SEMHF - GE Healthcare Technologies: The Dip Offers A Renewed Buying Opportunity

2023-04-27 17:49:55 ET

Summary

- GE Healthcare Technologies faced some pressure despite posting attractive financial results for the latest quarter.

- Overall, the company looks to be in solid shape and its future looks bright, especially with recent new wins under its belt.

- Add on top of this how cheap shares are compared to similar firms, and the company definitely deserves optimism.

Sometimes, no matter how hard you try, you just can't please someone. That's likely how shareholders and the management team at GE Healthcare Technologies ( GEHC ) feel at this moment. After the company announced financial results covering the first quarter of its 2023 fiscal year, shares of the enterprise plunged, closing down about 8.4% for the day. This was met by another slight decrease that followed the broader market down on April 26. Given this kind of performance, you would expect the company to be disappointing investors on its top line, its bottom line, or both. But the fact of the matter is that management came out with some very impressive results. Add on top of this just how affordable shares are compared to similar firms, and I do believe that this could represent a good buying opportunity for long-term, value-oriented investors. Because of this, I have no choice but to keep the 'strong buy' rating I had on the stock previously.

A stellar quarter

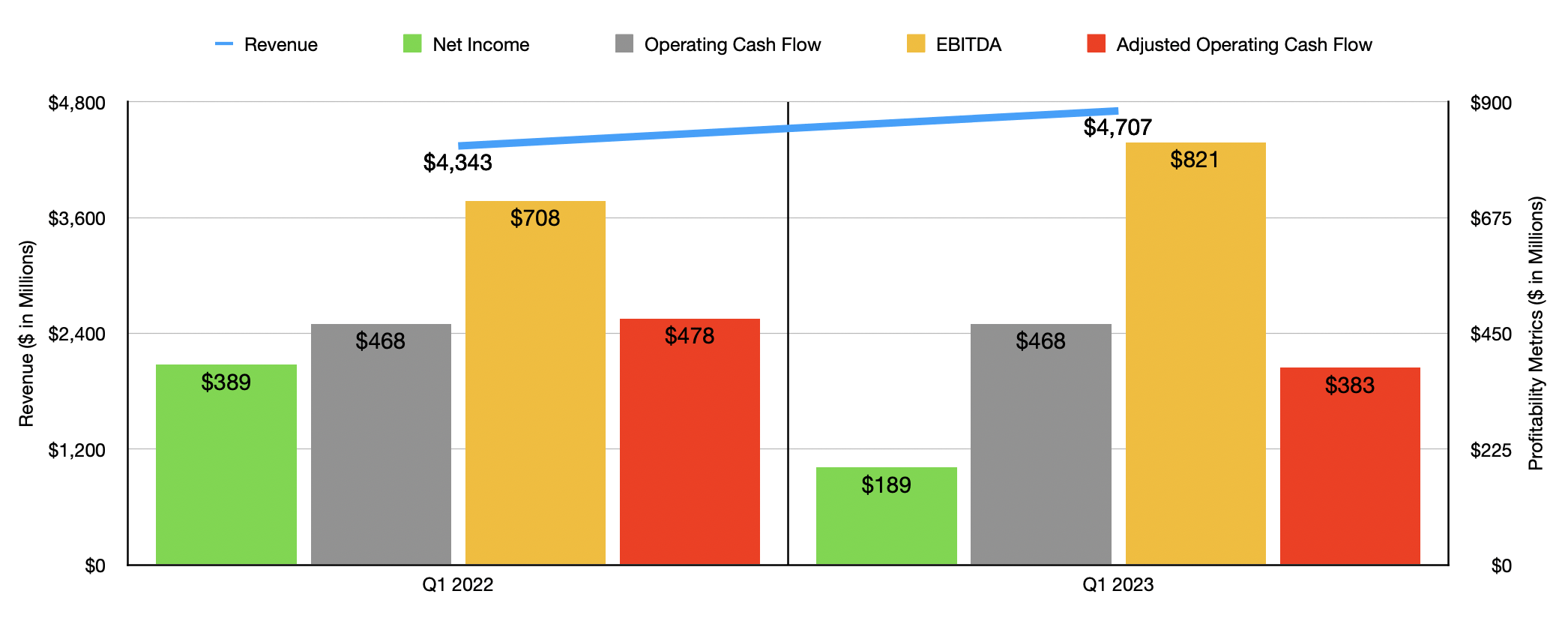

April 25 proved to be a rather difficult day for shareholders of GE Healthcare Technologies. After the company announced financial results for the first quarter of its 2023 fiscal year, shares of the enterprise plunged. This was the largest single-day drop in the company's admittedly short history. This comes in spite of the fact that the business outperformed expectations on both its top and bottom lines. Consider, for instance, the revenue the company reported. Sales for the quarter came in at $4.71 billion. That's 8.4% higher than the $4.34 billion reported one year earlier. It also was $80 million higher than what analysts anticipated.

