GNK - Genco Shipping: Playing The Supply-Demand Imbalances

2023-04-08 03:42:59 ET

Summary

- Genco Shipping owns a modern fleet of dry cargo vessels consisting of 27 Capesize and 17 Ultramax/Supramax vessels.

- I believe GNK stock has a fairly stable margin of safety, supported by the low order book and rising demand for dry bulk shipping services from emerging markets.

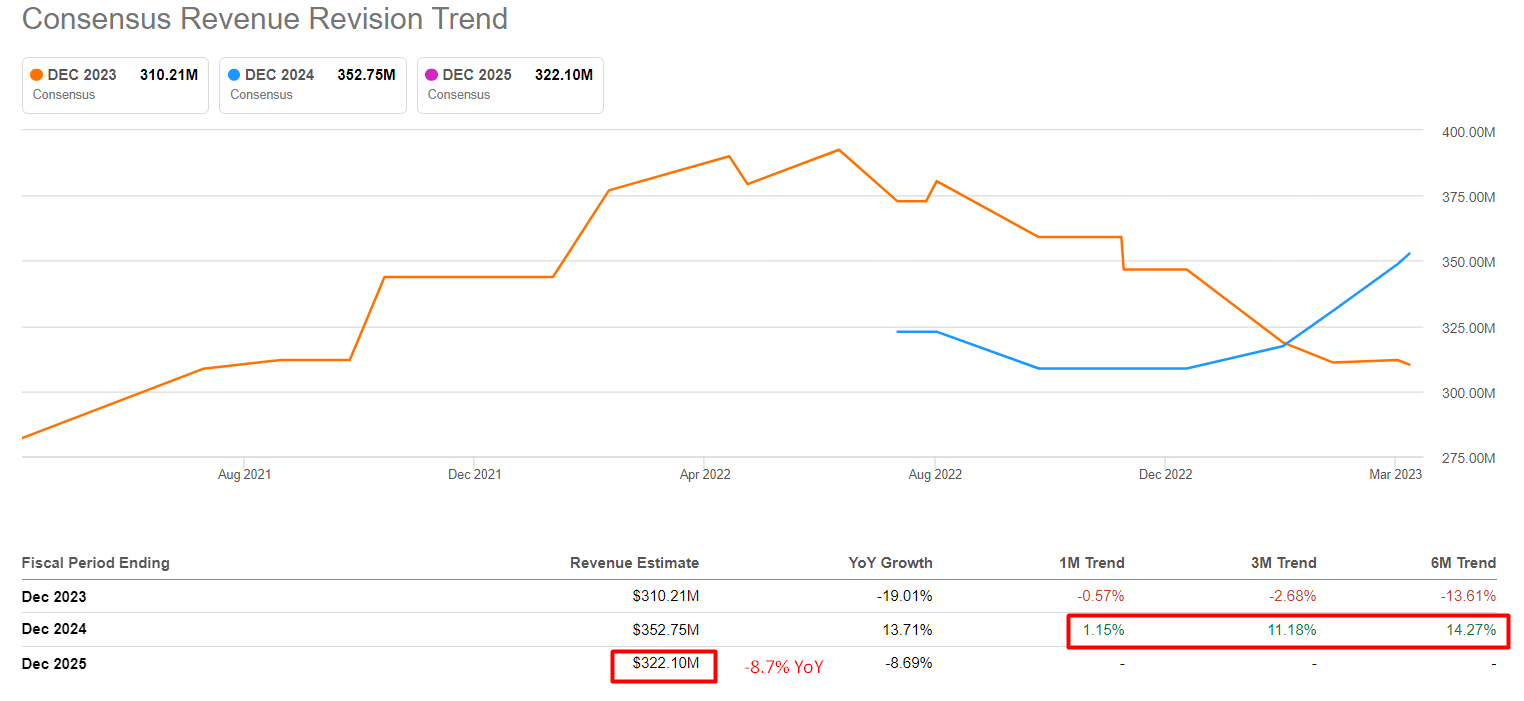

- In the last 3 months, EPS consensus for FY2024 has increased by more than 11%, while FY2025 is set to fall by 8.7% YoY - and this is amid a falling order book.

