GNK - Genco Shipping: A Quality Company With Excellent Financials And Attractive Dividend Yields

2024-01-08 21:17:25 ET

Summary

- Genco Shipping has the best balance sheet among similar-sized bulk carrier companies, with a strong liquidity position and low total debt-to-equity ratio.

- The company's fleet composition follows a barbell strategy, with a mix of Capesize and Ultra/Panamax vessels, providing advantages during different parts of the shipping cycle.

- Despite disappointing 3Q23 figures, GNK has been generating positive free cash flow and paying dividends for 17 consecutive quarters.

- GNK trades at lower multiples than its historical figures. However, it is among the more expensive in its peer group. Given all the arguments, I give GNK a buy rating.

Introduction

Genco Shipping ( GNK ) has the best balance sheet compared to similar-sized bulk carrier companies. The company has a 0.33 cash-to-total debt ratio, 15% total debt to equity, and 16% total liabilities to total assets. The GNK fleet comprises 18 Capesize vessels and 27 Ultramax and Panamax vessels. The average age of the fleet is 11.7 years. GNK trades at lower multiples than its historical figures. However, it is among the more expensive in its peer group. The company has been distributing dividends for 17 quarters. The dividend with yield is 5.62% ((TTM)). I give GNK a buy rating.

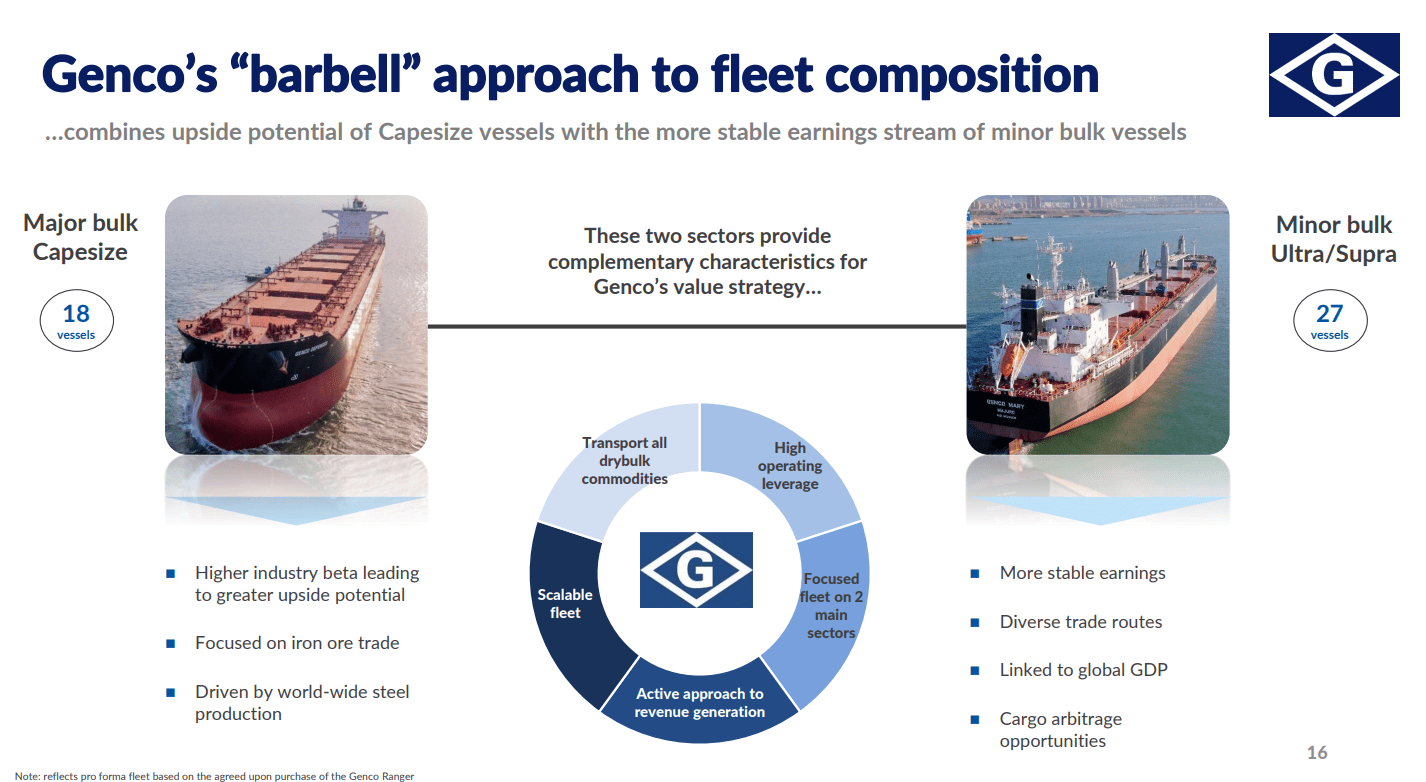

GNK fleet overview

GNK has 45 ships with an average age of 11.7 years. The company follows the barbell approach, as stated in its presentation .

{kind=link}

GNK has 18 Capesize vessels and 27 Ultra and Supramax vessels. Both categories have their pros and cons. Capesize ships have a higher beta to shipping industry changes. There is demand, which is primarily a function of iron ore demand. In other words, it depends on global steel production changes. Conversely, minor bulk carriers like Ultramax and Panamax have relatively stable earnings compared to Capesize vessels and navigate in diverse trade routes (usually regional voyages).

The demand for Utramax and Panamax vessels depends on more variables due to their purpose of carrying various cargoes. Unlike the Capesize ships, they do not carry mainly iron ore and metallurgical coal. They transport agricultural products, thermal coal, and minor bulks (cement, steel, fertilizers, pet coke).

