SEMHF - GE Healthcare: Unveiling Red Flags In Its Growth Story

2023-12-02 04:08:02 ET

Summary

- GE Healthcare Technologies Inc. faces significant competition and market share losses, leading to an undeserved premium and overly ambitious financial targets.

- GE Healthcare's Imaging segment struggles to maintain market share, while the Ultrasound market sees increased competition and pricing pressures. However, the Patient Monitoring and Pharmaceutical Diagnostics segments offer brighter prospects.

- Looking ahead, management's ambitious growth and margin expansion targets may face headwinds, considering the industry dynamics, competition, and the need for increased R&D spending.

- While shorting is not explicitly suggested, caution is advised, as the company's growth outlook, competitive positioning, and stock valuation may not align with investors' expectations over the next two years.

Investment thesis

I initiate my coverage of GE HealthCare Technologies Inc. ( GEHC ) and rate shares a “Sell/Avoid” as I see no upside for the next 24 months, with shares priced at an undeserved premium while the company is facing significant competition resulting in market share losses. Meanwhile, management does not seem to acknowledge these issues and serves investors with overly ambitious financial targets.

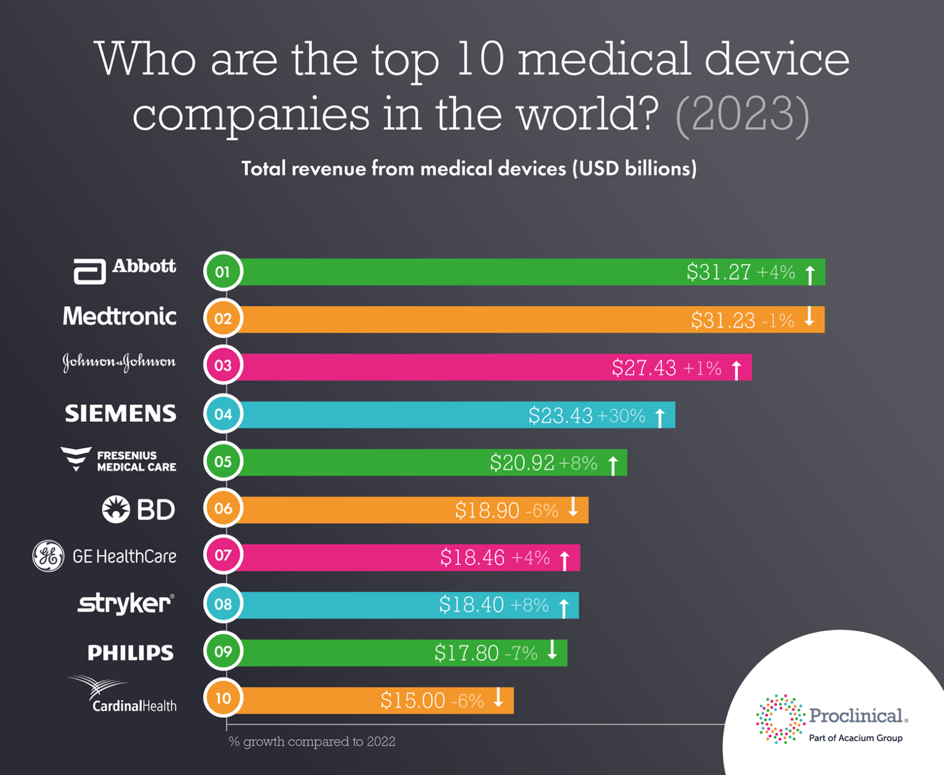

GE Healthcare operates in a highly attractive and steadily growing medical devices industry. The company, recently spun off from General Electric, has a significant market cap of $32 billion but faces challenges in gaining substantial market share due to the industry's fragmentation and the need for significant R&D spending.

The Imaging segment, which constitutes 54% of revenue, poses a concern as GE Healthcare struggles to maintain market share and faces technological challenges. The Ultrasound market, while contributing 17% to total revenue, sees the company losing ground to competitors due to increased competition and pricing pressures. However, the Patient Monitoring and Pharmaceutical Diagnostics segments present brighter prospects, with potential market share gains and growth outpacing industry forecasts.

Looking ahead, management's ambitious growth and margin expansion targets may face headwinds, considering the industry dynamics, competition, and the need for increased R&D spending. The stock, currently trading at a P/E multiple of approximately 18x, appears overvalued compared to peers, leading to a cautious outlook.

