GDL - GDL Trades At A 20% Discount To NAV Despite A Track Record Of Outperformance

2024-01-15 07:00:18 ET

Summary

- Gabelli Global Deal Fund is a closed-end fund managed by Mario Gabelli's GAMCO investment complex and focused on merger arbitrage.

- GDL has a strong investment track record, consistently outperforming its benchmark and other merger arbitrage-focused ETFs.

- The fund currently trades at a 20%+ discount to its net asset value, offering the potential for higher forward returns.

- GDL is taking advantage of the discount to NAV by aggressively returning capital to shareholders.

Thesis

Gabelli Global Deal Fund ( GDL ) is a closed-end fund that is part of famed value investor Mario Gabelli's GAMCO investment complex. GDL has a long track record of outperforming its benchmark via expert management using a niche investment style. Despite strong performance, GDL trades at a 20% discount to NAV.

GDL invests in merger arbitrage and other arbitrage situations. Short-term treasury bill yields are the baseline for pricing merger arbitrage spreads. I expect GDL to be able to continue beating the return of treasury bills with a similar volatility profile. I also expect GDL to be able to continue outperforming its passive benchmark.

However, I wouldn't expect GDL to outperform a traditional equity index over a long period. I'm using GDL for the part of my portfolio I would usually hold in cash or treasury bills that I don't need instant access to.

Investment track record

Merger arbitrage is a specialized investing strategy where investors bet on announced mergers to close. Merger arbitrage strategies are usually seen as alternatives to treasury bills. Since arbitrage situations have a short duration and in theory should not be correlated with the market.

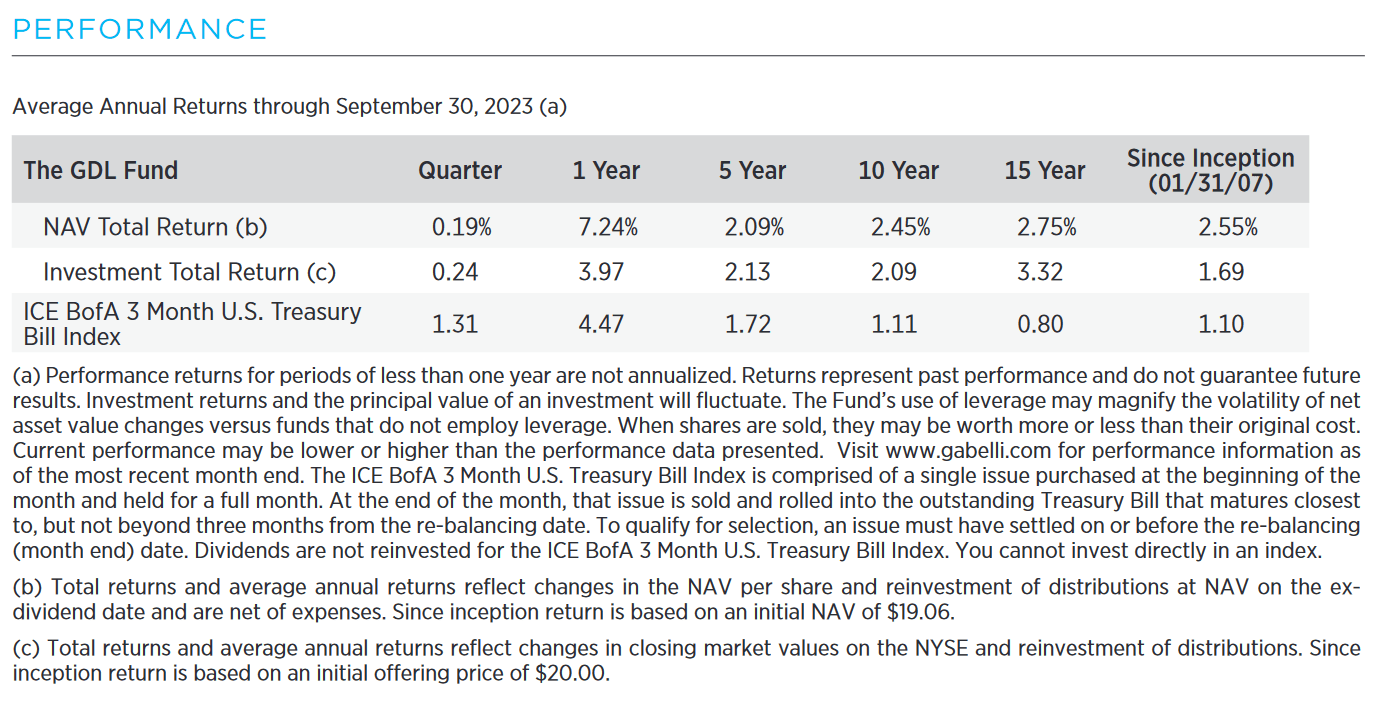

In this light, GDL's performance looks pretty exciting. GDL has outpaced its benchmark over the past 1, 5, 10 years and since inception. It has also outperformed the largest active merger arbitrage ETF, IQ Merger Arbitrage ETF ( MNA ), and the largest passive merger arbitrage ETF ( MRGR ) over the same period. This is even though GDL's discount to NAV has grown over this period.

