QQQ - GDP Surprise Throws Predictions Out The Window

2023-10-26 16:40:38 ET

Summary

- U.S. Third Quarter GDP grew at 4.9%, the highest rate in two years, led by Personal Consumption Expenditures - PCE.

- Inventory buildups contributed to growth, while Net Exports reduced GDP.

- Concerns arise over high consumer debt levels and rising delinquencies, as interest rates are expected to rise.

- Fiscal and monetary policy are working at cross-purposes so that the Federal Reserve can continue to pause as the market does the Fed's job.

- We expect consumer discretionary stocks, regional banks, and bonds to all decline. We're in anomalous times.

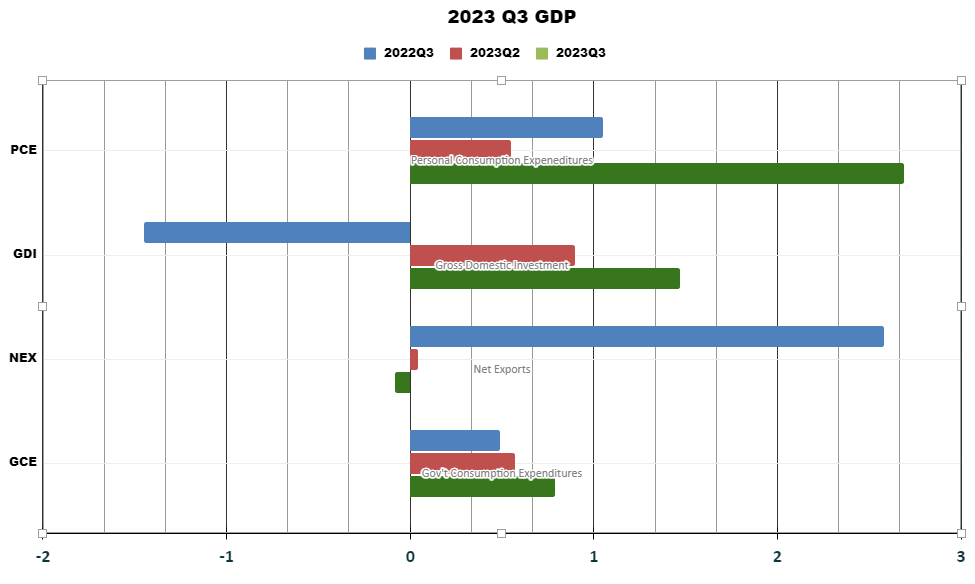

NEW YORK (Oct 26) - Third Quarter GDP surprised to the upside this morning, at 4.9%, the strongest rate of growth in two years. Growth was led by Personal Consumption Expenditures ("PCE"), as seen in our exclusive chart.

2023Q3 GDP by Major Category from BEA Data (The Stuyvesant Square Consultancy)

{kind=link}

The second largest component of growth was inventory buildups, accounted for under Gross Domestic (Private) Investment ["GDI"]

Government Consumption Expenditures ["GCE"] were the final increase to GDP as Net Exports ["NEX"] reduced GDP.

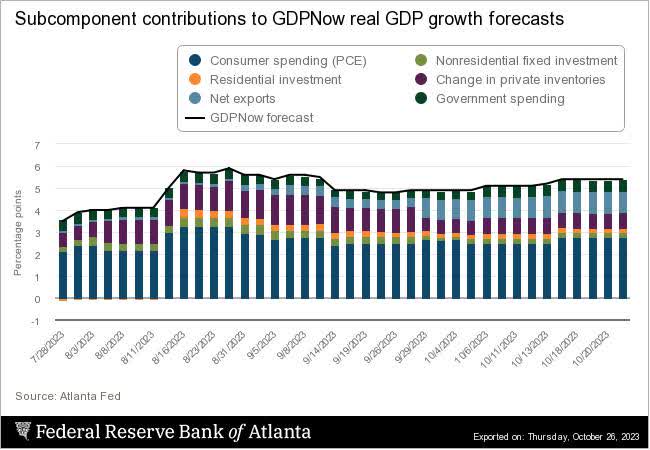

Most of the GDP PCE growth seems to have come in the Summer months. (Note that the chart below, by which the Atlanta Fed keeps track of the GDP for its "GDP Now" estimates, includes data after September 30.)

GDP Accumulation from July to October (Atlanta Federal Reserve)

{kind=link}

PCE has cooled since August, but net exports have surged after the end of the quarter.

ANALYSIS AND PROGNOSTICATION

Of the PCE spending, most was for services and, of those services, the greatest increases were - in order - for housing, healthcare, financial services, and food services and accommodations.

Today's numbers certainly exceeded expectations, and substantially so. But the investors should concern themselves with its makeup and the heavy reliance on PCE.

Consumer debt levels are, today, at their highest levels in over 20 years , although debt, as a percentage of income, is just around 9.8% , which is not excessive, given history. (It was about 14% prior to the 2008 financial crisis.) But delinquencies are rising and are at the highest levels since before the pandemic.

As the Five Year bond (US5Y) comes "danger close" to the 5% mark, investors should be wary of the ability of middle- and lower-income Americans to purchase consumer discretionaries at the same rate. Credit cards are being used more to counter inflation, and the supplemental pandemic cash many received is long gone.

We expect interest rates to continue to escalate, but mostly on the longer end of maturity as the markets do much of the Fed's job for it. We have said for some time that the terminal rate will be in the neighborhood of 6%, +/- 50 bps. We're close to that now. But the Federal Reserve and the Biden Administration are working at cross-purposes: as the Fed raises rates and tightens quantitatively, the Biden Administration has added $ 4.8 trillion to the deficit, according to the Committee for a Responsible Federal Budget, most recently in a $600 billion tranche accrued in a single month, according to the guys over at Zero Hedge.

{kind=link}

In that environment, Bloomberg points out that the old purchasers of Treasury Bills - governments, institutions, banks and the Fed itself - have been replaced by new purchasers of Treasurys - hedge funds, insurers, and pensions -

... that, unlike their more price-agnostic predecessors ...[are] likely to demand a heavy premium to finance Washington’s spendthrift ways, especially with debt sales set to surge as deficits swell .

While we anticipate higher rates, and credit standards tightening, we also expect profits in the consumer discretionary and durables sectors to fall. So, a downturn in both equities and bonds is likely into 2024.

Some regional banks may also face the kind of challenge that Silicon Valley Bank et. al. faced earlier this year as bond yields increase and they incur unrealized losses on their bond portfolio.

For the time being, modeling six months into the future is much more challenging as market behaviors (e.g., declining stocks and bonds) are currently anomalous. That said, we think a fourth quarter GDP in the range of 3% (+/- 25 bps) is most likely. First quarter 2024 is too unpredictable to estimate at this time. Watch for updates for our views and GDP updates in our monthly jobs reports and our X feed, @stuysquare, for additional commentary.

___________________________

Note: Our commentaries most often tend to be event-driven. They are mostly written from a public policy, economic, or political/geopolitical perspective. Some are written from a management consulting perspective for companies that we believe to be under-performing and include strategies that we would recommend were the companies our clients. Others discuss new management strategies we believe will fail. This approach lends special value to contrarian investors to uncover potential opportunities in companies that are otherwise in a downturn. (Opinions here with respect to whether to buy, sell, or hold such companies, however, assume the company will not change its current practices).

For further details see:

GDP Surprise Throws Predictions Out The Window