MEUSW - GeneDx Holdings: Busted SPAC Is An Asymmetric Opportunity With Huge Uncertainty

2023-03-29 07:56:11 ET

Summary

- GeneDx Holdings Corp. has had a dreadful performance as a stock.

- GeneDx's number of shares outstanding have absolutely exploded.

- GeneDx has a negative gross margin and is significantly burning cash.

- While its business model has merit, you need a lot of confidence this is the category winner, and cash burn will slow down.

GeneDx Holdings Corp. ( WGS ) has had a dreadful performance as a stock -- even for a SPAC, and that's something. Massive overspending and no focus on cash flow generation in a time of financial exuberance punished the stock when the market turned, and cash flow generation / profitability became the norm.

Yet, I find GeneDx's go-to-market strategy appealing. The focus on building an AI-driven genomic and clinical data platform - called Centrellis - can be a very lucrative investment. On the other hand, cash burn and dilution risks make the stock's risk profile very high.

I am writing up on GeneDx Holdings, but previously the company was known as Sema4 Holdings. Here's some context:

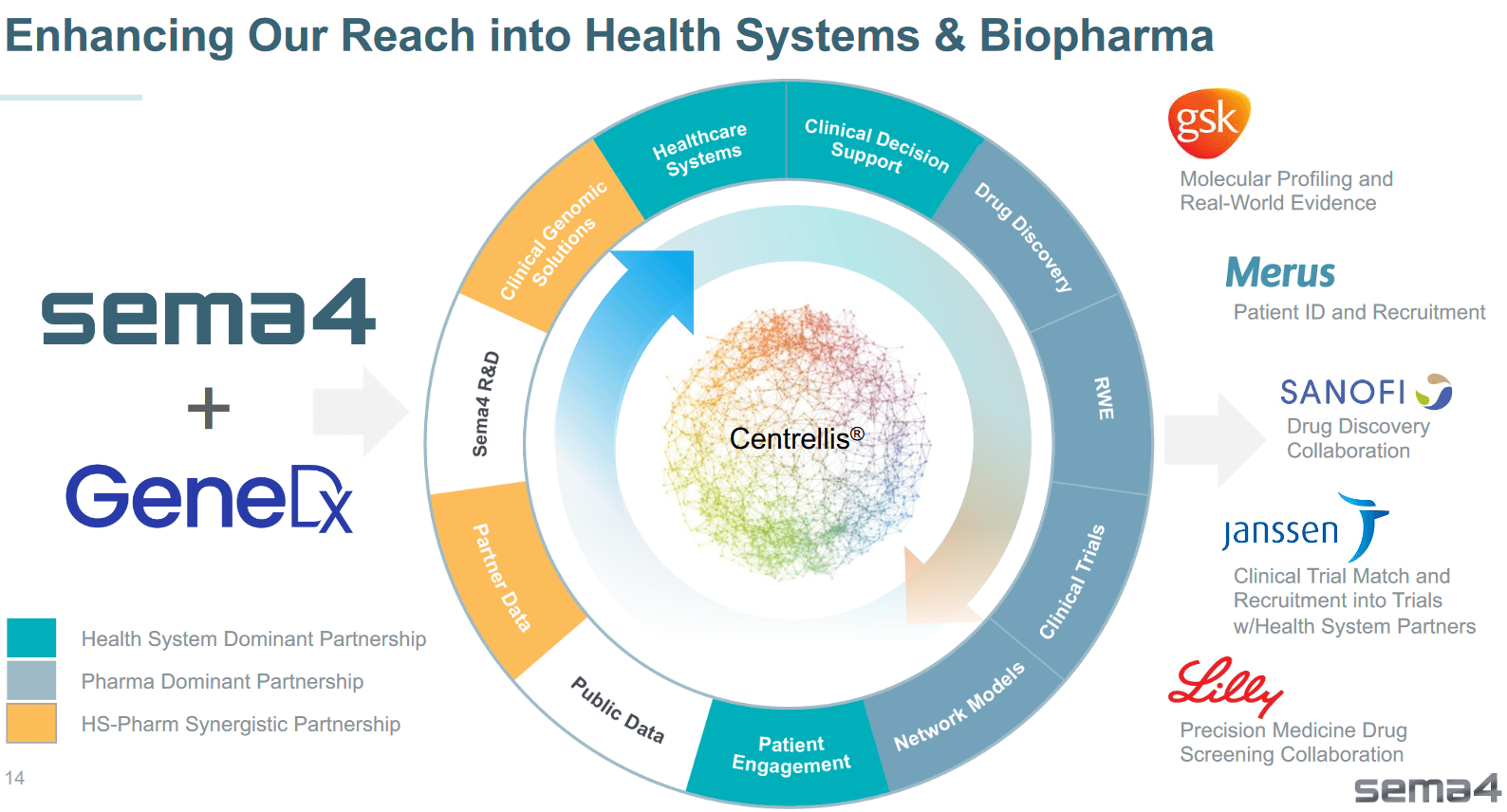

At the start of 2022, Sema4 acquired GeneDx to deepen and widen its offering on the Centrellis platform. GeneDx was particularly strong in providing clinical genomic solutions as this company has a huge dataset of clinical exomes and DNA extractions - as this is one of Sema's core focus areas, the acquisition makes a lot of strategic sense. The CEO of GeneDx, Katherine Stueland, also became the CEO of Sema4 Holdings at the time of the transaction.

At the end of 2022, the stock and company rebranded from Sema4 Holdings to GeneDx Holdings. And more recently, the company shut down its reproductive health business to focus on becoming the category winner with its Centrellis platform in genomic clinical insights.

SPAC's

There's a huge amount of massively punished SPACs around -- and I believe, just like after the dot-com bubble, this provides the diligent investor with very attractive investment opportunities.

The problem is there are many SPACs -- and many of them will continue to pump cash into unrealistic bad business propositions. They do not have a position in attractive markets and industries, and the stock market rightfully puts very pessimistic valuations on their businesses.

