GNRC - Generac- Tricky Residential Outlook But Valuations And The Risk-Reward Are In A Better Place

2023-08-03 10:37:43 ET

Summary

- Generac missed bottomline estimates in a big way, and the FY23 guidance was scaled down as well.

- The residential end-market looks weak, but the risk of higher power outages may help tilt sentiment.

- Despite a cut in the estimates, forward valuations still look attractive, and the stock is still a suitable rotational candidate within the clean power space.

- Investors are advised to wait for some bottom formation before diving in.

Introduction

The energy tech solutions firm Generac Holdings, Inc. ( GNRC ) was in the news this week after it came out with unsavory Q2 results which prompted the share price to tank by ~25% yesterday. Here’s the lowdown of the event and how things stand

Key Headlines

There are a lot of moving parts when it comes to Generac, but it’s fair to say that the weakness after the results were posted was driven by two key factors- a) a miss on earnings, b) a downgrade in the FY23 guidance, driven mainly by weak conditions in the residential market.

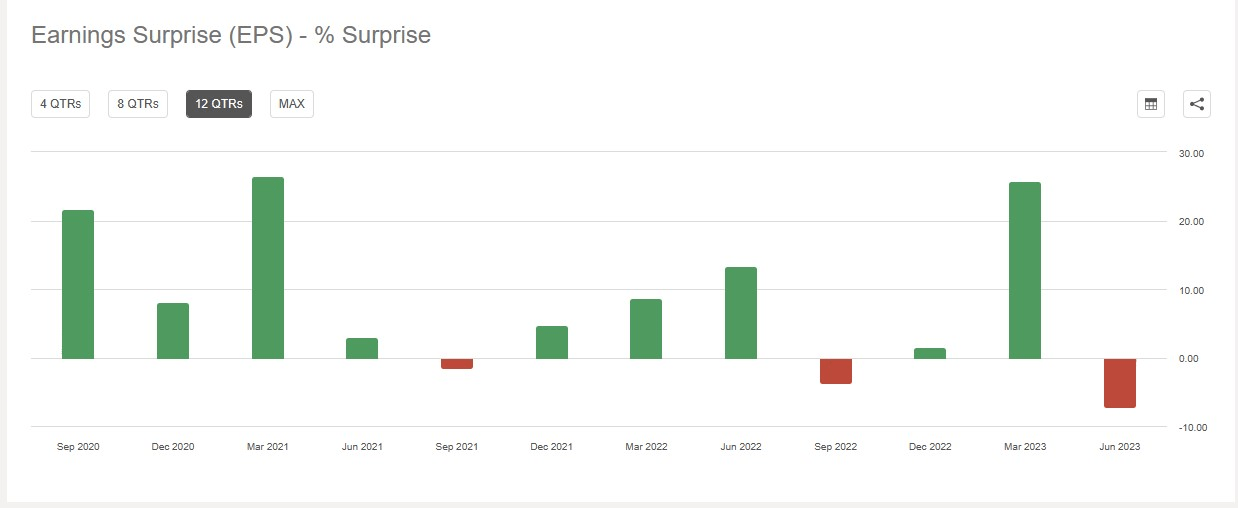

Firstly, on earnings, it’s worth noting that across its recent history, the stock had built up a decent track record of beating street estimates on most occasions, and even when it missed estimates, the variance wasn't too pronounced at low single digits. However, in Q2, the magnitude of the EPS miss relative to consensus was quite wide at -7%!

{kind=link}

Meanwhile, the FY guidance too was curtailed in a big way. Previously management had expected topline weakness to come in at -6 to -7% YoY, but this was brought down to -10% to-12% YoY. EBITDA margins which were previously budgeted at 17-18%, were brought down to 15.5%-16.5%. Also, the net income margin which was previously estimated to come in at 7.5%-8.5%, was scaled down to 6-7%.

Residential Category- The Chief Culprit

Much of GNRC’s troubles are currently being dictated by the residential market, the segment which accounts for the largest share of GNRC’s overall sales mix (59% of group sales). Admittedly, given the strong base effect of Q2 last year ( 49% YoY growth), where this segment benefitted from a significant clearance of its home standby generator backlog, nobody was expecting positive growth in Q2. In fact management had already warned that H1 was likely to be soft (Q1 resi sales had declined by 46%YoY) with positive YoY growth only expected in H2.

