BILS - GBIL: Balancing Income And Principal Protection

2023-10-20 17:48:43 ET

Summary

- Policy rate hikes are likely at an end.

- But volatility across the Treasury yield curve isn't ending anytime soon.

- Low-cost ETFs like GBIL, spanning the full spectrum of <12-month maturities, offer shelter in the meantime.

After a brief relief rally earlier this week, Treasuries have resumed bear steepening on the back of more fiscal concerns and a stronger-than-expected core inflation print. Barring a prolonged oil price spike driven by the ongoing geopolitical turmoil, though, the upside surprise in consumer inflation shouldn't alter the future rate hike path. Digging deeper, the key drivers appear to be isolated and transitory, with limited spillover to inflation expectations.

Plus, recent Fedspeak acknowledging the role of higher long-end yields in further tightening liquidity conditions skews the odds toward a neutral policy decision next month. That said, the market is currently pricing in a similarly benign view through year-end, so investors looking to mitigate any risk of a precautionary hike should probably stick to the front end. For now, the inverted curve also keeps front-end yields higher than the long-end, skewing the relative value argument firmly in favor of T-bills.

Even with more supply scheduled for next month, there should be more than enough demand at this part of the curve, given the higher bill yields vs comparable rates available to institutional and retail investors. At a +5% yield currently, the low-cost Goldman Sachs Access Treasury 0-1 Year ETF ( GBIL ) offers a compelling balance of income and principal protection.

Fund Overview - Low-Cost Exposure to the Highest-Yielding Parts of the Curve

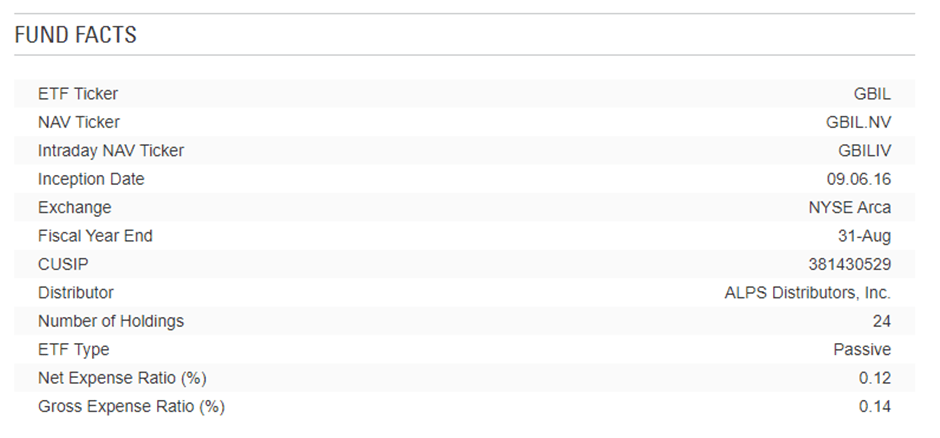

The US-listed Goldman Sachs Access Treasury 0-1 Year ETF offers investors an easy access vehicle that tracks, before fees and expenses, the total return performance of the FTSE US Treasury 0-1 Year Composite Select Index, a basket of USD-denominated Treasury securities subject to a twelve-month maturity constraint. The ETF is managed by the Goldman Sachs Asset Management Fixed Income and Liquidity Solutions team and holds ~$6.1bn of assets under management at the time of writing. The fund charges a 0.12% net expense ratio (0.14% gross), 2bps below its closest comparable, the SPDR® Bloomberg 3-12 Month T-Bill ETF ( BILS ).

