GBAB - GBAB: A Few Reasons I Wouldn't Get Too Aggressive Here

2023-12-06 11:05:33 ET

Summary

- Guggenheim Taxable Municipal Bond & Investment Grade Debt Trust offers exposure to taxable municipal bonds and has a primary objective of providing current income.

- GBAB has seen strong performance in the short term, but there are concerns about its ability to sustain this performance.

- I recommend looking for better value elsewhere and am downgrading my outlook to "hold" for this CEF.

Main Thesis & Background

The purpose of this article is to evaluate the Guggenheim Taxable Municipal Bond & Investment Grade Debt Trust ( GBAB ) as an investment option. This fund offers exposure in taxable municipal bonds, with a primary investment objective to "provide current income with a secondary objective of long-term capital appreciation". This is a diversified fund with a heavy allocation towards taxable muni bonds, bank loans, and high-yield credit securities.

It has been about four months since I last wrote about GBAB. Back in August, I saw the potential for reasonable gains from this CEF, and I opted for a "buy" rating on it. After some ups and downs along the way, it turns out my outlook has been vindicated. GBAB has seen a healthy gain with plenty of momentum in the short-term:

Fund Performance (Seeking Alpha)

Certainly I am happy to see such strong performance in a fund I follow and have recommended. But it has led me to question how likely it is that this performance can continue. There are a few attributes specific to GBAB that make me think now might be the time to take some chips (profit) off the table and look for better value elsewhere. I will explain each of these in turn in this review, which I believe support why I am downgrading this ticker to "hold" as we look to end the year.

Premium Prices Aren't For Me Right Now

Right off the bat, an issue I have with GBAB is the fund's premium price. While not outrageous, the premium clocks in around 3%, which is a notable bump since my last review. This suggests a good part of the fund's total return over the past four months has been due to premium expansion. While positive for current holders up through now, it isn't very helpful for suggesting more gains are likely going forward:

GBAB Fast Facts (Guggenheim)

Again, this isn't really an "alarming" premium and I certainly wouldn't get overly bearish on this metric alone. But it is worth pointing out that, as usual, GBAB trades at a pretty wide divergence compared to the other two CEFs that are closest to its make-up. These funds' and their current valuations - BlackRock Taxable Municipal Bond Trust ( BBN ) and Nuveen Taxable Municipal Income Fund ( NBB ) - are shown below, respectively:

BBN's Facts (BlackRock) NBB's Facts (Nuveen)

{kind=link}

{kind=link}

We should remember that GBAB is not a direct comparison to these two funds because they hold almost exclusively taxable muni bonds, while GBAB has almost half its securities tied to other sectors. So this is not apples to apples.

But it does indicate that there is a significant discount that can be paid for taxable munis by exploring those other options - calling in to question how strong an argument could be made for buying GBAB at the moment. That is key to why I am downgrading GBAB for now.

Distribution Still Just (Barely) Hanging On

My next topic refers to a continuation of a trend that concerned me back in August as well. This is the fund's distribution, which clocks in at a very healthy 9% on the surface. Considering the surge in demand for bonds right now - this is likely piquing the interest of investors across the spectrum.

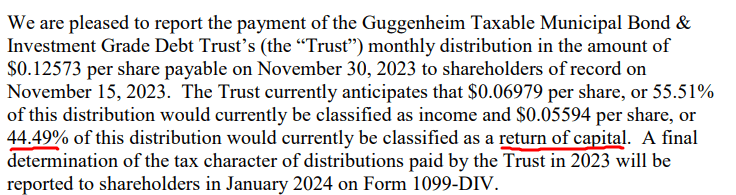

However, a 9% yield is really only attractive if it is sustainable. And that is where my concern is. In fairness, I have had this concern for a while and it has ultimately proven to be a bit unfounded given the consistency in the payout. But I continue to believe it is only a matter of time before it is cut. This is because the return of capital allocation is very high - and has been for most of 2023:

November's Section 19(a) (Guggenheim)

{kind=link}

The fact is that GBAB's payout is not sustainable for the long run based on current market conditions. Something could change and/or the fund could delay a cut for a while longer. But the reality is that if a cut occurs then the fund's market price is likely to take a hit. This is a situation I would want to avoid, so therefore suggest approaching this fund very carefully.

If The Fed Is "Done", Then Muni Exposure Will Help

To balance this review a bit, I will now touch on some potential tailwinds for GBAB. This is important because, as noted, I am not a bear on this fund. There is a very real chance of more gains going forward and that needs to be factored in to any analysis. While I personally don't feel the risk is worth it any longer at current prices, I could very well be wrong.