{kind=link}

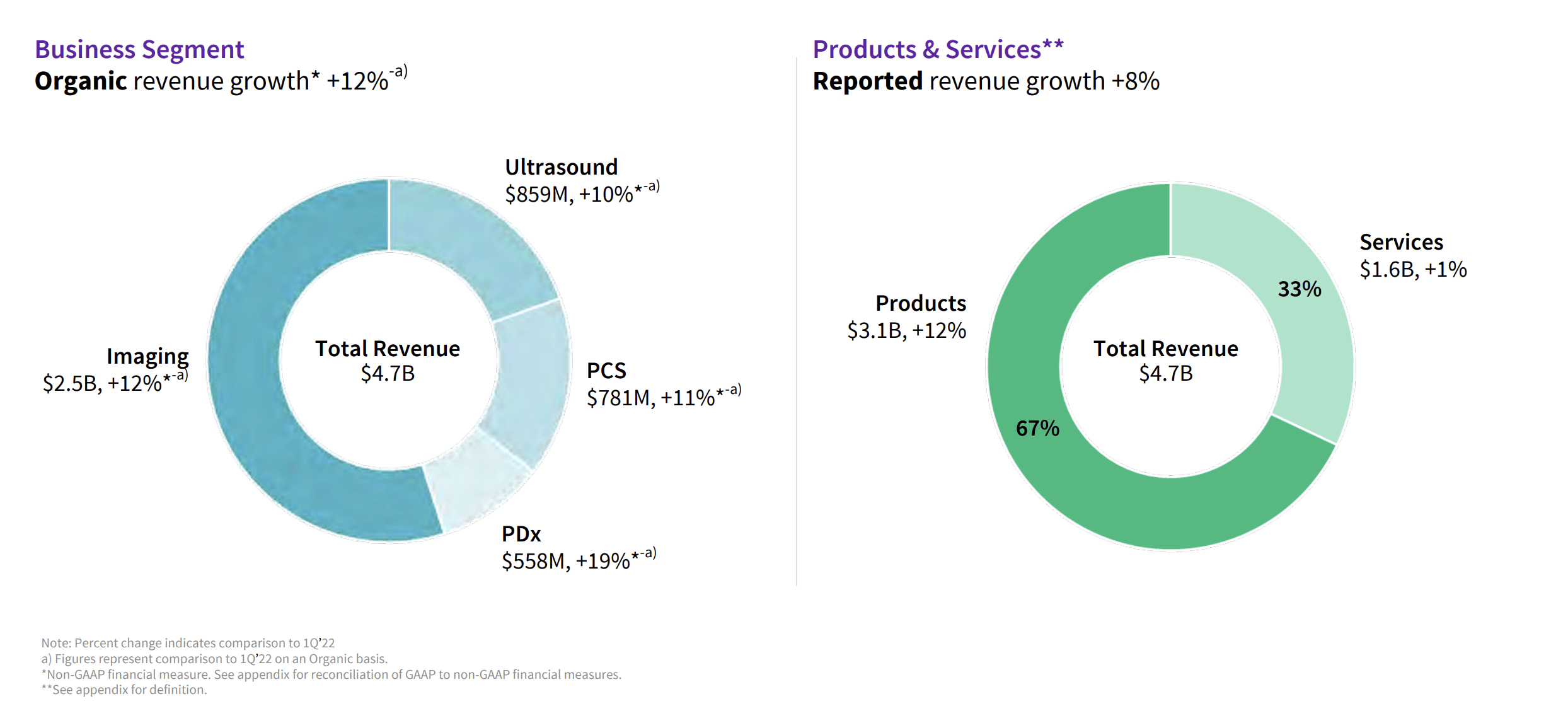

Interestingly, revenue growth would have been even more impressive had it not been for foreign currency fluctuations. Organic revenue actually jumped around 12% year over year. Although the company reported strength across the board, the most significant improvement came from its Pharmaceutical Diagnostics segment. Revenue there spiked 15%, or 19% on an organic basis, thanks to a combination of higher prices charged for its products and an increase in the volume of products shipped. The second-fastest growth came from the massive Imaging segment, with revenue up 8% and organic revenue up 12%. Management attributed this upside to multiple factors, including its MRI operations, its Molecular Imaging and Computed Tomography operations, new product introductions, and supply chain improvements that resulted in a greater ability for the company to deliver on robust demand.

