GD - General Dynamics: A Dividend Aristocrat Flying Too High (Rating Downgrade)

2024-01-19 07:30:00 ET

Summary

- Sentiment toward General Dynamics looks to have become greedy, with the stock firmly outperforming the S&P since my last article.

- The aerospace and defense contractor outperformed expectations in the third quarter.

- General Dynamics enjoys an A- credit rating from S&P on a stable outlook.

- Shares of the company look to have swung from undervalued to overvalued.

- General Dynamics could still outperform the S&P 500 in the coming 10 years, but there’s currently no margin of safety, in my opinion.

Anybody who has been a market participant for at least a while knows that volatility is a fact of life in the stock market. The market can seemingly shift overnight from apathy or fear of a stock to greed toward that same stock.

The aerospace and defense contractor, General Dynamics (GD) is a recent example of this argument in action. Since my article last September , shares have rallied 14% - - double the 7% gains of the S&P 500 ( SP500 ).

Just as U.S. funding for the war between Ukraine and Russia has dipped drastically in recent months, instability in the Middle East ramped up with the conflict between Israel and Hamas. Along with a double beat in the third quarter, as I'll discuss, these factors largely account for the rally in General Dynamics. For valuation reasons, I am downgrading the Dividend Aristocrat from a buy to a hold. Please let me dig into General Dynamics' fundamentals and valuation to explain further.

Dividend Kings Zen Research Terminal

{kind=link}

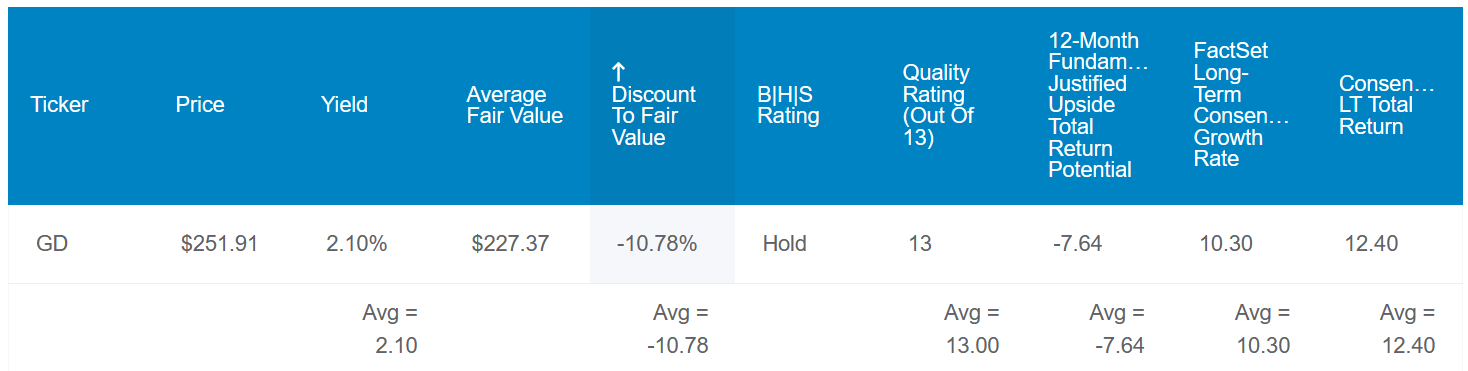

General Dynamics' 2.1% dividend yield isn't going to garner much attention from income investors. However, the company does offer a higher starting income than the 1.5% yield of the S&P.