GNK is focused on time charters. Capesize vessels are operated under 11-14 months long contracts, Ultramax under 5-7 months contracts, and Panamax under 4-6 months. I like such an approach because it distributes the contract durations across time. It is similar to creating a fixed-income securities portfolio with various maturities and interest rates. GNK can play the “yield curve” of the shipping cycle, shifting between contract durations based on the day rates.

In November 2023, GNK announced its fleet renewal strategy . In 2023, the company acquired two Capesize vessels with scrubbers: MV Ranger and MV Reliance. The purchase price of MV Reliance is $43 million. It will be financed by the company's own cash and revolving credit facility. In the press release, the GNK also announced its plans to sell one of its older ships, MV Commodus. She is a Capesize vessel built in 2009. The expected price of the ship is $19.5 million.

GNK fleet has 17 vessels equipped with scrubbers, which is 37% of the fleet. The scrubbers are installed mainly on the Capesize vessels. They consume more fuel, stay longer at sea, and bunker in main ports.

GNK reported 3Q23 97.7% utilization of its fleet, higher by one basis point over 3Q22. The day rates declined almost 50% QoQ from $23,624 3Q23 to $12,082 3Q23. However, GNK announced that 69% of 4Q23 days are fixed at $16,700.

GNK balance sheet

In the introduction, I stated that GNK has the best balance among mid-size bulk carrier companies. Now, it’s time to share my arguments.

Let`s start weighing up GNK against its peers:

- Genco Shipping $48 million cash; $141 million total debt; 0.33 cash to total debt ratio, total debt to equity 15%

- Safe Bulkers ( SB ) $74 million cash; $440 million total debt; 0.17 cash to total debt ratio, total debt to equity 57%

- Pangaea Logistics ( PANL ) $87 million cash; $275 million total debt; 0.31 cash to total debt ratio, total debt to equity 73%

- Diana Shipping ( DSX ) $173 million cash; $657 million total debt; 0.26 cash to total debt ratio, total debt to equity 135%

- Grindrod Shipping ( GRIN ) $71 million cash; $168 million total debt; 0.42 cash to total debt ratio, total debt to equity 60%

