GEAGF - GEA Group: At The Right Price You Should Buy This Company

2023-08-10 01:56:47 ET

Summary

- GEA Group is a systems supplier in the industrial sector, serving various end markets, including food production, beverage production, and the pharma sector.

- The company has solid financials, with billions in revenue, strong margins, and a decent dividend.

- GEA Group is a net beneficiary of global megatrends and has a diverse customer base, making it an attractive investment in defensive sectors.

Dear readers/followers,

It's been a long time since I reviewed GEA Group ( OTCPK:GEAGF )—several years, as a matter of fact, with the last article in 2019. I do not currently own the company, having rotated most of my position during the COVID-19 recovery. It was, however, a small position, so I did not think it merited much attention at the time with everything else that was going on.

However, I believe the time has come to lift every rock you can to find undervalued quality companies in defensive sectors. I believe defensive sectors will offer some of the best value, upside, and protection in the near term, and I'm allocating non-trivial amounts of capital to these sectors.

GEA is now on my list again. It's not at the top of that list - there are other companies with substantial upsides here - but it's certainly on my list of companies to look very closely at.

Let me show you why that is.

GEA Group - a Reminder

So, with almost 4 years since my last article, it's time for a reminder of just what this company is, and any updates that have happened in the meantime.

GEA Group is a systems supplier. That means that the company supplies manufacturing and processing systems on the industrial side for various end markets, including food production, beverage production, and the pharma sector.

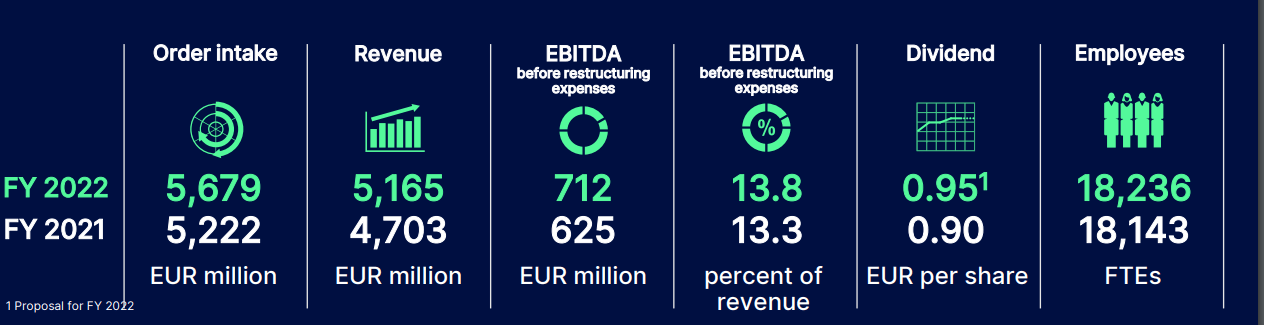

The company has billions in revenue, solid EBITDA and margins, a very decent dividend, and employs over 18,000 people.

{kind=link}

The company trades on the German market under the native symbol G1A. The ADRs are, to my mind, too thinly traded to constitute a decent investment in the company and should be avoided.

GEA is a market outperformed and even market leader. In terms of RoE, no company in the company's specific market does better. Even on the gross, operating, and net margin side, GEA performs exceptionally well, coming to a near 8% net margin in the industrial products sector. Its comps/peers mean that these numbers are seen in relation to companies like Siemens ( OTCPK:SIEGY ), GE ( GE ), Schneider Electric, Eaton ( ETN ), Emerson ( EMR ), and others. This is not a bad group to outperform/be above average. While these peers serve as decent high-level comps, GEA certainly does very different things to what these other companies describe and do.

Simply put, the company is active in sectors such as Food, Dairy farming, beverages, pharma, chemicals, refrigeration/heating, and Marine. Just how ubiquitous is what GEA does?

- Every third Chicken Nugget is made using GEA tech.

- Every third-line process for instant coffee was installed by GEA.