Finding the ones that actually have merit -- are growing in a market, solving legitimate customer problems and in an industry where they can attain significant competitive advantages. Those are attractive stocks that provide very asymmetric investment opportunities.

Business model

Very fundamentally, I think GeneDx's go-to-market strategy has lots of merits. Combining genomic and clinical data to provide personalized insights and decrease the time to find a clinical diagnosis -- makes intuitive sense and can make fewer people die from disease. GeneDx has more than 400K clinical exomes on its platform and more than a million DNA extractions. In contrast, Sema4 has 3.1 million patient health records, 8 million diseases diagnoses and 47 million phenotypes. All this data is now on the Centrellis platform. Very fundamentally, understanding the genome and people's fitness helps detect health risks, rare diseases etc.

The three focus areas of the company are rare disease detection, adult diagnostic setting and newborn screening. In total GeneDx estimates the TAM to be $30 billion.

This business benefits from a flywheel. The scale provides more data and better solutions, attracting new clients and strengthening the flywheel once again. I think there's little discussion that this platform at scale will benefit from significant competitive advantages and high returns on capital. Some SPACs have business plans that have no merits and are building businesses with little moats - I don't think that's the case here.

{kind=link}

GeneDx IR (GeneDx IR)

Sema4/GeneDx propose they are the frontrunner at turning this data into value - a position that, if true, can be very lucrative to shareholders - without a doubt.

{kind=link}

GeneDx IR

Turning this into a platform model -- where all stakeholders from life sciences and biopharma to healthcare providers and individuals benefit -- should benefit the shareholder, too, eventually.

Interestingly one of the big competitors Tempus uses GeneDx as a supplier for one of its genomic profiles. Another competitor is Invitae ( NVTA ), in terms of revenue they are twice as big but they also operate in different segments like women's health and oncology.

I think the market is big enough for multiple companies to become scaled and profitable; there seem to be different niches having different kinds of demands and needs.

