GNK - Genco Hauls A Bulky Dividend

- Genco is a long-term turnaround story and dividend play.

- The company has laid out a value strategy to focus on deleveraging, cash flow and growth.

- This higher risk stock could provide investors with a boost to their income-producing portion of their portfolios.

I first read about Genco Shipping & Trading Limited ( GNK ) not too long ago and what caught my eye in the article was a comment about the company paying down its debt. Further on, the article mentioned that the company was increasing its dividend at the same time. Finally, the article addressed the company’s plans for investing in future growth. Normally, when something sounds too good to be true, it rarely is, especially when it comes to investing. Sure enough, though, after doing some digging, these three elements are the basis of the company’s comprehensive value strategy, which management laid out last year. These elements are the foundation upon which Genco is executing in order to build lasting shareholder value, in an industry that investors have seen capsize time and time again.

Genco is the largest U.S. based dry bulk shipowner , with a fleet of 44 ships transporting major and minor bulk around the world. Major bulk consists of iron ore and coal, and minor bulk includes grains, cement, fertilizers and other dry, loose items. The Company is somewhat unique in that while it is headquartered in New York, it is actually incorporated in the Marshall Islands (more on this later). The current fleet is comprised of 17 Capesize, 15 Ultramax and 12 Supramax dry bulk carriers with a total capacity of 4.6 million deadweight tons. The average age of the fleet is about 10 years. The company sells time charters, spot market voyage charters and spot market-related time charters. The composition of the fleet allows the company to take advantage of the upside potential of the iron ore trade, while harvesting more stable earnings via the minor bulk offerings.

Company Q2 Presentation

The first element in the value strategy is the company’s debt burden. Genco has come a long way since emerging from bankruptcy in 2014. At the end of the following year, the company had a Total Debt/Assets ratio of 0.34. By the end of the first quarter 2022, that ratio had declined to 0.16. In fact, since 2020, the company has reduced the debt burden by $250 million. Similarly, the company’s Total Debt/Equity ratio has declined from 0.52 in the post-bankruptcy years to 0.20 at the end of the latest quarter.

| 2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| Q122 |

| Total Debt/Assets |

| 0.34 |

| 0.33 |

| 0.34 |

| 0.33 |

| .032 |

| .036 |

| 0.20 |

| 0.16 |

| Total Debt () |

| 579.0 |

| 513.0 |

| 515.4 |

| 535.1 |

| 482.7 |

| 439.6 |

| 238.2 |

| 189.9 |

| Total Debt/Equity |

| 0.52 |

| 0.50 |

| 0.53 |

| 0.51 |

| 0.49 |

| 0.59 |

| 0.26 |

| 0.20 |

Source: sec.gov, Company filings

Management has recognized that a capital-intensive business such as shipping requires financial flexibility to navigate economic booms and busts amid a continual need to replace older ships with newer, more efficient ones. By reducing the company’s debt load, and renegotiating a more flexible line of credit, the company has positioned itself to have one of the best balance sheets in the industry. As a comparison, competitor Eagle Bulk Shipping ( EGLE ) had a Total Debt/Assets ratio of 0.33 at the end of the latest quarter. Management has expressed a long-term desire to achieve a zero net debt position. To get there, they have pledged to make regular, voluntary debt repayments, assuming a stable cash flow continues to exist. Obviously, management must maintain this financial discipline to achieve this goal and the other goals of the value strategy. By doing so, this will help to differentiate Genco from its peers.

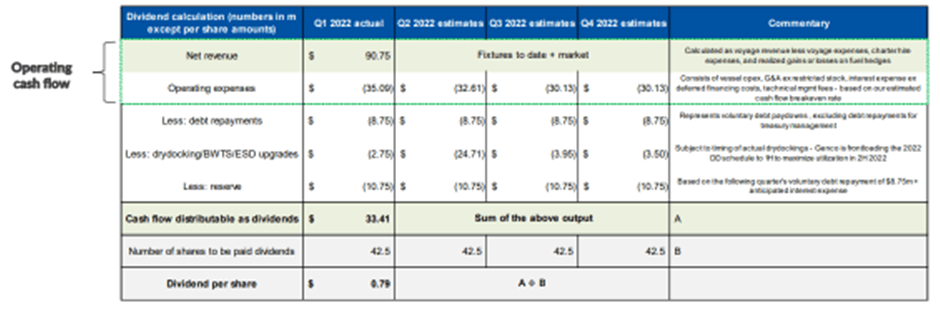

Simultaneously, the company has developed a plan for more stable and predictable dividend payments. The company has been paying dividends since 2019. However, there did not seem to be any strategy or plan about how much and when. It was difficult then as the company was dealing with a much higher debt burden and perpetual losses. But with the implementation of the value strategy, the company has created a dividend framework based on operating cash flow results, voluntary debt payments, certain capital expenditures and reserves. Basically, they have created a budget and they have become very transparent with their objectives. After the first quarter the company laid out the framework for the remainder of 2022:

{kind=link}

They have not filled in all of the blanks, but they have provided quite a bit. Based on this information and the first quarter results, I have estimated a full year dividend of about $3.29 per share. That is slightly higher than the annualized Q1 dividend, but the first quarter is typically one of their weaker quarters, the company’s strong first quarter results this year notwithstanding.