- A quarter of all processed milk comes from GEA production systems.

- Every second liter of beer is brewed using GEA production systems.

- Every fourth liter of human blood for plasma products is processed with GEA systems.

- More than 33% of all polymers are used using GEA drying tech.

- More than 50% of all container ships worldwide have GEA equipment on board.

Those are some impressive, albeit market/PR-based stats. GEA is a net beneficiary of global megatrends. This includes a growing population, urbanization, changing demographics, and other megatrends I often mention when looking at various businesses.

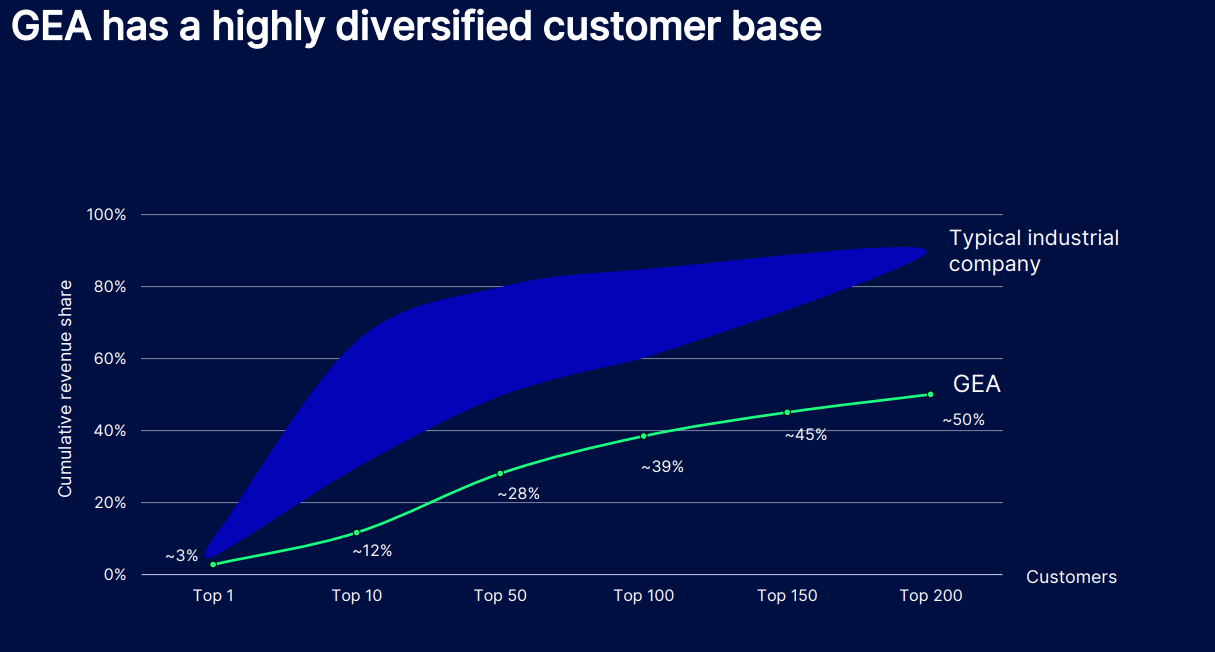

The company has, compared to other industries, far improved customer diversification.

{kind=link}

No single customer has more than 3% of sales. The company's sales and segment splits are as follows for the 2022A period.

{kind=link}

As you can see, the company has an overall attractive diversification, with liquid/power making up the largest at over 32%. COGS are below 67%, and for an industrial, this is good. If anything, I would argue that SG&A is comparatively high for the scale that the company has, but this could also be a product of exactly that SG&A. The company has a working business model that takes one dollar of revenue and makes around 8 cents of profit - and that's a good business model.

Operating revenue also has a very appealing geographic split. 21% NA, 24% APAC, but most of it, over 30%, in Germany and Western/middle Europe. LATAM is small for now at only 6%.