- I see Genco to remain a reliable and cheap dividend payer, despite lower operating days and declining TCE rates in FY2023.

Instead of an investment thesis

I have been writing about bulk carriers here on Seeking Alpha for a long time, but for reasons unknown to me I have passed over Genco Shipping & Trading Limited ( GNK ), incidentally one of the largest companies in its sub-industry .

I believe GNK stock has a fairly stable margin of safety, supported by the low order book and rising demand for dry bulk shipping services from emerging markets [especially China]. Therefore, despite the decline in freight rates, which are now starting to recover, the dividend policy looks good and should reward investors as they wait for the next upward move in the industry's cycle.

My reasoning

Genco Shipping & Trading LTD is a $625-million market cap Greek company that provides shipping and logistics services. Its fleet of vessels transports dry bulk cargo, such as coal, iron ore, and grain. The company was established in 2006 and has since grown to offer vessel management, chartering, and brokerage services.

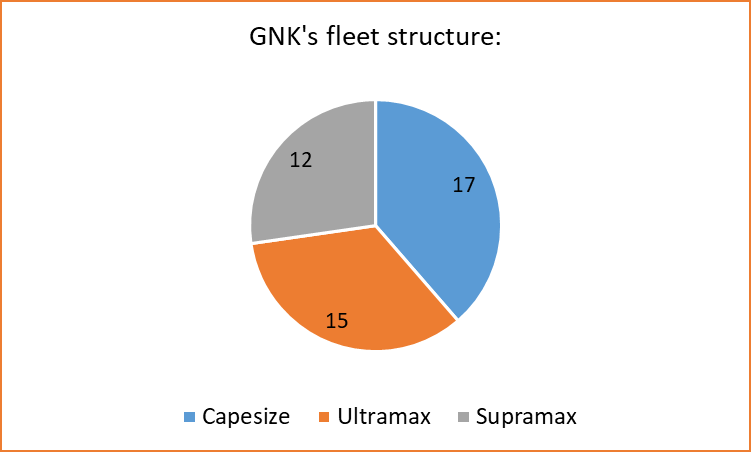

The company owns a modern fleet of dry cargo vessels consisting of 27 Capesize and 17 Ultramax/Supramax vessels, which are relatively well distributed with an average age of about 12 years:

Author's work, GNK's fleet structure

{kind=link}

According to the latest earnings call , the company had a strong financial year in 2022, generating EBITDA of $227 million, driven by fleet-wide TCE of $23,824 per day, which outperformed scrubber-adjusted benchmarks by almost $3,000 per day. The company's commercial platform alone added $44 million to the bottom line. In FY2022, Genco continued to execute its strategy of becoming a low-leverage, high-dividend payout company, resulting in declared dividends of $2.57 per share for the full year, representing a dividend yield of 14%. In the fourth quarter, the company declared a dividend of $0.50 per share, marking its 14th consecutive quarterly dividend.