{kind=link}

Goldman Sachs

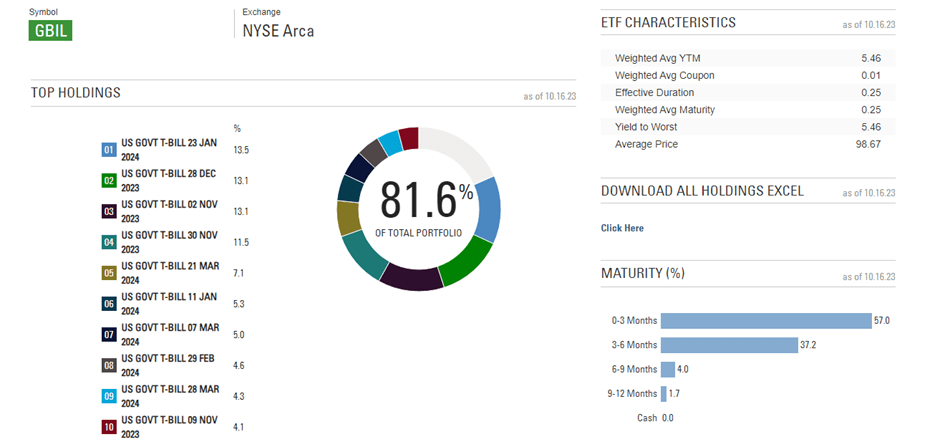

The fund is spread across 25 Treasury holdings, with a weighted average portfolio maturity of 0.25 years and an average yield to maturity of 5.5% (5.5% yield to worst). Specifically, the maturity profile is focused on the 0–3-month maturity (57.0%), followed by 3-6 months (37.2%), and 6-9 months (4.0%). Like other ETFs targeting shorter maturity Treasuries, the fund has far less duration risk, meaning it fluctuates less with interest rate changes. Importantly, though, the fund targets the full spectrum of T-bills (i.e., 0-12-month maturities), giving it a slight yield edge over the likes of more targeted T-bill ETFs like the iShares 0-3 Month Treasury Bond ETF ( SGOV ) and BILS.

{kind=link}

Goldman Sachs

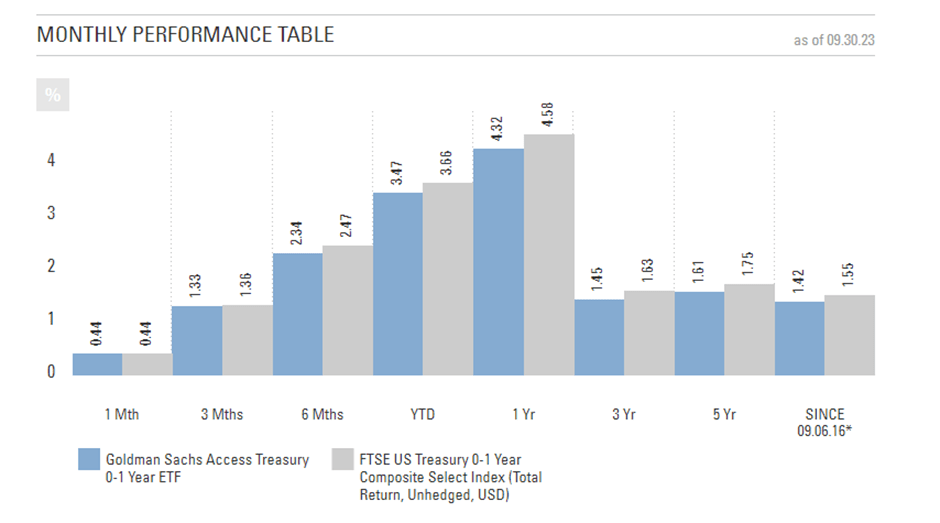

On a YTD basis, the ETF has appreciated by +3.5% in NAV terms (+3.4% in market price terms), slightly outpacing comparable front-end funds like BILS due to its overweight on 0-3-month maturities. On the other hand, GBIL returns haven't been quite as great over longer time frames, annualizing at a +1.4% pace since its inception in 2016. So, while the fund's low duration has shielded investors from the steep drawdowns suffered by ETFs targeting the long end of the Treasury curve, GBIL probably won't deliver the kind of long-term upside offered by equities and corporate bonds. In the current environment of volatility, uncertainty, and inverted yield curves, though, GBIL's balance of income (over 5% 30-day SEC yield) and principal protection make it a great place to park some excess cash.

