RYLPF - GE HealthCare: Great Quarter Upside Remains

2023-11-01 08:49:40 ET

Summary

- GE HealthCare's Q3 2023 financial results showed a 5% increase in revenue and a 90 basis point increase in gross margin.

- The company raised the low end of its Adj EPS guidance for 2023.

- GE HealthCare is facing challenges in China but is still performing better than competitors in the region, gaining market share.

- We remain bullish on the stock and reaffirm our $130 price target in 3 years.

Investment Thesis

In our previous article , we discussed the bull thesis for GE HealthCare (GEHC). The conclusion was that as an independent company, GEHC would have more room to grow and increase its margins than under the umbrella of GE. Coupled with its reasonable valuation and industry tailwinds, we believed it was a compelling long.

Since then, the company reported Q3 financial results . The market reacted positively to the report, with a 5% increase in the stock price on that day. In this article, we are going to analyze its performance and see if the thesis is still on track. Spoiler alert: we remain bullish.

Q3 2023 Financial Results

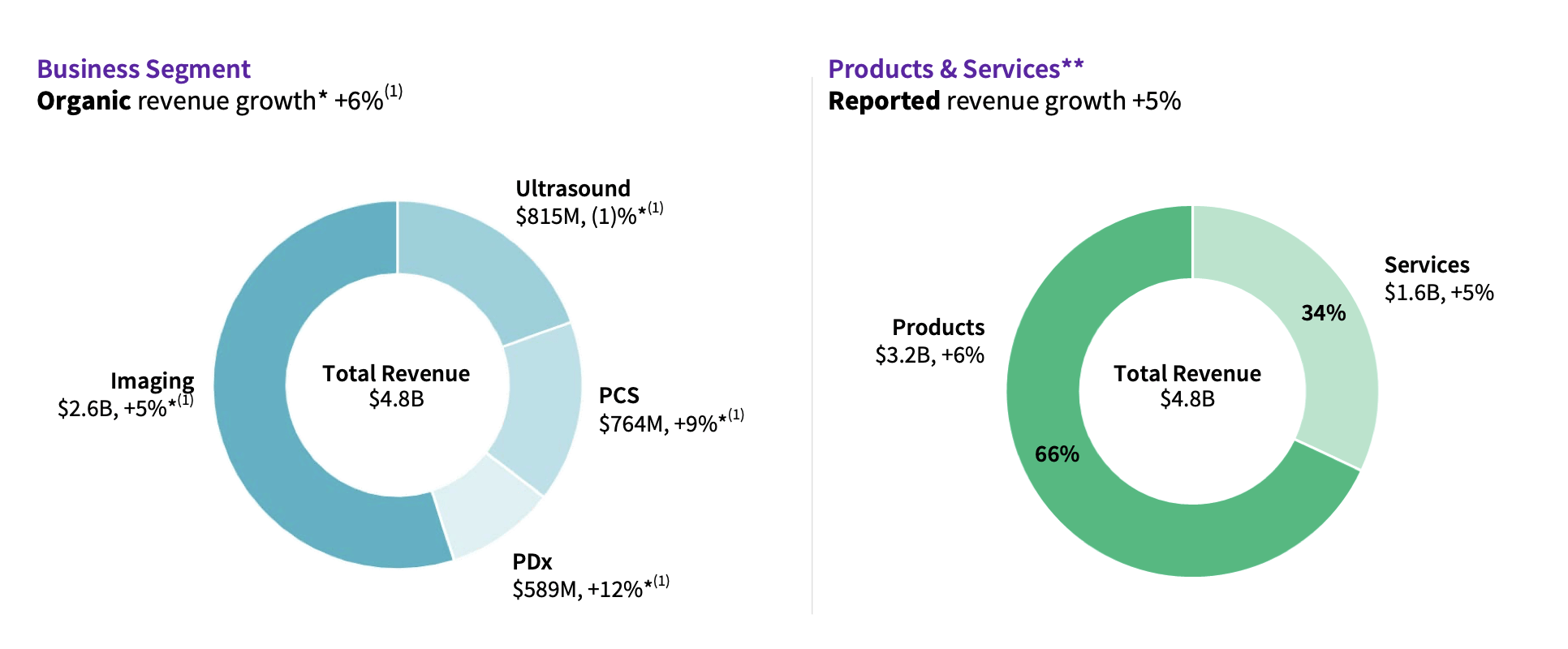

Revenue was $4.8 billion , a 5% increase reported and 6% on an organic basis YoY, driven by volume and price, and slightly ahead of street estimates. Management said that price was going to represent 2%-3% of growth in the full year, so the other half could be attributed to volume growth.

The ultrasound segment was the only one to post organic decline. In fairness, it faced a challenging comparison vs. Q3 2022 when it grew double-digit organically. On the other hand, the fastest-growing segment was the pharmaceutical diagnostics segment, which increased 12% YoY organically.

