GEN - Gen Digital: The Debt Post-Merger Is Worrying

2024-01-18 17:22:38 ET

Summary

- Gen Digital's financials show a massive debt load and slightly worsening margins, prompting a hold rating until debt levels decrease and operations improve.

- The company's current ratio is low but not a deal breaker due to deferred revenue from subscription-based models.

- The company's efficiency and profitability need improvement, and revenue growth is expected to slow down in the future.

Investment Thesis

Gen Digital Inc. ( GEN ) is about to report its quarterly results, so I wanted to take a look at the company's financials to see if it would be a good time to start a position. With a massive debt load on the books and slightly worsening margins, I am assigning the company a hold rating until I see the debt levels come down significantly and operations improve, as there is a lot of work ahead.

Briefly on the Company

The company recently changed its name from NortonLifeLock, after the company merged with Avast. The company provides cybersecurity solutions for consumers all around the globe. Its main product is real-time protection for PCs, Macs, and mobile devices. The product also offers a VPN service and other security solutions.

Financials

As of Q2 '24 , the company had around $630m in cash and equivalents against a whopping $9.3B in long-term debt. the outstanding debt increased significantly due to the company’s merger with Avast . That is a lot of debt, but I believe it was a good opportunity to expand its presence in the segment. Many investors will be put off by the excess of debt on the books as leverage does carry quite a lot of risk, especially if the company cannot manage it properly. I look at a few metrics that help me decide whether the debt is going to be a problem in the future.

Firstly, the company’s debt-to-assets ratio has been hovering around the range of .28 to .61. I like companies that stick to the upper range of .6 and not go over it, so in terms of assets, the company seems to not be overleveraged. The next metric is where it is starting to look a little shaky. The debt-to-equity ratio I look for is under 1.5. The company’s D/E ratio has been wildly fluctuating over the years due to negative equity and now due to the high amounts of debt on the books. It is well over my limit of 1.5, which means I will have to add more margin of safety to the valuation calculations later. Lastly, I look at the company’s ability to pay its debt obligations in the form of annual interest expense on debt. Due to such a high debt number, the interest expenses skyrocketed. Many analysts look for at least a 2x interest coverage ratio, which they deem to be sufficient, however, I prefer a company being able to cover the interest expense with available EBIT at least 5 times over. This allows for bad years of performance, as we see in the latest quarter, where EBIT is not able to cover interest expense, and for six months ended September, EBIT just barely covers it. So, even with the loose analysts' preference, the company’s debt is on the riskier side, in my opinion. I don’t think they will default as the company makes a decent cash flow from operating activities, coupled with cash on hand and EBIT that should improve over time. Nonetheless, 1 out of 3 metrics were red flags, which means I will be adding an extra margin of safety.

