GDL - GDL: Equity Merger Arbitrage CEF 5.9% Yield

Summary

- The GDL Fund is an equity arbitrage CEF from the Gabelli suite.

- The CEF falls in the equity relative value bucket, aiming to profit irrespective of the general market direction.

- A recent relevant example that falls in this category is the potential Twitter takeover by Elon Musk.

- This article covers CEFs from our suite of products - we focus on CEFs and yield-generating options strategies, targeting overall yearly portfolio returns of 9%+.

Thesis

The GDL Fund ( GDL ) is an equity merger arbitrage CEF from the Gabelli suite. The fund has total return as its main objective and aims to make money regardless of the general direction of the market. The fund focuses on merger arbitrages, corporate reorganizations and liquidations. As per Wall St Prep :

Merger arbitrage is an investment strategy that seeks to profit from the uncertainty that exists during the period between when an acquisition is announced and when it is formally completed. A simple merger arbitrage example will illustrate this: On June 13, 2016, Microsoft announced its acquisition of LinkedIn, offering $196 for each LinkedIn share. On the announcement date, LinkedIn shares jumped from the $131.08 pre-announcement price to close at $192.21.

The period between when a deal is announced and when it closes (and Linkedin shareholders actually get their $196) can last several months. During this period, Linkedin shareholders still have to vote to approve the deal and the companies still need to secure regulatory approvals and file a whole bunch of legal paperwork.

In a nutshell merger arbitrages and corporate reorganizations are relative value strategies. These strategies do not benefit from a market direction like a traditional mutual fund or closed end fund, but the benefit lies in the transaction occurring and the original "arbitrage" opportunity crystalizing. In the above example from Wall St Prep the money was made by betting the transaction will go through and the market price will ultimately end up at the same level as the merger offering.

To better contextualize this concept let us consider today's environment - in our opinion we are in the midst of a bear market rally. Let us presume that Microsoft decides to acquire another software company, let us call it Company ABC. Company ABC is trading at $79/share before the announcement. Microsoft comes out with the announcement for a takeover offer for $100/share. If the Company ABC stock does not rise to $100/share immediately then a merger arbitrage opportunity arises. Even if the general market subsequently tanks, the arbitrage opportunity still exists and theoretically should not be affected by the general market move.

These strategies are not always successful become sometimes the mergers do not go through. The best recent example is the Twitter ( TWTR ) saga, where Elon Musk announced his bid to take the company private only to rescind the offer later. In this case a portfolio manager who would have bought TWTR shares in the hope of the transaction going through, would have lost money. Merger arbitrage is not always easy.

That being said it should be clear by now that the "secret sauce" in these type of fund strategies is composed by portfolio managers and their ability to correctly understand the market dynamics and ultimate outcome of the merger. The risk factor here is the CEF's portfolio management team. And in this instance the only available benchmark is their track record. Mergers and reorganizations will always exist. The ability of a fund to take advantage of said opportunities can only be gauged at looking at how successful they were in the past in doing so. Which brings us to the next section of our article, namely "Performance".

Performance

The fund is down only marginally this year versus the directional S&P 500:

{kind=link}

In this case though one year of data is not that relevant, so let us have a look at performance longer term:

{kind=link}

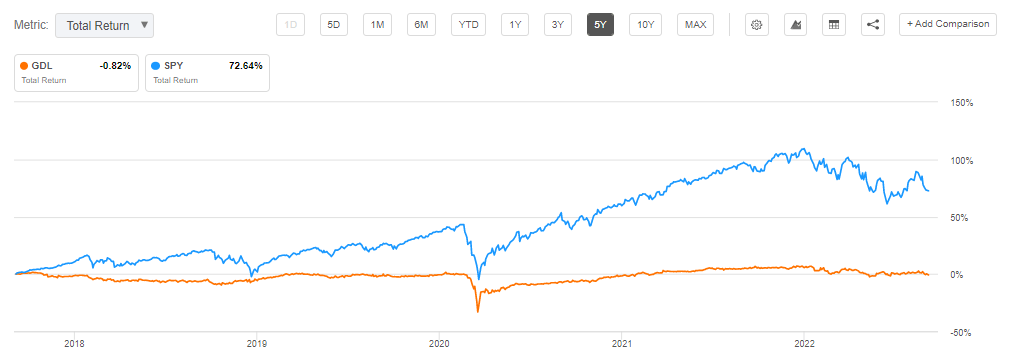

On a 5-year basis the fund is flat versus an outsized performance for the S&P 500. On a 10-year basis the fund is up, but not significantly:

{kind=link}

We can see from the above that on an annualized basis the fund produced only 2.4% per year in the past decade. That is fairly poor.