{kind=link}

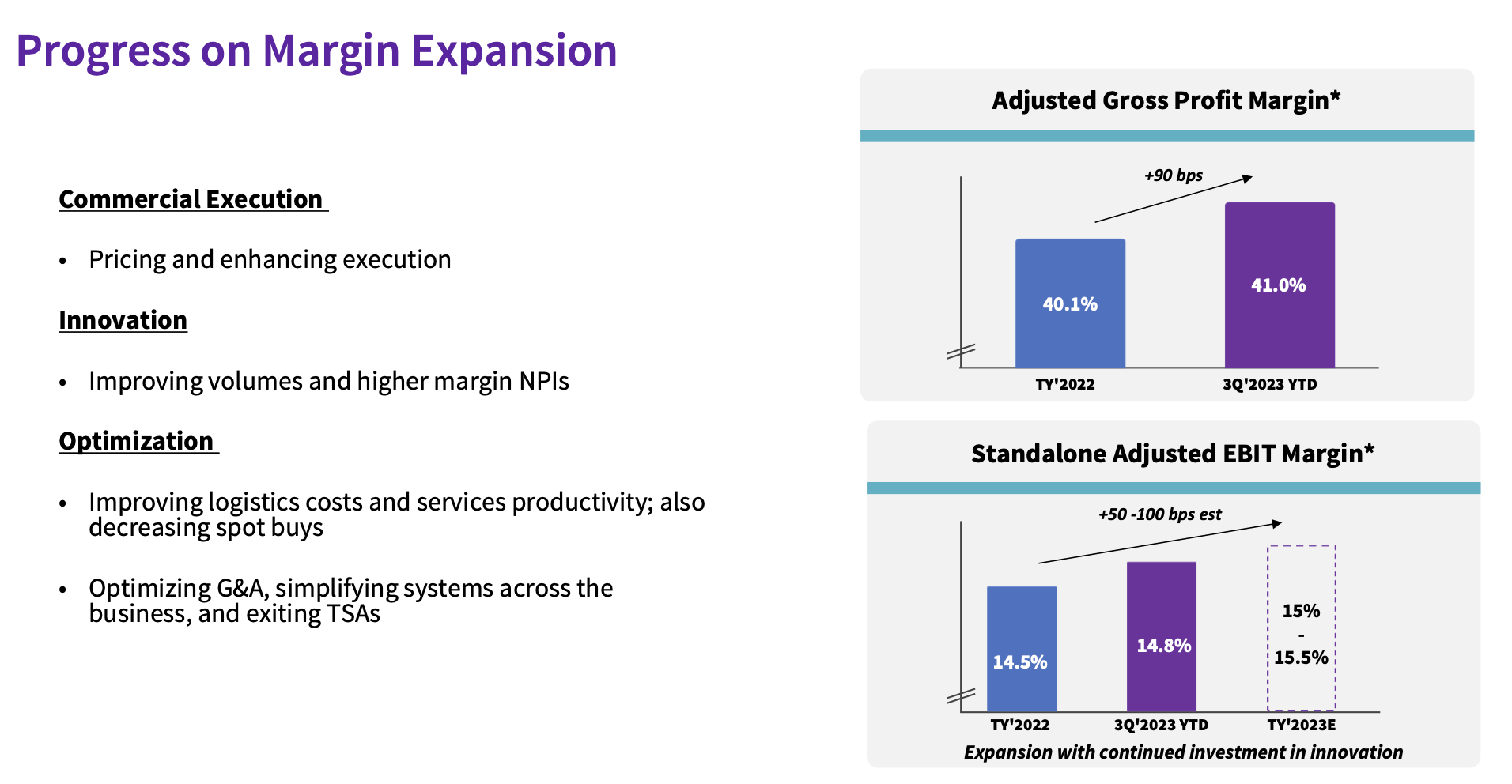

The gross margin increased by 90 basis points compared to FY 2022, and the adjusted operating margin is expected to exceed 15% for 2023. The efforts to improve logistics and optimize costs seem to be yielding results. Remember that management targets a 20% operating margin in the long run.

{kind=link}

Finally, net income was $375 million for the quarter, or $0.83 per share. The company generated $570 million of free cash flow in the quarter, $22 million more than a year ago while absorbing standalone interest and incremental post-retirement benefit payments. Inventory levels also help as they improve YoY as they leverage lean to improve lead times and drive faster inventory turns.

Something we would have liked to see was an indication of what they will start doing with the cash generation. They are making huge profits, but there is no buyback plan or investment projects announced, and the dividend they pay is laughable ($0.03 per share per quarter).

The company has $2.4 billion in cash and equivalent and $10.2 billion in long-term financial debt. As a result, net debt is $7.8 billion. The net leverage ratio (Net Debt/EBITDA) is 2.3x (we assumed an EBITDA of $3.3 billion in 2023). With the cash the company is generating, the debt situation shouldn't be a problem.