{kind=link}

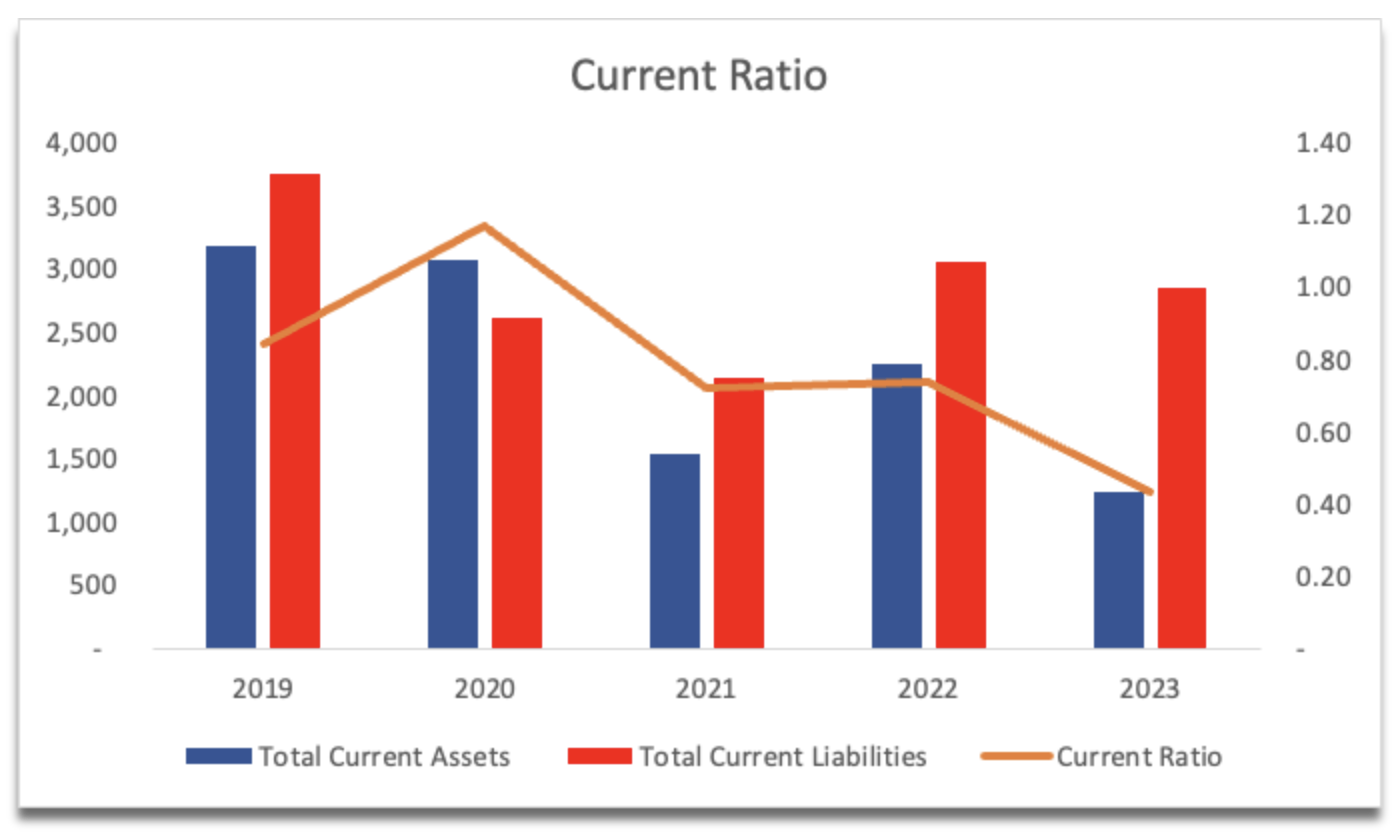

The company’s current ratio has been trending down for a while now, and as of the latest quarter, it is at around 0.44. I don’t think this should be an issue going forward, because the company has a lot of deferred revenue, which is income that has been received but the service has not been provided yet. This is usually the case with subscription-based models, which is Gen Digital's main way of receiving income. I would like to see the company returning closer to its historical average of around 1 over the last decade, however, it is not a deal breaker.

