GNRC - Generac: Inventory Issues Remain But Getting Better

2023-09-07 09:41:36 ET

Summary

- Generac is facing issues with excessive inventory of standby generators in the dealer channel, impacting sales and financial performance.

- However, areas such as the C&I business and international have been strong.

- Its inventory issues could linger due to higher interest rates and less spending on home and energy projects.

When I last looked at Generac ( GNRC ) back in March , I noted that while the company has transformed its business that poor execution and too much field-level generator inventory were issues impacting the company. Since then, the stock has risen about 4%, trailing the over 15% climb in the S&P over the same period. Let’s catch upon the stock.

Company Profile

As a refresher, GNRC sells generators to residential customers as well as to the commercial and industrial sectors. It sells both home standby generators that run on natural gas and are wired to the home and portable generators on the residential side. On the C&I side, it offers commercial grade natural gas and diesel powered generators.

The company has also made a number of acquisitions to become a more complete energy solution company. It entered the residential solar market in 2019 through its acquisition of Pika Energy, and sells a system that stores electricity from solar panels that consists of an inverter, photovoltaic optimizers, power electronic controls, and batteries. Meanwhile, following its acquisition of Ecobee, it entered the smart home market, offering smart thermostats, smart cameras, and security devices.

Inventory

In my original article on GNRC, I noted that the company was experiencing two big issues. One was that there was too much standby generator inventory in the dealer channel. The other was that the company had experienced quality issues with its SnapRS switches, which has hurting sales of its PWRcell energy storage systems.

The company was still feeling the impact of these issues in Q2, with sales declining - 23% to $1 .0 billion , and core sales, which exclude FX and acquisitions, down -26%.

Adjusted EBITDA dropped -49% to $137 million, with EBITDA margins falling to 13.6% from 21.0%. Adjusted EPS came in at 70 cents versus $2.21 a year ago.

Not surprisingly, most of the pain was felt on the Residential side of the business, as sales plunged -44% to $499 million versus $896 million a year ago.

Standby home generator channel inventory was about 1.2-1.,3x normal levels. That was an improvement from 1.4-1.5x when it last discussed it in April, but still higher than the company expected.

Addressing the channel inventory issue on its Q2 earnings cal l, CEO Aaron Jagdfeld said:

"Today, we believe that number is closer to 1.2x to 1.3x as we exited the first half. And with the assumption of a softer consumer spending environment, in particular around kind of residential investment, these types of projects, home improvement projects, we're really looking at a more moderated close rate it's interesting because we actually are seeing a lot of inbound activity. In terms of sales leads, the close rate on those leads is not growing at the rate that we thought it would, and then it just becomes a math problem from there. We're not going to drain the inventory as quickly because we're not going to convert those leads to activations at the rate that we thought we would here in the second half. And that's going to create basically a situation where that elevated field inventory is going to persist a bit longer than we had originally thought. So really kind of through the year here, it will start to taper off. And I think you've done this with channel checks. We do our own channel checks and we know what field inventory looks like really with a high degree of accuracy region to region and dealer-to-dealer, wholesale to wholesale or retailer to retailer. And so we see regions where actually, there isn't a field inventory issue anymore. And we see other regions where field inventories are still higher than normal. So, it's become more of a mixed bag, if you will, around the field inventory story, whereas I would say, you wind the clock back 2 or 3 quarters, it was 2 or 3 quarters ago, it was everywhere."

