SWMAY - GDV: Steady Distribution Rate And Discounted

2023-04-08 02:58:38 ET

Summary

- GDV is a fairly plain equity fund investing in value-oriented sectors.

- Its financial exposure is primarily tilted toward large banks and institutions; however, it also carries some exposure to regional banks.

- The fund continues to trade at a wide discount and carries a reasonable distribution yield that should be maintained in the current environment.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on March 24th, 2023.

The Gabelli Dividend & Income Trust ( GDV ) isn't one of the more exciting closed-end funds with a highly complex strategy that they implement. For the most part, it's a fairly straightforward equity fund that utilizes a mild amount of leverage. The fund continues to trade at a large discount. While I don't suspect that to end anytime soon, we are near the lowest levels this fund has shown historically.

The portfolio is tilted towards value-oriented sectors. The value-oriented sector does include financial exposure, primarily from the largest banks and financial institutions, but there is some exposure to a few regional banks as well. Of course, the regional bank space has been getting most of the headlines lately due to bank failures and continued worried there could be more. Thanks to being highly diversified, this isn't having any outsized negative impact on the fund. CEFConnect puts the number of holdings at over 500.

Since our last update , shares have declined. In this case, even further than the S&P 500 Index. While that might not be a directly appropriate benchmark due to positioning differences, it can be a go-to comparison metric for equity funds. Since our last update, the discount was actually right about this same level. In this case, it would appear my poor timing in providing an update was the culprit, as it appears it was near a peak.

GDV Performance Since Prior Update (Seeking Alpha)

In fact, both of the last two updates that I labeled as a "buy" resulted in postings near a peak. This time looks different with a trough in the chart. Of course, only time will tell, and I'm not so concerned about short-term volatility. I view this as a longer-term holding for myself.

The Basics

- 1-Year Z-score: -1.19

- Discount: -14.24%

- Distribution Yield: 6.60%

- Expense Ratio: 1.17%

- Leverage: 14.17%

- Managed Assets: $2.449 billion

- Structure: Perpetual

GDV is described as "a diversified, closed-end management investment company whose objective is to provide a high level of total return." Their investment policy is "under normal market conditions, the Fund invests at least 80% of its assets in dividend-paying or other income-producing securities. In addition, under normal market conditions, at least 50% of the Fund's assets will consist of dividend-paying equity securities."

The fund is fairly flexible to invest where it sees fit, with an overemphasis on dividend-paying securities. However, that's a fairly broad category, as most established and larger companies pay out some sort of dividend to investors.

The fund's expense ratio isn't overly high relative to other CEFs. However, with a basic investing approach could be considered on the higher end. When including leverage, the fund's expense ratio goes up to 1.35%. One of the benefits of GDV - at least in the rate hiking cycle phase we are in - is that most of their leverage comes from fixed-rate preferred. A minority of the leverage provided is through an auction market/rate-preferred form of leverage.

GDV Capital Structure (Gabelli)

Additionally, GDV's debt isn't significant when most CEFs are leveraged at around 30%. In that regard, GDV's leverage could be considered mild. When using leverage, there will always be a greater risk of volatility as downside moves are amplified (as well as positive as upside moves are also amplified.)

Performance - Attractive Discount

In 2022, the broader market indexes had struggled, but GDV outperformed by a touch on a total NAV return basis. Interestingly, despite the fund's more value-oriented portfolio, the fund's performance through most of 2022 was pretty well correlated with ( SPY ).

Ycharts

Over the longer term, it had been more of a detriment. As the fund has less of an overweight to tech that SPY carries with it, it meant weaker longer-term results. Their last fact sheet provided a table showing their performance relative to the S&P 500 Index and the Dow Jones Industrial Average. Besides positioning, the fund's expense ratio would have dragged results.

{kind=link}

Based on what we know now, I would have originally suspected GDV to perform even better in 2022, so this is a bit disappointing. However, as a primary income play and a fund that's trading at a decent discount, that's where GDV can shine. The fund has carried a wide discount for a significant period of time.