{kind=link}

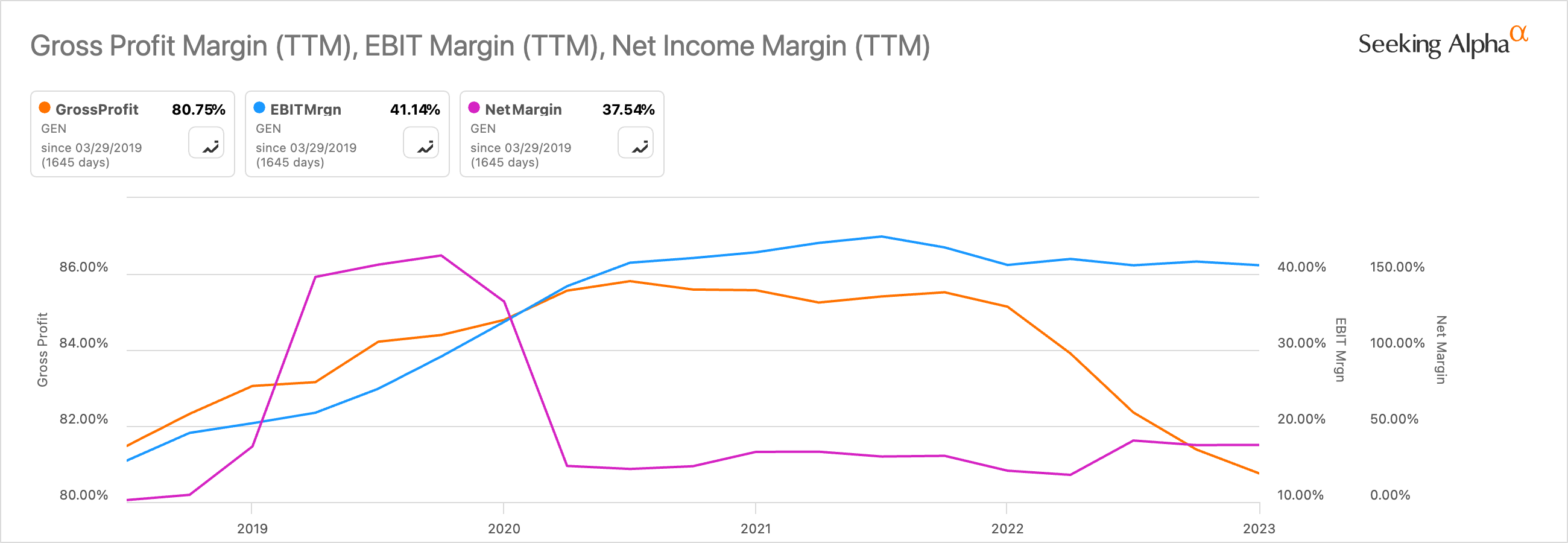

The company’s margins have slowly trended down recently, with the exception of net margins, which saw a decent improvement since the end of '22. It seems that a tax benefit in the last 6 months has helped the company's bottom line considerably, which means once the company starts paying taxes again, the margins will likely come down again. Would it be below where the company was at the end of 2022? Most likely, since gross and EBIT margins trended down in the same period. It seems the company has lost some of its efficiency over the last couple of quarters.

{kind=link}

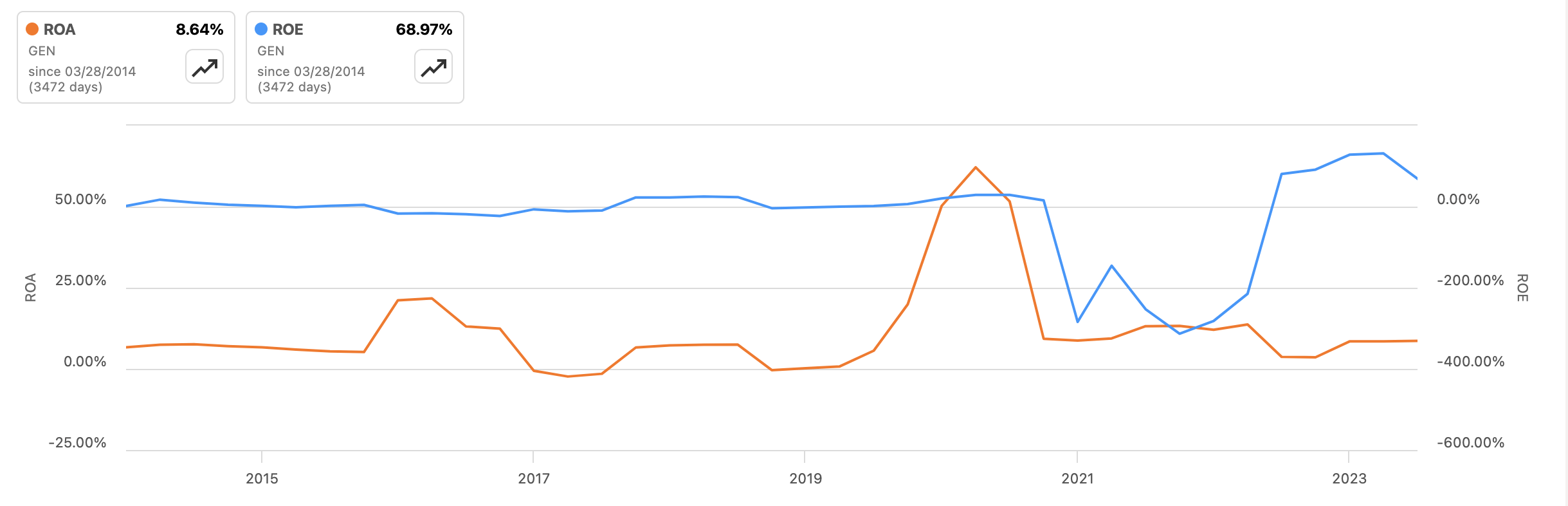

Continuing with efficiency and profitability, the company's ROA and ROE have seen slight improvements recently; however, I would expect ROE to come down considerably in the upcoming quarters, since the tax benefit may not be there any longer, and if we substitute a tax expense of around $200m, the ROE comes down to around 25%.