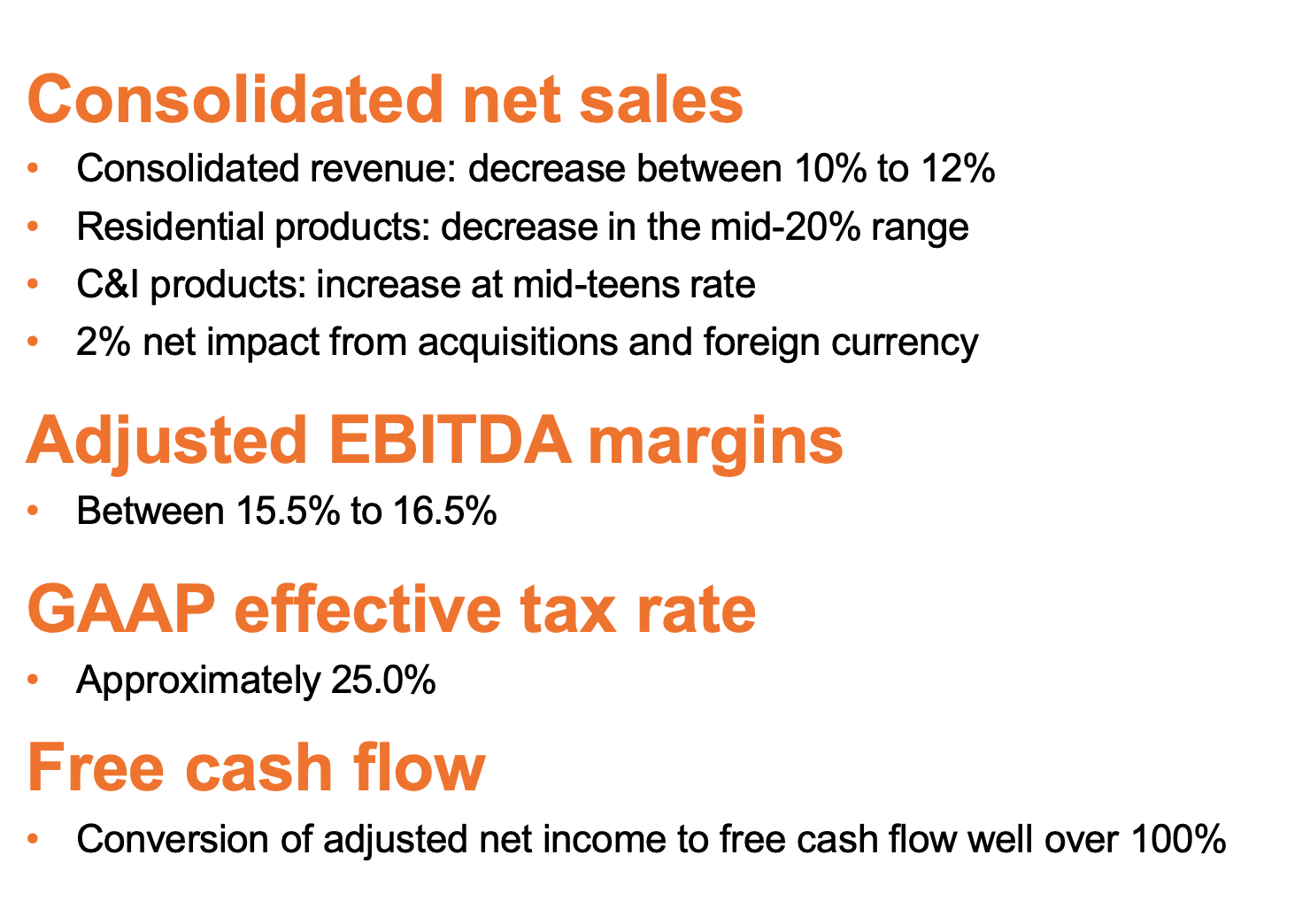

As a result of its ongoing channel inventory issue, GNRC lowered its full-year guidance. It now expects sales to decline by -10% to -12%, down from prior guidance of a sales decline between -6% to -10%. The company expects a return to growth in Q4. GNRC also lowered its net income margin from 7.5-8.5% to 6.0-7.0% and EBITDA margins to be 15.5%-16.5% versus a prior outlook of 17.0-18.0%.

{kind=link}

GNRC 2023 Guidance (Company Presentation)

On the energy solutions side, the company is working through its next-generation roadmap after its initial product quality challenges with SnapRS. It now expects solar and storage to contribute towards the low-end of its prior $300-350 million target. The company said higher interest rates as well as California’s NEM 3.0 have led to a softer market.

Outside of these areas, GNRC has been seeing strength. The C&I business saw revenue climb 24% to $384 million, while international sales rose 10% to $223.7 million. The company also noted that Ecobee sale were strong and that the brand is taking share in the smart thermostat market.

While there are some positive signs coming from GNRC, that is being outweighed by its continued standby generator channel inventory issues. With field inventory remaining at above-normal levels and higher interest rates impacting home improvement and energy solution projects, this issue could continue to linger.

Valuation

Based on the 2023 EBITDA consensus of $634.6 million, GNRC trades at an EV/EBITDA multiple of about 14x. Based on the 2024 EBITDA estimate of $820.3 million, it trades at about 10.8x.

Based off of 2023 EPS estimates of $5.35, it trades at 22x, while based on 2024 EPS estimates of $7.36 it trades at 16x.