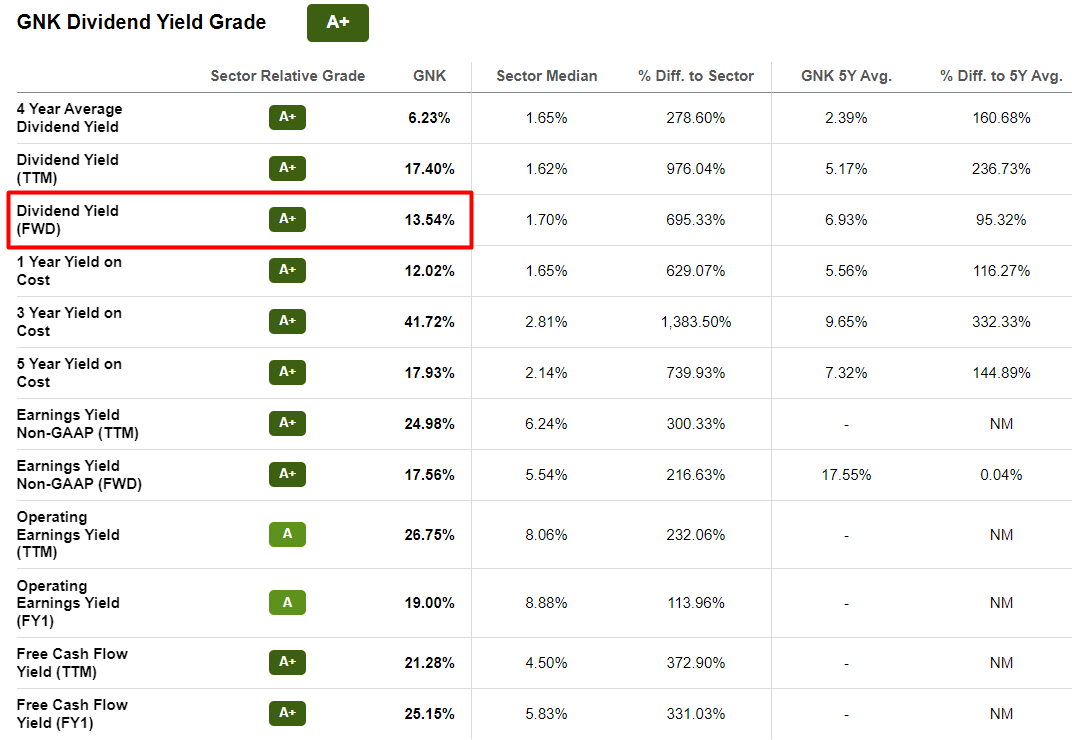

Right now, if you open up Genco's profile on Seeking Alpha, you'll see that it has a forwarding dividend yield of around 13.5%, which seems to be huge:

