GD - General Dynamics: A Significantly Undervalued Dividend Aristocrat

2023-08-09 13:14:41 ET

Summary

- General Dynamics Corporation is experiencing rapid order growth in all segments, benefiting from post-pandemic aerospace growth and increased demand for military hardware.

- The company has a solid moat, diversified revenue streams, and resilience in recessionary times, making it an attractive investment.

- Despite supply chain challenges, General Dynamics is poised for long-term revenue growth and potential outperformance, with a strong order performance and growing backlog.

Introduction

Aerospace & defense is the largest industry in my dividend growth portfolio. 18% of my entire portfolio is invested in America's largest defense contractors.

This was never based on my expectations of a full-blown war that would propel the order flow of companies producing military technology, but the fact that advanced technology is the reason why NATO nations are unlikely to be forced into a major war anytime soon. Defense through innovation, so to speak.

One of the companies that has been on my radar for a very long time is General Dynamics Corporation ( GD ) . This company is currently firing on all cylinders, thanks to rapid order growth in all of its segments. The company has benefited from strong post-pandemic growth in its commercial aerospace segment and the fact that the Ukraine war has put a new focus on military hardware like main battle tanks and various armored vehicles.

However, the company's earnings power continues to be negatively impacted by subdued margins, as supply chains still aren't as strong as defense contractors want them to be.

While that may be annoying, it comes with opportunities.

I believe that General Dynamics is one of the most attractive dividend growth stocks on the market, thanks to secular tailwinds and its attractive valuation.

Last month, I wrote an article titled General Dynamics Is Poised For Growth And Way Too Cheap. Since then, the stock has risen 5%, beating the market by roughly 3%.

In this article, I'll update my bull case using new developments, including its earnings, which confirm that the bull case is as strong as it gets.

So, let's get to it!

General Dynamics Is Where It's At

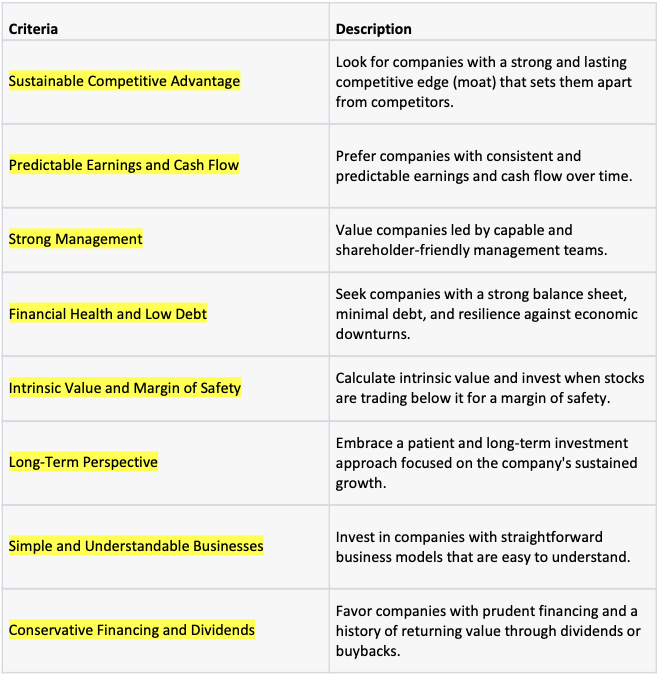

I'm currently building a framework to assess the quality of dividend growth stocks. So far, I'm working on the assessment criteria, which are based on Buffett criteria and other findings that I've applied for many years.

The overview below is what I'm currently working with. In the case of General Dynamics, I highlighted all criteria that apply to this $62 billion market cap defense giant. As we can see, all criteria apply to this company .

{kind=link}

Leo Nelissen (Dividend Investment Criteria - Work In Progress)

The company has a moat so big it can be seen from space. As we can see below, it has a highly diversified business consisting of four major segments, none of which account for less than 18% of its revenues (using 2022 numbers).

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

| Technologies | ||||

| 12,457 | ||||

| 32.4 % | ||||

| 12,492 | ||||

| 31.7 % | ||||

| Marine Systems | ||||

| 10,526 | ||||

| 27.4 % | ||||

| 11,040 | ||||

| 28.0 % | ||||

| Aerospace | ||||

| 8,135 | ||||

| 21.1 % | ||||

| 8,567 | ||||

| 21.7 % | ||||

| Combat Systems | ||||

| 7,351 | ||||

| 19.1 % | ||||

| 7,308 | ||||

| 18.5 % |

General Dynamics is a company that constructs nuclear submarines for the Navy, along with the Arleigh Burke-class destroyer and a wide range of other ships.

The company also manufactures the famous Gulfstream private jet, which is frequently used by celebrities, governments, and businesses.

Additionally, they offer the Abrams Main Battle Tank, the Stryker wheeled combat vehicle, and a comprehensive range of services that cater to advanced defense needs.

{kind=link}

General Dynamics Corporation

While the company is certainly dealing with competition, it does have a wide moat in the segments it is servicing, which is one of the major benefits that come with the massive consolidation of the defense industry of the past few decades.

