GDEV - GDEV Appears Cheap With Hero Wars Game And FCF Growth

2023-08-02 17:52:01 ET

Summary

- GDEV Inc. reported positive FCF and double-digit growth in paying users and active users.

- Further expansion into new territories and development or acquisition of new video games could drive future FCF growth.

- GDEV appears undervalued, but there are risks from failed monetization or problems with advertising platforms.

GDEV Inc. ( GDEV ) is the owner of the Hero Wars video game, and recently reported positive FCF as well as double digit paying users and active users growth. In my view, as soon as market participants review the recent corporate developments , and understand the potential growth of GDEV, we may see growing demand for the stock. I believe that further expansion into new territories like Latin America or Asia, new acquisition of video games, and further development of video games will most likely bring further FCF growth. Yes, there are risks from failed monetization or problems with advertising platforms, however GDEV does appear undervalued.

GDEV

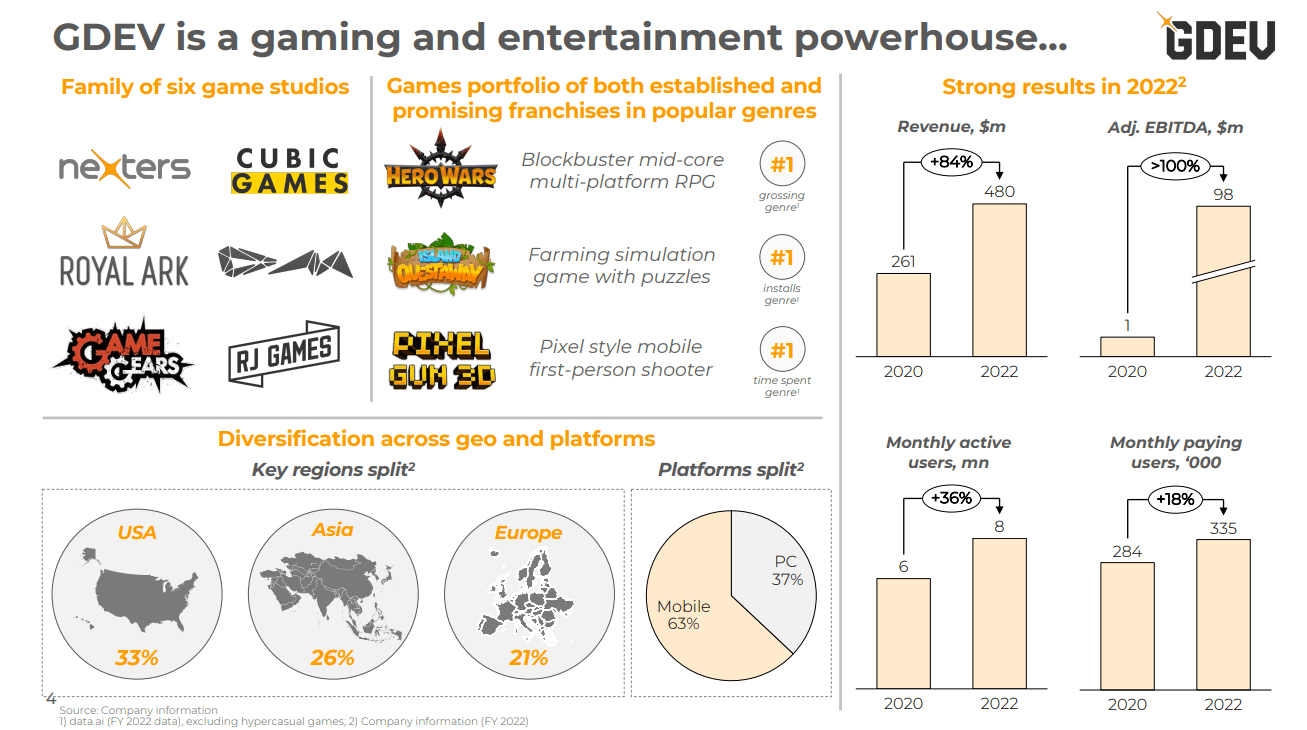

GDEV is a company dedicated to the development of video games for mobile and internet formats for millions of users around the world. The company is among the top 5 indie developers in Europe.

The games that GDEV offers are free to use, and the profits come from advertisements and unlocking features within these platforms. The company's most relevant product is the Hero Wars video game, introduced in 2016.

Historically, we have depended on Hero Wars for a majority of our revenues, and we expect that this dependency will continue for the foreseeable future. For the years ended December 31, 2022, 2021 and 2020, Hero Wars generated 96%, 99% and 98%, respectively, of our revenues for each period. Source: Prospectus

With that, during 2022, this video game franchise was ranked within the top 10 of Android users and the top 8 of iOS users.