What the market didn’t expect was a similar cadence of YoY declines, and that’s what we saw in Q2, where the run rate was almost similar to Q1 at -44% YoY. This also means that the recovery is likely to get pushed back because previously management had stated that H2-23 would not just witness positive resi growth, but it would also “partially offset the expected H1 decline” . As per the latest outlook, management “now anticipates lower residential product sales during the second half relative to prior expectations”.

GNRC has turned cautious mainly because of dynamics within the resi sub-category of home standby generator shipments which has been impacted by weak consumer sentiment. This segment typically moves in tune with home remodeling activity, and it's fair to say that the wheels have come off this year as the Fed does its bit to make financing dearer.

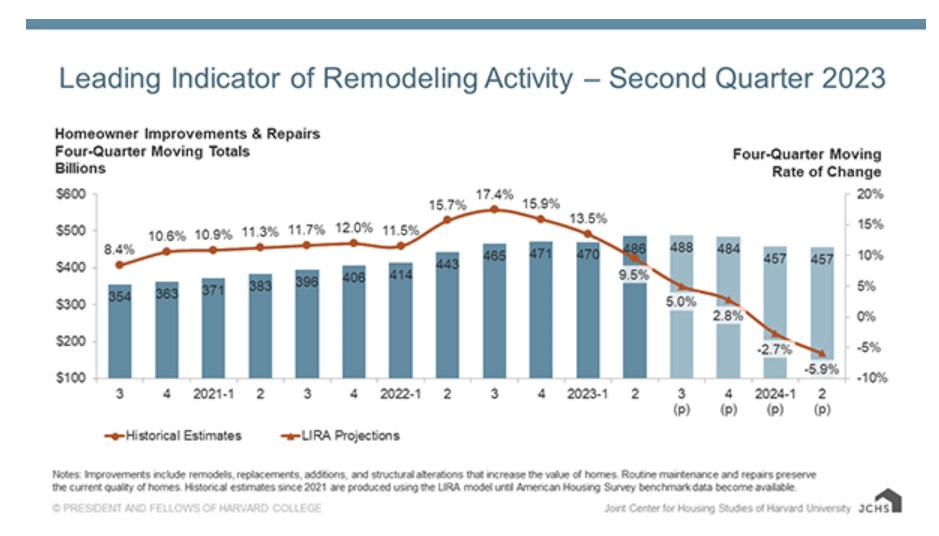

After witnessing double-digit YoY gains for quite a few years, it's only reasonable to expect the pace to slow, but at the start of the year, reports were suggesting that home remodeling work would decline by -3% or so.