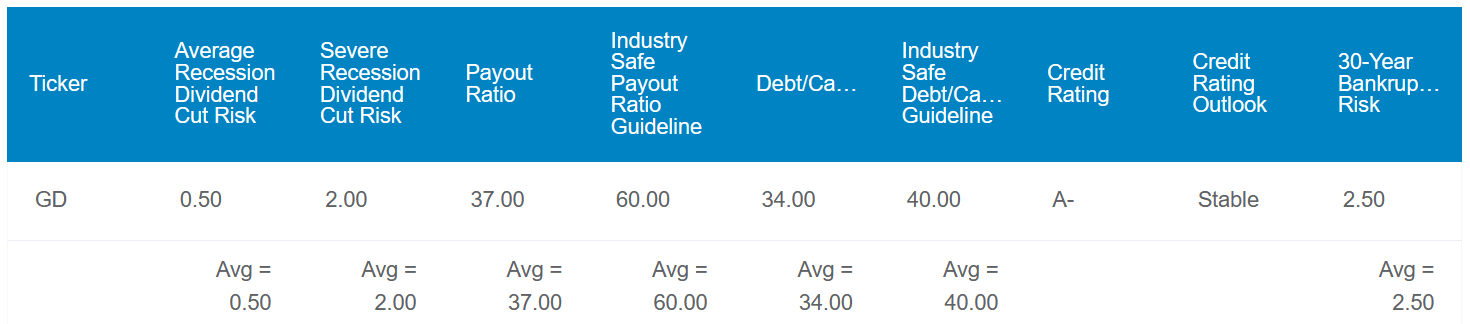

Most importantly, this payout is sustainable and has a lengthy growth runway. First off, General Dynamics' 37% EPS payout ratio is well below the 60% EPS payout ratio that rating agencies desire from the aerospace and defense industry. What's more, the company's 34% debt-to-capital ratio is less than the 40% debt-to-capital ratio that rating agencies prefer from the industry.

Thanks to these elements and General Dynamics' industry leadership, S&P awards an A- credit rating to the company on a stable outlook. That suggests the probability of the defense contractor going bankrupt in the next 30 years is just 2.5%.

Thus, the risk of a dividend cut in the next average recession is only 0.5%. Even a severe recession would push that likelihood to just 2%.

Dividend Kings Zen Research Terminal

{kind=link}

General Dynamics' rally has benefited existing shareholders but has been to the detriment of those wanting to open a position. According to historical dividend yield and P/E ratio, shares are worth $227 apiece. Relative to the $251 share price (as of January 16, 2024), that implies General Dynamics' shares are 10% overvalued.

If the company can deliver on the analyst growth consensus and reverts to its mean valuation, here are the total returns that could lie ahead in the coming 10 years:

- 2.1% yield + 10.3% FactSet Research annual growth consensus - a 1% annual valuation multiple drag = 11.4% annual total return potential or a 194% 10-year cumulative total return versus the 8.6% annual total return potential of the S&P or a 128% 10-year cumulative total return

A Record Backlog And Steady Financial Position

General Dynamics Q3 2023 Earnings Press Release

{kind=link}

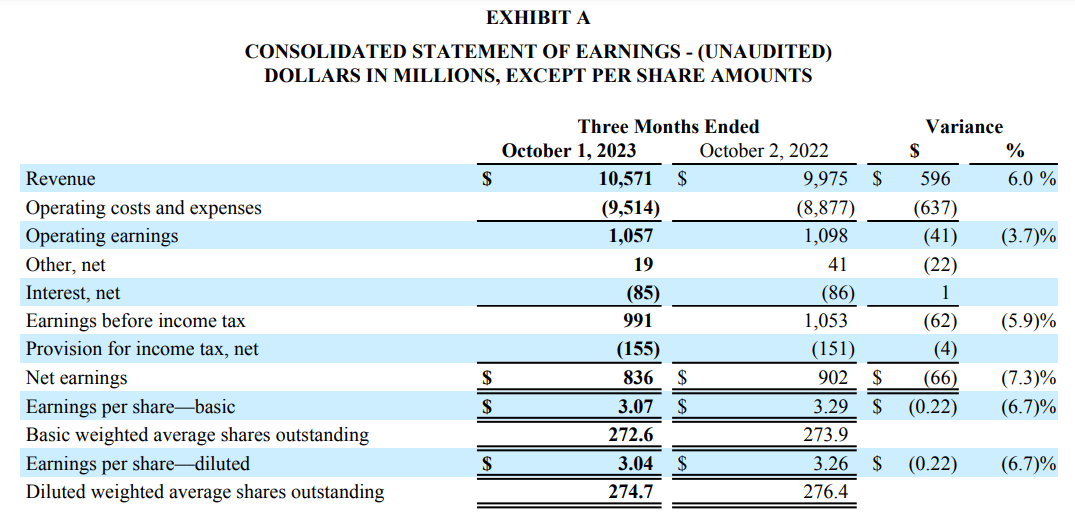

General Dynamics didn't fail to deliver in its third quarter ended October 1. The company's total revenue grew by 6% year-over-year to $10.6 billion during the quarter. That beat the analyst consensus by $520 million for the quarter.