Furthermore, it's a recession-proof industry for two reasons:

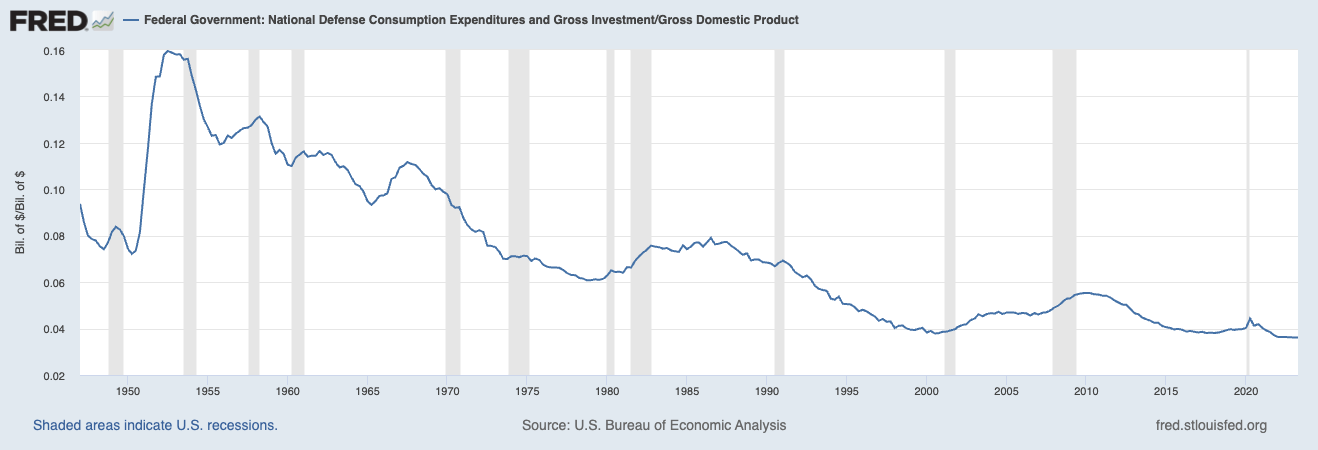

- Defense spending is a national security issue, which means it tends to be tied to GDP spending. The chart below shows that total defense spending in the US is hovering close to 4% of GDP, with uptrends during recessions.

- The fact that defense spending jumps as a percentage of GDP during recessions is not only caused by negative GDP growth during recessions but also because defense spending tends to rise during recessions. Boosting defense spending is an easy way to stimulate the economy, as hardware like planes have thousands of major suppliers, each having their own suppliers, employing millions of people.

{kind=link}

Federal Reserve Bank of St. Louis

Thanks to these long-term tailwinds, GD has been a great place to be for investors. For example, since January 2000, the stock has returned close to 1,300%, beating the S&P 500 by a wide margin. The lower part of the chart shows that outperformance has been consistent, although GD has become an underperformer since the economic growth peak of 2018. The factors that contributed to temporary underperformance are now fading.

Having said that, the company has more benefits than a wide moat and long-term opportunities.

Demand is going through the roof right now, while earnings are only held back by margin issues that are quickly fading, resulting in a highly favorable valuation that is likely to break the aforementioned post-2018 underperformance trend.