{kind=link}

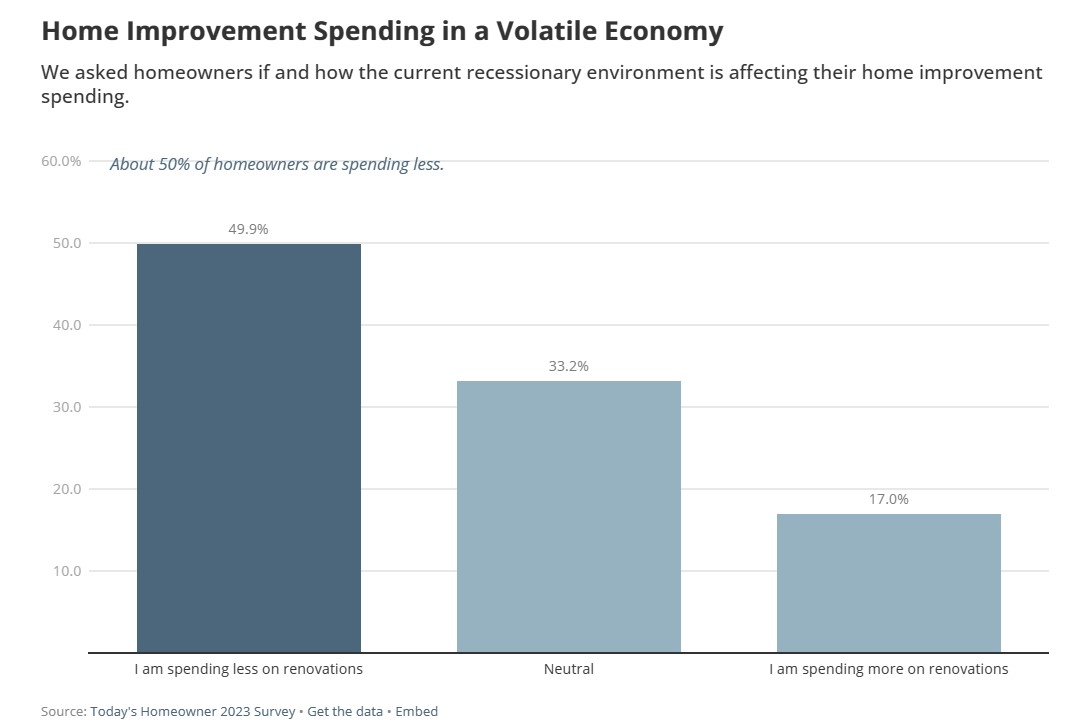

A homeowner survey also suggested that close to half of them would be spending less on home improvement this year. JCHS now expects this to be a persistent slowdown stretching to at least H1-24, with remodeling work in Q1-24 and Q2-24 expected to fall by -2.7%, and -5.9% respectively.

{kind=link}

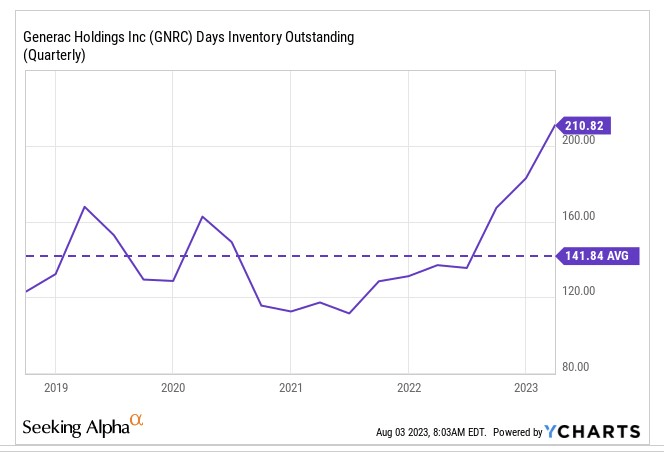

Weak homeowner sentiment means there’s an awful lot of field inventory that GNRC's channel partners are struggling to offload (channel inventory was 1.2-1.3x the normal level at the end of Q2). These inventory challenges exist not just with home standby generators but with clean energy products as well. Due to ample inventory in the channels (particularly in the retail and large dealer channels), GNRC has been forced to carry a lot of inventory on its books, which could put continued pressure on the working capital (although in fairness, management still expects healthy FCF conversion of over 100% from the net income level by the end of this year). Note that the company's days in inventory is currently roughly 49% over the typical average.

{kind=link}

Management was unable to provide definitive clarity on how the resi segment would fare going ahead but what’s encouraging to note is that home consultation and sales leads picked up from Q1, and are still 4x higher than what it was in Q2-19 . What GNRC’s sales force has been struggling to do is to close those deals (despite a higher level of promotional activity compared to what was seen 2-3 years ago), and they were unable to state if this was down to affordability or some other issue.