Since its inception, GDL's NAV has beaten its benchmark by 1.5% per annum. Which is quite large for such a low-return, low-volatility strategy.

{kind=link}

Discount to NAV

GDL currently trades at a ~20% discount to NAV. While it has almost always traded at a discount to NAV. The current discount looks larger than normal especially when compared to before COVID.

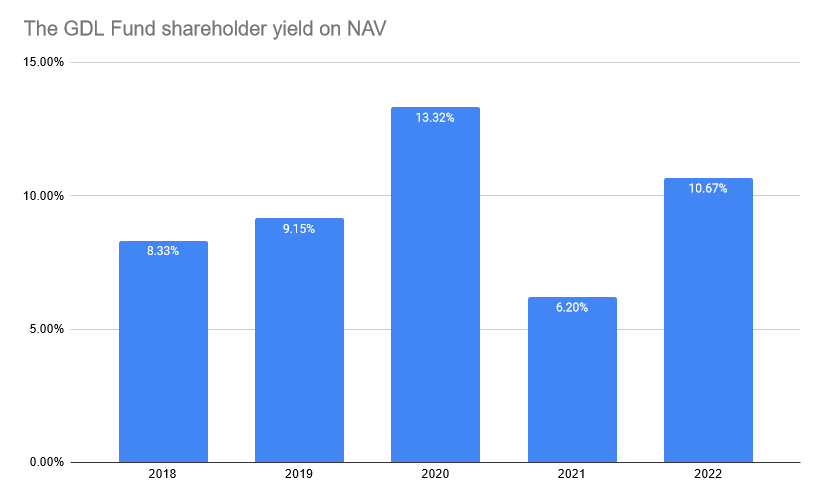

Even though I don't expect the discount to disappear GDL shareholders can still benefit from the discount. To battle the discount to NAV GDL is returning a large amount of capital to shareholders. In addition to a nearly 6% dividend yield GDL spent $10.1M repurchasing its own shares over the past year. When buying closed-end funds at a discount I have a strong preference for ones that have high shareholder yields where shareholder yield is defined as dividends plus buybacks divided by NAV. Over the past 5 years, GDL has had an average shareholder yield on NAV of 9.5%.

{kind=link}

Higher interest rates should also lead to a higher shareholder yield on NAV in the coming years.

Fund holdings

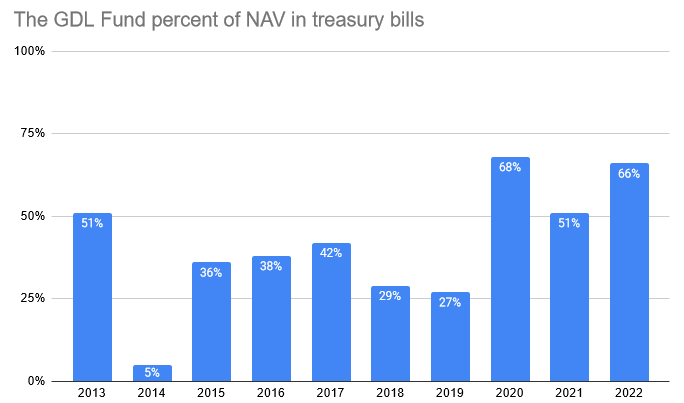

As mentioned GDL invests primarily in merger arbitrage situations. One thing you'll note if you look at the Q3 holdings is that a large percentage of GDL's assets are held in treasury bills. Usually, a closed-end fund doesn't hold its benchmark with 60% of its NAV. I'm not surprised that they are holding some amount in treasury bills. Merger arbitrage has a short holding period. But 60% at a given time seems excessive to me. The allocation to treasury bills at year-end varies quite a lot but has remained high for the last three years.

{kind=link}

GDL also tends to hold a diverse mix of arbitrage situations. Choosing a diversified approach over a concentrated one. A large position will only be 3% of the portfolio. This is typical for arbitrage funds that tend to spread out their bets in an attempt to reduce volatility.

Leverage

GDL's common equity is leveraged by two series of preferred shares. Series C and Series E pay a 4% and 4.25% yield on their liquidation preference respectively. Both have a mandatory redemption date of March 26th, 2025.

{kind=link}

This is an odd capital structure when combined with GDL holding such a larger amount of T-Bills. Currently, this provides a positive carry for GDL since treasury bills are yielding north of 5%. But this hasn't always been the case in the past this dynamic created a drag on GDL's performance.

I'll be interested to see if GDL issues another series of preferred equity in 2025 or if it decides to go without leverage. Diversified merger arbitrage as an investment strategy lends itself to some leverage because of its low volatility. But it doesn't mesh with the fact that the fund is holding such a large amount of treasury bills. If you are going to end up holding treasury bills you might as well just skip the leverage. Cleaning up the preferred shares also might be a precursor to winding down the fund or converting to an ETF either of which would be great for shareholders.