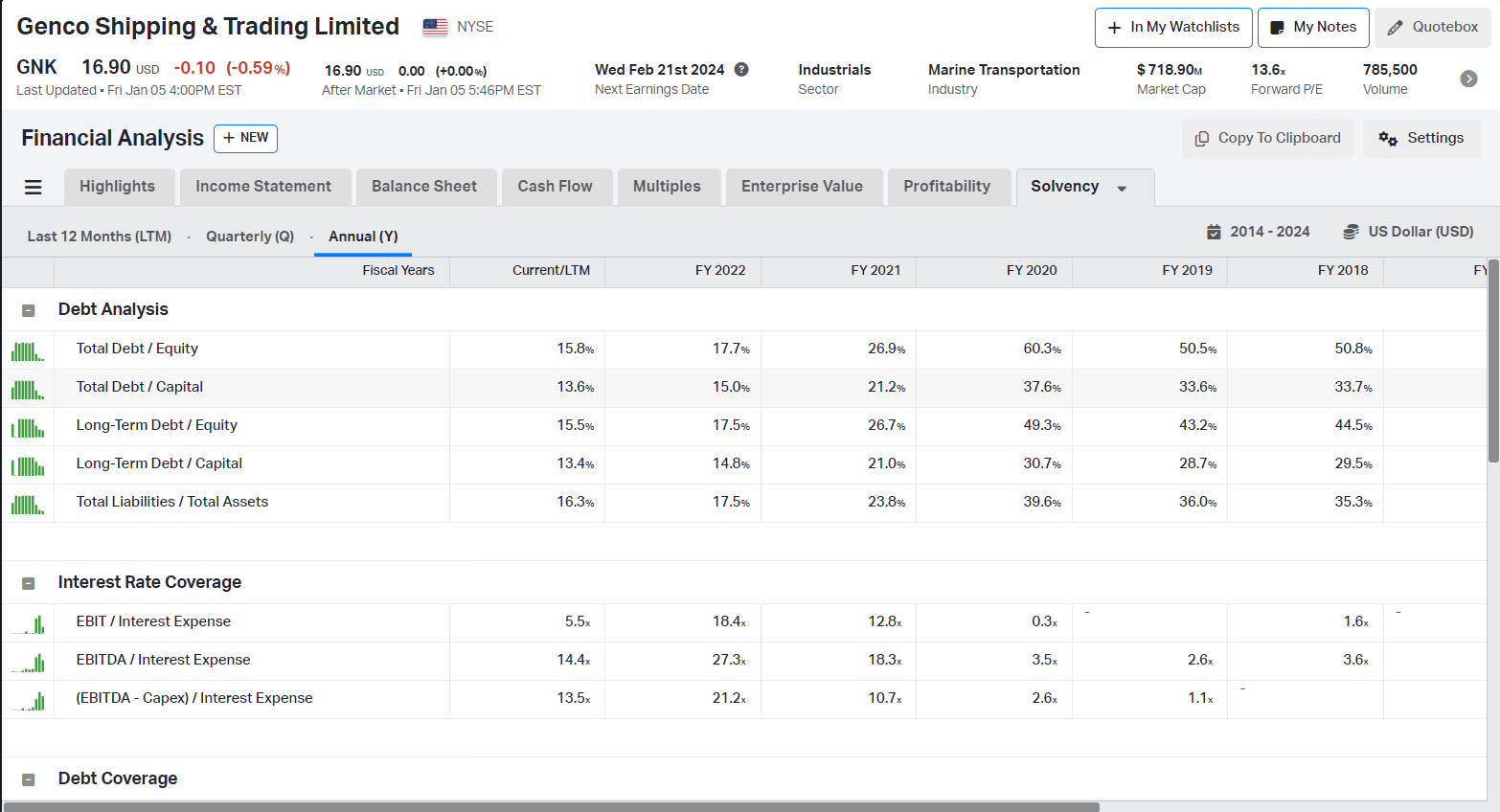

GNK leads the pack with the lowest total debt-to-equity ratio. The company has a strong liquidity position with a 0.33 cash-to-total debt ratio. GNK has a high margin of safety, considering the total debt/fleet scrap value ratio at 40%.

GNK has made solid progress over the years, reducing its debt burden, as seen in the table below.

{kind=link}

From 2020, the company has cut its debts by 68% while maintaining an adequate dividend policy and capital investments. Currently, GNK has $144 million total debt and $48 million cash.