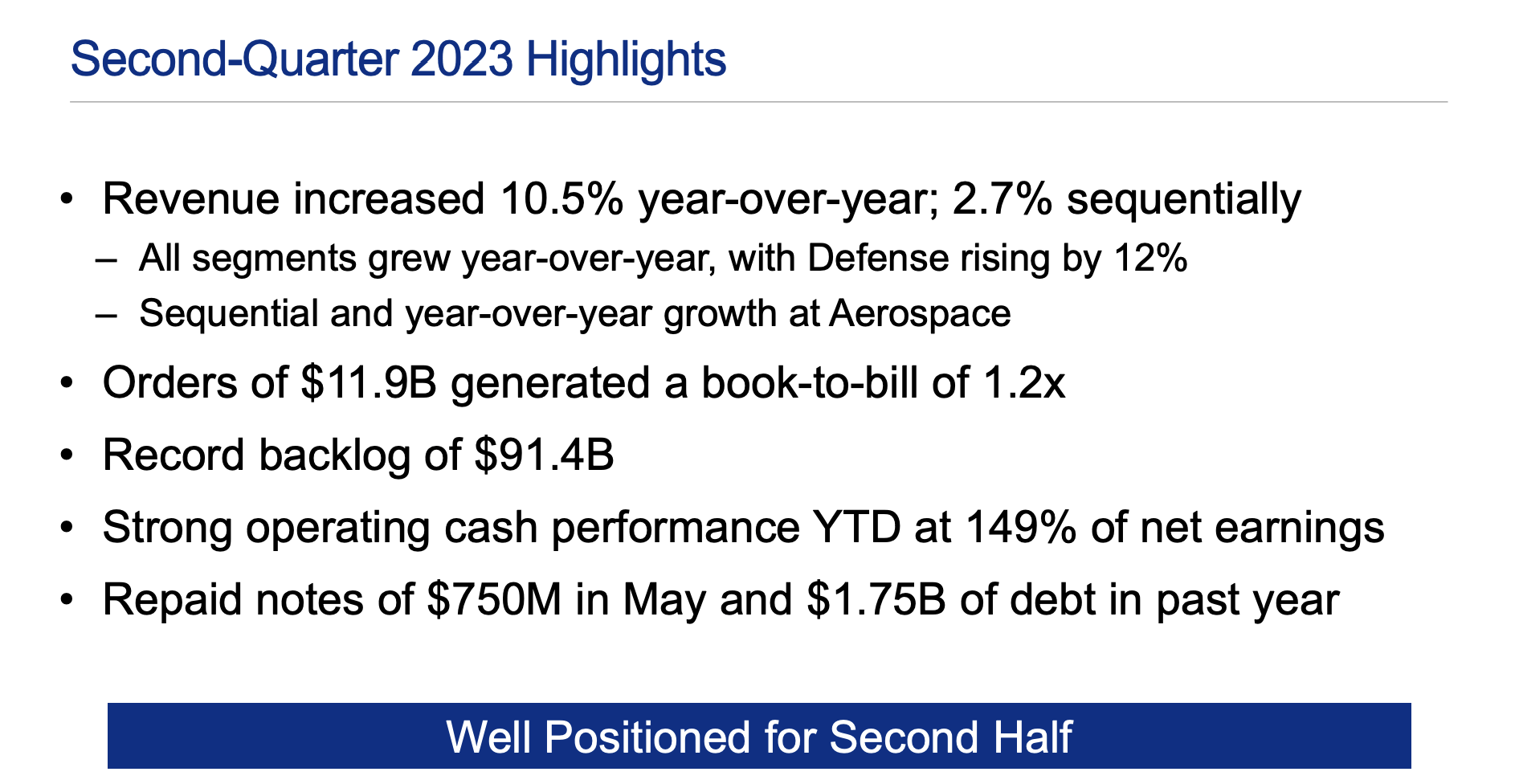

General Dynamics Is Firing On All Cylinders

In the second quarter, the company reported earnings of $2.70 per diluted share on $10.2 billion in revenue, reflecting a 12% increase in the Defense segment and a 4.6% increase in Aerospace.

{kind=link}

General Dynamics Corporation

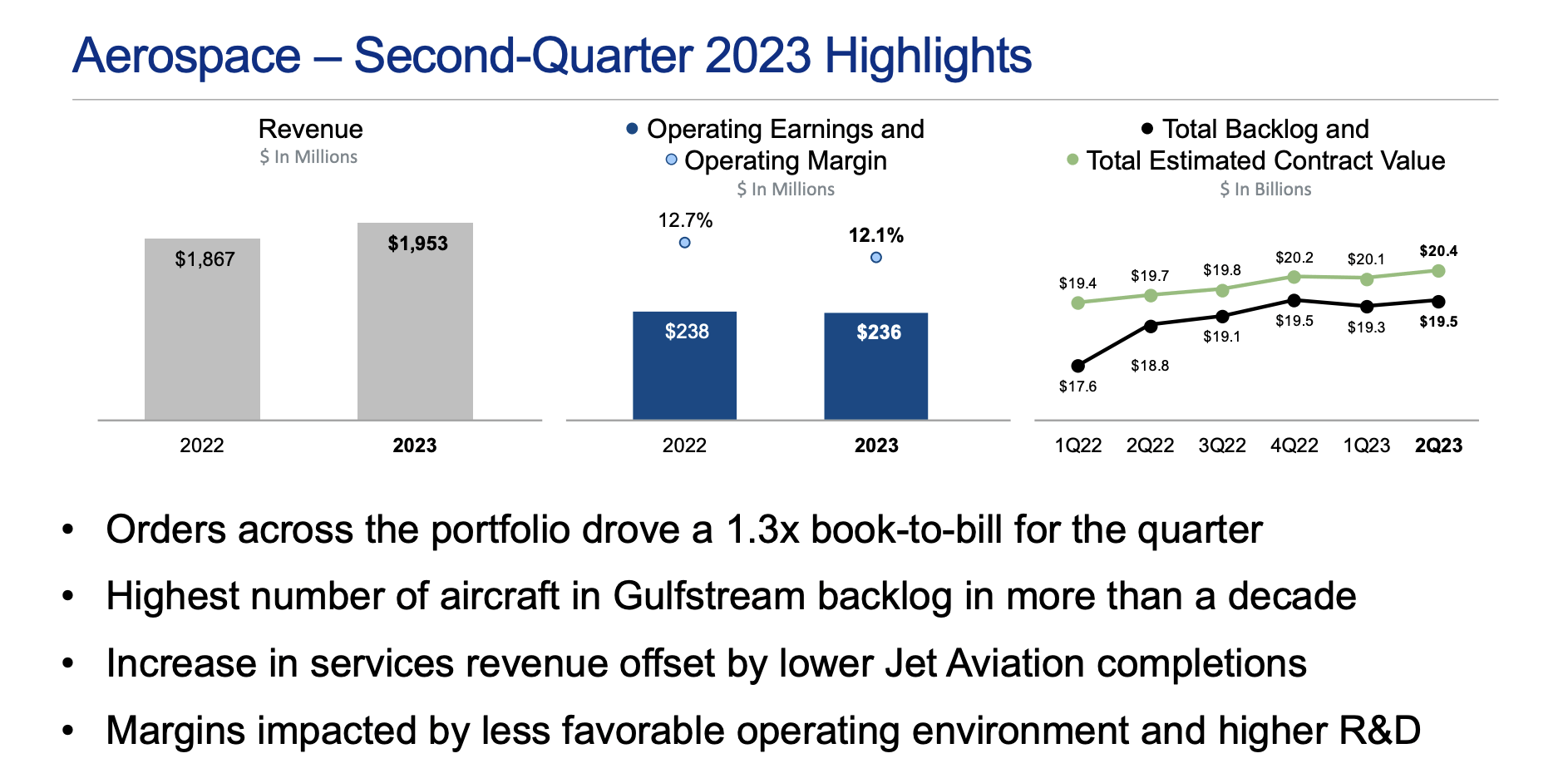

In the Aerospace segment, the company reported revenue of $1.95 billion and operating earnings of $236 million, yielding a 12.1% operating margin for the second quarter.

