GBAB - GBAB: Adding Corporates To Taxable Municipals Bond Has Mixed Results

Summary

- The Guggenheim Taxable Municipal Bond & Investment Grade Debt Trust is not a pure play, as it also owns corporate debt.

- Along with explaining this closed-end fund, I will compare it to two other taxable municipal bond funds I recently reviewed.

- Maybe due to its corporate exposure, GBAB results fall between the other funds. I would hold off until the FOMC is done raising interest rates.

(This article was co-produced with Hoya Capital Real Estate . )

Introduction

The taxable municipal bond market started after passage of the Tax Reform Act of 1986 , which eliminated the issuance of tax?exempt bonds for certain purposes. The Act lowered the top tax rate for ordinary income from 50% to 28%, greatly reducing the tax advantage that tax-exempt bonds offered.

For investors in states with high income tax rates, they should compare after-tax returns of these funds with their tax-exempt cousins as that is what really matters: the money still in your pocket after Uncle Sam and the state taxman visits.

This article reviews the Guggenheim Taxable Municipal Bond & Investment Grade Debt Trust ( GBAB ) and does some comparisons with both the BlackRock Taxable Municipal Bond ( BBN ) and the Nuveen Taxable Municipal Income Fund ( NBB ). A link to that article is provided later.

Guggenheim Taxable Municipal Bond & Investment Grade Debt Trust review

GBAB has $362m in assets under management ("AUM") and comes with 134bps in fees. The forward yield is listed as 9.1%.

Seeking Alpha describes this fund as:

The Trust’s investment objective is to provide current income with a secondary objective of long-term capital appreciation. The Trust seeks to achieve its investment objectives by investing primarily in a diversified portfolio of taxable municipal securities, including Build America Bonds (“BABs”), and other investment grade, income generating debt securities, including debt instruments issued by non-profit entities. Benchmark: BBgBarc US Aggregate Bond TR USD. GBAB started in 2010.

Source: seekingalpha.com GBAB

Guggenheim adds to the above description and provides information on the duration reduction strategies of GBAB on the home page .

- GBAB will invest at least 80% of its Managed Assets in taxable municipal securities, including BABs, and other investment grade, income generating debt securities, including debt instruments issued by non-profit entities (such as entities related to healthcare, higher education and housing), municipal conduits, project finance corporations, and tax-exempt municipal securities.

- GBAB will invest at least 50% of its Managed Assets in taxable municipal securities.

- GBAB will not invest more than 25% of its Managed Assets in municipal securities in any one state of origin.

By executing a proprietary duration management trading strategy, GBAB utilizes two strategies in seeking to reduce the portfolio’s effective duration to generally less than 15 years.

- Interest-Rate Swaps. GPIM will initially seek to take advantage of the relatively flat portions of the U.S. Treasury yield curve that appear to offer favorable decreases in duration without significant yield concessions. For example, this may be accomplished by combining the sale of interest-rate swaps on the long end of the yield curve with the purchase of interest-rate swaps on the intermediate portion of the yield curve. To take advantage of cost anomalies, GPIM will have the flexibility to opportunistically manage duration and may trade across other yield curves that exhibit similarly wide duration spreads with low spreads in yields.

- Fixed-Income Sector and Security Selection. The Trust may invest in short-duration fixed-income securities, which may help to decrease the overall duration of the Trust’s portfolio while also potentially adding incremental yield.

GBAB holdings review

guggenheiminvestments.com

I suspect the manager only updates their website quarterly, thus new data should be available soon. The top asset class, at 57%, is the allocation to the bonds investors would expect from the first part of the fund's name, the rest more related to the second part. Sector allocations are shown next.

guggenheiminvestments.com

Compared to the other BAB funds, there does not seem to be any bonds that require tax revenue; which is good if the U.S. is in a recession. The sector allocations show a good diversity of sources. The top two states, California and Texas, account for 25% of the portfolio. That doesn't mean they are dependent on state/local government revenue though.

guggenheiminvestments.com

The total number of states was not listed but should be over 30. I calculated the average credit rating for the GBAB portfolio to be "A-".

guggenheiminvestments.com

They hold 1.23% with ratings prone to defaulting much more so than the higher-rated bonds: CCC & D. The maturity schedule shows little coming due in the next few years, limiting GBAB to having free cashflow to buy higher coupon debt.

CEFConnect.com

They only listed the top 10 holdings.

guggenheiminvestments.com

These 10, out of about 300, come to just under 25% of the portfolio. The last full holdings list is from the May Annual Report .

I found several data points from various sites:

- Effective duration: 10.65 years

- YTM: 6.13%

- Leverage: 31%

- Average bond price: $95.61

- Portfolio turnover: 31%.

