GD - General Dynamics: Buying Ahead Of Earnings

2023-09-13 13:14:40 ET

Summary

- General Dynamics offers steady income through dividends. They have raised dividend distributions for over 25 years straight.

- The stock has an attractive valuation, with a price-to-earnings ratio below the sector average and a strong pipeline of contracts to reinforce future cash flows.

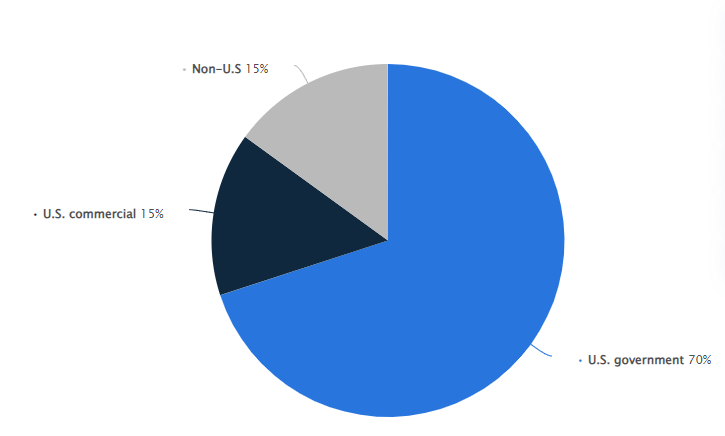

- General Dynamics obtains 70% of their revenue from government secured contracts.

Thesis

General Dynamics ( GD ) is a stock worth considering for investment due to several factors. It is a well-established defense company with a proven track record, offering steady income through dividends. The dividend yield is 2.4%, which is above the sector average of 1.51%. The stock also presents an attractive valuation, with a price-to-earnings ratio below the sector average and a reasonable price-to-book ratio.

Additionally, the current share price, around $217, is within a trading range that suggests it could be a buy opportunity before the next earnings report at the end of October. GD has a strong revenue engine and a backlog of contracts, making it a reliable long-term investment option. I plan to buy before earnings because to me, it doesn't matter what the upcoming earnings report states. I don't think it's wise to let short term noise, if there is any at all, take away from the opportunity to buy into a high quality company.

Dividend

General Dynamics offers a modest dividend yield of 2.4%, paying $5.28 per share. While this yield may not be exceptional, the 5-year growth rate makes me happy at 8%. GD is also a dividend aristocrat; a company that has increased dividend payouts for over 25 consecutive years. For comparison, the average dividend yield of the sector sits at a very small 1.5% alongside the sector's average 5-year growth rate of 7% per year.

Against their competitors, GD is doing pretty well in the dividend growth department. This is further reinforced by the fact that the payout ratio sits at a comfortable 42%. I think that with their strong cash flows, we are likely to see continued dividend increases, especially since GD is more incentive to continue raising the dividend since they have already achieved the aristocrat milestone. I think GD is the best pick for investors looking to get some exposure to the industry while also getting an up-front distribution that can be more easily scaled compared to the lower yielding competition.

Financials - Continued Growth

Cash flow remains strong with a net income margin of 8.2% compared to the sector median net income margin of 6.2%. GD also manages to maintain strong cash from operations at $4B! From their 2Q23 earnings results , they reported a 10.5% YoY revenue growth totaling $10.2B.

Net cash provided by operating activities in the quarter totaled $731 million. For the first half of the year, net cash provided by operating activities totaled $2.2 billion, or 149% of net earnings. During the quarter, the company repaid $750 million in fixed-rate notes, invested $212 million in capital expenditures, paid $360 million in dividends, and used $288 million to repurchase shares, ending the quarter with $1.2 billion in cash and cash equivalents on hand. In the previous 12 months, the company reduced total debt by $1.7 billion. - GD 2Q2023 Financial Results

While prior earnings reports have zero link to how well the upcoming earnings will be, it still paints a picture of strong cash flow to weather out a few bad storms. So even if this upcoming earnings is mediocre, I wouldn't let it bother me too much. GD's revenue per share has increased from $103/share in 2017 up to an estimated $149/share by the end of 2023. This represents a growth to revenue per share of 45%. GD's total long term debt has also seen steady declines. Their long term debt levels declined 5% YoY as of the most previous quarter end.

GD Combat System Contract Backlog

GD's ability to secure government contracts with long-term revenue visibility makes it resilient to economic downturns. GD was awarded a $768M fixed-price contract and the work is estimated to be completed December of 2027. Some other contracts in the pipeline consists of $580M for intelligence and homeland security, $385M for Navy training support services, and $185M to manufacture and deliver continued radar support. These contracts will keep GD loaded with cash, and I plan to get my fair share by continuing to hold for each of the upcoming dividend distributions.