The increase in revenue was driven by additional new aircraft deliveries and higher volume at the company's Gulfstream service center.

However, the completion center at Jet Aviation experienced lower volumes.

Also, supply chain issues led to a slight reduction in planned aircraft deliveries.

The good news is that supply chain conditions are improving, leading to better transparency and predictability.

The company is also seeing strong demand in this segment.

Vibrant sales activity and strong pipeline replenishment were evident in the quarter. The U.S., particularly large corporations, led the way with the Mid East and Asia participating to a lesser degree. - General Dynamics 2Q23 Earnings Call

{kind=link}

General Dynamics Corporation

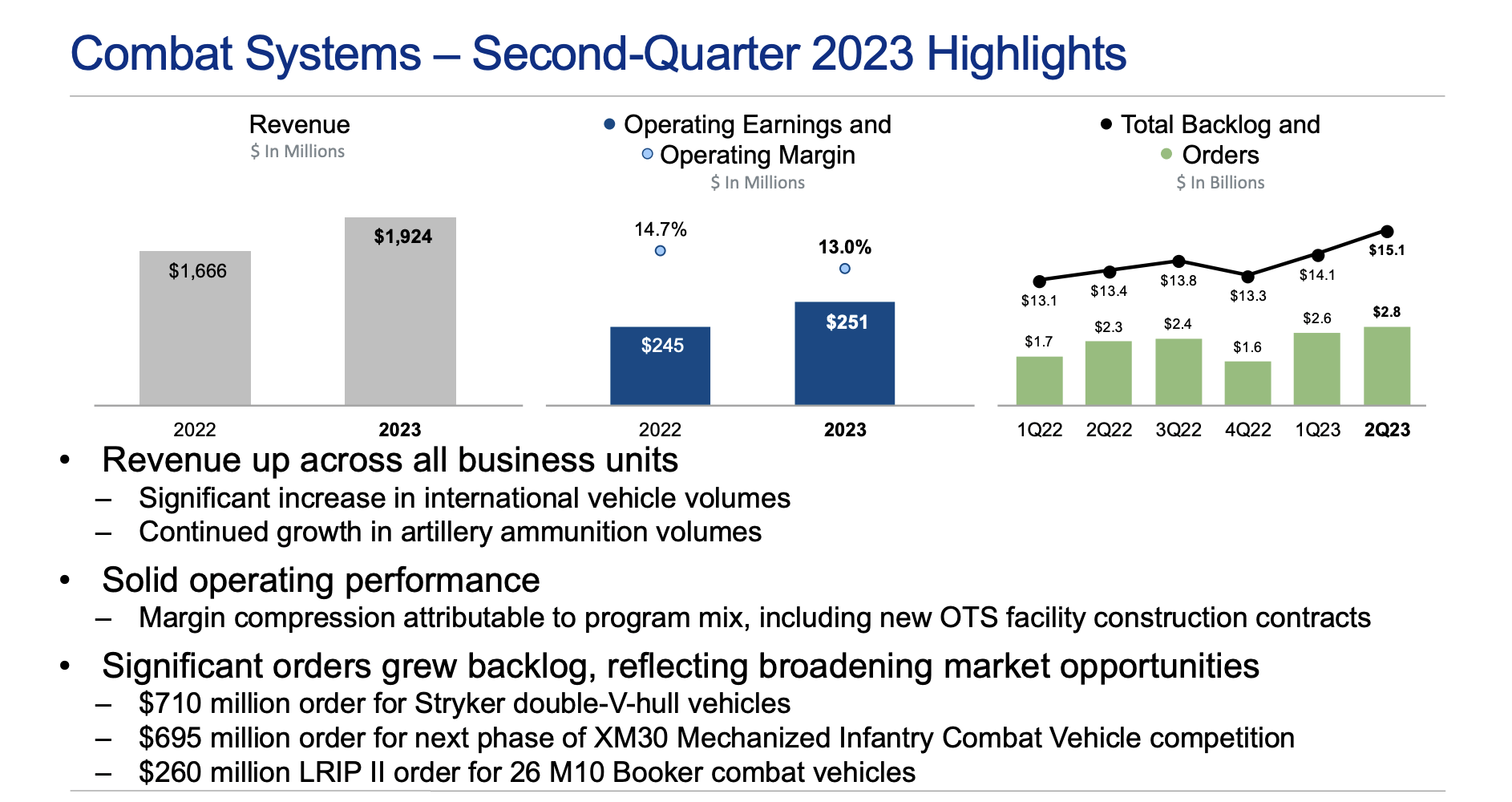

As impressed as I am with the Aerospace segment, the Combat Systems segment saw impressive growth, with revenue reaching $1.92 billion, a 15.5% increase over the prior-year quarter.