In light of these factors and the lack of a compelling upside, I recommend a "Sell" rating for GE Healthcare stock. While shorting is not explicitly suggested, caution is advised, as the company's growth outlook, competitive positioning, and stock valuation may not align with investors' expectations over the next two years.

The medical devices industry remains highly attractive for conservative long-term investors.

The medical devices industry is a highly interesting and attractive one for investors. The industry has shown steady growth over many decades, and while it is not one of the fastest-growing industries and maybe not as exciting as many technology alternatives, it is incredibly steady and, above all, reliable due to the strong secular trends driving this industry and the fact that healthcare demand is something we see through every cycle, meaning the industry is as anti-cyclical and non-volatile as they come. Precisely what every conservative investor searches for.

Furthermore, whatever source you use, one thing all market research agencies agree on is that the healthcare industry outlook is not much different from what we have seen over the last decade, and this means that we can safely assume this to keep growing steadily in the mid-single digits from a market size of around half a trillion in 2022 to somewhere in the vicinity of $800 billion by 2030 . These projections reflect the several global trends that drive demand for medical devices, such as the aging of the population, the growing middle class in emerging countries, and increasing demand for innovative new devices (like wearables) and services (like health data). This also reflects the changing health landscape with lifestyle and chronic diseases becoming more prevalent and the growing emphasis on early diagnosis and treatment, which leads to a growing number of patients undergoing surgical and diagnostic procedures as well as a higher need for self-monitoring equipment.

The expansion of the market is further propelled by the introduction of novel and advanced equipment. The surge in demand for cutting-edge therapies, coupled with technological progress in medical devices aimed at addressing unmet needs in the healthcare sector, stands out as a key driver for the anticipated growth of medical devices in the coming years.

Overall, this leads to a very reliably growing industry, supporting growth for its largest players. Therefore, taking into consideration the strong secular trends driving this growth in medical equipment so grows my interest in the manufacturers of this equipment, including the likes of Philips ( PHG ), Siemens Healthineers ( SMMNY ), and GE Healthcare.

In this article, I will focus on GE Healthcare or GEHC.

GE Healthcare – The basics

GE HealthCare is a global leader in medical technology, pharmaceutical diagnostics, and digital healthcare solutions, focusing on providing a wide range of medical technologies and services. The company operates as a leading global provider of healthcare solutions, offering products and services in areas such as medical imaging, diagnostics, patient monitoring, and pharmaceutical diagnostics.

Prior to this year, the company operated as a subsidiary of General Electric ( GE ) but was spun off at the start of 2023. It now trades on the Nasdaq as an individual company. Nevertheless, the company has a rich history, and with a market cap of $32 billion, GEHC is a leading player in the medical equipment market, operating alongside close peers Siemens Healthineers with a market cap of $63 billion and Philips at a market cap of just below $20 billion.

Still, despite its significant market cap and annual revenue of over $18 billion, the company only holds a minor market share in the industry, as the medical equipment industry is a highly fragmented one. We should keep in mind that it requires significant amounts of R&D spending and testing to bring medical devices to market, and with the sheer broadness of this industry, it is practically impossible to control a large share. Every company has its area of specialty, and even as GEHC spends over $1 billion in R&D annually and is a leader in its specific industries, it only accounts for a small piece of the entire market.

With revenue of $18.34 billion and a market size of $512 billion, we arrive at a market share of approximately 3.5% for GEHC, give or take. This makes the company the 7 th largest in the industry in terms of revenue. For reference, the company has over 4 million medical devices installed globally, and with this incredible installed base, the company serves over 1 billion patients annually.

{kind=link}

Proclinical

Furthermore, the company reports across four operating segments: Imaging, Ultrasound, Patient Care Solutions, and Pharmaceutical diagnostics. Management believes this gives it a TAM, which will grow to $100 billion by 2025, giving the company plenty of room for growth.

Medical Imaging – The largest segment is a drag on growth as it loses market share

The most important and largest segment in terms of revenue for GEHC is Imaging, which accounts for 54% of revenue. The company produces a variety of medical imaging devices, including X-ray machines, magnetic resonance imaging (MRI) scanners, computed tomography (CT) scanners, ultrasound systems, and positron emission tomography ((PET)) scanners. In Medical Imaging, GEHC is the second largest in terms of market share, only trailing Siemens Health.