The latest trends out of the company for 2022 speak to a strong continued trend. We saw organic sales growth as well as organic margin expansion, despite overall headwinds, resulting in a dividend increase. The company is not a high-yielder. At €0.95/share, the company yields about 2.5%, which is still okay, all things considered.

The company also lacks meaningful IG credit - but is one of the lowest-leveraged companies in its entire sector. The LT debt/Cap is below 10%, which makes this a net cash/no net debt company. This grants the company very high conservative safety scores and extreme cash/debt levels. The company has been a net cash company for over 8 years, with only one exception back in 2019 during COVID-19 - and only marginally.

However, GEA has faced some growth issues. By that, I mean that revenue has been mostly flat over a long period of time.

{kind=link}

So, margin improvement and growth are what we want to see here, not just over the short term as we're seeing now, but in the long term. GEA is delivering positive results here. It overachieved its 2022A targets with a 50 bps higher organic sales growth, and a substantially higher EBITDA margin at 13.8%. The expectation on the low end back in 2019 was 11.5%.

The next set of goals is for 2026, and the company is currently working hard to implement these.

{kind=link}

The order intake and sales continue to show stability. For the latest quarter, we have divisional improvements across all segments - and those improvements were organic. These are large individual orders with a value of above €15M contributing most to the growth here.

Margins are also improveing, driven by modernization and optimization. There is some increase in OpEx, driven by increased SG&A, in particular, travel, but this set of costs is likely to wind down as some of the new organizational build-up is finished. Overall, I'm not too worried about company margins being low on a forward basis, but expect them to be stable or improving.

Here is a good visual bridge representation of the latest set of published results in relation to YoY.

{kind=link}

Cash conversion stands at a good level - somewhat below the target corridor, but this was due to a one-off in net working capital for the FY22 period. The company has a very strong backlog in the billions of €3.2B for this year, which is set to continue to deliver solid trends on a forward basis.

On the risk and headwind side, we have cost increases - and these are significant. For 2023E, the company expects a €140M in annual cost increases from local inflation and wage which generate non-trivial headwinds and require the company to save elsewhere. Also, logistical headwinds are far from over, as we've seen in other companies. The 1Q23 results, reported in May, confirm this. It was a strong start to the overall year, with even higher levels of orders despite record YoY, to 3.9% growth and a €1.6B quarterly intake, coming to a run rate of over €6B. The company also raised guidance as of this.

However, risks exist. The companies in the industries that GEA serves are currently under pressure from inflation. Food price inflation does not only affect customers or supermarkets - supermarkets and FMCGs put pressure on producers. This is a double-edged sword. On one hand, new investments into more efficient machinery might be possible due to the pressure of ever-lower costs, but that also might result in some customers trying to leverage GEA.

GEA for the time being confirms that the business environment is very stable, and growth potentials are solid. However, I do want to mention that I do see instability in the overall FMCG market, and this is also expressed in the company's valuation and share price, which we'll look at here.

Valuation for GEA Group - It's attractive, but not the most attractive it's been.

Due to the company's very safe end markets, the GEA group is usually traded at a premium - and a high one at that. 25x P/E is standard for this company. On the surface, that makes the current valuation of below 15x P/E relatively undervalued. The problem is that despite lofty company targets for sales, margins, and earnings are under pressure, and we're currently expecting a low single-digit overall growth rate at least until 2025E.

By low single-digit, I mean that. Low. At 1.01%. Similar numbers come from S&P Global and FactSet here, and this puts into question just how high the company should be valued - especially with a sub-3% yield that is very unlikely to grow significantly.

Let's start conservatively.

