GENC - Gencor Industries: Not A Buy After The Recent Outperformance

2023-04-18 03:25:48 ET

Summary

- The funding for highway programs under the Infrastructure Investment and Jobs Act funding should benefit Gencor Industries' revenue growth.

- The margins should benefit from declining steel prices and increase in volumes.

- Not a buy at current levels.

Gencor Industries ( GENC ) manufactures heavy machinery used in the production of highway construction equipment and materials and environmental control equipment. The company designs, manufactures, and sells machinery and related equipment used primarily for the production of asphalt and highway construction equipment and materials. The company's core products include asphalt pavers, hot mix asphalt plants, combustion systems, and fluid heat transfer systems.

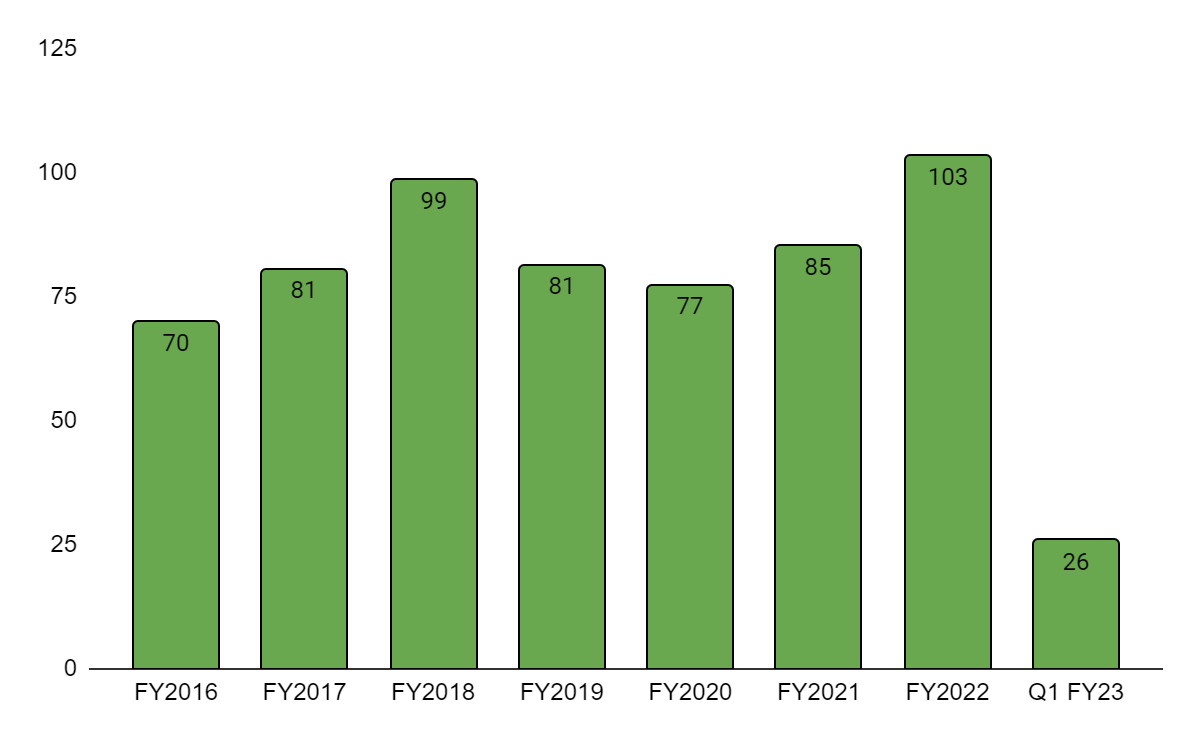

Revenue chart (Created by DzD Analysis using data from GENC)