However, while being the company’s largest segment, medical imaging is actually one of the slower-growing verticals of the medical devices industry. The global medical imaging market is expected to grow at a CAGR of 4.8% through 2030 , driven by the rising incidence of lifestyle-related diseases, a growing need for early detection tools, and advancements in technology aimed at enhancing turnaround times. This sits in line with management’s projected growth of 4-6% annually, indicating little change in market share. In addition, management believes it can expand its EBIT margin in imaging from a historical range of 10-13% to the high teens, which would be significant for EPS growth.

However, over the last few years, growth in the company’s imaging segment has been far from straightforward. GEHC seems to face challenges in competing in the high-end imaging market as it loses market share, making it hard to view management’s growth and margin goals as realistic. Crucial to understand is that GEHC has the broadest product portfolio in imaging of any of the top 5 vendors, but at the same time, there is no single clinical or product sector where it dominates or offers products of unique quality, but as an accomplished generalist, can meet the needs of a wide range of customers. However, in medical equipment or imaging in particular, this strategy does not seem to work out today.

On top of this, the company has struggled in recent years to integrate digital technologies into its imaging equipment and has fallen behind the competition in technological dominance. Citing Signify Research , one of the world’s largest intelligence providers to Healthcare leaders:

The vendor has held a large share of the market for a long time, but that share is slowly being eroded. Whether GE can stem this customer leakage is dependent on how well it can deliver on the newer, better-connected, data-driven facets of imaging IT.

Therefore, I am quite bearish on the company’s prospects here and actually view the imaging segment as a drag on the company’s growth potential, especially with this segment accounting for 54% of total revenue.

With GEHC heavily depending on this market to drive its growth, I am not too optimistic. Current R&D levels also cannot match that of peers, and I believe it will, therefore, require at least a few years of significant R&D spending for the company to strengthen its position in this market. Therefore, I expect GEHC to struggle to grow this segment in line with its goals over the next couple of years, as further market share losses are highly probable. As a result, I project a CAGR of closer to 2-5% for this segment.

Ultrasound – GEHC is losing market share as it faces intense competition

In the Ultrasound market, GEHC leads with a 13% market share (17% of total revenue), followed closely by Siemens Health and Philips. GEHC produces a range of ultrasound equipment designed for medical imaging purposes. The company’s ultrasound technology is applied in various medical specialties, including obstetrics, gynecology, cardiology, and radiology. The ultrasound equipment is designed to provide detailed imaging for diagnostic purposes, allowing healthcare professionals to visualize and assess organ structures, blood flow, and abnormalities. GE Healthcare's ultrasound offerings typically include a variety of system models with different features and capabilities to meet the diverse needs of healthcare providers and medical facilities.

Growth in ultrasound has been strong, and this segment also carries far higher margins in the 22-28% range, positively contributing to the company’s bottom line. And yet, the company is also struggling in this segment. Research by SkyQuest Technology Consulting shows that GEHC struggles in this market as it has been losing market share to rivals such as Philips and Siemens Health in recent years. On top of this, several new entrants into the market, such as Samsung and Hitachi, are offering competitive products at lower prices, putting further pressure on GEHC.

Suppose GEHC wants to stay competitive and put a stop to the market share losses. In that case, it will likely be forced to increase R&D to regain its technological dominance or sacrifice margins to undercut competitors on pricing. Either way, the company is facing financial headwinds, and as a result, I don’t view management growth goals as realistic here either.

Management aims to grow revenues of this segment at a CAGR of 4-7%. Meanwhile, SkyQuest Technology Consulting expects the ultrasound industry to grow at a CAGR of around 4.1% through 2028, indicating that management expects to outgrow the industry. While I very much hope it can turn recent trends around, I can’t see this happening anytime soon and therefore expect management to perform in line with the industry at best, projecting a revenue CAGR of 3% to 4.5%

Patient Monitoring and Pharmaceutical Diagnostics – Growth is looking better here

GEHC also has a strong presence in both the patient monitoring devices and Pharmaceutical Diagnostics markets. The company provides patient monitoring systems that enable healthcare professionals to monitor and track vital signs and other patient data in real-time. This helps continuously assess a patient's health status, measuring factors like heart rate, blood pressure, respiratory rate, and oxygen saturation. The company’s offering also includes bedside monitoring and wearable monitoring devices.