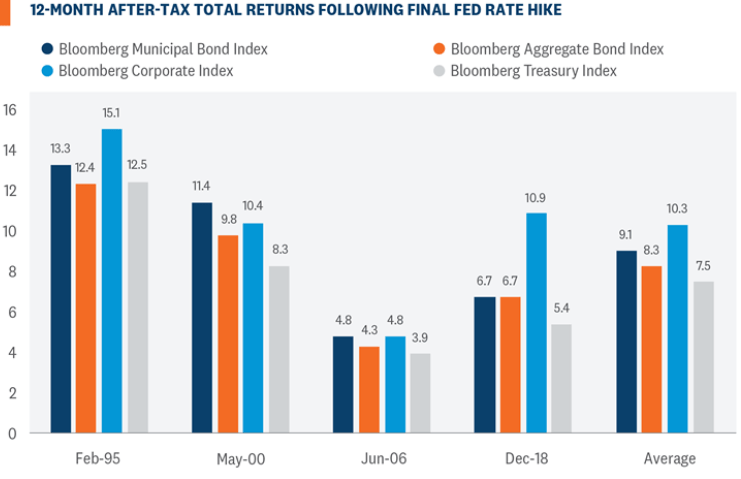

One of the reasons has to do with the potential for bonds as a whole if the Fed has indeed hit its peak rate. This is something the market has been counting on over the past month and bonds have surged as a result. This includes muni bonds, but pretty much every fixed-income sector. The good news - aside from the welcome relief rally - is that munis tend to be a strong out-performer once the Fed has stopped hiking rates. If we use history as a guide, we see this is a sector that often pulls up the aggregate bond index:

Past Returns After Fed Peak (Bloomberg)

{kind=link}

What this means is that if the Fed does continue to pause (or even cut interest rates), then munis are likely to see strong gains in early 2024. The market is certainly hoping for this to happen, partially explaining the recent gain in GBAB (and other fixed-income funds). So while a lot of optimism is already baked in, more could be on the way if the Fed delivers. This is something to keep a close eye on in the first few quarters of next year.

Equities Ain't Cheap

Another supporting factor for GBAB is a more macro-one. This is again relevant for munis, but really for more fixed-income securities. Therefore, while this is potentially a tailwind for GBAB, it can be extended to most of the CEFs and ETFs that readers review in this space more broadly.

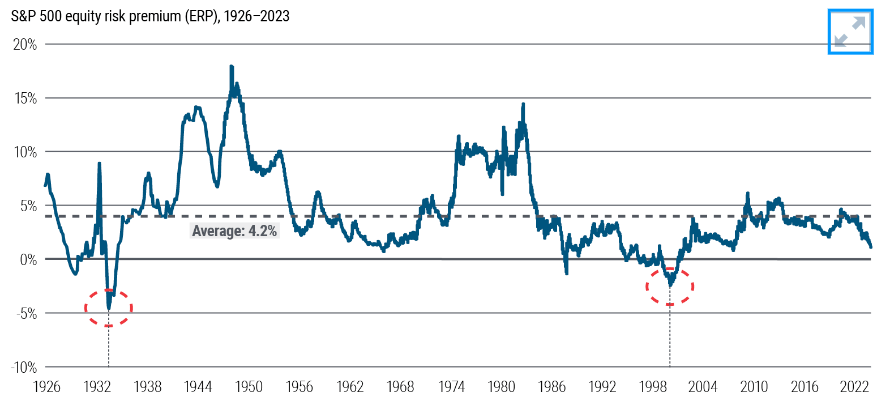

What I am referring to is the relative attractiveness of bonds relative to equities. One measure to consider is the equity risk premium, which is the inverse of the price/earnings ratio of the S&P 500 minus the 10-year U.S. Treasury yield. This is a common investment metric that can be utilized by investors when evaluating the two asset classes if one is deciding where they want to add to their portfolio at any given time.

Currently, the risk premium is currently at just over 1%, which is quite low as it is well below its longer term average:

Equity Risk Premium (measured for S&P 500) (PIMCO)

{kind=link}

The implication here is that equities are likely to get less expensive compared to bonds in the future. This could occur through a number of scenarios. One is that equities see underlying corporate earnings rise. That would be the ideal scenario. Barring that, another is for equities to decline in price - evening out the valuation gap between them and bonds. The third would be for bonds to get more expensive, likely due to increased demand and - therefore - higher prices for those assets going forward.