Despite a reduction in margins due to the program mix, the segment saw strong order performance, resulting in a book-to-bill ratio of 1.4x.

Essentially, this means that for every $1.00 in finished products, the company gets $1.40 in new orders, which is indicative of future growth.

Not only that, but according to General Dynamics, the Combat Systems segment is poised for further growth due to ongoing demand for munitions and domestic combat vehicles, as well as international programs.

{kind=link}

General Dynamics Corporation

The Marine Systems segment also demonstrated impressive revenue growth, with a 15.4% increase to $3.1 billion compared to the previous year's quarter.

This growth was driven by Columbia-class construction and engineering volume, with incremental margin growth expected over time.

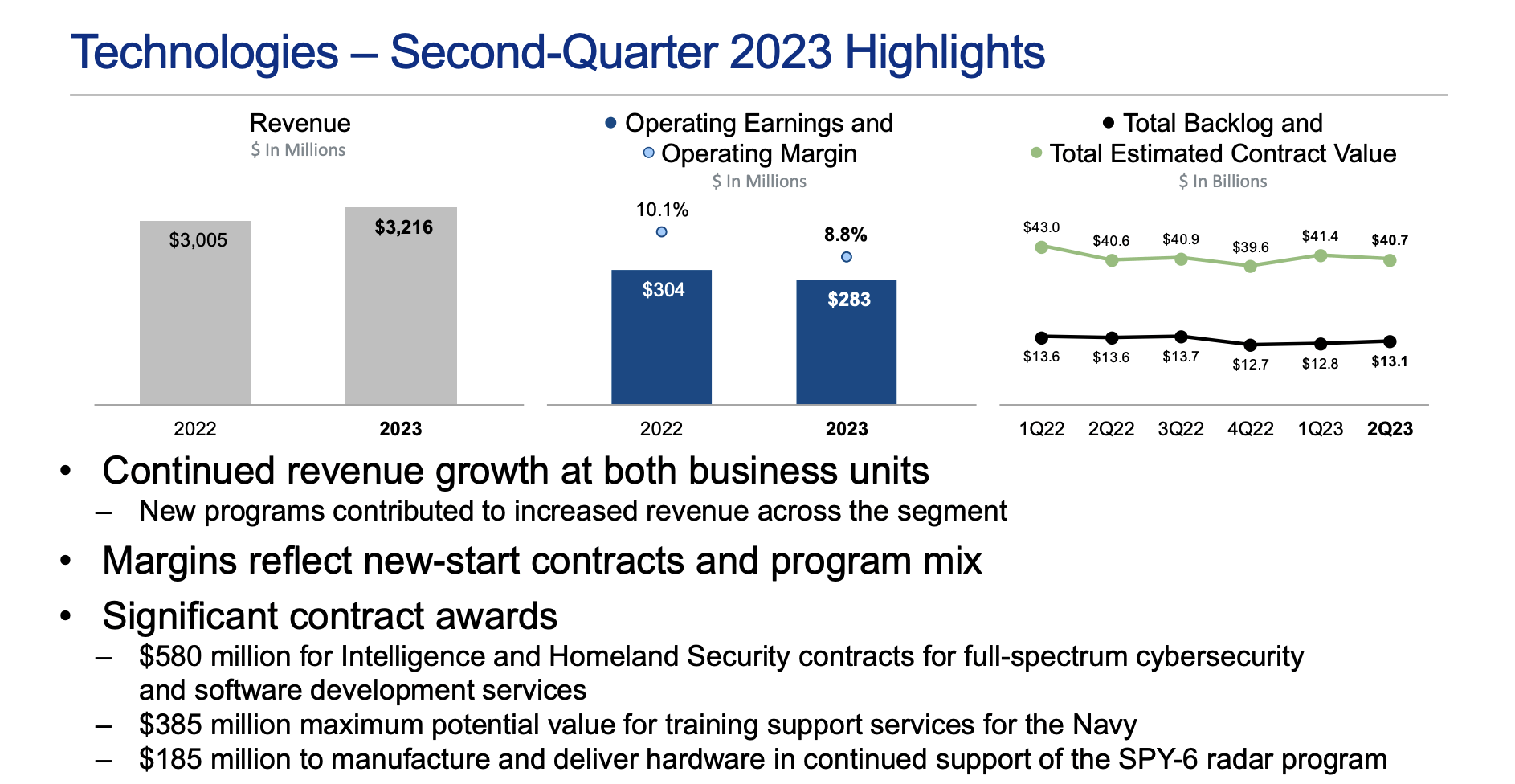

Last but not least, GDIT achieved its highest second-quarter revenues since before the pandemic, continuing its steady year-over-year growth trajectory.

Operating earnings for the quarter reached $283 million, with a margin of 8.8%. Margins were influenced by the mix of IT service activity, hardware volume, and the impact of new start programs.

{kind=link}

General Dynamics Corporation

When combining all segments, the company has no segment with a book-to-bill ratio of less than 1x, which is great. It also sets the company apart from most of its peers.