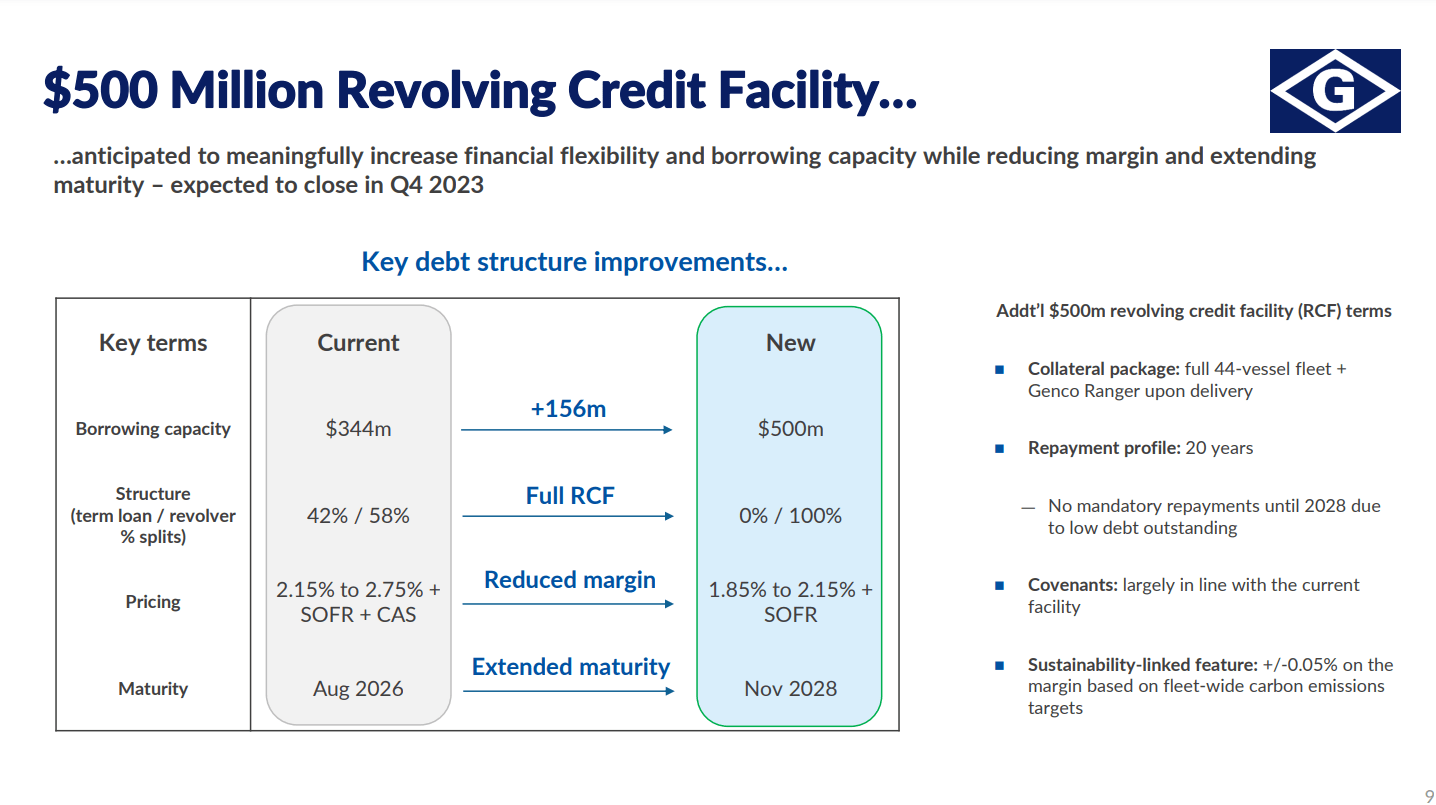

In November 2023, GNK made another important announcement . The company signed for a new $500 million revolving credit facility.

{kind=link}

In my opinion, the new credit facility puts GNK in pole position at the right time. We are in the middle of the bull shipping cycle with multiple catalysts, and having access to liquidity is an enormous advantage.

As seen in the table above, the loan terms are much better. There are three points I would like to address. First are the interest rates: 1.85% (for the term loan) and 2.15% (for the revolver) + SOFR is a good deal. The second point is the extended maturity till November 2028. At that point, the first payments must be made. However, the repayment profile is 20 years. Last, the borrowing capacity increased by 50% to $500 million. The collateral for the credit facility is the GNK fleet.