The company currently holds the #2 position in this industry, trailing only Philips. The company has seen some market share gains in recent years following a shake-up of the industry due to the COVID-19 pandemic, which has driven some additional growth. GE Healthcare’s dominant global presence in core clinical markets, including anesthesia and diagnostic cardiology, also aided the company in increasing its share of the global clinical care device market overall.

Looking ahead, the company’s offering is looking strong. As Philips has been experiencing significant problems with its patient monitoring equipment in recent years, we could see GEHC take some additional market share from the industry leader due to the brand damage for Philips. Therefore, we could see GEHC outgrow the industry’s growth forecast.

Currently, the industry is expected to grow at a CAGR of 9.1% through 2027 , making it one of the fastest-growing verticals in the entire healthcare equipment industry. This growth is driven by the increasing prevalence of chronic diseases, such as cardiovascular disorders, diabetes and respiratory conditions, the aging population, and ongoing advancements in technology, including the integration of wireless technologies, data analytics, and AI.

Meanwhile, management seems somewhat conservative here, projecting growth at a 3-6% CAGR through 2025. Management also sees room for margin expansion from a level of 10-12% in the last few years to the high teens, which is reasonable. However, I also expect faster growth at a 7-10% CAGR through 2030.

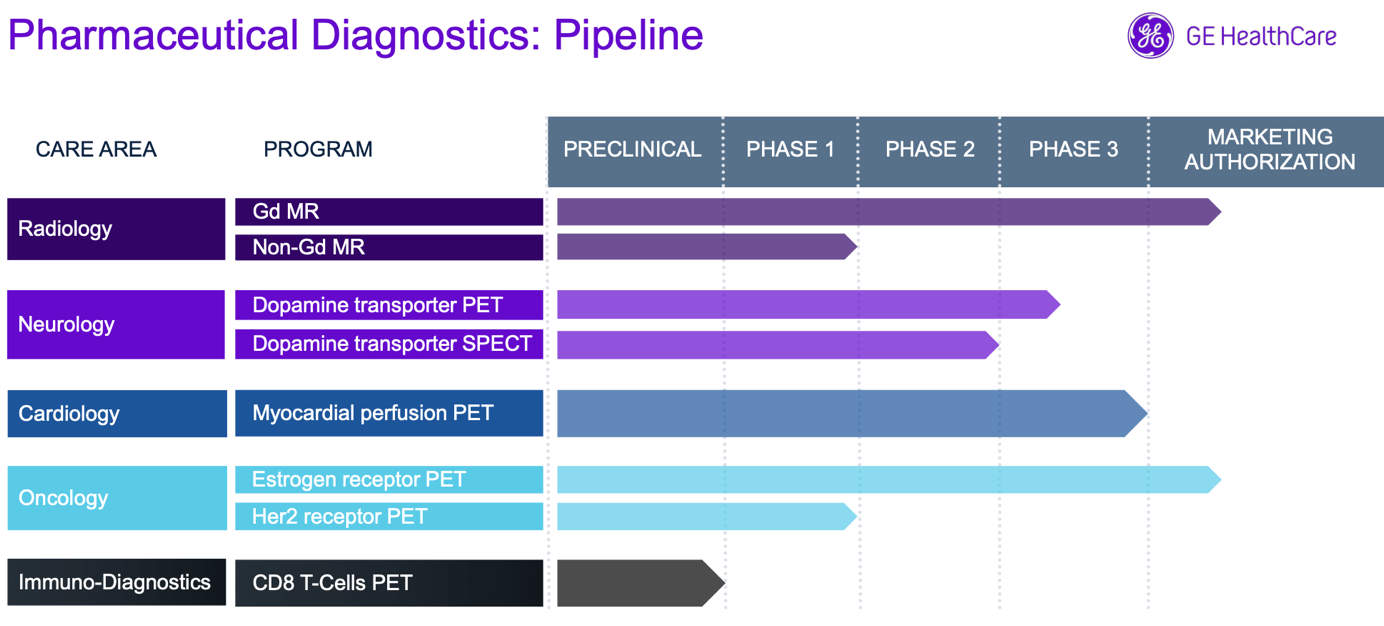

Finally, there is the Pharmaceutical Diagnostics segment. The company offers diagnostic solutions for various medical conditions, including laboratory diagnostics, molecular diagnostics, and point-of-care testing. This includes equipment and technologies for clinical chemistry, immunoassay, hematology, and microbiology. In addition, GE Healthcare is involved in developing and manufacturing tools and technologies used in life sciences research and biopharmaceutical manufacturing. This includes equipment for cell culture, protein purification, and bioprocessing.