Genome sequencing

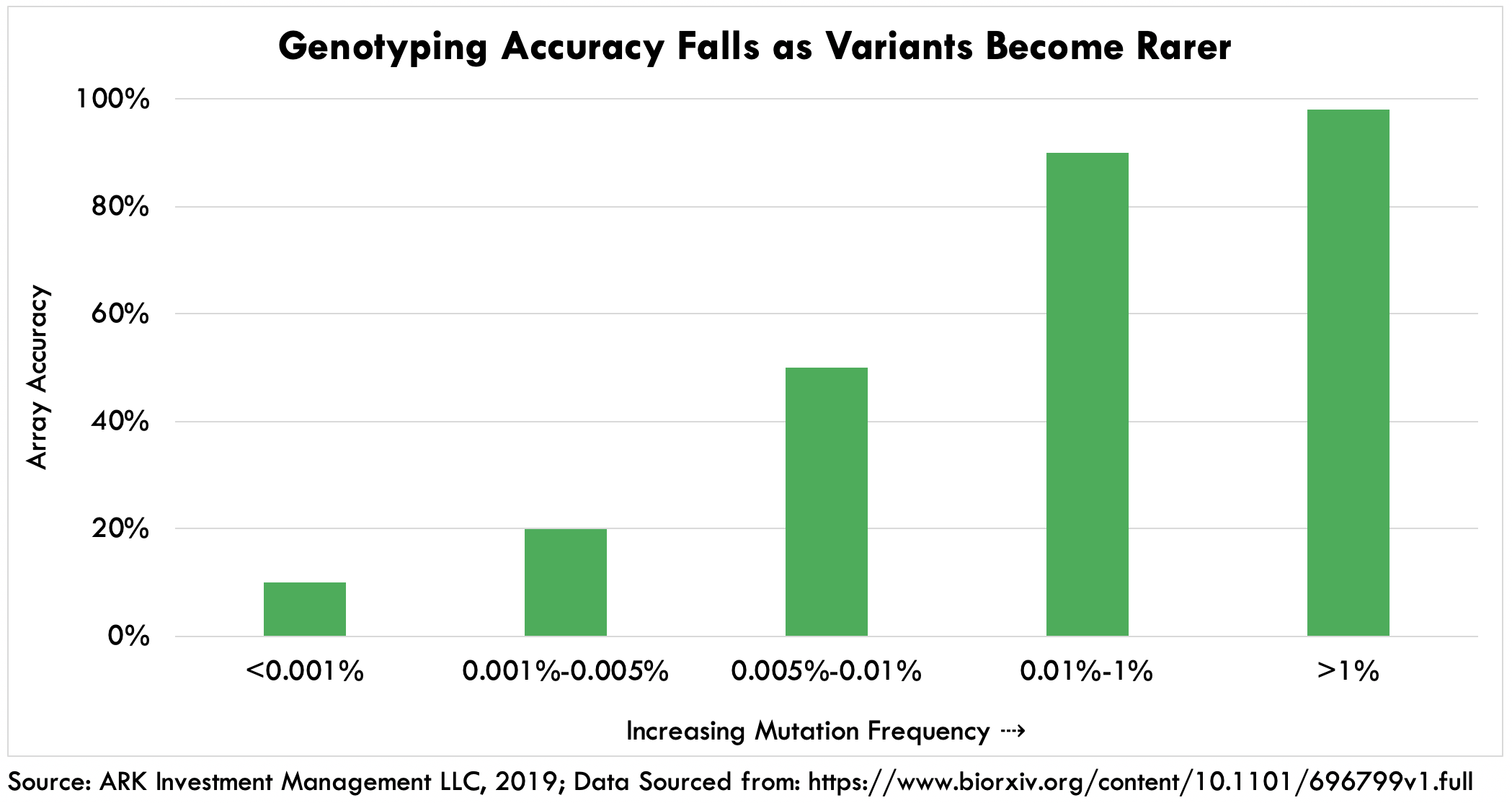

The field of AI and genome sequencing is very competitive. But it's important to understand that genome sequencing is becoming cheaper and cheaper. And that's set to benefit companies like GeneDx.