Even better, the company-wide book-to-bill ratio is 1.2x, driven by a 1.4x ratio in Combat Systems and 1.3x in Aerospace.

As a result, the quarter ended with a record-level backlog of $91.4 billion, which marks a 1.7% increase from the previous quarter and a 4.3% increase from the prior-year quarter.

The total estimated contract value, including options and IDIQ contracts, surpassed $129 billion at the end of the quarter.

Guidance Wasn't Great. But...

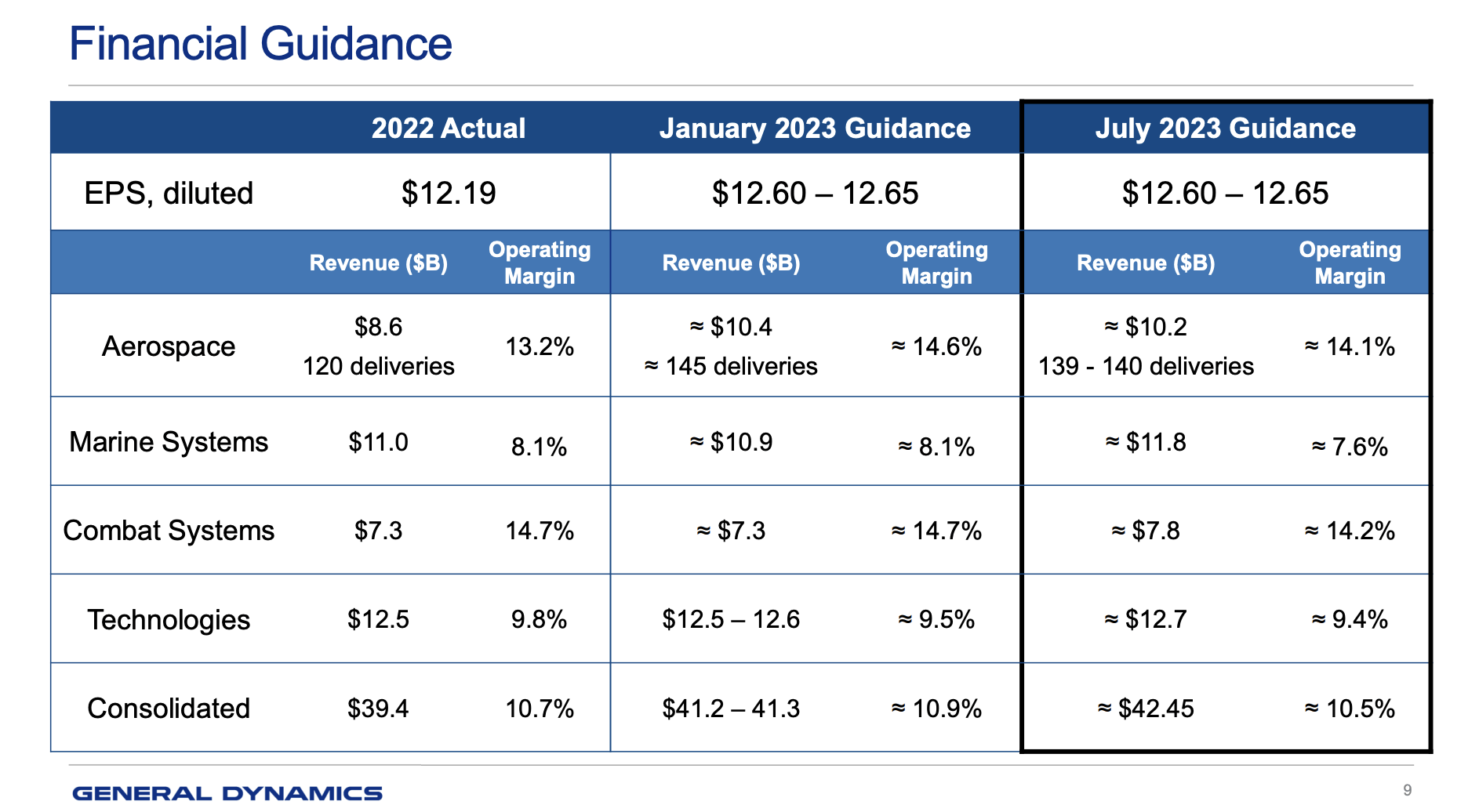

Looking at the overview below, we see that the company stuck to its January 2023 guidance, which sees a full-year diluted EPS range of $12.60 to $12.65.

However, the company adjusted margins in all segments. The only reason why EPS guidance was unchanged is due to higher revenue expectations, offsetting lower-than-expected margins.

{kind=link}

General Dynamics Corporation

- In the Aerospace segment, revenue guidance was adjusted by $200 million due to lower aircraft deliveries, offset by stronger service activity. Margins are projected to be slightly down.

The Defense businesses, including Combat Systems and Marine Systems, are anticipated to perform well, at least when it comes to revenue guidance, which was upgraded across the board.

- Combat Systems revenue is projected to be $400 to $500 million higher due to new program starts and an increased threat environment.

- Marine Systems revenue is expected to increase by $900 million to $1 billion due to accelerated work throughout its yards, indicating improving efficiency.

- Technologies revenue is forecasted to be better than previous guidance, with a slightly lower operating margin.