{kind=link}

GE Healthcare

This segment is another one with a stronger EBIT margin, sitting in the low 30s. Furthermore, growth has been stable recently, and the company is performing well. Therefore, the 4-5% CAGR targeted by management should be achievable, although this could end up slightly higher depending on market dynamics. Note that this segment only accounts for 12% of revenue as of the most recent quarter.

GEHC should be able to boost growth with its lead in AI integrations

Across the product portfolio, GEHC management aims to boost growth by focusing on investing in AI integrations and digital solutions, in addition to the obvious focus on introducing new and more innovative products. For reference, 35% of orders today are derived from products introduced after 2021.

{kind=link}

GE Healthcare

Positively, in terms of AI innovation, GEHC is ahead of the competition, which could give it a technological edge and position it more favorably in the market as demand for these AI developments is skyrocketing. GEHC topped the FDA’s list for most AI-enabled medical devices for the second year in a row as it now has 58 FDA-cleared or authorized AI-enabled devices in its portfolio, far ahead of second place Siemens Health with 29.

Meanwhile, Morgan Stanley estimates that AI will represent 11% of healthcare budgets in 2024 , showing rapid growth and making it a massive market. With GEHC having an edge over its competitors on this front, it could be a primary beneficiary of the growing demand for AI technologies in the healthcare industry. Moreover, according to Acumen Research and Consulting, as a result of these growing budgets and the focus on AI, the Healthcare AI market is projected to grow at a stellar CAGR of 44% through 2032 , representing a massive runway of growth for GEHC.

With the company already leading the way in AI development in healthcare equipment, I expect AI to drive additional growth across product categories. However, the significance of this is hard to estimate today, so I remain conservative with using this in my financial projections. Nevertheless, this is a significant positive for GEHC investors.

Revenue is well diversified and de-leveraged, but management’s growth target seems out of reach

Finally, let’s take a quick look at the company’s revenue stream, which looks mostly well-diversified and de-leveraged. Crucial here is that 50% of revenue is recurring and is made up of services, digital solutions, value-added offerings, and education & training. As discussed, this industry is already very anti-cyclical. Still, the recurring service revenue further strengthens this while also boosting margins: a big positive, but no different from what we see from peers.

Also, GEHC’s revenue is well diversified by region, with the US being the largest, accounting for 42% of revenue, followed by the EMEA with 26%, China with 15%, and the rest of the world with 17%. This not only means the company’s revenue is well diversified, but it also means that it derives the majority of revenues from stable economies and regions, de-leveraging the revenue stream. In the meantime, the company has more exposure to emerging markets than most of its peers, which could drive some additional growth due to the faster-growing healthcare market in these regions. In general, there are just very few things to complain about here.

Now, while management is positive about its long-term growth and has set optimistic margin expansion targets, growth for the company is not as straightforward as it is for the previously discussed underlying medical devices industry, and the targeted margin expansion will be hard to accomplish.

Overall, management targets revenue growth of mid-single digits and high teens to 20% EBIT margin, which I view as slightly ambitious despite this sitting in line with the projected industry growth. Considering everything discussed so far, I am expecting growth to come in slightly lower or in line with management's growth targets at a CAGR of 3-6%.

In terms of margins, there definitely is room for margin expansion, just not as much as management targets. According to management, driving margins is the focus on higher-margin products as a result of innovation and a better product mix, including more software revenue. All this makes sense, but we should also consider the headwinds GEHC is facing on the margin front, including higher required R&D levels to keep up with the competition and protect its market position.

Furthermore, the company is facing pressures from governments worldwide to lower healthcare costs, especially in the most expensive part of the system: hospitals. As a result, we will increasingly start to see downward pricing pressure, making margin expansion a serious challenge, according to KPMG . Therefore, I am slightly more skeptical toward the targeted margin expansion and expect GEHC to slightly disappoint here as EBIT margins above the 17-18% level for the group seem unlikely in the medium term.