Guidance

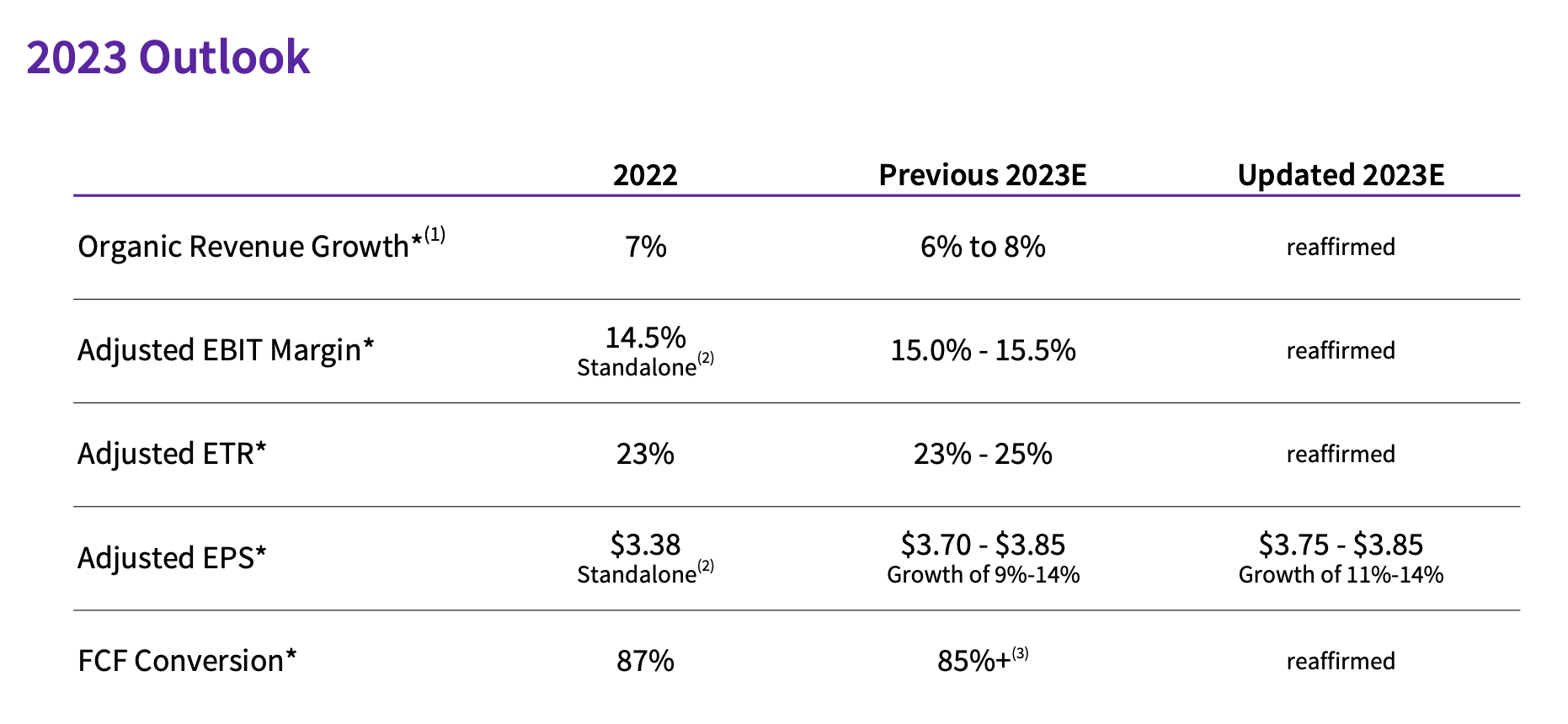

GEHC only raised the low end of its Adj EPS guidance for 2023 to $3.75-$3.85 from $3.70-$3.85. This has to do with a favorable FX impact in Q3 and a lighter impact projected for Q4.

{kind=link}

China Problems?

During the quarter, China launched a sweeping anti-corruption campaign targeting its hospitals, pharmaceutical industry, and insurance funds as it grapples with mounting economic challenges and long-standing public frustration about high costs in the behemoth healthcare sector.

In one case, the president of a small hospital in southwestern Yunnan province is alleged to have illicitly obtained over $2.2 million during the purchase of a medical device for cancer treatment in a 2021 incident that has recently been brought to the forefront by anti-graft officials.

In line with this, the company disclosed for the first time that beginning 2018 they self-disclosed to the SEC and DOJ "tender irregularities and other potential violations" of the Foreign Corrupt Practices Act related to its activities in some Chinese provinces. GEHC also said it wasn't able to predict what, if any, action the regulators may take or penalties they may impose.

China region revenues were $719 million, growing 8% or $51 million due to growth in Imaging revenues, partially offset by unfavorable foreign currency impacts. This comes as a surprise as competitors Philips (PHG) and United Imaging saw very meaningful declines in China revenue during Q3, signaling that GEHC may be taking market share or simply weathering the storm better. Going into Q4, management are more optimistic that in Q3 and expect this trend of growth to continue. It will important to keep an eye on this.

Takeaway

Since our last article the valuation actually compressed slightly. The stock currently trades at 12.7x EV/EBIT and 16.6x P/E (forward measures). For comparison, Phillips trades at 12.5x EV/EBIT and 15.1x P/E. We believe that as the market stops seeing the company as the spinoff of GE (GE) and instead views it as a growing, profitable independent company gaining market share and generating a significant amount of cash flow for dividends and buybacks, the multiples will expand. As such, we reaffirm our target of $130 in 3 years, which translates into a ~25% CAGR from current prices.

For further details see:

GE HealthCare: Great Quarter, Upside Remains