SWMAY - GDV: Attractively Discounted And A ~6% Distribution Yield

- GDV continues to reward shareholders through its steady monthly distribution.

- The fund also continues to remain at an attractive discount.

- Combining the discount with lower broader markets makes GDV a fairly attractive fund worth considering.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on July 28th, 2022.

In our previous update of Gabelli Dividend & Income Trust ( GDV ), the fund was in a similar situation with a wider discount than usual. The discount continues to remain attractive at a wider discount with the combination of the overall market declines.

In fact, the discount since that update has slipped just a tad deeper, too. That can present a compelling opportunity to add to or initiate a position potentially.

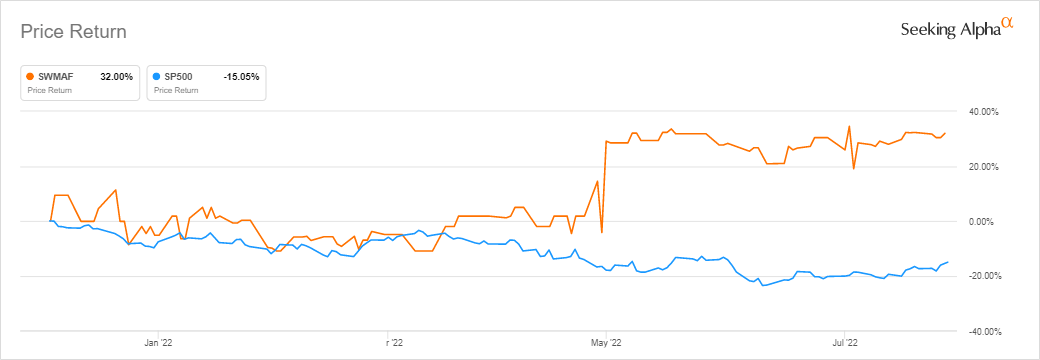

However, we have been making up quite a bit of those losses more recently. This was both experienced in GDV and S&P 500. Over the last month, they have performed quite similarly. So while we are looking at a nearly 12% discount, some of the overall declines have reversed more recently.

GDV And SP500 1 Month Returns (Seeking Alpha)

{kind=link}

The Basics

- 1-Year Z-score: -0.59

- Discount: -11.82%

- Distribution Yield: 6.10%

- Expense Ratio: 1.30%

- Leverage: 14.34%

- Managed Assets: $2.452 billion

- Structure: Perpetual

GDV is described as "a diversified, closed-end management investment company whose objective is to provide a high level of total return." Their investment policy is "under normal market conditions, the Fund invests at least 80% of its assets in dividend-paying or other income-producing securities. In addition, under normal market conditions, at least 50% of the Fund's assets will consist of dividend-paying equity securities."

Overall, they are pretty free to invest how they see fit with a tilt towards owning a fairly substantial dividend-paying stock weighting. That would generally help fund the distribution. However, the preferred dividends take a large portion of the fund's net investment income.

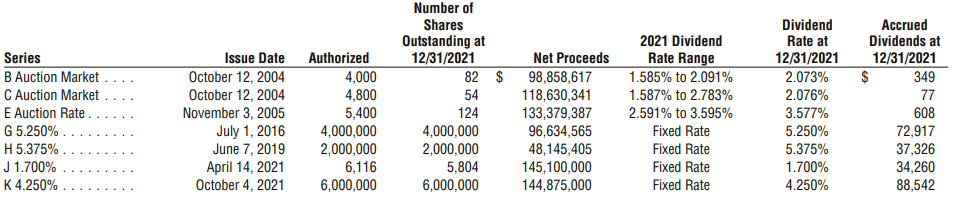

Here's the latest outstanding preferred that they have. They had redeemed their Series G Cumulative Preferred at the beginning of this year. While the dividends are higher on these preferred, they also benefit from being primarily fixed rates - an important distinction in a rising rate environment. That is except for the Series B, Series C and Series E preferred. Those are a small minority of the outstanding preferred. Overall, they are only moderately leveraged.

