GCV - GCV: More Interesting At Current Discount

2023-12-12 05:51:23 ET

Summary

- Gabelli Convertible & Income Securities Fund has fallen to a discount, making it a much more compelling choice compared to where it was.

- GCV's portfolio is diversified and seems to have become even more varied in terms of sector exposure.

- The fund's distribution rate is high but lacks coverage and seems precarious, posing a risk, but it's also what could be the driving factor to see a narrowing discount.

Written by Nick Ackerman, co-produced by Stanford Chemist.

The last time we touched on the Gabelli Convertible & Income Securities Fund (GCV) was earlier this year in April . At that time, it was a recap to touch on how our prior idea of swapping GCV in favor of the Ellsworth Growth and Income Fund (ECF) played out. While I still wasn't overly bullish on GCV at that time, it at least looked much more appealing.

Since then, the divergence has continued to actually play out despite GCV's much more attractive distribution rate. A good reminder that, eventually, given enough time, valuation wins out in terms of discounts/premiums with closed-end funds. With that being said, GCV has now succumbed to a discount, and enough of a discount to make it interesting. That's made its fall look much more dramatic for investors as it came off of a premium level.

Despite this, the discount for its ECF peer does remain larger on an absolute basis. So, if I had to pick one over the other, I would still tend to lean toward ECF, but on a relative basis, GCV is looking compelling.

The Basics

- 1-Year Z-score: -1.68

- Discount: -9.42%

- Distribution Yield: 13.87%

- Expense Ratio: 1.95%

- Leverage: 16.67%

- Managed Assets: $90 million

- Structure: Perpetual

GCV's investment objective is to "seek a high level of total return on its assets." They will attempt to achieve that objective by a "disciplined approach to investing in convertible securities and other debt or equity securities that are periodically expected to accrue or generate income." They also mention that their "goal is to generate consistently positive inflation-adjusted returns."

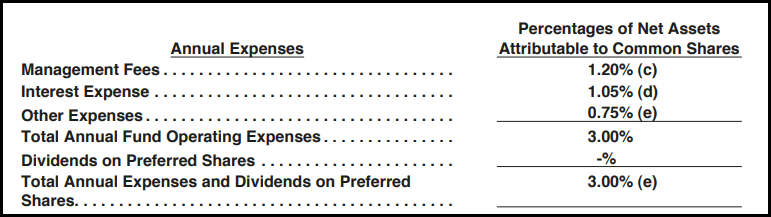

The fund's total expense ratio, when including leverage, comes to 3%. Given it is a smaller fund, it isn't a surprise to see a higher expense ratio.

{kind=link}

However, the fund also has fixed rate leverage. That put it in a better situation when rates were rising, and even now, the fund benefits from a lower cost of leverage relative to having to borrow on a credit facility, where most funds see costs rise to 6%+.

GCV Capital Structure (Gabelli)

Performance - Valuations Matter

Our recap article was initially posted on April 13, 2023. Since that time, we can see that GCV's total NAV return slightly beat out that of ECFs due to a slightly different portfolio. However, thanks to the large plunge from a slight premium to a deep discount for GCV, on a total share price return basis, it wasn't even close. Bearing in mind, during this period, it isn't as though either fund had put up an enviable performance to boast about.

Ycharts

If we want to go back further to when I originally pointed out the opportunity for a swap, we'd have to go back to the public posting on July 17, 2022. From there, we can see that the divergence was even more significant in terms of total share price returns. You either lost a boatload in GCV or came out about flat with ECF.

Ycharts

Both funds hold significant weighting to convertibles, which faced pressure after having a rocking good 2020 and maintaining significant gains through most of 2022 before tumbling; this was a time when investors were clamoring over anything with growth. With higher rates, investors could find income from safer sources such as risk-free Treasuries.

Ycharts

On the other hand, convertibles are looking more attractive overall and were highlighted this year by Calamos , a convertible specialist firm, that we are seeing two things happen.

First, yields have risen, so any convertibles on the market today or being issued today have to be more competitive. This often means a higher initial yield and or lower conversion premiums.

At this time last year, the coupon of a new convertible issue was nearly 0% and the average conversion premium was nearly 35%.

This meant that an investor in a new convertible was paid very little or nothing to wait for the underlying stock to appreciate 35% before the conversion option would move into the money. More recently, terms have improved as interest rates have moved higher. The typical coupon on convertibles now exceeds 4% with a conversion premium below 25%

Second, they also noted that besides these more favorable factors, higher quality companies are coming to the market to issue convertibles. The reason is simple. Rates have risen, and when refinancing comes due, companies are either faced with paying down debt or refinancing at now higher rates. Given the convertible feature of these securities, companies can still get away with relatively lower yields being issued, so the higher financing costs don't cut too much. Of course, the downside comes with potential future dilution to the equity shareholders.