{kind=link}

On the bottom line, the picture was in some ways disappointing. The company saw its earnings per share drop from $0.86 in the first quarter of 2022 to $0.41 the same time this year. This brought net income down from $389 million to $189 million. This was largely driven by a $183 million hit associated with a deemed preferred stock dividend of redeemable non-controlling interests. But even excluding that, a rise in interest expense, as well as higher core costs like research and development expenditures, negatively impacted the company's bottom line. Despite this pain, the company did beat analysts' expectations by $0.06 on an adjusted basis, with adjusted earnings per share of $0.85. Fortunately, some of the cash flow data provided by management was fairly strong. Operating cash flow remained flat year over year at $468 million. If we adjust for changes in working capital, however, we would have seen the number drop from $478 million to $383 million. On the other hand, EBITDA for the company rose from $708 million to $821 million.

Moving away from the financial metrics for a moment, it's important for investors to understand that the company has had some interesting wins under its belt. For instance, in early March, the company announced a multi-year agreement to help expand access to provide its Healthcare Technology Management services to the clients of Advantus Health Partners in a deal valued at $760 million over 10 years. There are many other developments that I could point to. But perhaps the most significant one came in early February when the company announced that it was acquiring Caption Health, an artificial intelligence healthcare company that develops clinical applications that help in early disease detection by using artificial intelligence to assist in conducting ultrasound scans. Although terms were not discussed, it's important to note that the ultrasound business under GE Healthcare Technologies is quite large, with annual revenue of around $3 billion.