To closely tie the dividend payment to available cash flow is smart. It may lead to fluctuations in the dividend payment, but at least there is a basis for it. The company should not be stuck committing to a particular payout or yield when business slows down. Investors may not like the variability in the dividend payout, but the company is being transparent. Furthermore, CEO John Wobensmith said on the Q1 earnings call that they would like to see the stock yielding in the 8% to 10% range.

With an estimated annualized dividend of $3.29, the current yield on the stock is 16.8% at a recent price of $19.66. A yield of 8% to 10% would put the price between $33 and $41, which is a solid increase from current levels. If the company can achieve that, I think investors would be happy with both the income and the capital appreciation. A look at the most recent price is below:

The final leg of the value strategy pertains to the company’s growth proposition. Over the short and medium term, the company seems content in harvesting older ships which still have value to upgrade to new, more efficient ships. Technology is improving in the shipping industry to allow companies to monitor fuel usage, route efficiency and environmental impacts. The company has a proven strategy for disposing of older ships in favor of these new models. This leads to a reduction in operating expenses, as well as a return on capital when the ship is sold or disposed. By strategically expanding the makeup of the fleet, the company can take advantage of global trade trends more quickly to maximize operating performance.

Another example of management thinking more strategically is the JV with GS Shipmanagement Pte. Ltd. The 50/50 JV was formed to provide technical ship management services to the company. Technical management fees decreased 37% in the latest quarter from a year earlier. This is a direct improvement to the company’s bottom line. Steps like these should help keep the company at the top of the industry and ultimately lead to increasing shareholder value. Over the longer term, if the company can achieve the desired financial results, and management feels the stock is trading at a premium to the company’s NAV, then there could be a reason to use the shares to make an acquisition.

The early results of this new value strategy are favorable. In 2021, revenues increased 54% over 2020 revenues to $547.1 million.

The strong growth continued through the first quarter of 2022 as the company posted revenue growth of 56% over the year ago period. Operating profits, which were nonexistent prior to 2021, were $201.1 million in 2021, compared to an operating loss of $203 million in 2020. In the first quarter of 2022, operating profits were $42.1 million compared to just $6.3 million in the first quarter of 2021.

Global trade has shown signs of steady improvement since the worst of the pandemic appears to be in the past. However, supply chain issues are still abundant and the war in Ukraine has caused disruptions in the grain markets. Even so, management seems to be optimistic for positive results leading into Q2 and the second half of the year.

A word about the company’s status. As mentioned earlier, the company is incorporated in the Republic of the Marshall Islands. While a U.S. territory, the company noted that the Marshall Islands does not have a well-developed body of corporate law, and it may make it difficult for shareholders to protect their interests. Furthermore, the company qualifies for the Section 883 exemption of the U.S. tax code. As such, it generally does not pay federal income taxes. There are certain exceptions to this exemption for both the company and its investors, and investors would be wise to consult a tax advisor to determine if this is an appropriate investment. These points are important as the stock may not be suitable for all investors.

I think Genco is an interesting story. The company has gone through challenging times in the past, but the message out of management last year regarding the value strategy going forward appears promising. The stock is yielding a ton right now, but long-term management would like to see an 8% to 10% yield, which is still great. Investors could find some volatility in that number with the ups and downs of global trade and shipping. Given modest growth assumptions, a slightly improving profit line and stable dividends, I have modeled a scenario in which the value of the company increases to the low $30/share range. As mentioned earlier, that would put the stock in the ballpark of management’s yield expectations.

The company and stock are not without above-average risk. There could be some bumpy quarters ahead, particularly if global growth shows more signs of slowing down, higher inflation sticks around or the war in Ukraine continues to drag on. That being said, for investors seeking higher income with additional risk, I think this is a cautious buy. Investors should understand that with a company like this in a historically volatile industry, they should keep a very close watch on developments or appropriately size the investment in the portfolio to minimize the risk. This may not be for everyone, but for those who want to see a transparent management action plan unfold in front of them, they could be in for an exciting voyage.

For further details see:

Genco Hauls A Bulky Dividend