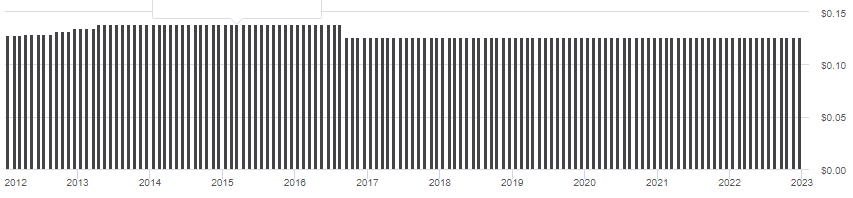

GBAB distribution review

{kind=link}

Since the cut in 2016, the monthly payout has been $.1257. Based on recent 19-a letters, about 80% is income, 10% STG, and 10% from ROC; 2021 19-a forms looked the same.

Price and NAV review

Investors must have been shocked earlier this year when GBAB broke below $20/share, a price not even breached during the height of the COVID crisis! Could this mean that the FOMC is more powerful than that disease. Like COVID, the end is not yet in sight with another meeting set for mid-December.

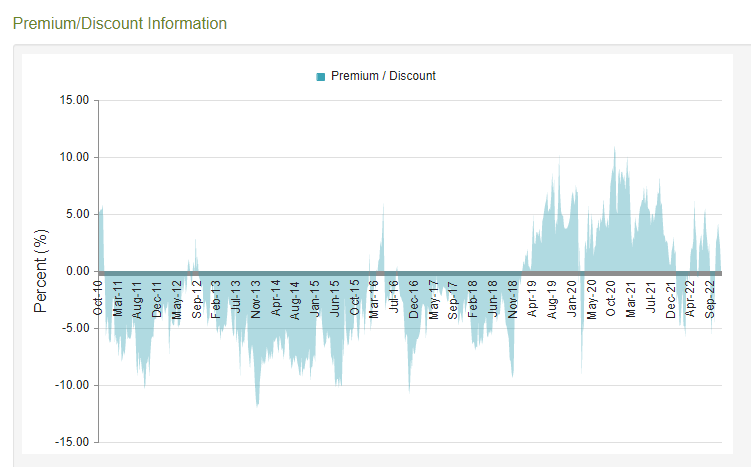

GBAB use to spend most of its time selling at a discount, but not so much in recent years.

{kind=link}

Currently GBAB is at a 1.5% discount, up from 7% in mid-November. With its recent fluctuations between premium/discount prices, waiting for another 5% discount should be contemplated. That said, all those 2022 reversals occurred as the GBAB price was in freefall. Maybe the October low will hold.

Portfolio strategy

Taxable Municipal funds are mainly for investor either not overly concerned about taxes and wanting to add to the diversity of their fixed income allocation or want municipal bonds in their tax-free feature is not valuable, such as inside a IRA or 401k account. That said, what one earns after the taxman takes their cut is what really counts. In that vein, I included the following chart, which includes BBN & NBB CEFs (article link), plus Invesco Build America Bond Portfolio ETF (BAB), and since GBAB owns corporates, the PIMCO Investment Grade Corporate Bond Index ETF ( CORP ).

{kind=link}

With GBAB's CAGR falling between the other two pure taxable municipal CEFs, its allocation to corporates effect is hard to measure; allocation and other factors are playing a deciding part. GBAB did better than either of the ETFs included. The above returns, of course do not account for how the different funds are taxed, which also depends on the type of account they are held in.

Final thoughts

Here is one view of what might occur after December’s meeting:

Expectations are high that the Fed will step down their rate hikes to 50 bps. That would raise the target federal funds rate ((TFFR)) to 4.25%-4.50%. The TFFR would be at its highest level since late 2007 when the Fed started to cut rates from its 5.25% peak.

At the Fed meeting, attention will focus on what the Fed signals for 2023. The “dot plot” in the SEP (which lists forecasts for the TFFR) will likely suggest that the TFFR will rise above 5% in 2023. Below is the summary of the September dot plot for 2023 to 2025:

TFFR implied by the September SEP dot plot

- 4.50%-4.75% (one 25-bp hike) by end of 2023

- 3.75%-4.00% (three 25-bp cuts) by end of 2024

- 2.75%-3.00% (four 25-bp cuts) by end of 2025

With the TFFR likely rising to 4.25%-4.50% next week, the new dot plot should show a higher TFFR in 2023. At the very least, it should be 25-bp higher at 4.75%-5.00%. That would imply one more 50-bp rate hike next year or two 25-bp rate hikes next year. As this WSJ piece describes, “Brisk wage growth may lead officials to consider raising policy rate above 5% in 2023.”

Source: depositaccounts.com .

As we have seen across almost all fixed income funds in 2020, FOMC actions are driving this (and other) asset class results. For those believing these forecasts, wading in on GBAB at this time might not be prudent versus holding T-Bills or CDs for the first part of 2023.

For further details see:

GBAB: Adding Corporates To Taxable Municipals Bond Has Mixed Results