{kind=link}

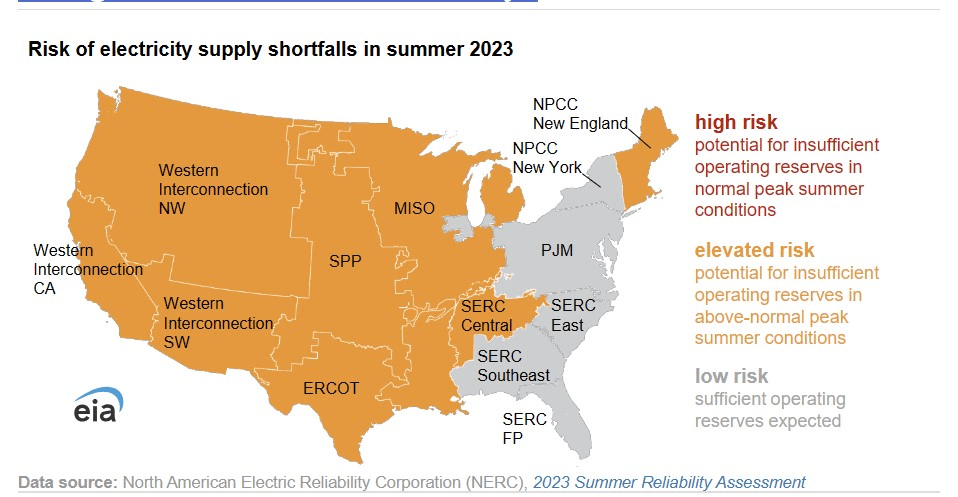

Nonetheless, these tenuous engagements with the salesforce would suggest that the populace is still concerned by the level of power outages , which will likely only get worse over time. In the short term, NERC estimates that 66% of North America could be at risk of energy shortfalls. Note that GNRC is currently only budgeting for a normal outage environment through this year, but if things were to get worse, there's every chance you could see sales perk up.

As home standby generator sales take up a lower chunk of the overall sales mix, this also reflects poorly on GNRC’s overall gross margins which were down by 260bps. Nonetheless, management feels that cheaper raw material costs, better plant utilization, and lower logistics costs could likely help drive a better margin performance in H2, so much so that FY margins could actually improve by 100bps YoY.

Closing Thoughts: Stock-Related Considerations

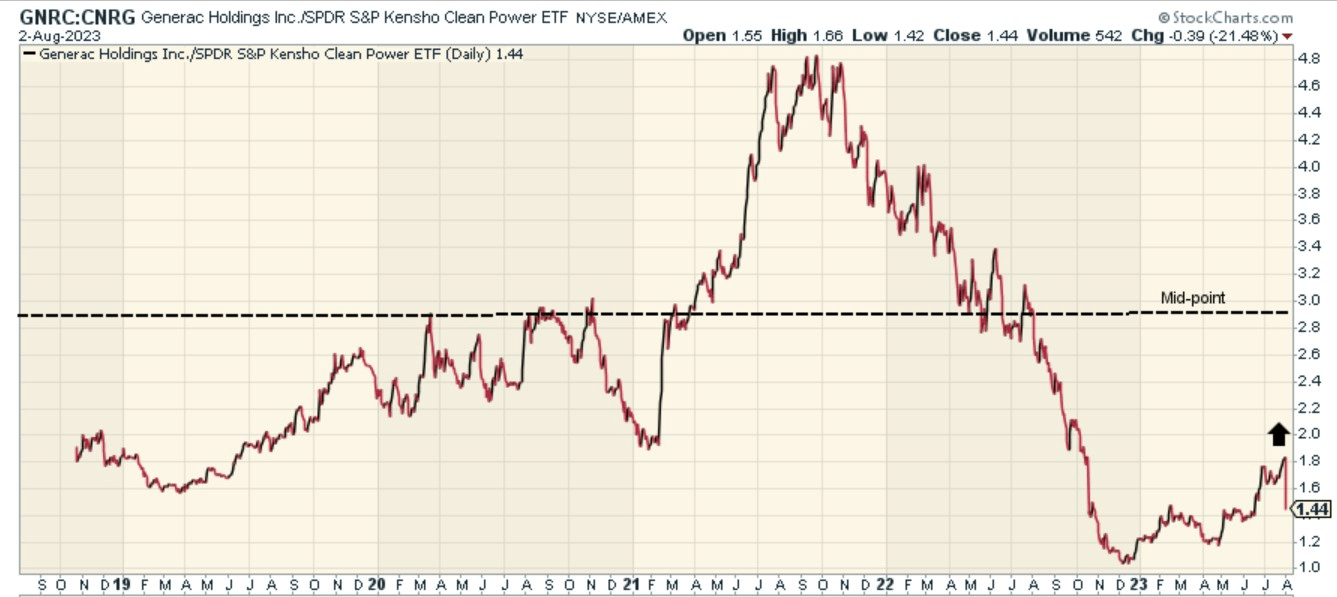

{kind=link}

Even before the abysmal Q2 event, GNRC looked like one of the more promising rotational candidates within the clean power space. The chart above provides some context of GNRC’s strength relative to its clean energy peers. Before the results, the relative strength ratio was trading around 38% off the mid-point of the range, now it looks even more oversold, trading around 50% off the mid-point.