GNK profitability

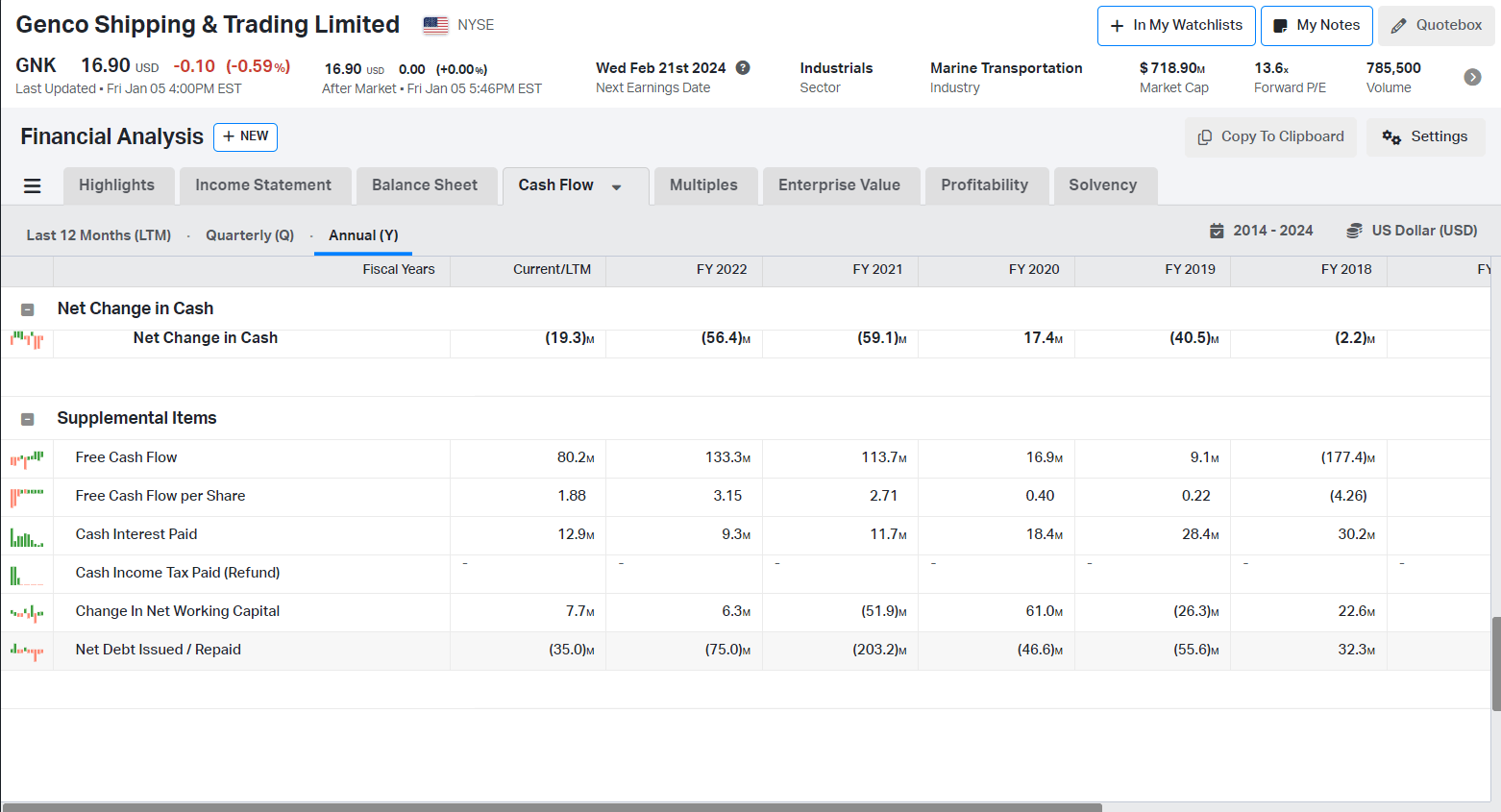

The 3Q23 report disappointed investors with negative net income and EBITDA. The primary reason for the disappointing results was the lower day rates. However, the situation is not as bad as it seems when looking at the bigger picture. The table below shows GNK's free cash flow over the last five years.