Seeking Alpha, GNK, author's notes

{kind=link}

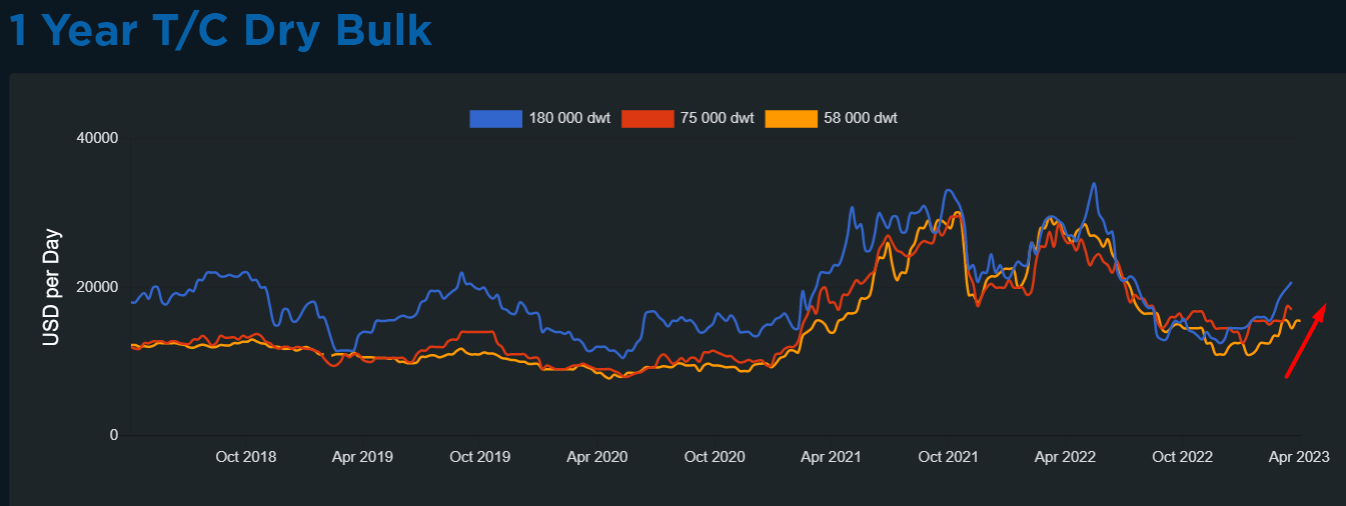

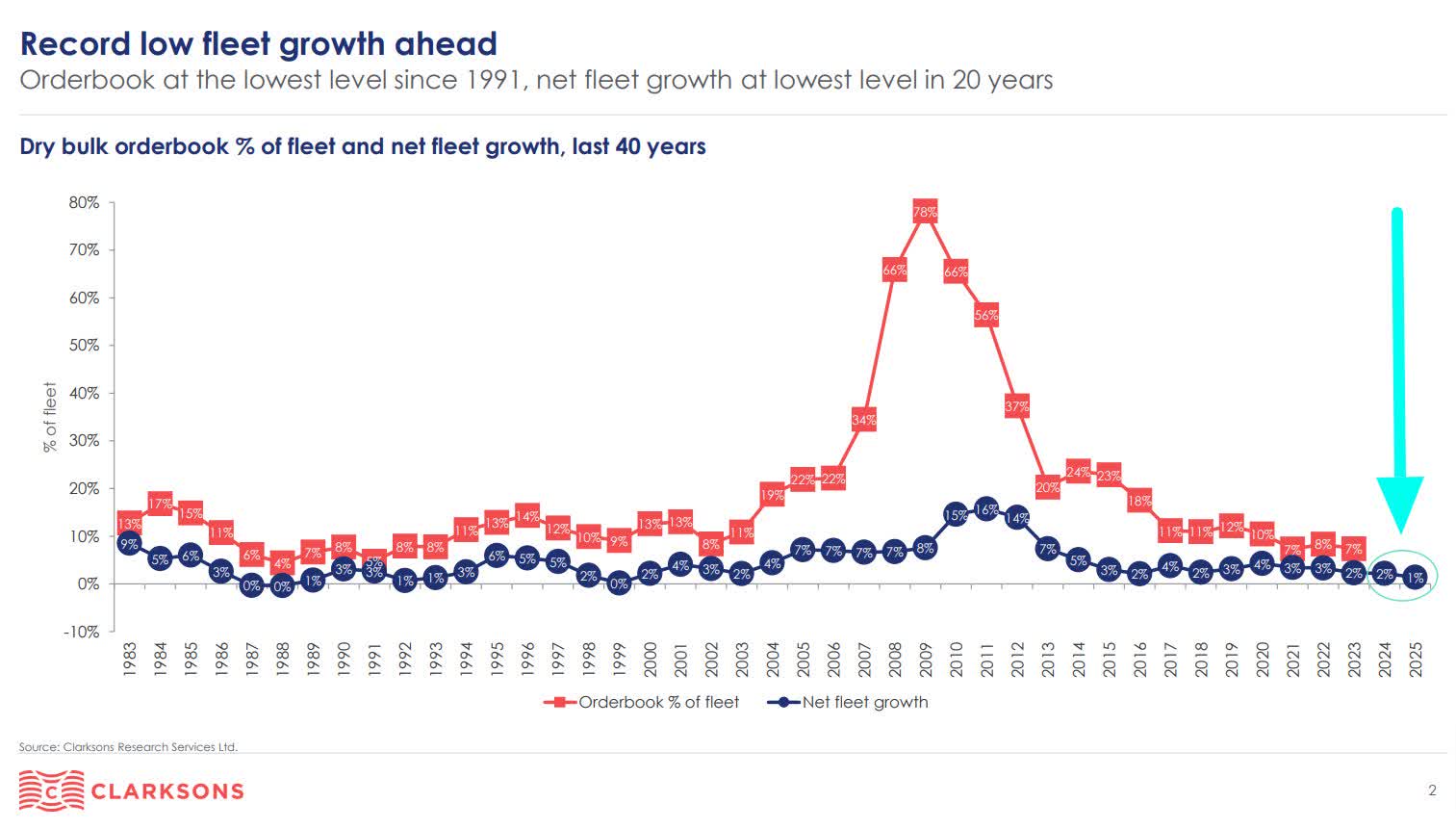

Looking ahead, Genco management sees several catalysts that could support the dry bulk market, including the reopening of China, further stimulus measures, tightness in the global energy market, and rerouting of coal cargo flows due to the Russian war in Ukraine. These factors should primarily benefit Capesize rates, while the South American grain season should provide higher bulk yields as Q1 ends and Q2 begins. In addition, the Black Sea Grain Initiative agreement, under which over 22 million tons of grain have been exported since its inception, expires in less than a month, and Ukrainian grain exports are expected to decline by about 30% in the current marketing year. The Ukrainian grain season usually peaks in Q3, but currently, exports are light with 2 to 3 million tons per month. January was particularly slow due to Russia possibly delaying vessel inspections. The management hopes the grain deal will be extended for longer than 120 days, potentially up to a year. The lack of investment in new coal mines has led to rerouting and ton-mile demand, which has been positive. I was able to find a chart that shows what the tonnage mile situation looks like right now - this is one of the most bullish charts for dry bulk shippers that I have seen in the last few weeks:

Twitter: @brajakica

Demand for dry bulk freight services is beginning to rebound as emerging markets - particularly China - recover from COVID-19 constraints.

Fearnpulse.com, author's notes

{kind=link}