With that, prospects for convertibles are more encouraging in this current environment going forward. Given GCV's now sizeable discount, there could be a tactical play here.

Ycharts

Distributions - Precarious But Tempting

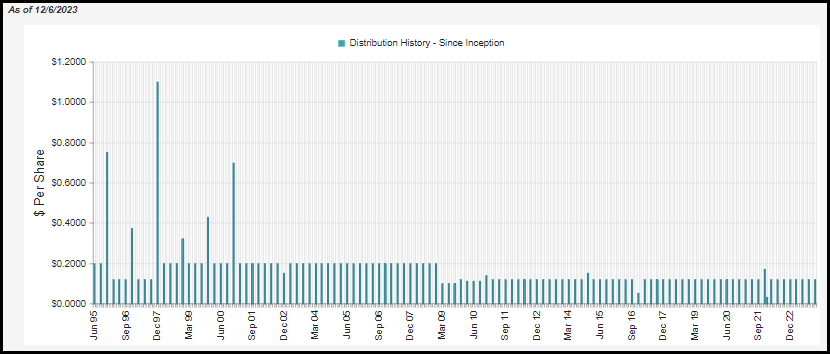

The biggest draw on some CEFs is higher distribution rates, and they can get to a point where they get too high, and that's when yield chasing generally happens. Whether the distributions are supported or not, the deciding factor for what many think is an interesting investment is the higher distribution rate. So it's worth pointing out that with GCV's price falling relatively dramatically, its distribution rate has extended further to nearly 14% now.

On an NAV basis, the distribution rate comes to an elevated 12.57%. Similar to ECF, GCV comes with a minimum managed distribution policy. In this case, it comes to 8%, so they are paying well above the stated minimum amount they are looking to deliver.

We already know that Gabelli really has an issue with cutting distributions when they should, so that's what could make this investment more compelling: the fact that they have historically avoided making adjustments.

Gabelli Utility Trust (GUT), in particular, is an extreme example and is the poster child of absurdity with not only a 20%+ NAV distribution rate but also a 100%+ premium. When they cut, or the fund ceases to exist because it pays out all of the NAV, there will be investor tears . I digress.

The last time for a distribution cut for GCV was in the global financial crisis, but clearly, looking at the annualized past performance, they haven't been able to really earn this, or NAV would have been flat over time. So, a distribution cut seems to be a main risk here in what could see GCV's discount widen further or at least not recover.

{kind=link}

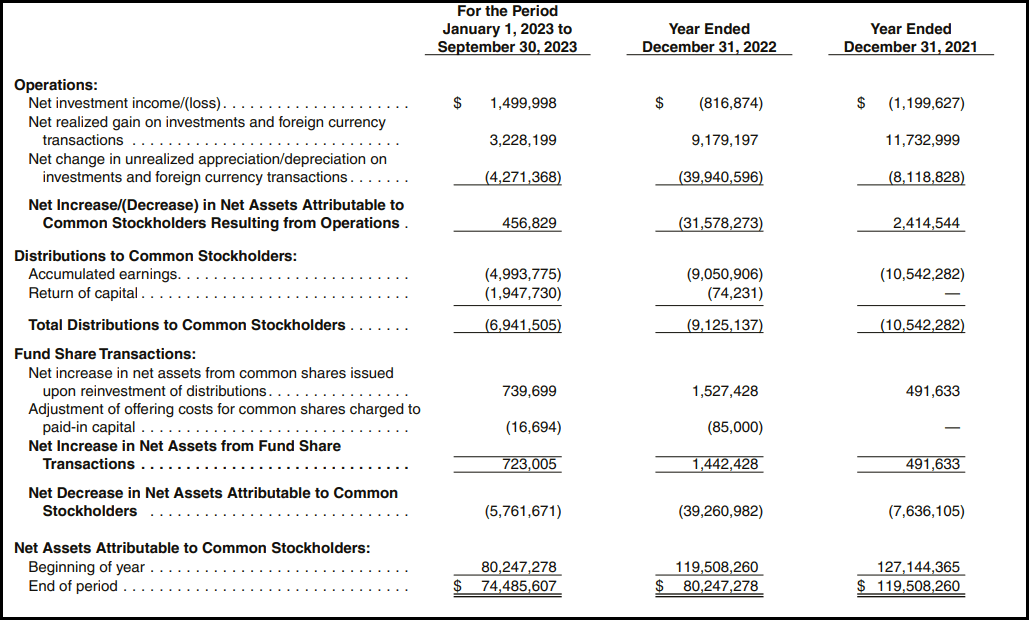

The fund's last annual report showed that the fund generated net investment income, which was a massive improvement from 2022 when it produced no positive NII. This was for an abbreviated period, which is worth pointing out because the fund switched to a fiscal year-end of September 30 as opposed to December 31 previously. This put it in line with its sister funds.