Besides the Aerospace segment, these results were driven by strength throughout the business. That segment recorded $2 billion in revenue in the third quarter, which was down 13.4% over the year-ago period. Fortunately, weakness in the Aerospace wasn't due to any concerning issues with the business. Rather, it was caused by fewer deliveries at Gulfstream, which was the result of supply chain constraints per CFO Jason Aiken's opening remarks during the Q3 2023 earnings call .

The Combat Systems segment revenue soared 24.4% year-over-year to $2.2 billion during the third quarter. According to Aiken, that growth was driven by strength within the European Land Systems and Ordnance and Tactical Systems businesses.

Margin Systems segment revenue increased by 8.4% over the year-ago period to $3 billion for the third quarter. This topline growth was fueled by Columbia-class submarine constructions and engineering per Aiken.

Lastly, Technologies segment revenue grew by 8% year-over-year to $3.3 billion in the third quarter. These results were made possible by relatively evenly distributed growth within GDIT and mission systems.

General Dynamics' diluted EPS fell by 6.7% over the year-ago period to $3.04 during the third quarter. This managed to top the analyst consensus by $0.12. A 100 basis point contraction in net profit margin to 10% was to blame for diluted EPS decreasing as revenue moved higher.

Looking toward the future, General Dynamics is well-positioned. The company's book-to-bill (e.g., orders divided by revenue) was 1.4 for the third quarter. As a result of the robust demand for the company's products and services, the backlog rose by 7.7% year-over-year to $95.6 billion. For more perspective, that is more than two years of backlog based on the respective $42.3 billion and $46 billion analyst revenue estimates for 2023 and 2024.

The company is set to report its financial results for the full-year ended 2023 next week (January 24). The current analyst consensus of $12.18 for 2023 implies that analysts think the aerospace and defense contractor will post $3.79 in diluted EPS in the fourth quarter. If this were to materialize, it would represent a 5.9% year-over-year growth rate versus Q4 2022's figure of $3.59 per Seeking Alpha.

From the looks of it, General Dynamics could be set to post a meaningful diluted EPS beat versus analysts' expectations. That is because CFO Jason Aiken indicated that he is holding year-end guidance at $12.65 during the Q3 2023 earnings call. This suggests the company is forecasting around $4.26 in diluted EPS for the quarter - - a 19% year-over-year growth rate.

These forecasts certainly make sense considering that Aiken noted revenue was up 4.1% sequentially and EPS was up 12.6% sequentially. The belief that these strong results will continue underpins not only the argument for an exceptional performance in Q4, but a great 2024. Management hasn't yet provided guidance for 2024, but analysts anticipate that the company's diluted EPS will rise to $14.93 next year - - a 22.6% growth rate over the consensus for 2023.

Moving to General Dynamics' financial health, the company's interest coverage ratio through the first nine months of 2023 was 11.4. That is a solid interest coverage ratio, which lends support to the argument that General Dynamics is a financially solvent business.

Strong Free Cash Flow Can Power Future Dividend Growth

General Dynamics' annual dividends paid have cumulatively compounded by 43.8% from 2018 to $5.22 in 2023. There's also reason to believe that similar growth can keep up in the years ahead.

General Dynamics generated $2.9 billion in free cash flow in the first three quarters of 2023. Against the $1.1 billion in dividends paid, that equates to a 36.7% free cash flow payout ratio (page 7 of 51 of General Dynamic's 10-Q filing ). That allows the company to retain ample capital to repay debt, repurchase shares, and grow its dividends further.

Risks To Consider

General Dynamics' fundamentals are undoubtedly vigorous. But like any company, it isn't perfect, either.

As I have outlined in previous articles, the biggest risk facing the company is concentration risk. Through the first nine months of 2023, the U.S. government contributed $22.6 billion or 72.7% of General Dynamics' total year-to-date revenue (page 14 of 51 of General Dynamics' 10-Q filing).