GEHC’s Q3 results accentuate weaknesses

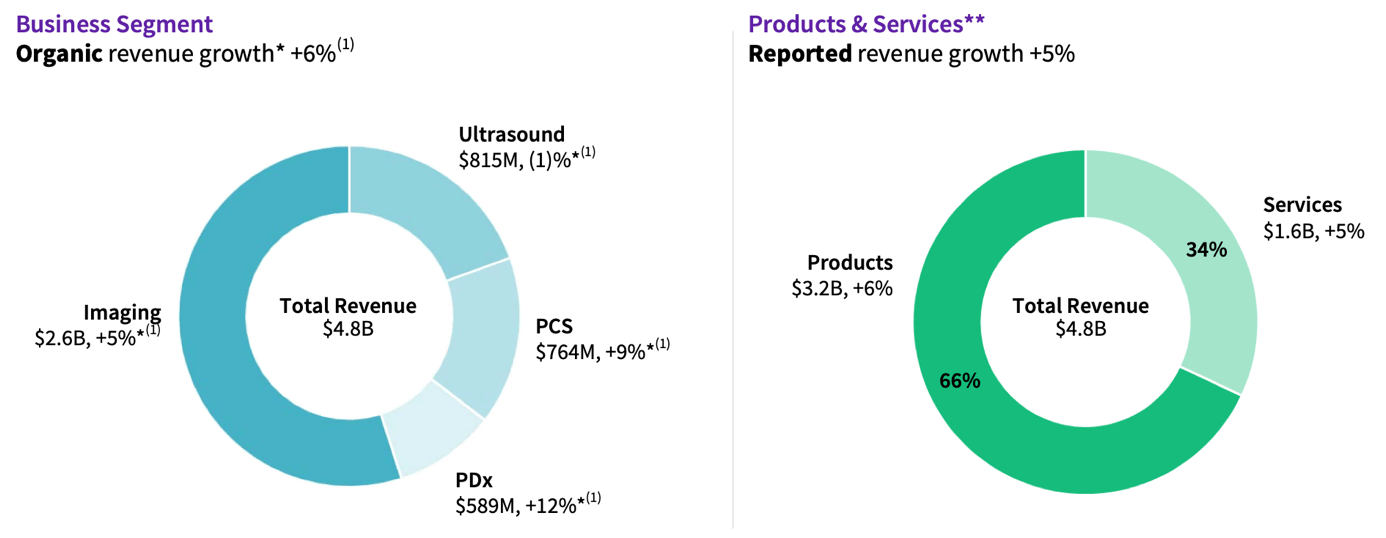

GEHC reported its Q3 results on October 31 and marginally beat the revenue consensus while beating EPS by 10%. The company reported revenue of $4.8 billion, up 5% YoY or 6% organically. This was driven by both volume and price and sat below the growth reported by the likes of Philips and Siemens Health, with a growth of over 10%, which is far from ideal. Across the board, growth is still normalizing from significant price increases and recovering supply chains.

Growth for GEHC was driven by all regions. This meant the company saw little impact from the Chinese anticorruption campaign, something Philips struggled with much more visibly. Both system deliveries and orders from China were stable for GEHC.

Looking at the segments, Ultrasound was the most significant drag on growth as this segment saw revenue fall by 1% YoY, which was partly due to a challenging comparison versus the third quarter of 2022 but also the result of some market share losses and a weak demand environment.

Meanwhile, Imaging grew by a steady 5% YoY. While this might seem fine, this growth sat significantly below peers, with Siemens reporting growth of over 15% in imaging and Philips reporting 12.7% growth in its Diagnosis and Treatment segment over the same months. Therefore, we can clearly see that GEHC is underperforming peers in both of its most significant segments, straight up reporting much slower growth.

{kind=link}

Q3 data (GE Healthcare)

Furthermore, for the Patient Care Solutions segment, GEHC reported organic revenue growth of 9%, driven by volume and price, as it was able to fulfill more of its backlog due to an improving supply chain. As explained earlier, this growth was much better than that of the closest peer, Philips, as GEHC is performing exceptionally well on this front. Finally, Pharmaceutical Diagnostics revenue was up 12%.