China's reopening and infrastructure spending should benefit Capesizes and positively impact the iron ore trade. The company's executives expect demand for Capesize vessels to increase as iron ore prices rise, which is still far from reality as I'm writing these lines - what happens to the freight rates when iron ore prices finally take off?

Genco has a cash flow breakeven rate of approximately $9,500 per day - way lower than their TCE rates. Of course, investors should be ready for drydocking's effect on earnings and dividends in Q1 2023. Drydocking is a process where a vessel is taken out of service and brought to a dry dock for maintenance and repairs. The frequency of drydocking is typically determined by international regulations, which require vessels to undergo inspections and repairs regularly to ensure their safety and compliance with environmental standards. One also needs to understand that the company contracts the lion's share of its revenue at spot rates, which means that the drawdown in TCE rates in late 2022 should be felt in Q1 2023. On the other hand, a lower CAPEX number for FY2023 is significantly lower than last year, which is obviously, lowering the company's breakeven and giving more room for dividends as a whole.

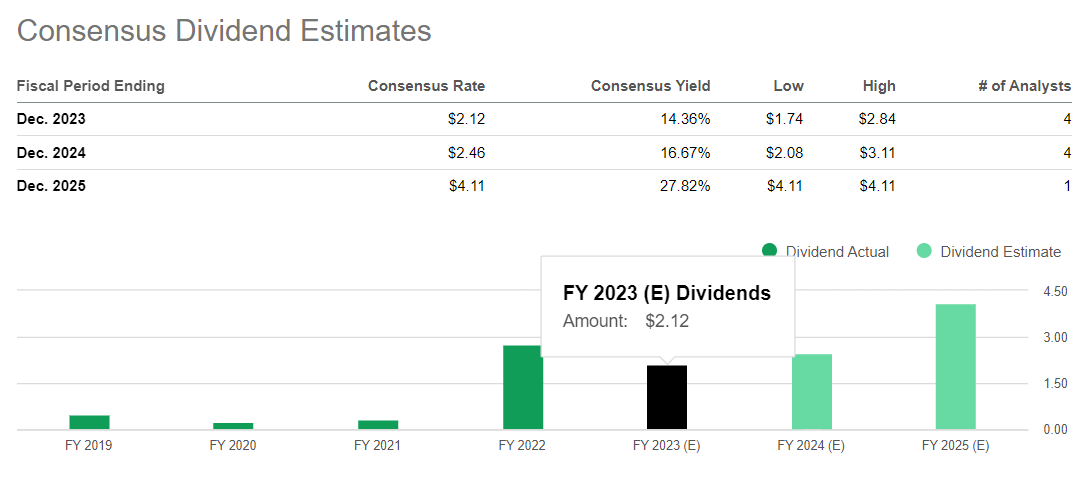

So Q1 2023 may not be the best quarter for those looking for good dividends - but longer term I think Seeking Alpha's consensus FY2023 dividend of $2.24 per share is not far from the truth.

Seeking Alpha, GNK, Dividend Estimates

{kind=link}

If we disregard demand and look at the supply side, dry bulk carriers in general - and Genco Shipping in particular - have something to offer investors as well.