Suffice it to say, that the company's success moving forward still hinges on U.S. defense spending remaining a top budgetary priority. If debt-related interest expenses and entitlement expenses keep growing, that could lessen funds available for defense spending. This would somewhat weigh on General Dynamics' growth prospects if it were to come to fruition.

Summary: Keeping This Dividend Aristocrat On My Radar

FAST Graphs, FactSet FAST Graphs, FactSet

{kind=link}

{kind=link}

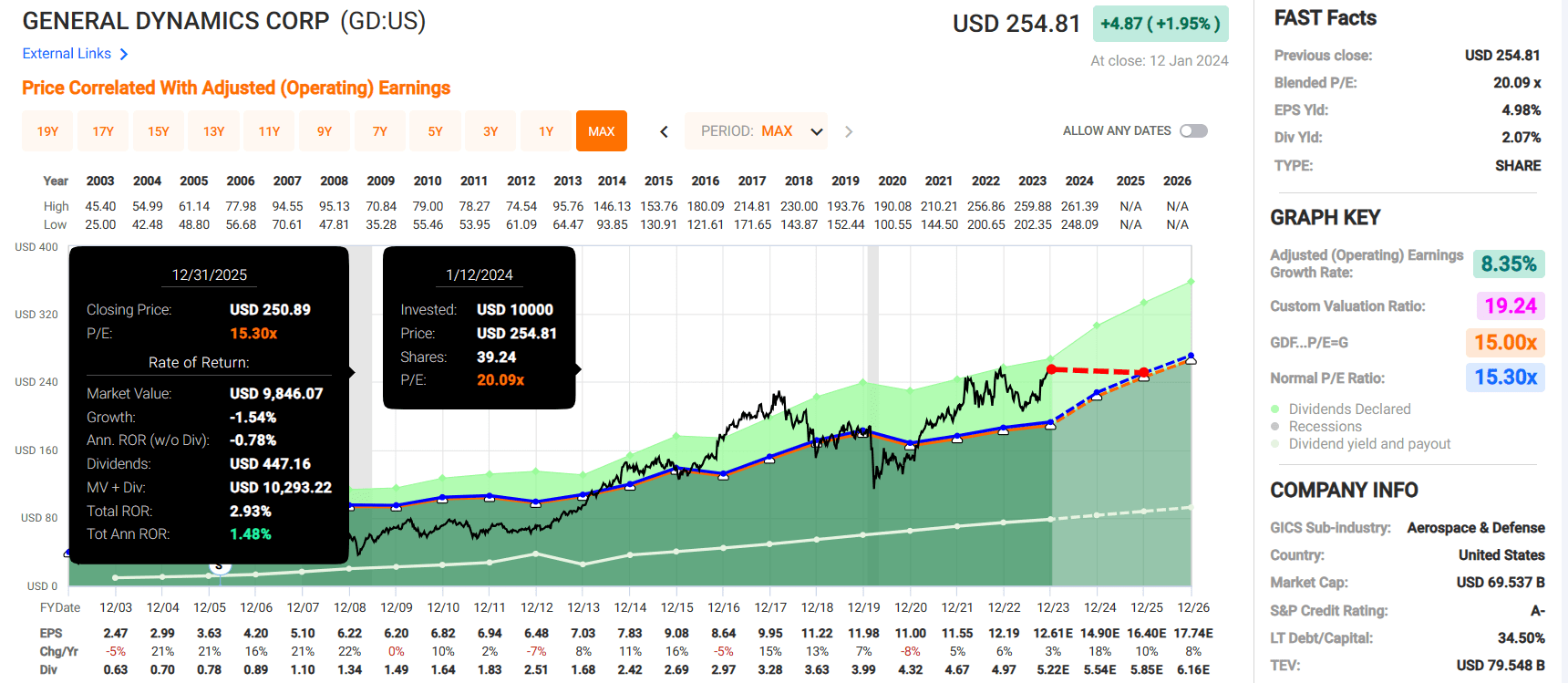

As my intro demonstrated, General Dynamics could well outperform the S&P over the next 10 years if growth materializes. My only cause for concern at this juncture is the impact that the current valuation could have in the next couple of years.