{kind=link}

For three quarters in 2023, GNK generated $80.2 million FCF. Given the lower day rates in the first three quarters of 2023, I consider that for success.

In the list below, I compare GNK's profitability metrics against its peers:

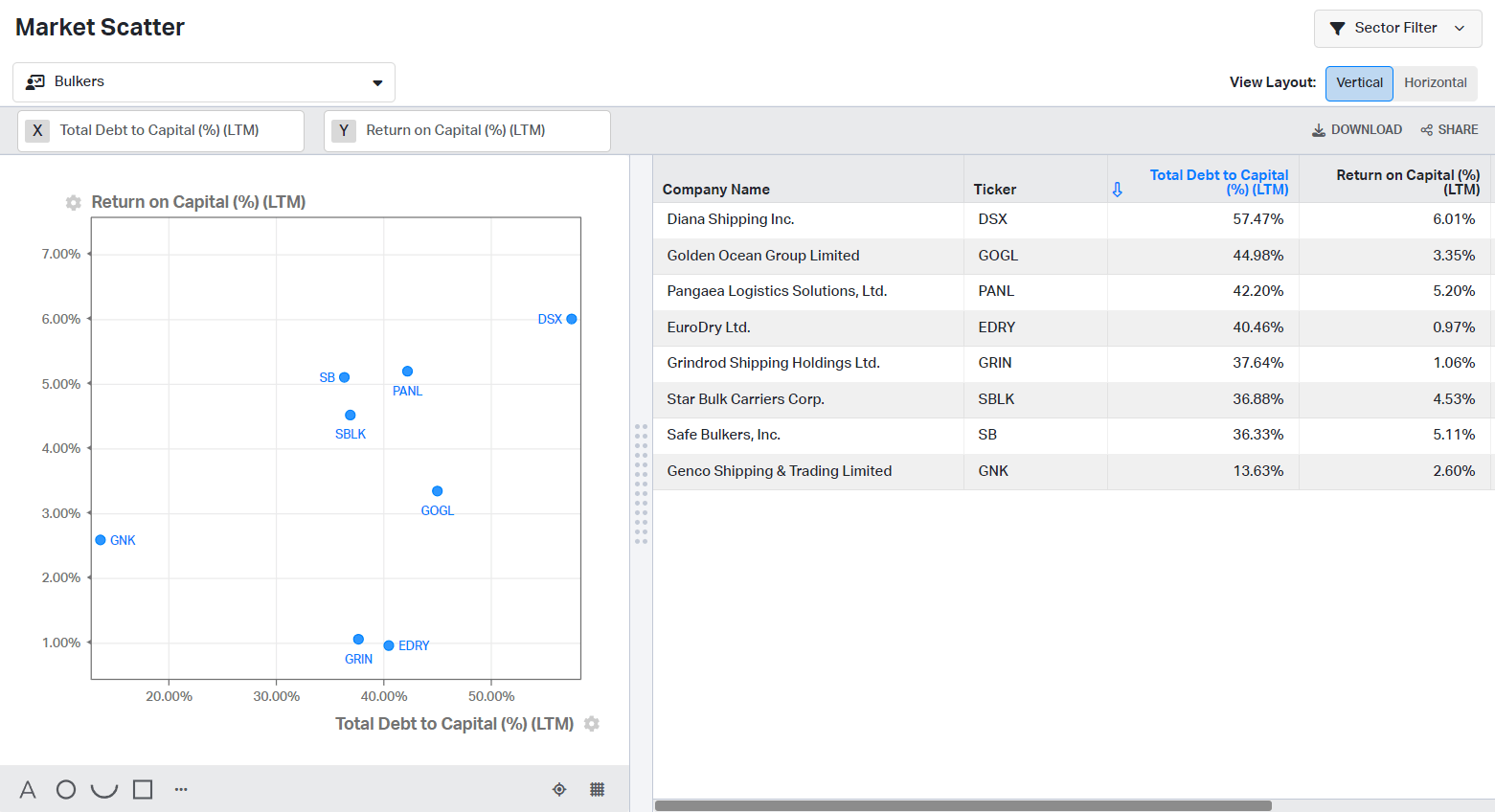

- Genco Shipping 5% gross margin, 26.3% EBITDA margin, 1.2% ROE, 3.71% ROTC

- Safe Bulkers 62% gross margin, 52% EBITDA margin, 11.1% ROE, 5.1% ROTC

- Pangaea Logistics 21% gross margin, 17% EBITDA margin, 11.4% ROE, 5.2% ROTC

- Diana Shipping 65% gross margin, 49% EBITDA margin, 14.4% ROE, 6.0% ROTC

- Grindrod Shipping 29% gross margin, 7.8% EBITDA margin, (3.5)% ROE, 1.0% ROTC

In the last disappointing quarter, I squeezed GNK margins and returns. From the group above, I consider SB and DSX direct competitors, given their fleet size and type of vessels. GNK has the oldest ships; however, more than a third have fitted scrubbers, while DSX has zero. SB excels with its higher percentage of scrubber-equipped vessels and lower average age.

GNK cash breakeven at $8,073; every $1000 increase in TC day rates means $16 million added to the annual EBITDA. If Capesize day rates grow by $5000/day, GNK annualized EBITDA will increase by $31 million. With the rising day rates due to Panama Canal limitation and the Red Sea crisis, I expect GNK will catch up in 4Q23 and 1Q24. Company margins and returns will improve significantly.

The table below compares bulk carrier companies by ROTC and total debt to total capital ratio.

{kind=link}

Dividing ROTC by TD/TC measures how prudently the managers invest the company`s capital. GNK leads at 20%.

The company has been distributing dividends for 17 quarters. The dividend with yield is 5.62% ((TTM)). As pointed out earlier, GNK has generated free cash flow for the last few years. I believe GNK will keep paying dividends in the foreseeable future, given GNK`s ability to generate free cash flow and rosing day rates.

GNK Valuation

First, I will compare GNK against the same companies from previous chapters:

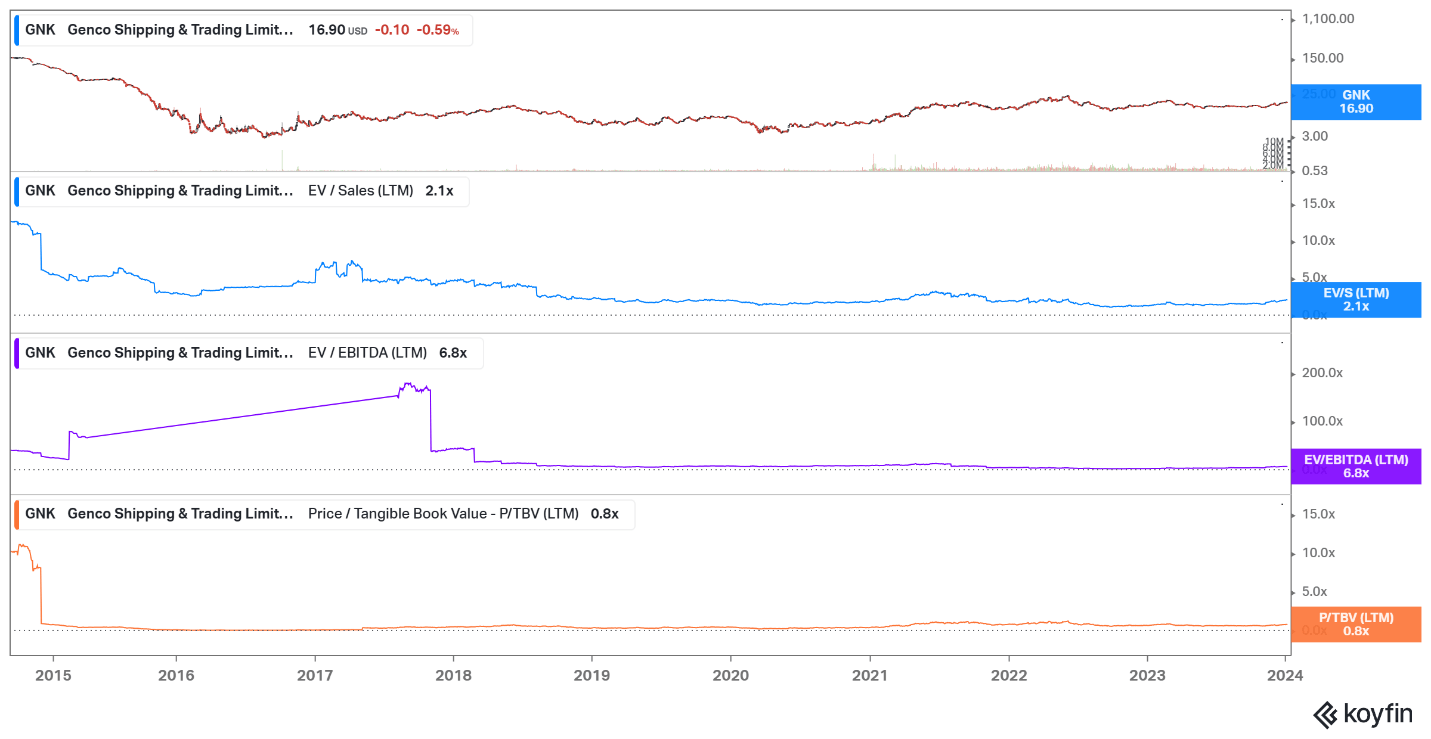

- Genco Shipping 1.99 EV/Sales, 7.56 EV/EBITDA, 1.02 P/BV

- Safe Bulkers 2.8 EV/Sales, 5.38 EV/EBITDA, 0.57 P/BV

- Pangaea Logistics 1.22 Ev/Sales, 7.15 EV/EBITDA, 1.12 P/BV

- Diana Shipping 2.83 EV/Sales, 5.72 EV/EBITDA, 0.62 P/BV

- Grindrod Shipping 0.73 EV/Sales, 9.34 EV/EBITDA, 0.57 P/BV

GNK trades at the second-highest EV/EBITDA and P/TBV. Considering EV/EBITDA, GNK holds a mid-position in its peer group.

The table below shows SB multiples over the last ten years.

{kind=link}

GNK is deeply undervalued compared to its 10Y peaks (12.6 EV/Sales, 159 EV/EBITDA, P/BV). Conversely, the company trades close to its 5Y average multiples (1.82 EV/Sales, 7.11 EV/EBITDA, 1.03 P/BV).

GNK trades below its peak multiples. I expect the day rates to increase in the coming 6-12 months due to multiple reasons discussed in my DSX article. Simply put, there is still a place for appreciation.

Risks

Capesize vessels transport primarily iron ore and cocking (metallurgical) coal. That means more than 50% of GNK revenue depends on the global steel demand. The two largest economies and consumers of steel are China and the US. The health of their economies predetermines the global steel demand. 2024 is the year of the Dragon in China. I expect the fiscal stimulus for the Chinese economy to get traction, boosting steel demand.