Overall, the company expects total revenue of around $42.45 billion, about $1.2 billion higher than previous guidance, with operating earnings of around $1.2 billion, consistent with prior guidance, with the main reason being much higher global defense requirements.

However, while the company acknowledges strong tailwinds, we'll have to wait until 2024 to get a better understanding of the duration and total dollar value of these tailwinds.

With respect to Combat, the world has become a less safe place, and that’s reflected in the increased demand, both internationally and in the United States. So we expect the -- this year to be considerably higher than last year. And we’ll give you clarity around 2024 in January . But as you may recall, we had anticipated flat to down growth in this business segment. Clearly, that trajectory has changed. We won’t be able to -- we can’t quantify it right now, but we’ll give you more clarity on that. - General Dynamics 2Q23 Earnings Call

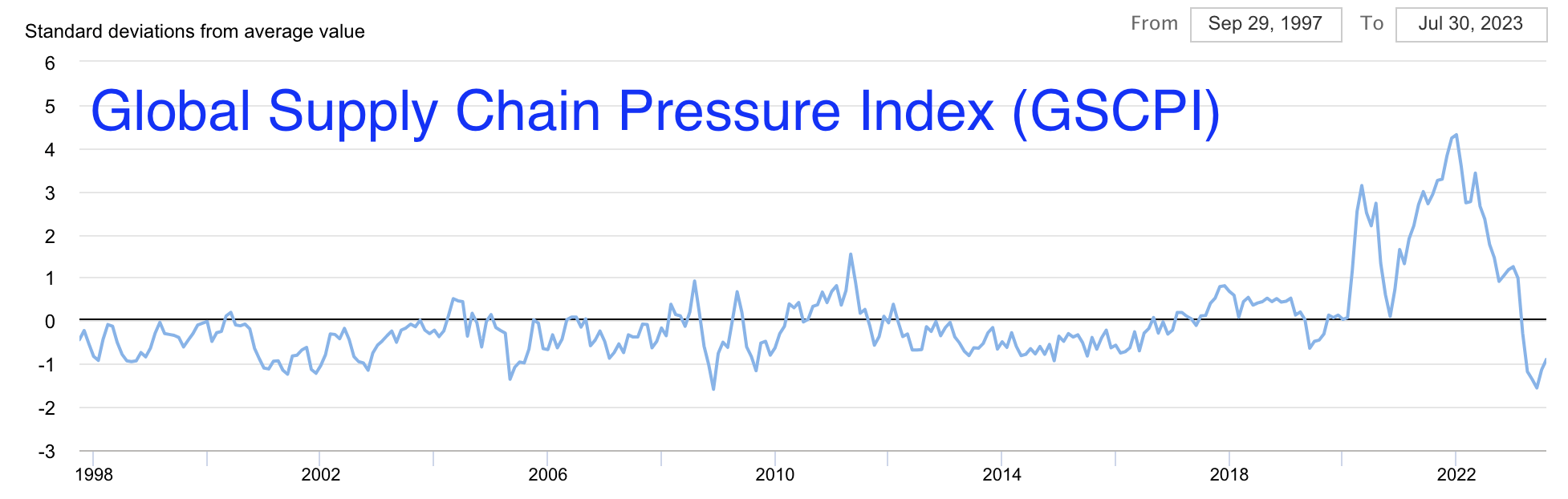

Furthermore, the company sees improvements in its supply chains, which should allow the company to benefit from both higher revenue and accelerating income after 2023.

Supply chain issues and past COVID labor issues have impacted operating margins, but there is relief in sight . We expect improvement as we progress.

In addition to easing global supply chain issues (as displayed by the chart below), the company also sees higher margins in newer programs due to the benefits of a steep learning curve. I expect this to be a strong tailwind in its Aerospace segment.

{kind=link}

Federal Reserve Bank of New York

Having said that, shareholders also remain in a terrific place.

Shareholder Distributions & Valuation

In 2Q23, the company generated a lot of cash. Free cash flow came in at $519 million, bringing the year-to-date number to $1.8 billion. This indicates a 123% cash conversion rate, which is indicative of high-quality earnings.

In the second quarter, GD paid $360 million in dividends and repurchased 1.4 million shares for $288 million.

The company also repaid $750 million of debt, lowering net debt to $8.6 billion. In the third quarter, the company is expected to repay an additional $500 million in debt.

This year, the company could end up with a net leverage ratio close to 1x (EBITDA). It has an A- credit rating.

Having said that, the company currently yields 2.4%. This dividend has a payout ratio of 43% and a five-year average annual dividend growth rate of 7.8%.

On March 9, the company hiked by 4.8%, which maintains a dividend growth streak of more than 30 consecutive annual hikes, making it a dividend aristocrat.

While dividend growth has come down, I expect it to accelerate after 2023, when GD benefits from both easing supply chain issues and strong orders.

Moreover, over the past ten years, GD has bought back more than a fifth of its shares, which contributed to earnings per share growth and its favorable stock price performance.