Source: Investor Presentation

The activities are gathered in a single business segment that covers all the developments of the company: videogames of different categories such as RPGs, casual games, and mid or hard-core games. Between 2013 and 2018, the company achieved an increase in the number of contracts made within its video games, breaking the 1.5 billion mark in historical records.

Based on its customer and user base, according to the prospectus, the forecast for the future continues to include growth, sustaining the monetization of the use of the platforms. It is worth saying that during 2022, almost 80% of the contracts were within the video games of the Hero Wars franchise, the main product of GDEV.

With a presence in the USA, Asia, and Europe as well as double digit paying users and active users growth, in my view, I would expect further business growth in the coming future.

{kind=link}

Balance Sheet

The last balance sheet reported included right-of-use assets worth $1 million, intangible assets close to $12 million, and goodwill of about $1 million. Besides, with long-term deferred platform commission fees of about $94 million, total non-current assets stood at $133 million. Current assets included trade and other receivables of about $45 million, other investments worth $50 million, cash and cash equivalents close to $86 million, and total assets of $322 million.

The asset/liability ratio appears to be below 1x, which is not ideal, however let’s remember that GDEV owns many video games, which may include intangible assets. The valuation of these assets is always a bit difficult, so the total amount of assets could be a bit larger than reported.

Source: Prospectus

With respect to the list of liabilities, long-term deferred revenue stands at $96 million, with share warrant obligation worth $13 million and a put option liability of $27 million. GDEV also reported trade and other payables of close to $30 million, provisions for non-income tax risks worth $1 million, deferred revenue worth $295 million, and total liabilities of $470 million.

Source: Prospectus

DCF

Under my financial model, I assumed that the company would continue to focus on its existing intellectual property as well as to improve the product offering and its monetization. Besides, I believe that demand for the stock will appear if the company successfully diversifies the revenue channels currently focused on the Hero Wars franchise. More diversification may bring lower volatility in net sales. If demand for the stock increases, the cost of capital may decrease, which would lower the WACC, and push the valuation of the stock up. Management discussed some of these capabilities in a recent presentation given to investors.

Source: Investor Presentation

I also expect further expansion and improvement of the information traffic channels in order to gather data to guide the profiles of potential customers who are willing to pay for the benefits within the platforms.

Besides, further increase in the supply of products to new markets, mainly the Asian market, will most likely accelerate net sales growth. With know-how accumulated in the United States and Europe, I think that existing video games may also be profitable elsewhere.

Finally, I believe that new merger and acquisition opportunities with other companies and hiring of the best talent available in the sector will also play a major role in FCF generation. I think that GDEV did prove that it knows how to conduct M&A operations, and successfully hired a lot of personnel.

Our headquarters are in Cyprus. As of June 30, 2022, we had 1,044 employees. On June 29, 2022, the Company had announced changes to its headcount; accordingly, as of December 31, 2022, we had approximately 848 employees. Source: Prospectus