In the US, it is an election year. Democrats must lure the population (or at least keep them away from the Republicans). Being prudent with fiscal spending is not among the proven strategies to achieve that goal. Simply put, I expect gov spending to keep growing, artificially accelerating the economy. That means growing steel demand. Rising steel demand means more iron ore has to be shipped across the globe. Hence, more bulk carriers will be needed.

The trump card is the geopolitical risk, which benefits most shipping companies. The big winners are containers, followed by crude and product tankers. Bulk carriers follow different routes, often bypassing the present hot spot, the Red Sea. However, the drought in the Panama Canal has a significant impact on bulkers.

Investors takeaway

GNK is a top bulk carrier company. Despite the disappointing 3Q23 figures, there are multiple reasons I like GNK. GNK fleet composition follows the barbell strategy, having 18 Capesize vessels and 27 Ultra/Panamax vessels. Both sides of the bar have their advantages during different parts of the shipping cycle. 37% of GNK ships are equipped with scrubbers. The company has the most conservative balance sheet, with 15% total debt to equity. Has been generating positive FCF over the last few years and paid dividends for 17 consecutive quarters. GNK trades at lower multiples than its historical figures. However, it is among the more expensive in its peer group. Given all the arguments, I give GNK a buy rating.

For further details see:

Genco Shipping: A Quality Company With Excellent Financials And Attractive Dividend Yields