Whole and exome genome sequencing is much better at detecting and understanding rare diseases than genotyping - which is a genome sequencing method taking only a fraction of the coding DNA. Exome genome sequencing - of which GeneDx has a huge dataset of samples - maps out the entire coding DNA, while whole genome sequencing also maps out the non-coding DNA. The most known genotyping company is 23andMe.

{kind=link}

ARK

This makes it so that companies like 23andMe ( ME ) in the genotyping space have a vast genetic database, are not well positioned to put that to use in the rare disease field.

Instead, companies like GeneDx that focus on exome genome sequencing with a strong AI backbone are the frontrunners. GeneDx management had this to stay about it:

"So first, there's the rare disease and pediatric segment, which we estimate to be about $3 billion conservatively. That's where we are today. So I'll talk about the commercial strategy in that space. We expect of that $3 billion that we're going to be able to get to about 17% of market share by the end of this year."

But I feel like the rare disease market. That alone can already justify a much higher stock price.

Let's say the company gets to a 40% market share - I don't know if it will I am trying to quantify the potential. That's a $1.2 billion revenue stream. Currently, we are talking about a $260 market cap and $212 enterprise value. That seems very asymmetric to me, at a 15% EBIT margin, that's $180 million in EBIT every year. And that's just 1 of the 3 focus areas of the company. Frankly, I can see 30+% EBIT margins easily.

And the $3 billion -- that's a target but its moving up, not down.

If you want to diagnose and understand rare diseases, the patients or parents of the patient desire the best diagnosis and fast. The company with the most data and the best algorithm will provide that service.

It is very clear to me that GeneDx has a huge asymmetry priced into the stock, particularly considering the other market opportunities (newborn screening and adults) represent $26 billion according to management.

Financials

GeneDx Holdings has been a huge cash burner. At one point, the company had $461 million in cash and cash equivalents, but with negative gross margins, the company burned hundreds of millions of cash per year.

Currently, the company has $138.2M in cash and cash equivalents which management believes makes it 'fully funded t o expected profitability in 2025 '. I think the market has its questions; while it is true that in terms of cash outflows, the gross margin has turned positive - there is much to improve.

The platform scale has to drive margin expansion rapidly to control cash burn and make the company well-financed. And I think that might succeed. But you can't invest in 'might'. Particularly considering if that doesn't work out, we could see the outstanding shares grow multitudes again.

Obviously, GeneDx is selling at a discount to its intrinsic value and future earnings power as the company carries significant dilution risks. Dilution risks can massively alter an investment's returns forever - particularly for a publicly traded massive cash burner with relatively small cash reserves.

That makes me far less confident owning the shares as it becomes more a matter of estimating cash burn in the coming years - or hoping for a buyout - instead of confidently buying shares on future cash flow generation with a reasonable expectation of the number of shares outstanding in the company.

When the company entered the market through a reverse merger with a SPAC, there were 240 million shares outstanding. Now that's 798 million shares. Having that amount of dilution massively changes the future per-share value of this company.

Positive developments

The company has rationalized by closing down a position in the reproductive health market. Management said that would eliminate 'at least $30 million in cash burn on a quarterly basis'. That amounts to more than $120 million per year. At a free cash flow of -$329 million in 2022, that is a good start, but alone not enough.

The moment the market is confident cash burn stops before further dilution has to occur and the company can fund its business through internal cash flows; that is the moment this can be a 10-bagger as the market potential could justify a much higher stock price.

Takeaway

But, GeneDx is still scaling up. I would need more insights into competition like Tempus and Helix - before being confident GeneDx is scaled enough to become the category winner.

I can also see GeneDx being picked up by a major player in the sector: Quest Diagnostics ( DGX ) has a significant M&A chest. I don't think the market is putting any value on that right now.

For now, I remain neutral as I prefer to sit out and get more data that makes me more confident GeneDx has what it takes to become the category winner without massively diluting shareholders.

For further details see:

GeneDx Holdings: Busted SPAC Is An Asymmetric Opportunity With Huge Uncertainty