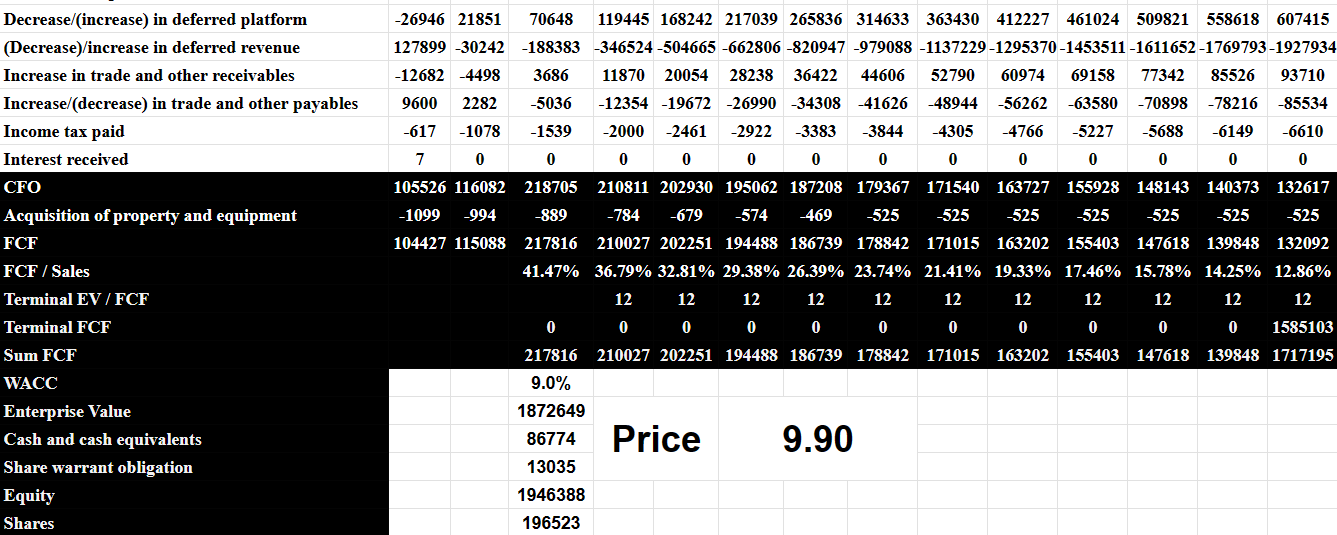

I was quite conservative while conducting my financial model. I assumed 2034 net revenue worth $1.026 billion, with net revenue growth lower than 9.5% and net income/net sales close to 25%-14%.

{kind=link}

My model also included 2034 depreciation and amortization close to $59 million, 2034 share-based payments expense worth $3 million, changes in goodwill of about $816 million, and 2034 impairment loss on trade receivables close to $388 million.

{kind=link}

Besides, with changes in deferred platform revenue of $607 million, changes in deferred revenue close to -$1928 million, and increase in trade and other receivables worth $93 million, I obtained 2034 CFO of about $132 million.

If we also assume 2034 acquisition of property and equipment of -$1 million, 2034 FCF would be close to $132 million. Finally, if we also include FCF/Sales close to 12x, the terminal FCF would stand at $1.585 billion.

With a WACC of 9%, the implied enterprise value would be $1.872 billion. If we add cash and cash equivalents worth $86 million and share warrant obligations of $13 million, the implied equity would be $1.946 billion, and the fair price would be $9.9 per share.

{kind=link}

Competitors

Competition in this market is high and is given by independent and private video game developers. Depending on the type of video game, the competition is based on the interest of the users, with specific niches in each case. In general terms, all video games developed for mobile devices or computers generate competition for GDEV in any of its product lines. It is interesting to note that the conditions for entering the competition through a new product are apparently low due to the ease of development and distribution, but this does not translate to the monetization capacity and the scale growth of the companies that offer them. According to statistics from data.ai, during 2022, only 164 games with international users maintained profits above $100 million, which shows that competition at the macro level is determined by high barriers and conditions for the entry to the markets.

Risks

Two fundamental factors to name within the company's risks are its total dependence on third-party platforms for the distribution of video games and the reach of users, who can change their delivery policies at any time, and the concentration of profits that the company has in only one of its products. Within this concentration, there is also a concentration on a low number of users, which means the total earnings for this video game. During 2022, 10% of paid users generated 84% of the profits. Undoubtedly, this is a risk factor to review in order to make a general analysis of the company.

Regarding the conditions of the industry, GDEV must manage offers and prices for the paid functions of its video games in accordance with the global economic conditions along with attracting new users through a correct reading of the forecasts on tastes and preferences in video games. This factor linked to price management accompanies that of managing the company's growth as well as future acquisitions that are part of its current strategy. The same is true if we talk about the ability to attract companies that pay for advertising within their platforms.

Our games are primarily accessed and operated through Apple ( AAPL ), Facebook ( META ), and Google (GOOGL) ( GOOG ), which also serve as significant online distribution platforms for our games. Substantially all of the virtual items that we or our distributors sell to paying players are purchased using the payment processing systems of these platforms. Consequently, our prospects and expansion depend on our continued relationships with these providers, and any other emerging platform providers that are widely adopted by our target players. Source: Prospectus

In addition to the operational and industry risks, we must mention that a large part of GDEV's business success is given by the collection and use of user data, and this practice is subject to a large number of regulations and possible changes in the forms of collection. The regional legal frameworks and their variation in the application can eventually generate complications for the expansion of the business in certain markets and keeping the operational structure running, forcing the company to re-adapt its information traffic channels and the implementation of new strategies.

When our players use our games, we may collect both personally identifiable and non-personally identifiable data about the player. Often, we use some of this data to provide a better experience for the player by delivering relevant content and advertisements. Our players may decide not to allow us to collect some or all of this data or may limit our use of this data. Any limitation on our ability to collect data about players and game interactions would likely make it more difficult for us to deliver targeted content and advertisements to our players. Source: Prospectus

Conclusion

GDEV does not only report FCF, but also double digit paying users and active users growth. I think that further expansion into new territories in Asia and development or acquisition of new video games could bring significant FCF generation in the coming years. I believe that market participants did not really review GDEV, and the market did fail to understand that GDEV is the owner of the Hero Wars video game. In my view, the company appears quite undervalued at its current price mark.

For further details see:

GDEV Appears Cheap With Hero Wars Game And FCF Growth