{kind=link}

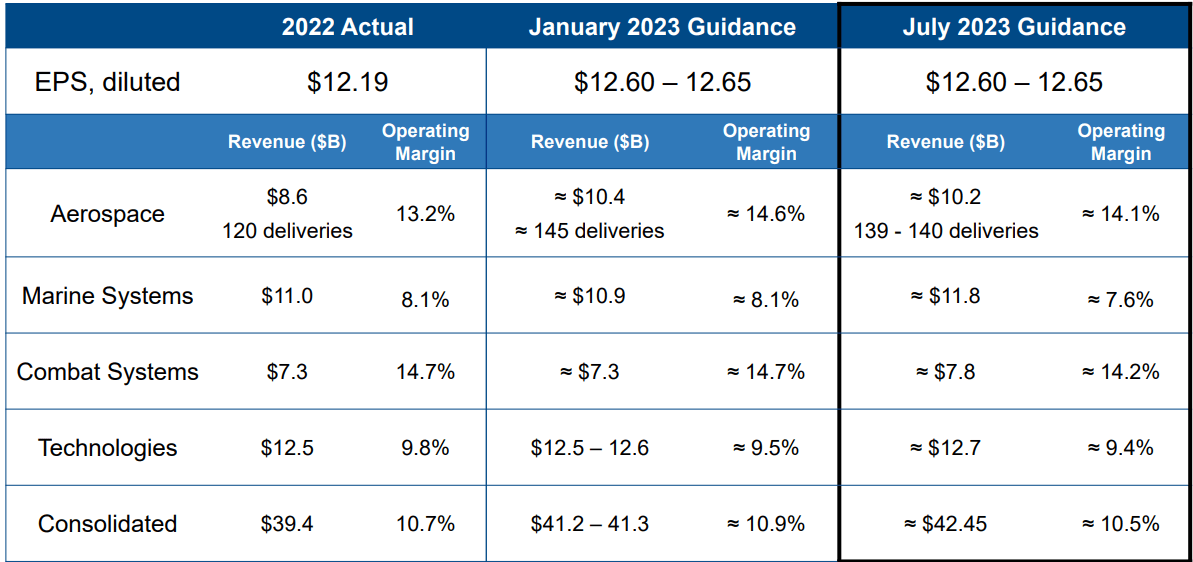

The company also demonstrates a strong cash flow conversion, with free cash flow representing 123% of net income. GD has been reducing its debt load strategically, maintaining a safe net debt to EBITDA ratio of 2.0x. This strong financial position contributes to its A- credit rating. GS continues to operate with strong margins in each category of their business. According to the latest investor presentation , the operating margins are as follows:

- Aerospace: 14.1%

- Marine Systems: 7.6%

- Combat Systems: 14.2%

- Technologies: 9.4%

GD has also been implementing debt reduction strategies as they've managed to knock out $1.75B worth of debt in 2023 so far with $750M of notes repaid in May alone.

Trades Under Fair Value

According to Seeking Alpha's earnings page for GD, the estimated EPS for 2023 sits at $12.65. If we base the future projections off of previous earnings growth, we can settle for an average YoY EPS growth rate of about 5%. Management projects an average revenue growth rate of 9%. If we want to take a conservative estimate, we can project a future growth rate of roughly 7%. Using these metrics, we can identify that going into 2024 there is a fair stock value of $241 per share. This would represent a possible upside of 11% going into next year. While this is a very slight discount to fair value, we are more interested in buying for the long term gains that are possible.

Money Chimp

GD's strong cash flow alongside their strategic debt reduction pay-down makes this an attractive buy for me. As more contracts get confirmed, we can expect GD to continue sitting on fat piles of cash. Even though the current price action trades at only an 11% discount, management's forecasted 9% annual revenue growth goal alongside a commitment to growing the dividend makes this an interesting opportunity.

Risk

General Dynamics relies heavily on government contracts for its revenue. About 70% of their total revenue comes from government spend. Any reduction in defense budgets, changes in government priorities, or delays in contract awards can significantly impact the company's financial performance. Government shutdowns or budget constraints can also disrupt contract execution. Although, this was more relevant at the height of the Russia-Ukraine conflict. Impact risk from this isn't completely off the table as the conflict is still ongoing, but I am not stressing it.

{kind=link}

This large dependence on government contracts / spend isn't uncommon in this space, but it's worth mentioning because 70% is a large concentration. The defense industry experiences contract wins and losses, leading to earnings volatility. The timing and magnitude of contract awards can significantly impact financial performance from quarter to quarter. As we await the next earnings report, any indication of change in these funding areas can cause a drastic stock price reaction. Any sort of negative news can also lead to the price being suppressed for an extended period of time.

Conclusion

General Dynamics ((GD)) presents an interesting investment opportunity for several reasons. GD is a dividend aristocrat, having consistently increased its dividends for over 25 years, and its payout ratio of 42% suggests room for further growth.

Financially, GD demonstrates strong cash flow, outperforming the sector median net income margin, and maintaining strong cash from operations even through uncertain times. With a history of revenue growth and strategic debt reduction, the company is in a favorable financial position at the moment. Its ability to secure long-term government contracts provides resilience to economic downturns, as exemplified by its contract backlog.

However, I think that we should be aware of the risks associated with GD's heavy reliance on government contracts, as any reduction in defense budgets, shifts in government priorities, or delays in contract awards can impact the company's financial performance.

For further details see:

General Dynamics: Buying Ahead Of Earnings