I don't expect that to reverse any time soon. That being said, besides a quick spike in 2020, we are near the deepest discount levels for this fund. That could mean there is some downside already priced in, and a further deepening of a discount is possible, but it could be short-lived.

Ycharts

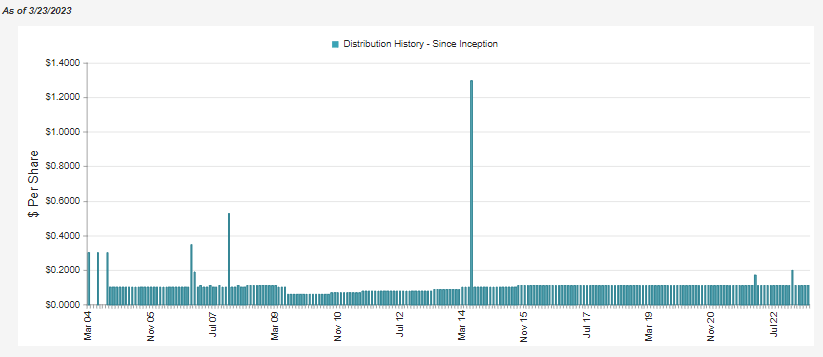

Distribution - Steady

The fund has been a reliable payer. They cut in the GFC but so did a lot of other CEFs and even companies. I won't hold any distribution cuts in 2008 or 2020 against a fund. They raised after that to the point where it was in line with the $0.11 per month it had pre-GFC. They achieved that level in 2015 but have maintained the same level since.

{kind=link}

One of the reasons it's been so steady and reliable is simply because it is a lower yielder in the realm of CEFs. Honestly, that's one of the main reasons it trades at such a large discount. In this case, the fund's NAV rate is 5.66%. Thanks to the large discount, the distribution yield for investors comes to 6.60%, so a bit more appealing.

That being said, it's still like any other equity CEF. They will rely significantly on capital gains to fund their distribution. For GDV, their net investment income coverage was 13.70%.

{kind=link}

Since they paid a year-end of $0.09, the actual coverage for the regular distribution would have been a bit higher. The regular distribution based on the number of shares outstanding at the end of 2022 would mean $119,048,808 to be paid out to investors. In that case, the regular NII distribution coverage would be 14.64%.

Not an overly large jump when factoring out the year-end special. Significant capital gains will still need to be realized on the fund. So over time, if years go by without some appreciation and sizeable unrealized losses continue, then in that case, a distribution cut could take place. For now, it still seems that the distribution is reasonable.

For tax purposes, we have another benefit of GDV. With most of the distribution for common shareholders regularly long-term capital gains, they are generally more tax-favorable for investors. Additionally, in 2022 , they noted that 100% of the ordinary income was classified as qualified dividends.

{kind=link}

This would mean the distributions would have been taxed at 0 to 20% for investors.

GDV's Portfolio

GDV's portfolio isn't only boring equity investments but also boring in that there aren't too many changes year-to-year. The turnover rate for the fund last year was 10%. In the last five years, the high water mark was 16% turnover in both 2020 and 2019. Despite the fairly low turnover, the fund still has 13 portfolio managers listed.

With that being said, as expected, their portfolio doesn't change very dramatically between updates. The fund consistently carries financial services as the largest sector exposure. This is then followed by healthcare and then food & beverage categories.

This is almost the same exact order we saw previously. Except in this case, energy & utilities have now made their way as the fifth largest sector weighting. That crowded out consumer products that previously showed. This positioning is as of their latest fact sheet, which was for the period ending December 31st, 2022.

GDV Sector Allocation (Gabelli)

Swedish Match had formerly been a regular position in the portfolio at the highest allocation.

GDV Top Ten Holdings (Gabelli)

Those that followed this name will know that Philip Morris ( PM ) had acquired nearly all of the company . That being said, it would appear that the remaining Swedish Match shares continue to trade under ( OTC:SWMAY ). A new name to make the top ten is Deere & Co ( DE ) to replace the removal of Swedish Match from the top holding spot.