While the revenue performance was far from strong compared to peers, there is also room for some positivity as the company’s order intake was solid, which is an essential indicator of customer demand and future growth. GEHC reported a healthy book-to-bill in Q3 of 1.03x, below the 1.11x reported by Siemens Health, but much stronger than Philips. Philips reported a decline of 9% in its order intake dollars YoY, while GEHC actually grew order intake dollars by 1% YoY. As a result of this strong order intake, the backlog remains robust at $18.4 billion, driven by Services and Imaging products. This gives the company some visibility on future revenues. Also, the company completed a customer pulse survey in the US and saw no significant change in sentiment on capital spending in the second half of 2023 versus the first half of the year, indicating a healthy demand environment.

Moving to the bottom line, GEHC saw some margin expansion across the board. The adjusted EBIT margin was 15.4% and expanded by 10 bps YoY and 60 sequentially, benefiting from increased volume and productivity actions. The company has focused on optimizing its G&A by rationalizing its real estate footprint and simplifying IT services and systems across businesses to create efficiency at scale.

These efforts offset the growth in R&D investments, which still only represent 7% of revenue, compared to the 9.1% reported by Siemens Health and the peer-leading 14.2% reported by Philips. Clearly, GEHC has to get its priorities straight if it wants to compete.

If the company wants to stop the market share losses, it will have to increase its R&D to catch up technologically. If it would increase R&D to 11% of revenue, in between its two closest competitors and what I view as the real minimum, this would lower the EBIT margin to just 11.2% based on the Q3 financials, which is precisely why I view management’s margin goals as too optimistic. It will be able to maintain current margins at best if it does not want to lose more market share.

Moving back to the Q3 results, the gross margin was up 90 bps YoY to 41%, and this was driven by pricing and enhanced execution, as well as variable cost productivity initiatives. These margin improvements led to an adjusted EPS of $0.99, up 14% YoY on a stand-alone basis. Also, free cash flow was up year-over-year to $570 million.

As a result, the company ended the quarter with a cash position of $2.4 billion and a total debt of $10.2 billion, which is manageable considering the company’s strong free cash flow and no significant dividend obligations.

Outlook & Valuation – Is GEHC stock a Buy, Sell, or Hold?

Following these Q3 results, management now guides for Q4 revenue growth in the range of 6% to 8%, reflecting revenue of $5.2 billion at the midpoint. This would result in FY23 revenue of around $19.5 billion. Meanwhile, the FY23 EBIT margin is expected to remain in the range of 15.0% to 15.5%, and following the relative outperformance YTD, management has increased its FY23 EPS guidance to $3.75 to $3.85, representing growth of 11% to 14%.

Following this guidance from management, the Q3 results, and my in-depth analysis of the company, I now project the following financial results through FY26.

{kind=link}

Financial projections (Author)

Based on these estimates, GEHC shares are now trading at a P/E multiple of approximately 18x, which I believe is quite a premium to pay for a company losing shares in its largest markets, with R&D levels below peers and questionable growth and margin expansion outlook. Honestly, considering the risks involved and potential actions needed to be taken by management to ensure a strong future, I don’t believe a multiple of over 15x is reasonable for GEHC today when taking into account peer valuations.

Considering recent developments, I never expected to say this, but I prefer Philips over GEHC. This is primarily due to Philips’ offering holding a much stronger position in the market. GEHC and Philips compete in three healthcare device markets. Philips currently holds the dominant market share in all three, primarily due to the company’s higher R&D spending and superior products.

Of course, whether Philips is worth buying considering developments in recent years and weeks is a whole another question and not one I am looking to answer here, but what I am trying to point out is that GEHC is simply not the best positioned or best-diversified pick in the Healthcare devices market today. Quoting BTIG analysts : “GE HealthCare faces competition from all angles.”

All things considered, I am awarding the shares a 15x multiple, and based on this and my FY25 EPS estimate, I calculate a target price of $65 per share, representing a downside of 6% from today’s levels around $69.40. Therefore, I do not see any upside over the next two years from current share price levels unless GEHC can significantly outperform my expectations, which I deem highly unlikely.

With questionable growth targets, the company losing share to competitors, and it simply not being the best-positioned in the industry, leading to a disappointing growth outlook, I see no other option than rating shares a sell at current levels. Don’t get me wrong, I am not recommending shorting GEHC shares, but I don’t see any upside and expect shares to keep trading around current levels for at least another two years.

As a result, I recommend avoiding GEHC stock for now, resulting in a “Sell” rating

For further details see:

GE Healthcare: Unveiling Red Flags In Its Growth Story