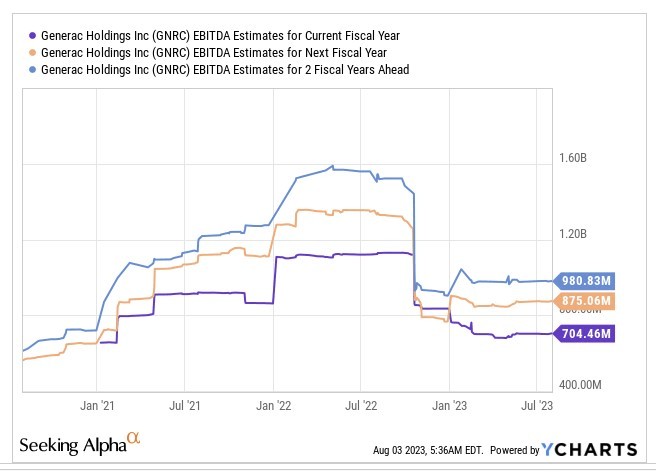

Given the drastic bout of selling after the earnings report , Generac’s forward valuations are in a much better place, even if one accounts for the downward revision in consensus estimates that will likely take place over the next few days. For context, before the Q2 event consensus was budgeting for an FY23 EBITDA figure of $704mn.

{kind=link}

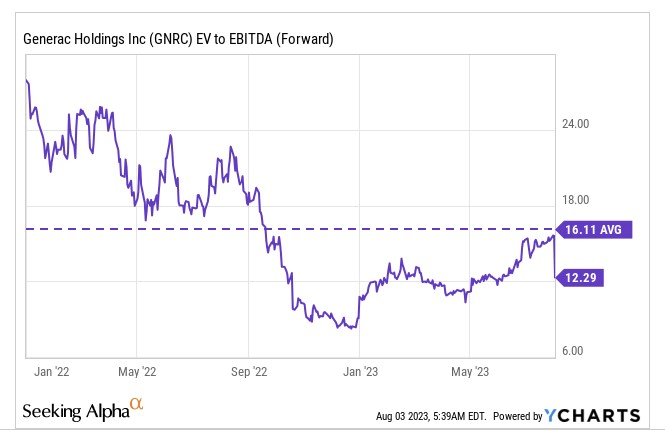

Now that FY revenue decline has been scaled down even further by 300bps (at the mid-point of guidance), and FY EBITDA margin will likely only come in at 16% (mid-point again), versus the old guidance of 17.5%, one could be looking at approximately $45-$50m of downward revisions on the EBITDA front by the sell-side community.

This means, if GNRC does not withstand further correction in its market cap, you could be looking at a forward EV/EBITDA multiple of 13.1x, up from the current pre-revision EV/EBITDA multiple of 12.3x (YCharts). At 13.1x, GNRC would still come in around 20% cheaper than the stock’s long-term average multiple of 16.1x.

{kind=link}

Also consider that this is increasingly looking like an FY23 theme, and even if one sees some marginal trimming in FY24, and FY25 numbers, the weak YoY base effect of FY23 could provide the foundation for EBITDA growth to potentially come in at mid-teens levels over the next couple of years (before the Q2 results, consensus was forecasting 24% EBITDA growth in FY24, and 12% growth in the year after). Mid-teens EBITDA growth for an entity priced at 13x EV/EBITDA doesn’t look like a bad deal.

