compared to historic data. The graphic below outlines market conditions for the last 15 years, with the last seven years being considered as “weak”.

Industrywide, leasing profitability is based on three basic attributes: utilization rates, length of contracts, and price of contracts. GATX is no different. With utilization rates consistently high, length and price of contracts become the underpinning of GTAX profitability. Management has developed an index to track these important data points. GATX annually issues its Lease Price Index LPI which compares contract length and renewal price. The graphic below from GATX 2022 Corporate Overview presentation outlines a 15-yr history of the components of the LPI from 2017 to 2021. Updating for 2022 numbers, contract length was 33 months, renewal prices was +23%, renewal success rate at 85.5%, and utilization at 99.5%. When the graphic is updated, a bottoming trend in 2020 will become more apparent.

Lease Price Index 2008 to 2021 (GATX Presentation)

{kind=link}

Earnings per share for 2022 were negatively affected by a write-off of assets located in Russia, a loss from exiting its specialty ship leasing business, and the timing of tax adjustments. Before adjustment, GATX earned $6.07 per share and $4.35 after adjustments, up from $3.98 in 2021. Without adjustments, management is forecasting 2023 EPS of $6.50-$6.90, with midpoint at $6.70. The few analysts covering GATX expect 2024 EPS to be relatively flat. Of concern to me is the downgrade by CFRA of its SPGMI Quality Rating for 10-yr consistency in earnings and dividend growth from A- (above average) to B+ (average). As overall leasing market conditions improve from their 6-yr “weak” conditions, I expect GATX to be upgraded again to A-.

GATX offers investors a conservative balance sheet and approach to the leasing business. Management has been known for offering best-in-class customer relationships with a full range of repair and maintenance services. The ability to maintain a profitable relationship between lease contract length and price, as shown by the LPI chart above, should maximize shareholder returns for long-term shareholders. GATX's major competitors are either privately held (Union), or part of a much larger organization (Wells Fargo, Trinity, CIT). GATX provides investors exposure to the largest "pure" publicly traded railcar leasing company.

I have known of GATX since the mid-1970s and have been a shareholder off and on a few times over the past 50 years. Last fall, I nibbled on a new position and expect to build it over time. While the stock could be considered as fully valued, with most price targets in the $125 to $130 range, GATX stock is a quality, niche, capital gains selection for long-term investors. Even though GATX could be considered as a “Steady Eddie” choice, management has voiced some concerns with the short-term outlook. In the conference call, Robert Lyons, President and CEO, assessed the challenges as:

We enter 2023 facing uncertain economic conditions in North America and Europe, continued global supply chain challenges, and a heightened interest rate environment. This is one of the most unpredictable environments I have ever dealt with at GATX in my 25 years here.

My recommendation is to establish a small position at current prices and then to build a position with the pending market weakness I see on the horizon. GATX is a quality stock selection for my investment bucket titled, “equites primarily bought for long-term capital gains”.

For further details see:

GATX: Railcar Leasing Firm Is An Overlooked Capital Gains Candidate