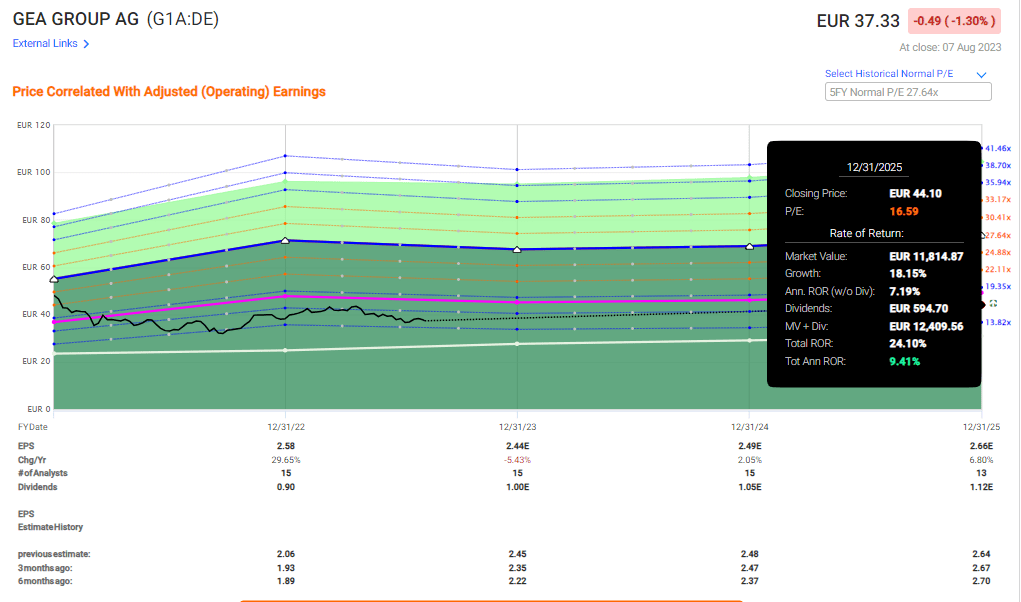

You're unlikely to lose money on GEA. Even at a sub-14x P/E, the RoR is positive. At 16.5x forward, it looks something like this - and this is well below where the company currently trades.

{kind=link}

But obviously, 9% per year is no longer good enough for me. I want a 15% minimum per year worth of annualized RoR. What does it take for us to get this when it comes to this company?

Around 19x P/E is where we find above 15% annually. It's a likely turn-out to my mind, given the sheer premiumization and fundamental safety of the business. That being said, It's far from the best investment potential out there today.

The company is considered at an average price target range of €31 on the low side to €52 on the high side. €31 is too low and €52 is way too high. 17 analysts follow the company and only 5 at "BUY" or equivalent showcase the degree of uncertainty due to the muted growth forecasts. Still, the average PT of €43/share is relevant here. I forecast it somewhat lower, giving the company an average target of around €41/share, which is an upside here, but one of only about 11%.

Still, that's good enough for me to invest in. When I look at GEA, I consider above other things the fundamental safety of the operations and allow a premium for this. I've considered also engaging in selling cash-secured puts, as well as trying for the buy-write covered calls option, but none of these give me the returns that I'm looking for. For this reason, straight investment into the common share is the preferable way to go for me here.

Here is my thesis on the company.

Thesis

- GEA Group is a market-leading name in the food processing and other processing systems industry. The company is a market leader with excellent tradition and overall safety. It has no net debt, and it's a net beneficiary of overall macro trends, including demographics, urbanization, and food consumption. This is the sort of company I like buying.

- However, I want a 15% annualized RoR for this company. At this valuation and these prospective growth rates, that is not an easy estimate to find on a realistic overall basis. We find it at around 19x P/E, which constitutes a significant discount even to a 20-year premium of 22x P/E.

- I consider it likely for the company to be worth around a 20-21x P/E long term, and for that reason I consider the company a "BUY" with a €41/share PT - but the upside here isn't large. So if you "BUY" GEA, you should do so for quality - because there are companies with better upsides out there.

- Nonetheless, at €37/share I'm back in, and I'm now LONG GEA.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills every single one of my criteria, making it relatively clear why I view it as a "BUY" here.

For further details see:

GEA Group: At The Right Price, You Should Buy This Company