{kind=link}

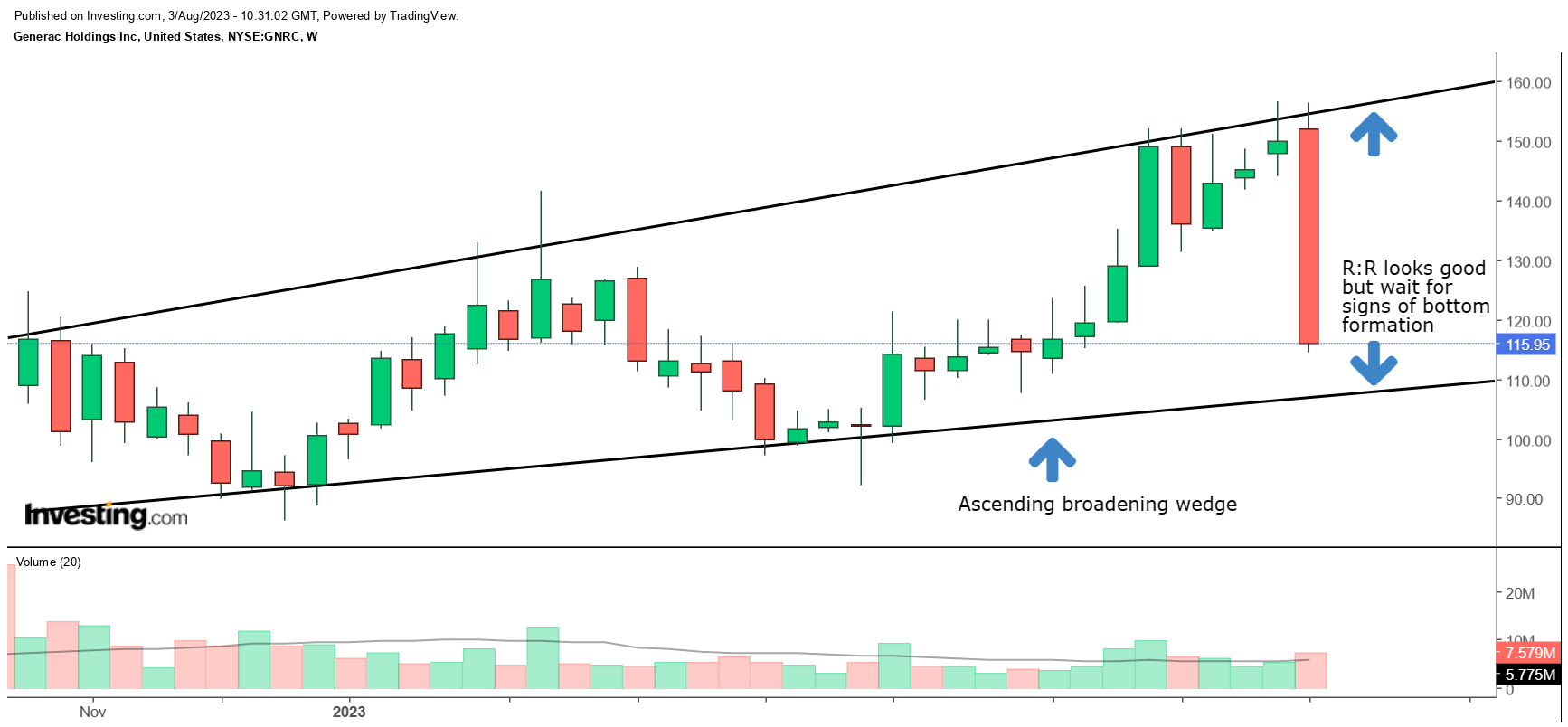

Finally, if we switch over to a chart showing GNRC’s weekly price imprints, we can see that since forming an intermediate bottom last year, the stock had been trending up in the shape of an ascending broadening wedge pattern. Prima facie, if you consider the two boundaries of this wedge, the risk-reward looks more favorable at current prices. However, considering some of the cautious management commentary from the Q2 earnings call, we would advise investors to wait for a few more weeks to ascertain how the stock fares around the $110 levels. If it’s able to build a base around those levels, a long position may be considered. At these lowly levels, one may also see management deploy a greater chunk of the pending buyback war chest of $278m and help support the price.

For further details see:

Generac- Tricky Residential Outlook, But Valuations And The Risk-Reward Are In A Better Place