{kind=link}

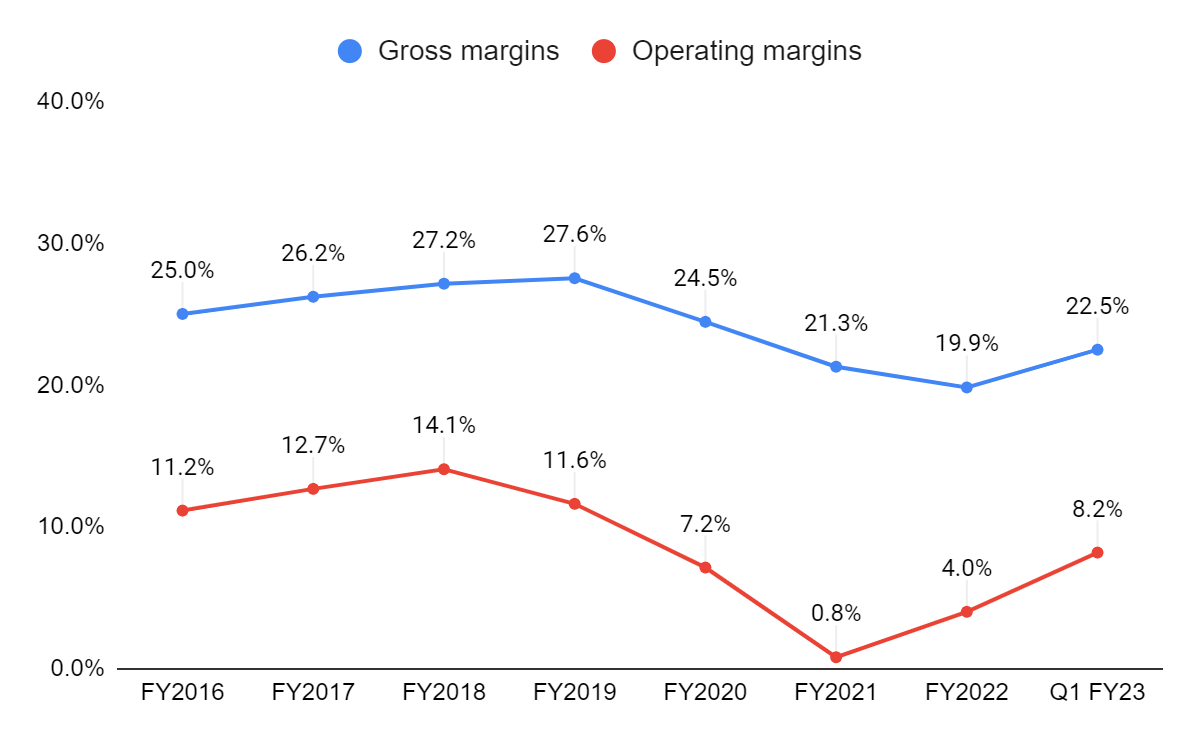

GENC's stock jumped approximately 10% post-Q1 FY23 earnings release in February and is up approximately 40% since then. The company reported a 28.4% Y/Y increase and a 12% sequential increase in revenue in the quarter due to higher equipment and parts sales. The gross margins had been below pre-covid levels in FY21 and 1H FY22 due to higher manufacturing costs associated with wages, steel, and purchased parts. However, over the last few quarters, the company's gross margins have improved due to the increased production volume and favorable price realization. SG&A expenses increased in FY21 and 1H FY22 due to the increased headcount and engineering wages related to the Blaw-Know paver product line. However, the company is reducing its headcount, which has led to lower professional expenses over the last three quarters. This is helping the company bring its operating margins back to their pre-Covid levels of 12%.

GENC's margins chart (Created by DzD Analysis using data from GENC)

{kind=link}

Looking ahead, the company's revenue should be driven by the healthy order backlog and state and federal funding. GENC had an order backlog of $42.5 million at the end of Q1 FY23. The principal factors driving demand for the company's products are federal and state funding for domestic highway construction and repair, the replacement of existing plants, and a trend towards efficient, larger plants. The company should benefit from the $550 billion in federal funding under the Infrastructure Investment and Jobs Act (IIJA) for roads and bridges, water infrastructure, broadband, and environmental remediation. Approximately $350.8 billion is for highway programs, which are expected to run until FY26.

Apart from organic growth, I believe GENC's revenue should also be driven through acquisitions. Gencor acquired Blaw Knox, its first company after a decade, in July 2020 to enter the hot mix paver segment. The company has zero debt on its balance sheet, with approximately $6 million in cash on hand and $91.72 million in marketable securities that can be liquidated at any time. This gives GENC the flexibility to make acquisitions in the future and further expand its business portfolio.

On the margin front, I believe the gross margins should continue to improve in FY23 as the steel prices are well below their 2022 highs. The increased production volumes should reduce overhead expenses, thus improving operating margins in FY23.

Risks

-

The demand for GENC primarily depends on federal and state-level funding. If there is a delay in this funding, the company's revenue should be negatively impacted.

-

Commodity prices are difficult to predict and if steel prices increase, it should impact the profitability.