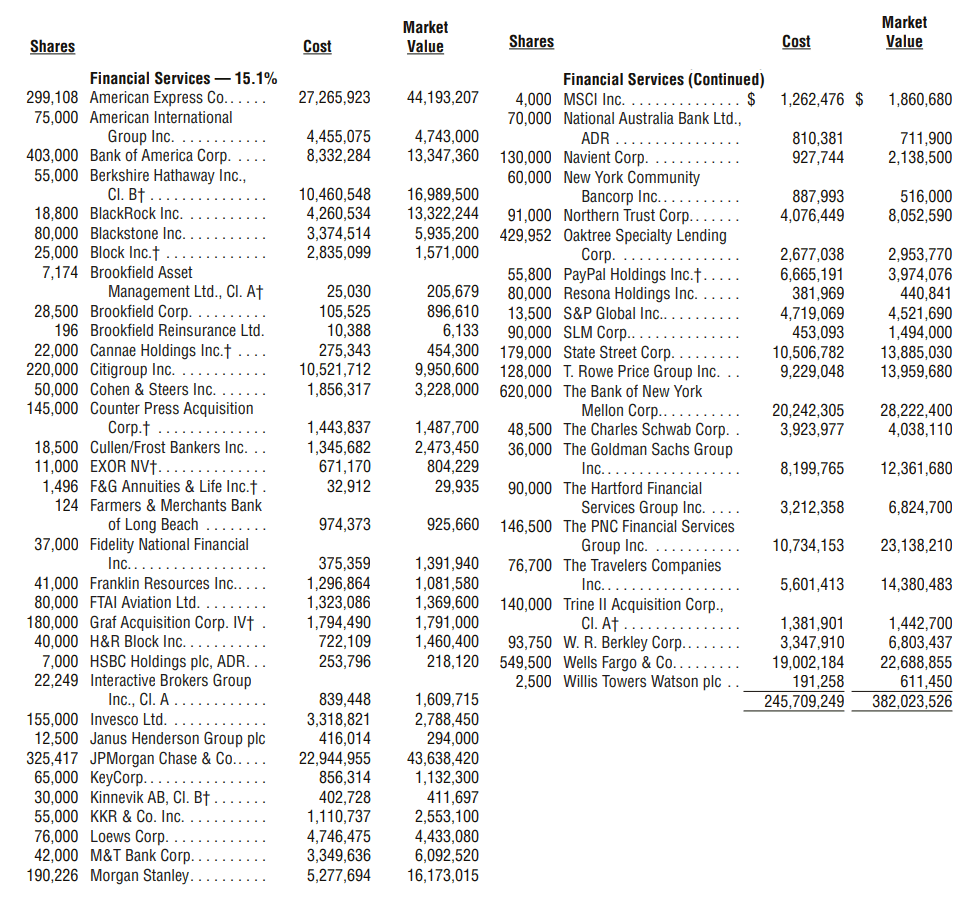

In the top ten, we also have JPMorgan ( JPM ); with a mini-banking crisis unfolding, it's good to see such a solid name in the top ten. However, as noted above, the financial services sector makes up around 15% of the fund. Some of those names aren't the largest names, with a couple of regional banks.

Fortunately, the portfolio is positioned in around 55 different financial services positions. Those include some of the largest banks, but it also includes asset managers, insurance companies and payment processors. So the actual regional bank exposure here is going to be fairly limited. Additionally, this list was as of the end of December 2022. At that time, they didn't carry any exposure to the collapsed banks.

{kind=link}

Conclusion

GDV is a fairly straightforward equity fund that utilizes a mild amount of leverage. The value-oriented portfolio has helped contribute to the results of underperformance relative to the S&P 500. So if you're looking for strong past performance or are looking for performance to start outperforming going forward, I don't necessarily feel that will happen. It isn't necessarily designed to try to beat SPY. On the other hand, they've provided a steady and reliable distribution to investors. With the fund's current discount being near the widest in its history, excluding the COVID crash, I feel it is still a compelling time to consider the fund.

For further details see:

GDV: Steady Distribution Rate And Discounted