GDV Capital Structure (Gabelli)

Below is a look at dividend rates through 2021 from their previous annual report . (The series G is shown here but has since been redeemed, as mentioned above.) Series H is currently the highest yield but cannot be redeemed before June 10th, 2024.

{kind=link}

Performance - Discount Drifting Wider

In our previous article, the discount was around 10.5%. This has now widened out just a bit further. We even saw an over 13% discount on the fund recently for a short period. That discount has been moving in the other direction, along with the stronger rebound in the market over the last month.

In the last five years, the fund has averaged a discount of 9.64%. Below, we can see that significantly wider discounts have been relatively short-lived. Of course, shallower discounts are also relatively short-lived.

GDV Premium/Discount History (CEFConnect)

For me, that means it is quite attractively priced. Combining that with the markets still being lower overall, I believe that's why GDV is more compelling at this time.

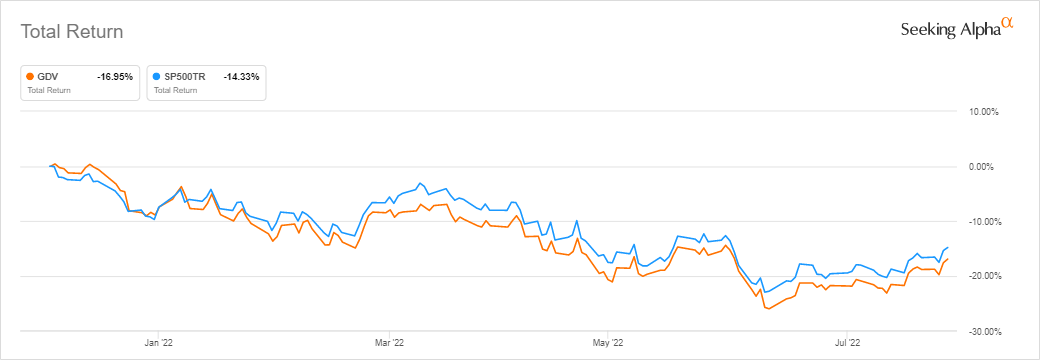

Here's the YTD total return chart. I've also included the S&P 500 Index to provide some context. GDV isn't invested similarly to the S&P 500 in that they aren't as heavily invested in tech.

GDV and SP500 Returns (Seeking Alpha)

{kind=link}

At the end of June 2022, CEFConnect showed the total NAV return at -19.42% compared to the -22.10% on a total share price basis. That just goes to show how much we have recovered over the course of July.

Distribution - Attractive 6.10% Yield

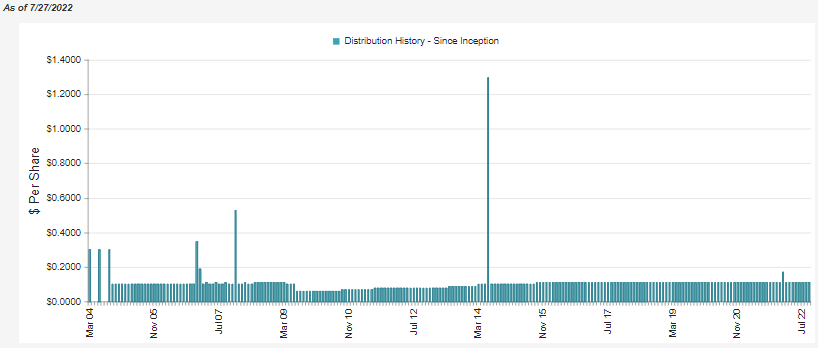

GDV has provided a relatively attractive and stable distribution to shareholders. They pay monthly and have been paying out $0.10 per month, going back to around 2015. They only show two distribution cuts, both of which were in the great financial crisis. That's a period where I would criticize and look past such a blemish.