The bottom-line to me is that equities probably won't register this unfavorable dynamic for much longer, given their trading history. Given that I am not anticipating a corporate earnings boom, I am left to anticipate either higher bond prices or lower equity prices in the coming months. This makes funds like GBAB more attractive than many equity options under this outlook.

Bonds Aren't The Only Hedge In Town

Bringing this back to my "hold" rating, I want to reiterate why I'm still not a buyer of GBAB here. I just noted that GBAB has a few aspects that could push it higher. But I remain concerned about the premium valuation, the fact that bonds have already seen a big push higher, and the cost of leverage. This leverage headwind has been in place since last year and we see it in the fund's return of capital metric. Until the Fed actually moves on rates this won't change (as opposed to investor speculation of a move).

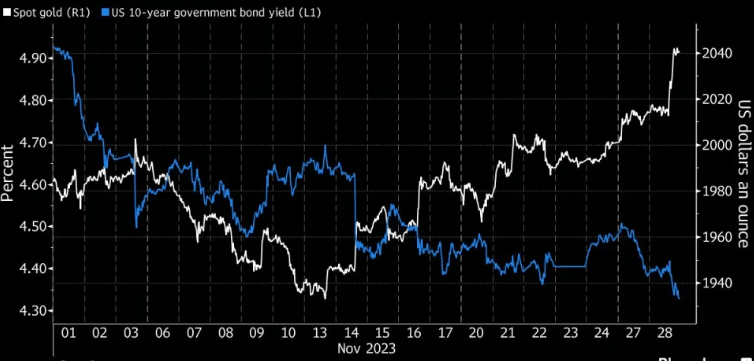

The good news is that bonds - or GBAB by extension - are not the only game in town if one wants to hedge equity exposure. One of my favorite hedges is gold and this is an asset that also has plenty of bullish momentum right now. If the Fed does reverse course on rate hikes next year, this is another area that is sure to continue a rally. That is because gold often moves inversely with treasury yields, as shown below:

Gold Spot Price vs. US Treasury Yield (Yahoo Finance)

{kind=link}

This is not a sure thing of course, but it is one of the more pronounced relationships we are going to see across asset classes.

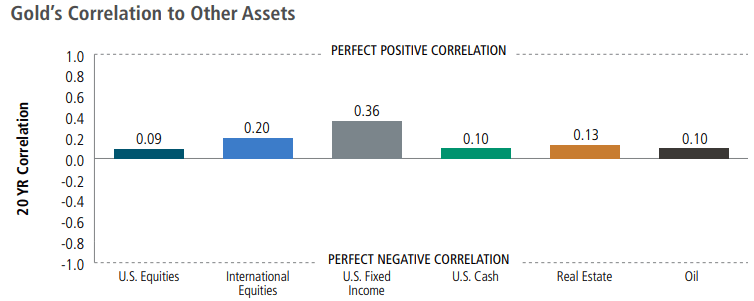

Another reason I like gold is that it doesn't have to be an "either or" dynamic. Bonds still have a place, I am not suggesting otherwise - just that gold may be a stronger value right now than bond CEFs that trade at a premium. But if one finds their bond portfolio allocated fully, then gold could be a supplement because its correlation across a host of sectors is quite weak:

{kind=link}

I bring this up because it helps to support why I am not a bull on GBAB. We don't need to only buy bonds - whether through GBAB or any other product - in order to hedge an equity-centric portfolio (like the one I have). But the value I see in gold helps to convince me that I don't need to create a buy case for GBAB when there isn't one.

Bottom Line

GBAB has delivered a nice pop for holders since August so the "buy" call was the right one for a while. More gains could be on the way as investors rotate to bonds - and munis bonds in particular, which have seen a surge in retail buying. Further, GBAB's 9% yield remains well above the risk-free rate so that is going to keep buyers interested in the short-term.

But I have concerns. That income stream is suspect, with a distribution cut a very real possibility in my view. Further, the fund's premium price suggests the time may be ripe for locking in some gains and/or waiting for a better (cheaper) entry point. The fact is that other hedges, both in the bond sector and elsewhere, represent a more attractive value to me at the moment. Therefore, I am downgrading my outlook to "hold", and suggest my followers approach any new positions very selectively.

For further details see:

GBAB: A Few Reasons I Wouldn't Get Too Aggressive Here