{kind=link}

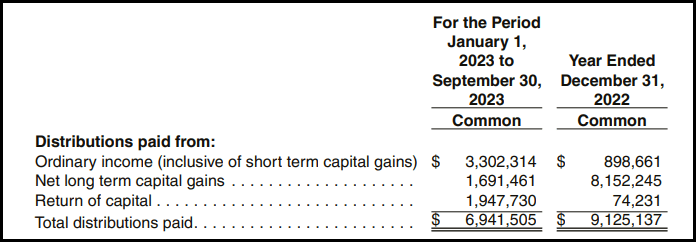

On a per-share basis, that worked out to $0.08, so clearly, there is still room for improvement. Essentially, the vast majority of the distribution would need to be covered through capital gains. Despite the strong prospects of convertibles in the future, it is still going to be a high hurdle to leap to put it at a sustainable level. With that, expect NAV to continue to dwindle away. Thus, I feel that the fund is more of a tactical play in the shorter term for potential discount narrowing.

For tax considerations, the fund is mixed. We see ordinary income, long-term capital gains and return of capital in each of the prior two years. That can make it difficult to come to a clear conclusion on which type of account an investor would find to be the most appropriate, tax-sheltered or taxable.

{kind=link}

GCV's Portfolio

As is often the case with convertible funds, they are positioned more in tech-oriented sectors that are commonly going to be growth-focused. That said, with GCV, one is getting meaningful exposure to other sectors such as energy and utilities, healthcare, and financial services, with business services also making up fairly meaningful weights.

GCV Top Sector Weighting (Gabelli)

Last year, when we looked at the fund , it did have 21.1% allocated to the computer software and services space. There was another 11.1% in healthcare and 7.6% in business services, with financial services and telecommunications at 5.8% and 5%, respectively.

This could be a function of more companies coming to the convertible space for the reasons discussed above. As we move forward, this will be interesting to watch if we see any dramatic shifts overall or if these tiltings are specific to GCV.

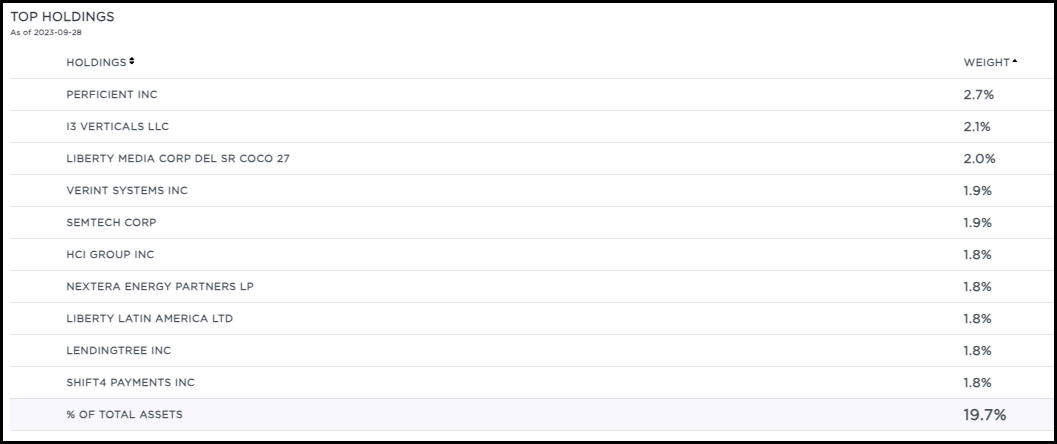

One thing that has been fairly consistent has been the fund's top holdings, reflecting the fact that nothing is really overly outsized in their portfolio. Greater diversification can mean less upside as you get the good with the bad, but alternatively, it should also help with avoiding one position causing too much harm.

{kind=link}

The fund is concentrated in convertibles, but they also were carrying a 12.3% weighting to U.S. Treasury Bills. These yielded anywhere from 5.368% to 5.446%. That was up from earlier in the year from their semi-annual report, where Treasuries were 4.6% and yielding 4.547% to 4.743%.

Worth noting is that equities made up around 4.4% of the fund's assets. That's compared with ECF at a weighting of 17.6% for equities and 7.5% for Treasury Bills.

Going back to the fund's leverage, this is one way to earn a safe income in Treasuries because they are paying a fixed rate of 5.2% on their Series G Cumulative Preferred offering. The spread isn't massive, but it is something. It should also keep volatility slightly lower too.

Conclusion

GCV has mostly acted as expected, which was seeing its large premium come down to a smaller one over the last year and a half. However, from there, the fund continued to sink to where it is now at a deep discount. That puts it at a much more compelling valuation, but I believe it more particularly for those willing to dollar cost average down or take a shorter-term tactical play. The fund's distribution rate is certainly tempting, but it comes with a lack of coverage, and that creates a situation where it becomes the risk but also the driving factor for the potential upside to play out.

For further details see:

GCV: More Interesting At Current Discount