GDV Distribution History (CEFConnect)

{kind=link}

The fund had paid a small year-end distribution last year to comply with its regulated investment company structure distribution requirements . That requires the fund to pay almost all of its realized earnings (income and gains) or pay an excise tax.

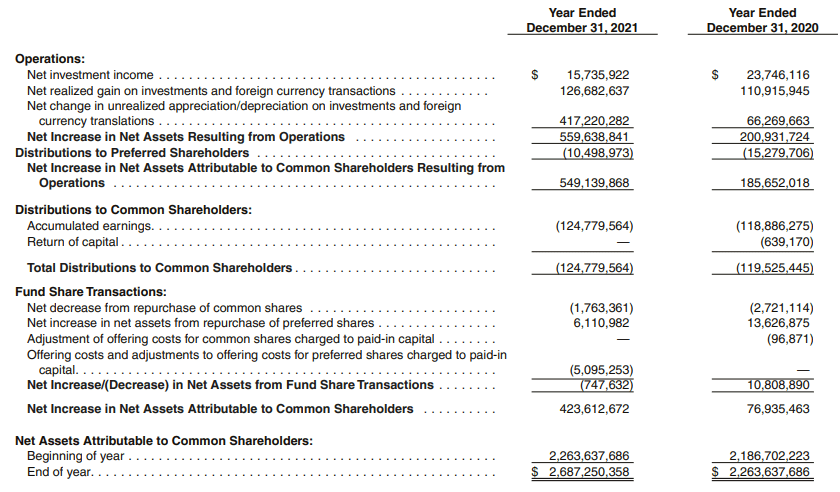

To fund its distribution, the fund will require capital gains. That can be tougher to come by in a bear market that we have been experiencing in 2022. Still, there are ways that they can generate capital gains. That can be through built-in unrealized gains in the underlying fund and turning them into realized. Entering this year, the fund had an unrealized appreciation of $1.35 million.

We also have to consider that even if most investments are down, they can still have rising positions. Even in 2022, not every single investment is down - just most! Swedish Match ( OTCPK:SWMAF ) is such a position that we'll touch on below.

{kind=link}

As I mentioned above, the preferred dividends are quite an expensive way to leverage the fund. That has pushed GDV to require even more capital gains to fund both the common and preferred distributions. Some of these distributions to preferred will be lower now that the Series G has been redeemed. That being said, it will certainly remain a sizeable portion being pulled away from common shareholders' cut of the income.

After factoring out the preferred, we are looking at just over $5 million NII for common shareholders. That's against the nearly $125 million the fund pays out annually.

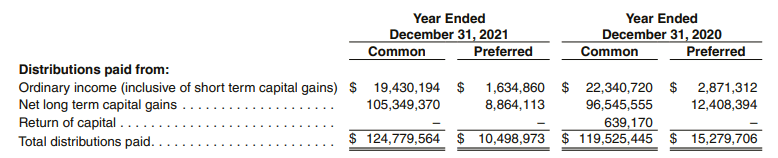

We see primarily long-term capital gains in the distribution characterization for tax purposes. This is to be expected. The smaller portion that is identified as ordinary income is generally going to be considered qualified dividends too.

GDV Tax Character (Gabelli) From my own 1099, GDV's ordinary dividends were 100% classified as qualified dividends for the last year.