{kind=link}

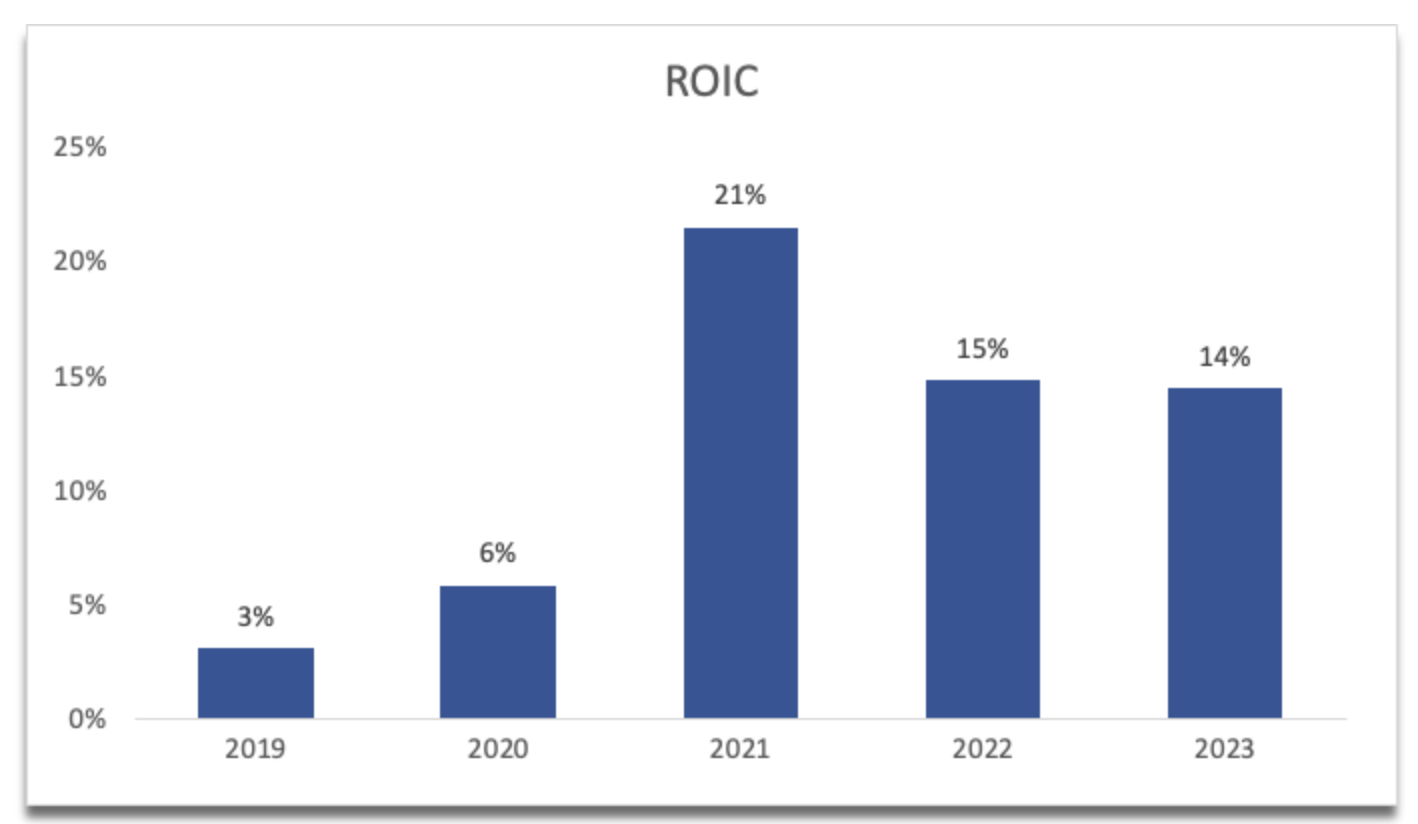

In terms of competitive advantage, it is very hard to find some comparable peers, as most of them are private, and I was only able to find 2 others that the company lists as competitors in their 10K reports. It also lists Apple ( AAPL ), Microsoft ( MSFT ), and Alphabet (GOOG) (GOOGL), but these are not comparable due to their size and the many different industries they operate in. So, I will look at the company’s return on total invested capital by itself, which shows me that the company has lost some of its efficiency in allocating capital to profitable projects. Nevertheless, the company is still above the minimum of 10% I’d like to see.