Valuation

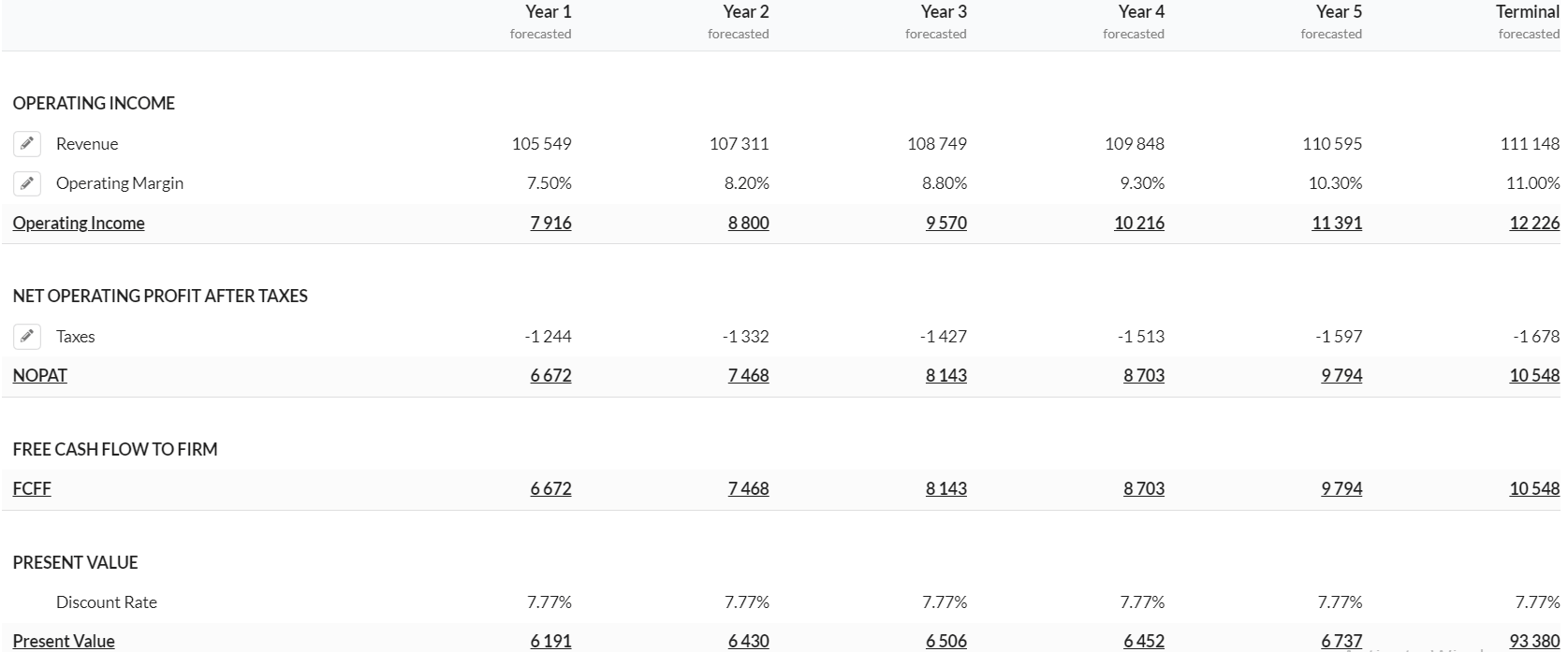

DCF valuation (Created by DzD Analysis using Alpha Spread)

{kind=link}

In my DCF calculations, I am assuming revenue growth to be in the low-single digits in 2023 given the healthy order backlog and demand from federal-level funding. Beyond 2023, I have assumed growth to be in the low-single digits, with a terminal growth rate in the low-single digits, as the company will continue to benefit from the Infrastructure Investment and Jobs Act (IIJA) funding till FY26. I used a discount rate of 7.77% by using the cost of equity of 7.77% and arrived at a fair value of $15.32 for GENC.

Conclusion

To summarize, GENC appears to have strong potential for revenue and margin growth. However, I'm currently maintaining a hold rating at the present levels as the stock has already experienced a significant surge following the release of its first quarter FY23 earnings. Moreover, there are other compelling opportunities within the construction machinery equipment sector that offer solid growth prospects and are available at more attractive valuations. Therefore, it may be prudent to consider exploring these alternatives before making any investment decisions.

For further details see:

Gencor Industries: Not A Buy After The Recent Outperformance