{kind=link}

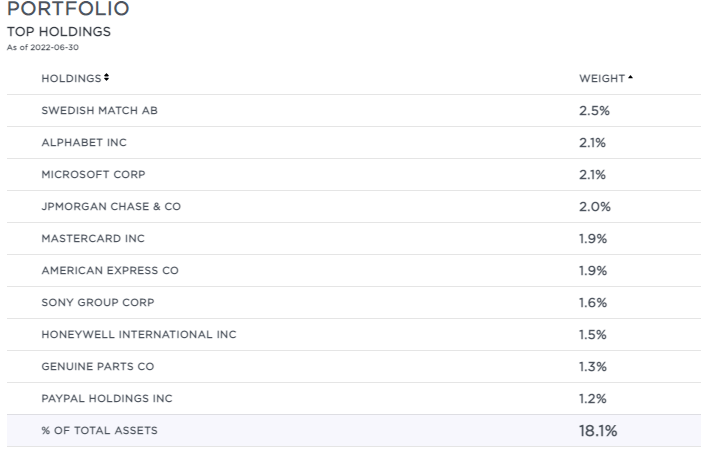

GDV's Portfolio

One of the more interesting positions in the fund's portfolio has been SWMAF. While I never really understood why it was such a sizeable position. What would a Swedish tobacco company focusing mostly on smokefree tobacco be doing in a dividend portfolio? Gabelli even includes the position in his utility funds. (The largest position in the Gabelli Global Utility & Income Fund ( GLU ) is also SWMAF.)

Swedish Match Sales Split (Swedish Match)

Well, apparently, Mr. Gabelli knew what he was doing. The stock got a bid from Philip Morris ( PM ) to be acquired. This saw the stock pop and hold an elevated level.

{kind=link}

However, this acquisition isn't set in stone yet. Activist management group Elliot is looking to oppose the sale. They have raised their stake in the company to have more control to fight this. It seems this isn't the only group with some grumblings on this deal. This could ultimately lead to an even better deal for shareholders with a higher price or work the other way and push any buyer away.

Whatever the ultimate outcome is in the end, this just helps provide one example of a position that can still produce gains. Those are the types of gains that can be trimmed to go towards the distribution to shareholders in GDV.

{kind=link}

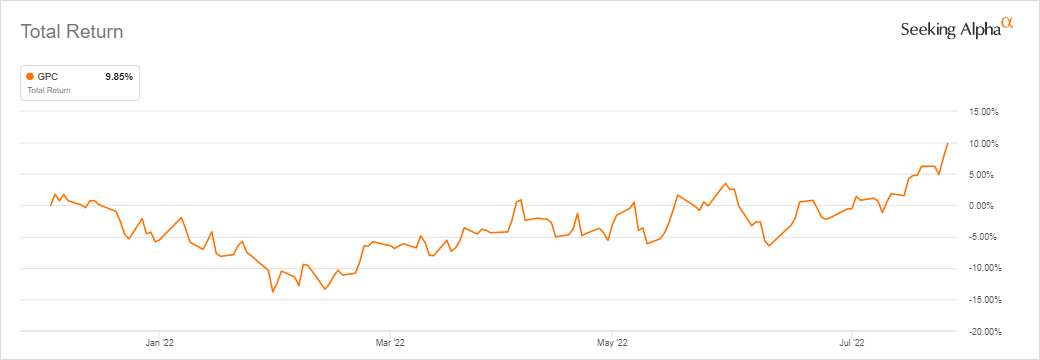

That isn't the only top position that has shown gains for the year, either. Genuine Parts ( GPC ) shares are also higher this year. Another oddball position that I certainly wouldn't have come across my radar.

{kind=link}

GPC released their earnings recently , which showed a beat on both the top and bottom line. They had also boosted their guidance on top of this too. Shares were already higher for the year, but this propelled the stock even further. This company provides automotive and various other vehicle parts, including recreational vehicles and farm and marine equipment.

Overall, GDV's portfolio is tilted towards more value-oriented sectors rather than growth. Financial, healthcare and food & beverage industries represent the highest weighting in this fund. I believe this makes it relatively more attractive and a way to diversify away from more tech-heavy funds.

Conclusion

GDV remains an attractive deal for investors. The discount has even slightly widened since our last update. At that time, it was already at a slightly larger long-term discount. The market has been rebounding over the last month quite aggressively. That being said, it is still lower, which adds to the fund's discount being attractive. I believe that the fund is a buy at this time for a long-term investor looking to vary their portfolio away from the more usual positioning in other diversified funds.

For further details see:

GDV: Attractively Discounted And A ~6% Distribution Yield