{kind=link}

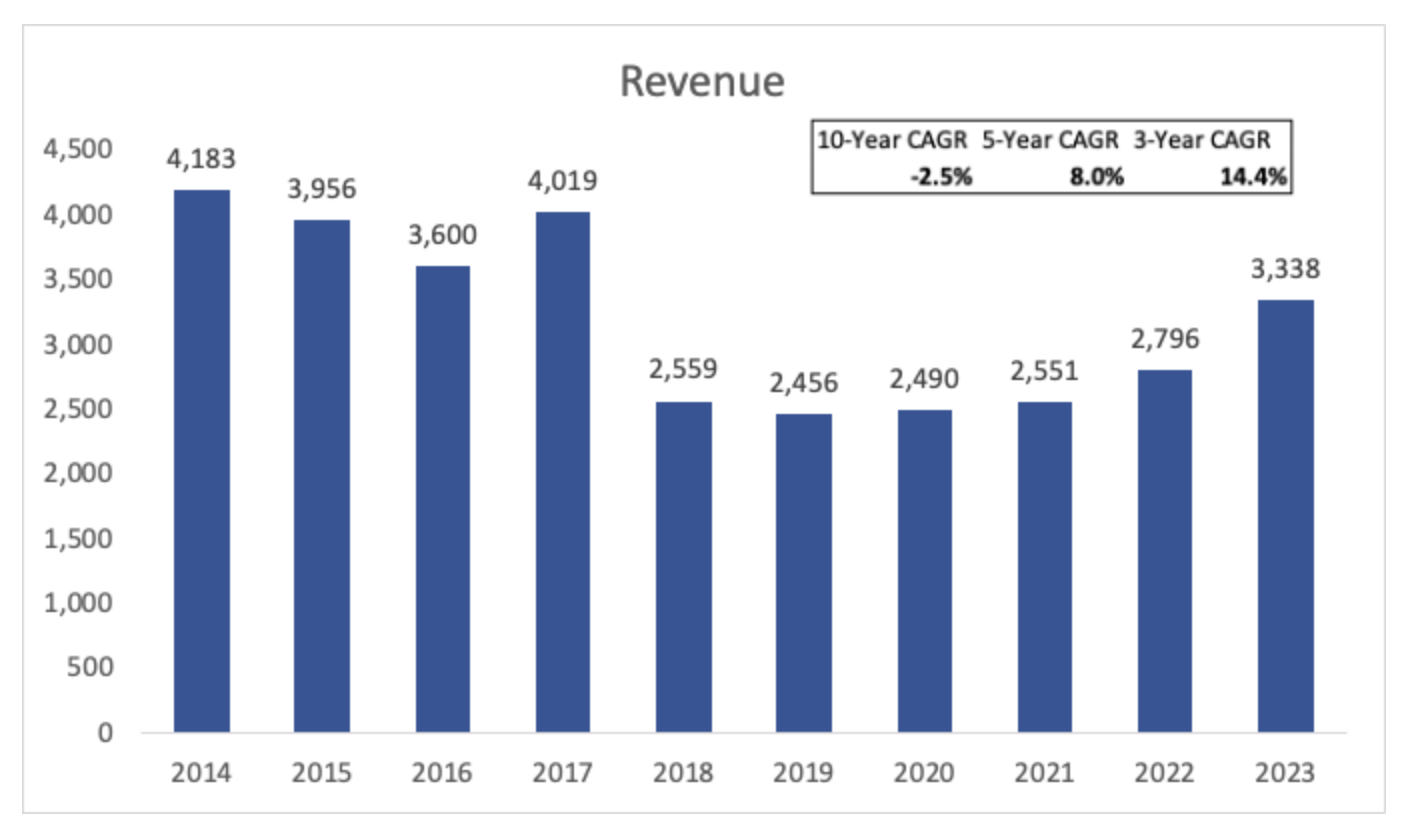

In terms of revenues, if we look at the last 10 years, the company lost around 2.5% a year, but if we look at more recent revenue development, we can see that it is beginning to accelerate, which is a good sign indeed. The merger with Avast is going to help revenue growth further, however, it won’t be a substantial increase, since the company before the merger did around $483m in revenue which was flat at actual rates. The company still has a ways to go before coming back to the revenues it saw a whole decade ago, but if the growth rates remain, it shouldn't be a problem over the next couple of years.