{kind=link}

Goldman Sachs

Policy Path Likely Unchanged Despite Core/Super-core Pressures

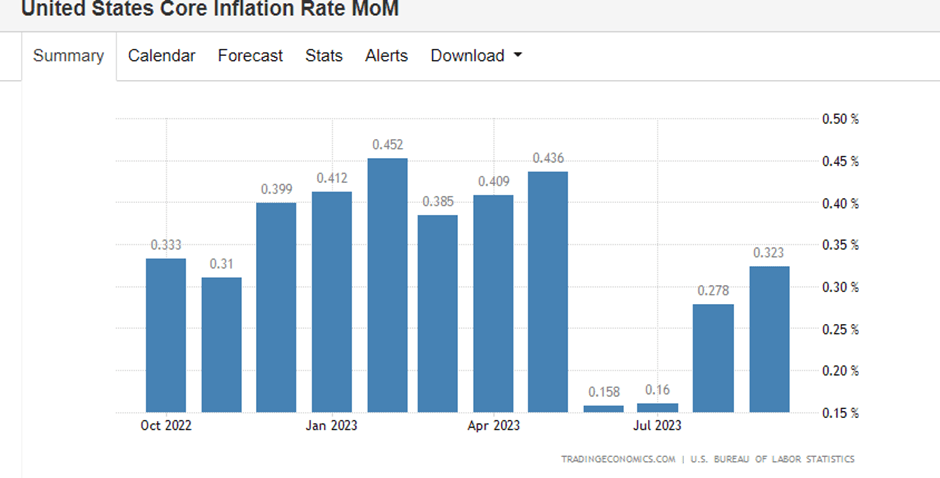

Throughout the month, the 'Fedspeak' messaging has been clear - tightening of higher long-end yields has done a good portion of the work for the Fed (equivalent to one additional hike per one member ). Even with the September CPI report surprising to the upside, the extent of the inflationary pressures doesn't warrant a meaningful deviation from a neutral policy path. To recap, core CPI inflation accelerated to +0.3% MoM in September (headline inflation was up +0.4% MoM), while the all-important 'super-core' CPI inflation (i.e., services excluding energy and housing) accelerated at a faster +0.6% MoM. The latter was driven by higher non-rent service prices, while the pace of core and headline inflation was mainly down to owners' equivalent rent (i.e., homeowners' rental estimates) and lodging-away-from-home prices offsetting lower used vehicle prices.

{kind=link}

TradingEconomics

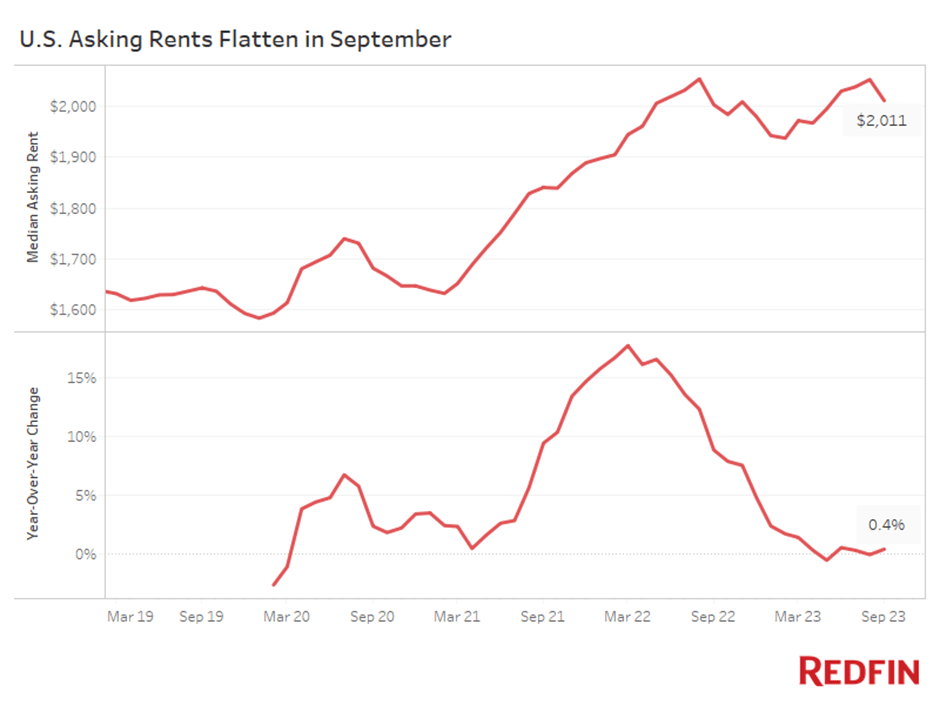

Despite the headline miss, a closer read of the inflation report suggests a benign outcome remains on the cards. The owners' equivalent rent component, the key driver behind the acceleration, is, after all, a lagging estimate and hasn't fully reflected the impact of higher mortgage rates (now at ~8%) on the housing market. Increases also contrast with leading private rent trackers ( flattish YoY per Redfin ) that have continued to moderate through this year. Plus, it's worth noting that the super-core PCE basket, which features lower weights on volatile items than the CPI, is what the Fed targets. And relative to median forecasts for a +3.7% YoY print in Q4, inflation is tracking well within range. Thus, further hikes seem unnecessary here, given the well-telegraphed commitment to higher-for-longer rates.

{kind=link}

Redfin

Balancing Income and Principal Protection

The Treasury curve has remained inverted through the year, and until it normalizes, there isn't a better 'risk-off' asset than short-duration Treasury Bills, in my view. While inflation remains a factor (see the stronger-than-expected headline and core CPI prints this month), a lot of the incremental tightening has already been done by the steepening yield curve.

Hence, the odds are that the Fed will remain on hold through year-end vs current market pricing for a non-zero probability of a Q4 hike, limiting the downside at the front end. The demand/supply balance is also much better supported at this section of the curve, given bill yields at over 5% are already at a premium to comparable rates available to institutional and retail investors. Investors looking for alternatives to owning the bills outright and don't mind some reinvestment risk should find a lot to like in GBIL, currently among the lowest-cost ETFs targeting the full spectrum of under 12-month maturities.

For further details see:

GBIL: Balancing Income And Principal Protection