Management fees

One thing to watch with a closed-end fund is management fees. GDL lists its most recent expense ratio as 4.2%. However, this is incorrect, in my view, since they are counting interest expenses on the preferred shares as part of the expense ratio. The fund owes an investment advisory fee of .5% of assets under management plus 1/4 of all out-performance achieved over the benchmark treasury bill index up to a cap of 2%. However, this is also not the correct way to look at the expense ratio, since it doesn't account for overhead expenses or the management fee charged on the preferred equity.

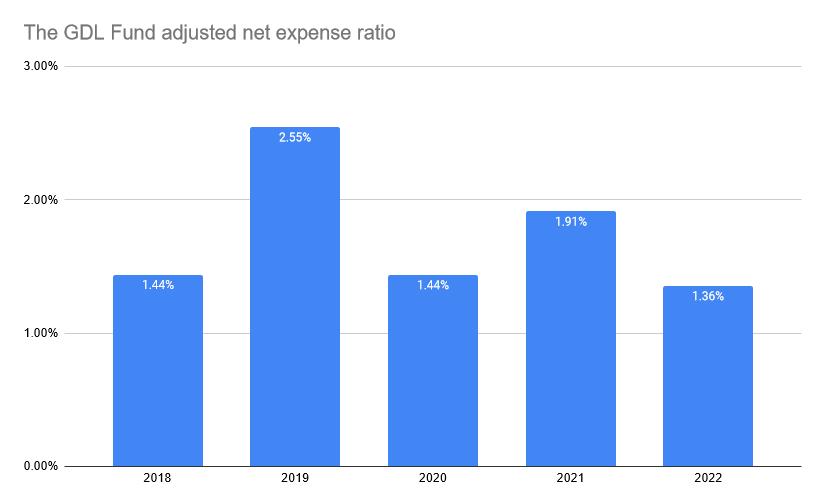

My preferred metric is the ratio of net expenses less interest expense on preferred shares less dividend expense on securities sold short less service fees for securities sold short divided by net assets attributable to common shareholders. For the past 5 years, this ratio has averaged 1.74%.

{kind=link}

A 1.74% expense ratio is high, although it is not particularly high for a closed-end fund. The thing I find most objectionable about it is that GAMCO is charging a management fee for holding a large portion of GDL's portfolio in treasury bills. I would never buy the fund trading at NAV, however there is a price for everything. When looking at closed-end funds I like to buy them at a price where the expense ratio is less than the discount to NAV times the shareholder yield as a percent of NAV.

The logic behind this is when money is returned the discount between the NAV and the shareholder's return is closed. If a closed-end fund trades at a 10% discount to NAV and returns 10% of its capital the investor will accrue a 1% benefit simply from this mechanism. I like closed-end funds where this benefit is larger than the expected expense ratio. As previously discussed the fund returned an average of 9.5% of NAV to shareholders over the past 5 years and I expect stronger returns going forward. So I'm interested in buying GDL when it trades at about a 17% discount to NAV. So I find the current discount of 22% to be interesting.

One other note on alignment is that the investment manager GAMCO owns 40% of GDL. While I'm sure they enjoy the fee stream from management they should be aligned with common shareholders.

Risk - Is GDL non-correlated?

A key selling point of owning GDL and merger arbitrage as a whole is the non-correlation with equity markets. A good example of this is 2022, when GDL returned -.6% on NAV while the overall market returned -18%.

However, if you look at GDL's total return chart since inception you might be skeptical of it being non-correlated. In both the GFC and the COVID scare GDL looks very correlated with the equity markets. Merger arbitrage tends to be uncorrelated with markets unless there is a panic. In a panic, all assets sell off as liquidity is removed from the market. Merger arbitrage spreads tend to blow out in these situations. GDL is doubly exposed to this since it is a low-liquidity closed-end fund.

Given these types of panics are when you'd most like to own treasury bills this is a major flaw in the thesis.

However, I do think there are two good pushbacks here. The impairment is demonstrably temporary. Merger spreads tend to close fairly quickly once the panic ends and the discount to NAV on the fund should eventually reverse. In a sideways or slowly declining market, you should be able to fully benefit from the non-correlation. We just haven't seen many of these types of markets over the past decade.

Where it fits in a portfolio and what I expect it to outperform

I rate GDL a buy, on Seeking Alpha this means the performance will be compared with the S&P 500. But I don't expect GDL to outperform the S&P 500 over a long time horizon. Rather my call for outperformance is against the short-term treasury benchmark index and MNA as a representation of merger arbitrage as an investing strategy.

In terms of absolute returns. You can think of buying GDL as buying a basket of treasury bills at a 20% discount. So if you expect treasury bills to return 5% on a forward basis, I'd expect GDL to return about 6.5% assuming no change in the discount to NAV. Of course, this is an oversimplification but I think it can help give a rough idea of what to expect.

I see value in holding some of my portfolio in short-term treasuries and equivalents given the current interest rate environment. I decided to move about half of the money I was holding in short-term treasuries into the GDL fund. This should allow me to benefit from its outperformance while still having some very liquid assets available to purchase a large bargain if I identify one.

For further details see:

GDL Trades At A 20% Discount To NAV Despite A Track Record Of Outperformance