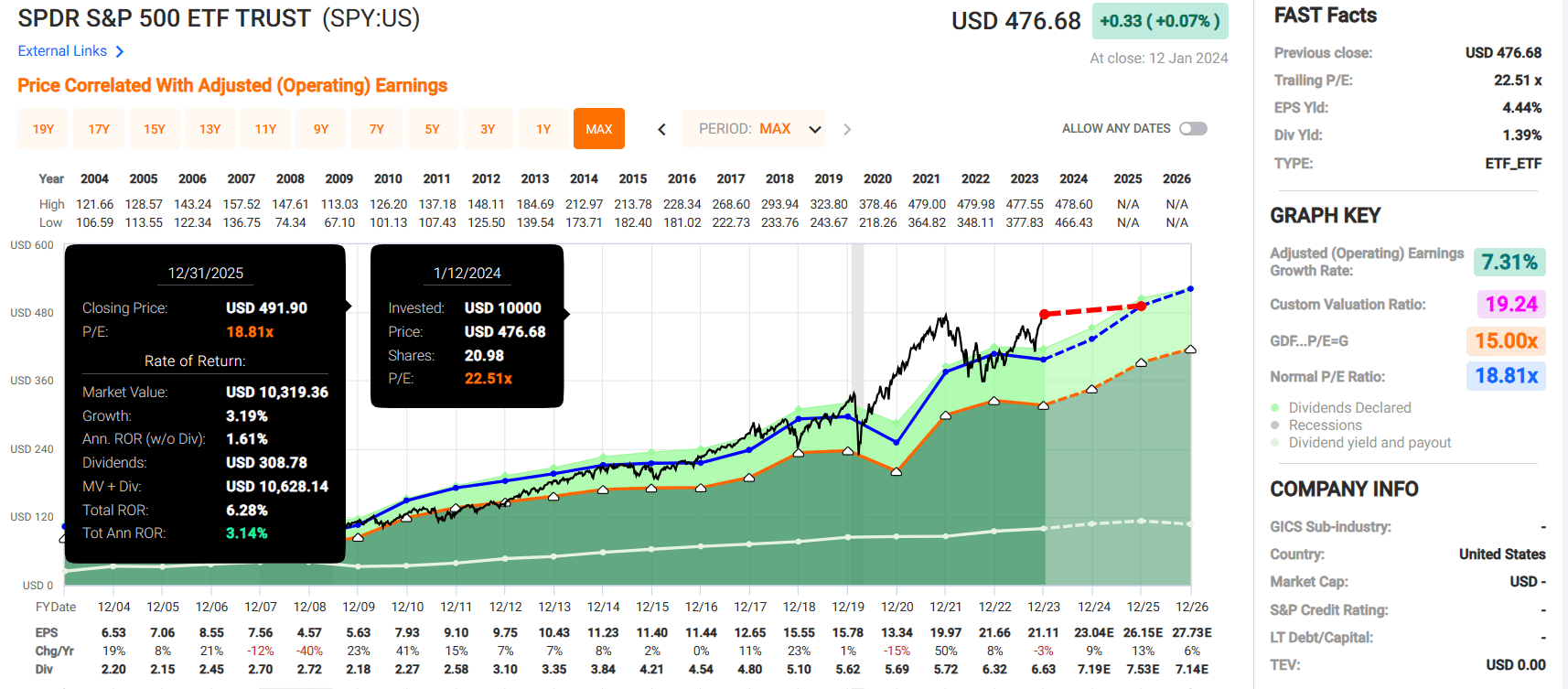

General Dynamics' 20.1 blended P/E ratio is considerably higher than the normal P/E ratio of 15.3 per FAST Graphs. If the company grows as anticipated and reverts to this multiple, 3% cumulative total returns could be generated through 2025.

That's not a particularly attractive near-term total return profile when the SPDR S&P 500 ETF Trust (SPY) is expected to produce 6% cumulative returns during that time. Therefore, I am rating shares of General Dynamics a hold until they come back down to the mid-$220 range or less (or shares become more valuable over time, whichever comes first).

For further details see:

General Dynamics: A Dividend Aristocrat Flying Too High (Rating Downgrade)