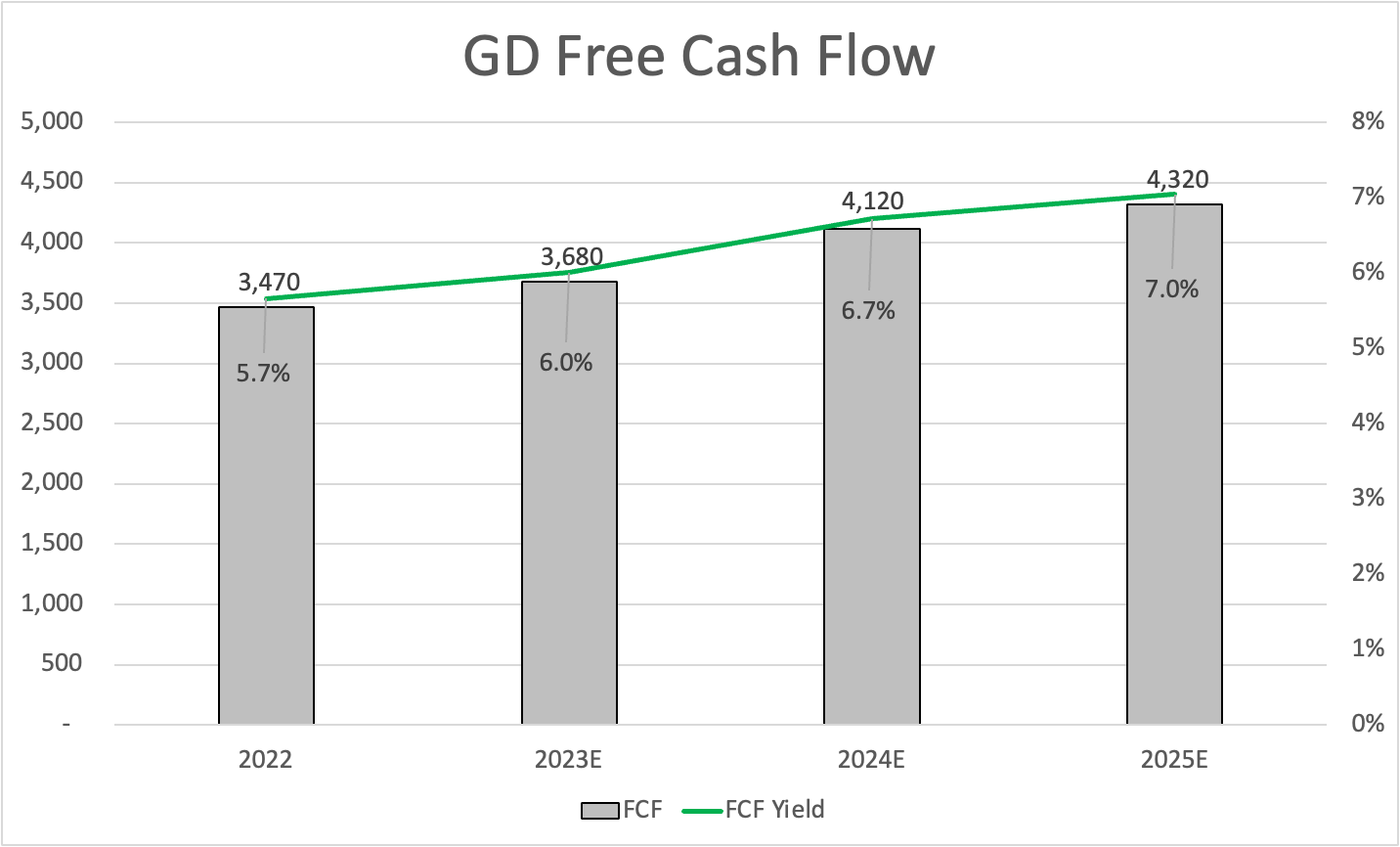

With regard to the valuation, the company is expected to grow its free cash flow by roughly 8% per year between 2022-2025E. Not only does this pave the road for higher dividends, but it also indicates a path to a 7% free cash flow yield, which is very attractive.

{kind=link}

Leo Nelissen (Based on analyst estimates)

Using the company's 2024 estimates, it's trading at 14.9x FCF.

This is a very favorable valuation.

In my prior article, I made the case that GD should not trade below 20x free cash flow, especially not given the aforementioned long-term tailwinds.

The current consensus price target is $264, which is 17% above the current price.

I'm more bullish than that and believe GD should not trade below $280.

Furthermore, after a few challenging years, I expect GD to start outperforming the S&P 500 again on a prolonged basis, backed by strong order growth, easing supply chain issues, strong buybacks, and improving dividend growth.

The only reason why I do not own GD is because I already own four defense contractors. It wouldn't benefit diversification if I added a fifth one.

Takeaway

General Dynamics is thriving across all segments, driven by post-pandemic aerospace growth and a renewed focus on military hardware due to global events.

While supply chain challenges persist, they create opportunities for improvement, with major indicators pointing at significant tailwinds in 2024.

General Dynamics also boasts a solid moat, diversified revenue streams, and resilience in recessionary times. Its recent earnings confirm a promising trajectory, with impressive growth across its divisions.

With a strong order performance and a related growing backlog, the company is poised for long-term revenue growth.

Though its guidance is cautious, the long-term outlook remains bright, setting the stage for potential outperformance and elevated dividend growth for many years to come.

Given my bullish outlook, my rating remains Strong Buy .

For further details see:

General Dynamics: A Significantly Undervalued Dividend Aristocrat