In case you don't know exactly what an order book in shipping is - it is a record of all ship orders received by shipyards from customers for future deliveries, essentially a list of ships being built and expected to be delivered. The order book is critical for monitoring the balance between supply and demand in the shipping market. A high order book level can lead to oversupply, where too many ships are available for too little freight demand, resulting in lower freight rates and profitability. Conversely, a low order backlog indicates tight supply, which can lead to higher freight rates and greater profitability. Therefore, the order book is an essential indicator for shipping companies and investors to keep an eye on, as it offers valuable insights into the future of the shipping market.

Today, the dry bulk order book is standing at the lowest multiyear levels, creating a favorable environment for dry bulkers with a relatively young fleet.

Clarksons data, provided by E. Finley-Richardson

{kind=link}

Overall, I think the macroeconomic environment is very positive for the dry bulk shipping industry as a whole as we head into 2H 2023 and FY 2024. GNK's management approach, which focuses on dividend yield, deleveraging, and growth, should allow the company to remain relatively stable and continue to reward investors while they wait to see how the shortage of vessels affects rates - supply constraints typically lead to more elasticity; so GNK, which is focused on spot rates, should get a strong tailwind once this catalyst kicks in.

The company is currently valued at only 5.7 times P/E and 4.14 times EV/EBITDA [also FWD]. In the last 3 months, EPS consensus for FY2024 has increased by more than 11%, while FY2025 is still expected to decline by 8.7% YoY - and this is against the backdrop of a deteriorating order book [see chart above].

Seeking Alpha data, author's notes

{kind=link}

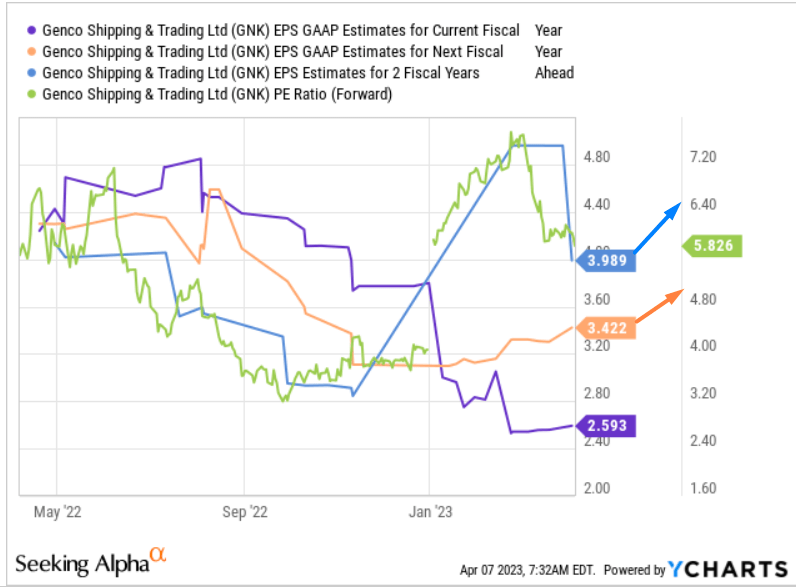

I expect EPS forecasts to gradually increase, making the company's valuation unbearably low.

{kind=link}

Maintaining dividends amid expected continued growth in TCE rates should hold most income-seeking investors and provide some protection to buyers at current price levels.

Closing thoughts

Investing in Genco Shipping shares involves certain risks that investors should consider. Shipping stocks are highly volatile and can be affected by fluctuations in the global economy, geopolitical risks, and other factors. The shipping industry is highly competitive and cyclical, making stocks susceptible to fluctuations. The shipping industry is also subject to various regulations relating to safety, environmental protection, and other factors that everyone should consider.

In any case, I think GNK looks quite attractive even compared to other companies. Even if the number of operating days in FY2023 is lower and average TCE rates decline year-on-year - which is already the case - the company will not lose its status as a fairly reliable and cheap dividend payer.

For further details see:

Genco Shipping: Playing The Supply-Demand Imbalances