{kind=link}

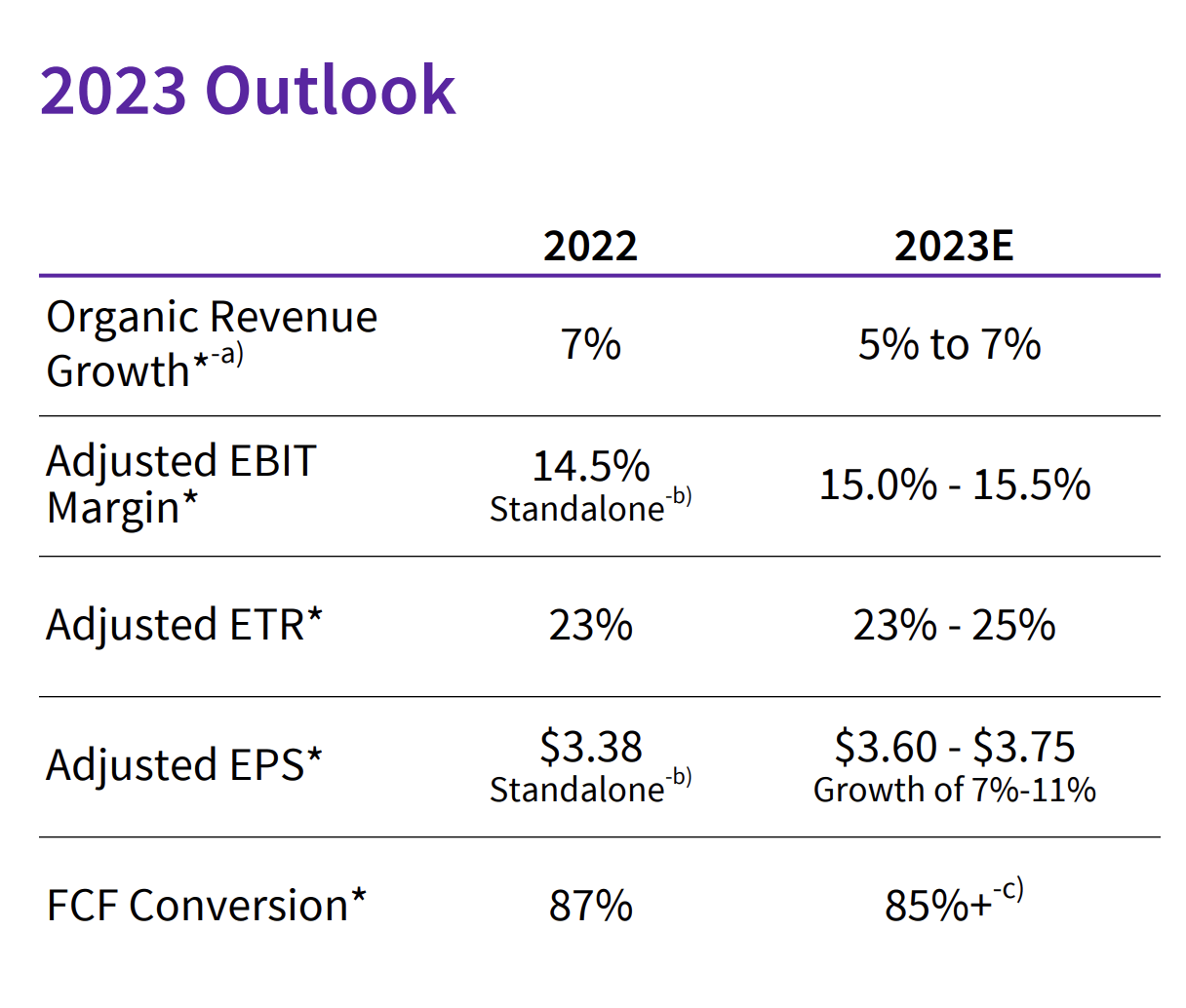

Management has provided some guidance when it comes to the 2023 fiscal year. For instance, they anticipate organic revenue growth of between 5% and 7%. Earnings per share are forecasted to rise by between 7% and 11%, coming in at between $3.60 and $3.75. That would stack up nicely against the $3.38 per share reported for the 2022 fiscal year. If this comes to fruition, it would translate to net income of roughly $1.68 billion on an adjusted basis. Management is also forecasting an improvement in its EBIT margin. At the midpoint, and factoring in the organic revenue growth, we should get an EBITDA of roughly $3.59 billion for 2023. That would be up slightly from the $3.49 billion reported in 2022. If we assume that adjusted operating cash flow should rise at the same rate, then we would anticipate a reading for the year of $2.46 billion.