Revenue is projected to fall -11% this year, and growing nearly 9% in 2024.

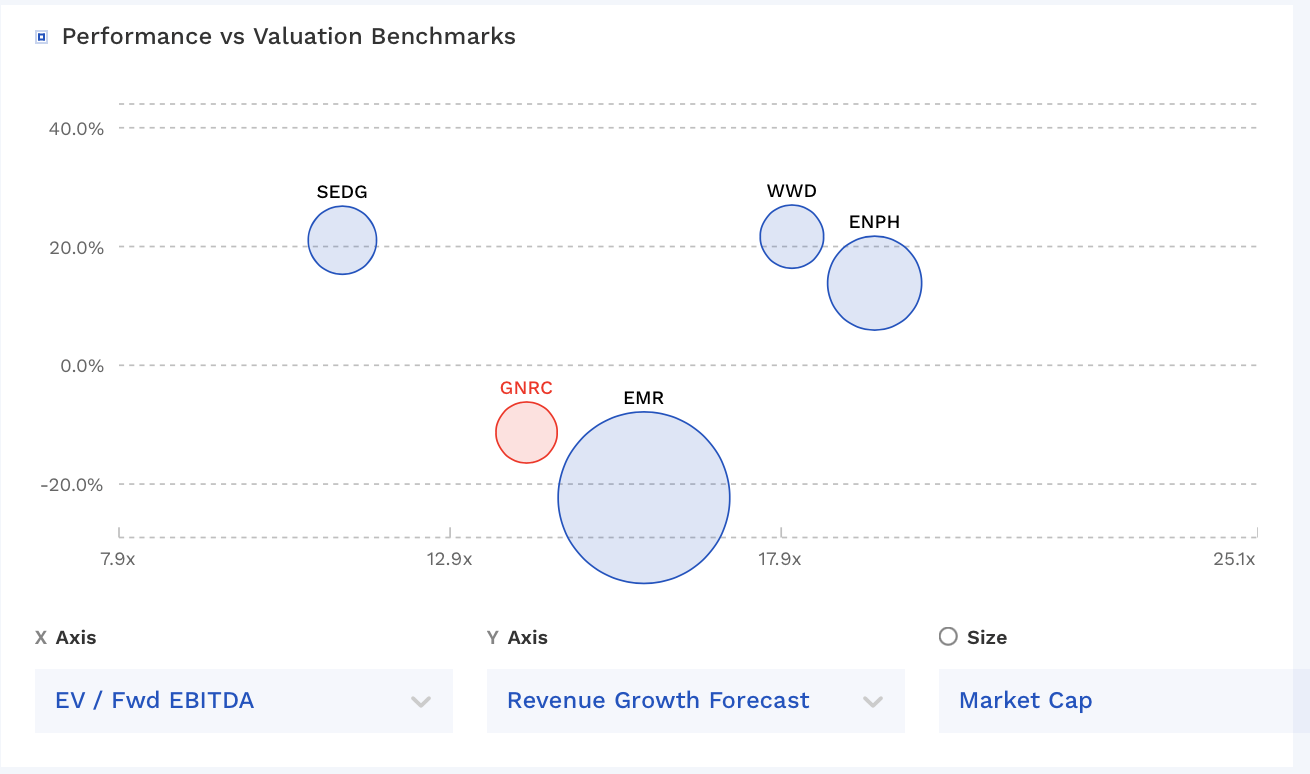

The stock looks reasonably valued versus its electrical equipment peers.

{kind=link}

GNRC Valuation Vs Peers (FinBox)

Conclusion

GNRC is still dealing with channel inventory issues, but it appears to be getting closer to a more normalized level. With some recent adverse weather events in places like Florida and California, two of GNRC's largest markets, this could help speed up the process, although it does appear to be more regionalized at this point and these events tend to help portable generator sales more immediately. Meanwhile, the company is doing well in the C&I segment, as well as making inroads internationally.

{kind=link}

Company Presentation

The solar business is seeing some of the same issues Enphase ( ENPH ) is seeing, but it’s a much smaller piece of business for GNRC and remains more of an opportunity long term. That said, higher rates and loan costs could also put a dent into standby generators sales similar to solar, as installing a standby generator is quite expensive.

As such, while I think the GNRC story is getting more interesting, I’m going to remain cautious for now and remain neutral on the name.

For further details see:

Generac: Inventory Issues Remain, But Getting Better