GDL Holdings

The fund keeps a larger portion of its assets in cash to clip yield when there is a lack of deals to invest in:

Portfolio Highlights (Fund Fact Sheet)

The top names in the fund currently are:

Top Names (Fund Fact Sheet)

However please keep in mind that the names themselves do not matter that much. The transaction/arbitrage opportunity occurring is the important risk factor here.

Premium/Discount to NAV

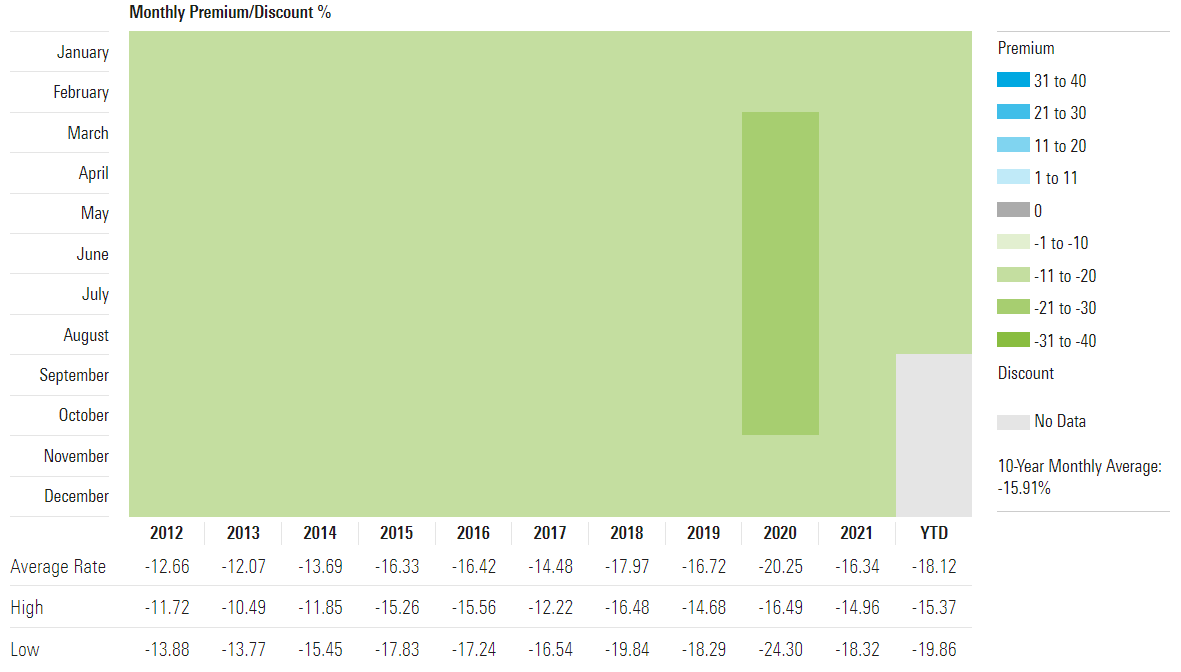

The fund has always traded at a discount to NAV:

{kind=link}

We can observe nice "green" boxes above, meaning the fund never traded at a premium to NAV in the past decade. Currently, the market does not appear to believe in this fund, with the discount at almost -20% now.

Conclusion

The GDL Fund is a small equity merger arbitrage CEF from the Gabelli suite. The fund has total return as its main objective and aims to make money regardless of the general direction of the market. The fund focuses on merger arbitrages, corporate reorganizations and liquidations. These type of funds thrive only through the performance of their portfolio managers, given the lack of market directionality they are taking. GDL has posted mediocre long term returns, with the fund being flat on a 5-year basis (i.e. no return) while on a 10-year time frame the annualized total return is a meager 2.4%. The fund currently holds 50% of its capital in cash, waiting to deploy it for new transactions. We feel the cash portion of the fund will make the bulk of its performance for the year given where risk free yields are. For us there is nothing here that would prompt a retail investor to take a position or consider this name.

For further details see:

GDL: Equity Merger Arbitrage CEF, 5.9% Yield