Revenue Growth picking back up (Author)

{kind=link}

Overall, the company seems to be coming back to life. I'm a little worried about the gross and EBIT margins declining slightly, however, I would need to see more quarters to be sure. Nevertheless, the 80% gross margin is still very good. Once the company sorts out the kinks, its efficiency and profitability should come back. The debt outstanding is a big cautionary flag, especially if the company potentially experiences a further downturn in revenues.

Valuation

For the revenue assumptions, I went with analysts’ estimates for FY24 , as that is around what the company has guided in the latest press release . For the future revenue inputs, I decided to approach these with a lot more conservatism, to give myself even more margin of safety. The company will see around 5% CAGR over the next decade in the base case. To cover my bases, I also modeled a more conservative case, and an optimistic case. Below are those assumptions.

{kind=link}

In terms of margins and EPS, the company is guiding for around $1.9 EPS, which is non-GAAP. To give myself a little more margin of safety, I decided to use metrics that are somewhere in the middle of GAAP and non-GAAP. This way I get a very small growth in EPS, which should be quite easy to beat if everything goes according to plan.

{kind=link}

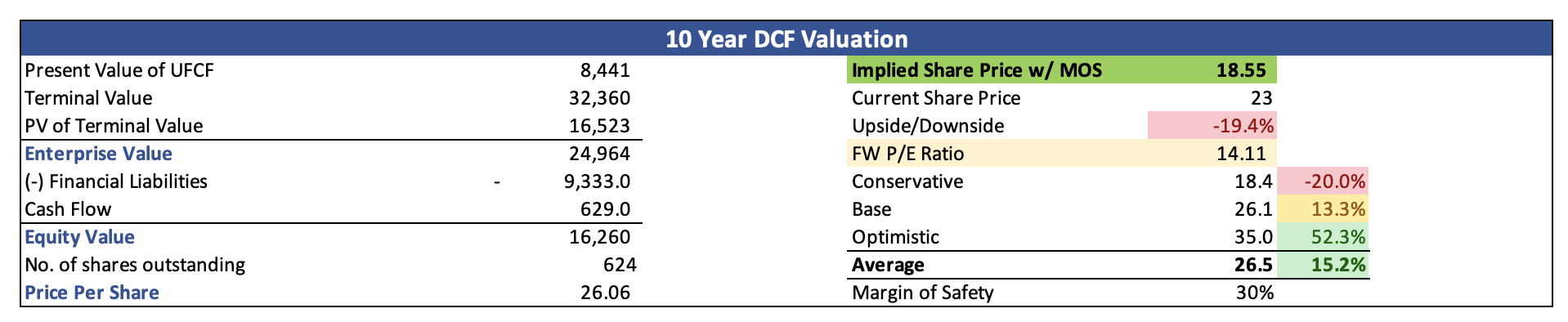

Furthermore, I went with the company's WACC of around 7% as my discount rate for the DCF analysis and a 2.5% terminal growth rate. Additionally, just to have even more room for error in my calculations, I went ahead and added another 30% margin of safety to the final calculation. The debt is very high and I believe that if operations don’t improve, it could pose a danger to the company’s solvency, that is why I added the 30% on top. With that said, Gen Digital’s intrinsic value is around $18.55 a share, which means it’s around 20% over its fair value.

{kind=link}

Comments on the Outlook and Takeaway

I would like to see the company take on the massive pile of debt it took on to merge with Avast. So far, it has only reduced around $200m since March 31, 2023. The massive interest expense on it takes away the flexibility of capital that could be used to further the growth of the company, especially when operating income just barely covers interest expenses.

The company's efficiency and profitability need to improve also, especially when we look at GAAP margins. The most recent quarter's operating margins fell from 32.2% to 2.6% due to an increase in restructuring and litigation costs, which may not repeat, however, I need to know for sure when the company reports its next quarter, which is at the beginning of February.

FY24 seems to be a good year in terms of revenue growth, however, as you can see in the analysts’ estimates from the link above, the revenue growth slows down significantly. I would like to see the management’s outlook for the next year, to see if my lower revenue assumptions are justified.

It seems that the company had a decent rally since the end of October, where it was below my assigned fair value, however, with the shaky economic outlook still in play, I don’t think I’ve missed the boat yet. I will be setting a price alert at around $19 a share and follow how the company’s financials turn out in the following quarters.

For further details see:

Gen Digital: The Debt Post-Merger Is Worrying