{kind=link}

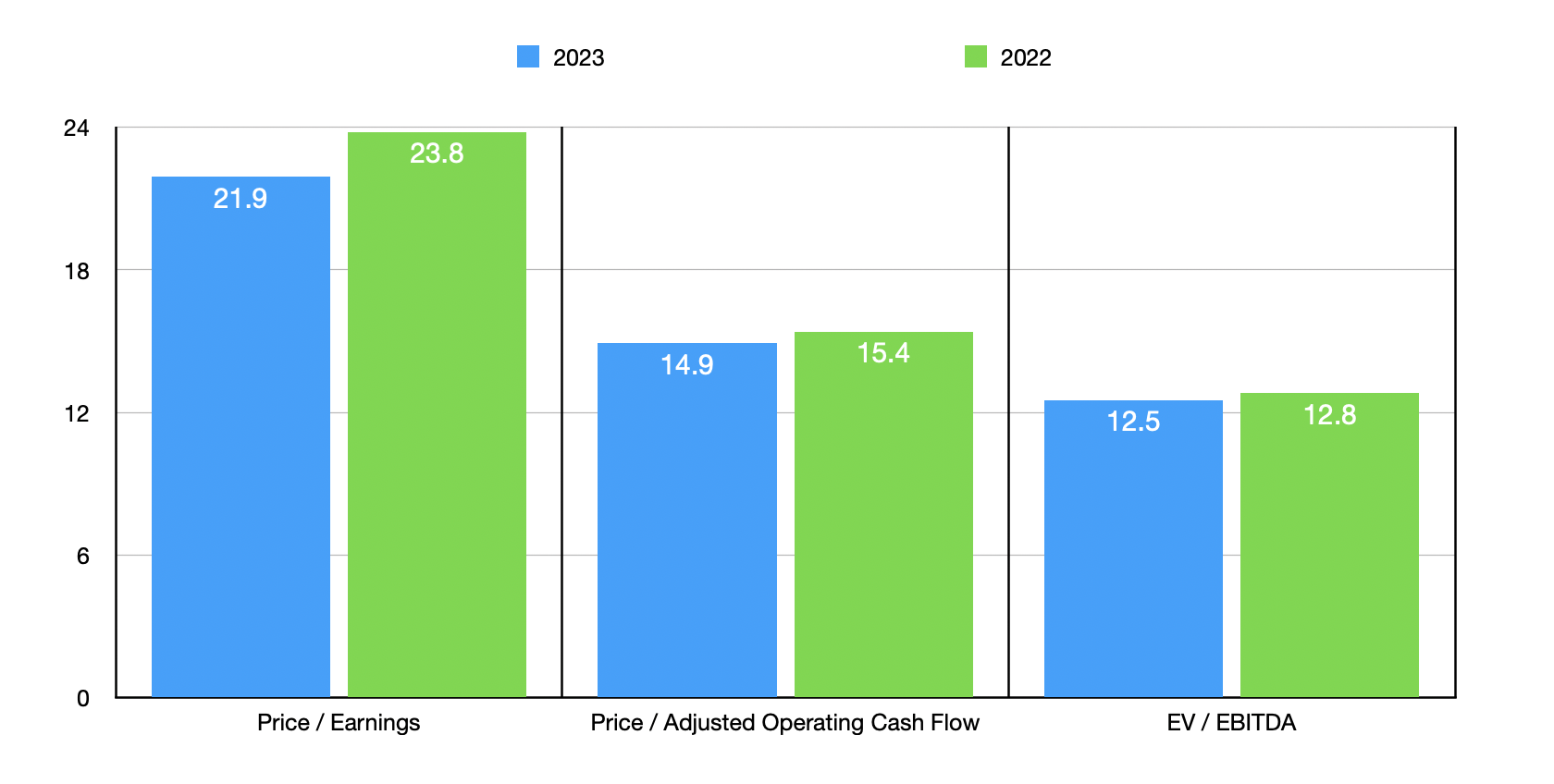

Based on these figures, the company is trading at a forward price-to-earnings multiple of 21.9. That would stack up against the 23.8 reading that we get using data from 2022. The price to adjusted operating cash flow multiple, as well as the EV to EBITDA multiple would also improve from 2022 to 2023. This can be seen in the chart above. In the table below, you can see how the company stacks up against six similar firms using each of these valuation metrics, with data drawn from the 2022 fiscal year. Our prospect ends up being the cheapest of the group across the board.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| GE Healthcare Technologies |

| 23.8 |

| 15.4 |

| 12.8 |

| Danaher ( DHR ) |

| 24.1 |

| 20.1 |

| 18.7 |

| Thermo Fisher Scientific ( TMO ) |

| 31.1 |

| 23.6 |

| 20.7 |

| Agilent Technologies ( A ) |

| 29.4 |

| 28.8 |

| 21.5 |

| Illumina ( ILMN ) |

| 40.5 |

| 87.8 |

| 79.8 |

| Mettler-Toledo International ( MTD ) |

| 38.2 |

| 38.9 |

| 29.6 |

| Siemens Healthineers AG ( SMMNY ) |

| 33.3 |

| 34.7 |

| 16.1 |

Taking my analysis a step further, I wanted to see what kind of upside potential might exist for shareholders. To do this, I looked at two different scenarios for each of the multiples that I valued the company with. In the first scenario, I looked at what kind of upside would exist if GE Healthcare Technologies were to trade at the multiple of its cheapest rival. And in the second scenario, I stripped out the most expensive peer, averaged out the trading multiples of the other five, and calculated what kind of upside potential, if any, GE Healthcare Technologies would warrant if it were to trade at said multiple. Although the price-to-earnings approach implies a fairly limited upside. The cash flow and EBITDA approaches imply an upside of between 30.5% and 89.6%.

{kind=link}

Takeaway

Based on the data provided, I must say that I remain encouraged by GE Healthcare Technologies. I believe, at this point, that the company remains attractively undervalued, even though significant upside has already been captured. The fairly attractive results experienced for the first quarter of the 2023 fiscal year further bolstered this belief. Given these developments, I feel comfortable keeping the company rated a 'strong buy' for now.

For further details see:

GE Healthcare Technologies: The Dip Offers A Renewed Buying Opportunity