GD - General Dynamics: Cheap Stock On Growth Fundamentals

2023-07-28 10:35:13 ET

Summary

- General Dynamics Corporation's second-quarter results were impacted by supply chain challenges resulting in lower margins.

- The company updated its guidance, with lower margins expected in the Aerospace, Marine Systems, Combat Systems, and Technologies segments.

- Despite these challenges, GD stock is still considered a buy for long-term investors due to its history of dividend increases and attractive product portfolio in the current threat environment.

I have been covering General Dynamics Corporation ( GD ) since the start of this year and have a buy rating on the stock. However, the performance to date has been more or less in line with the performance of the broader market, with a 7% total return and a 6.4% stock price change compared to a 6.9% change for the S&P 500 (SP500). So, you would certainly not have lost money, but General Dynamics stock did not have the outperforming nature I am typically looking for. In this report, I will be looking at the second quarter results and revisit my price target for the company.

Supply Chain Challenges Continue To Hit General Dynamics

{kind=link}

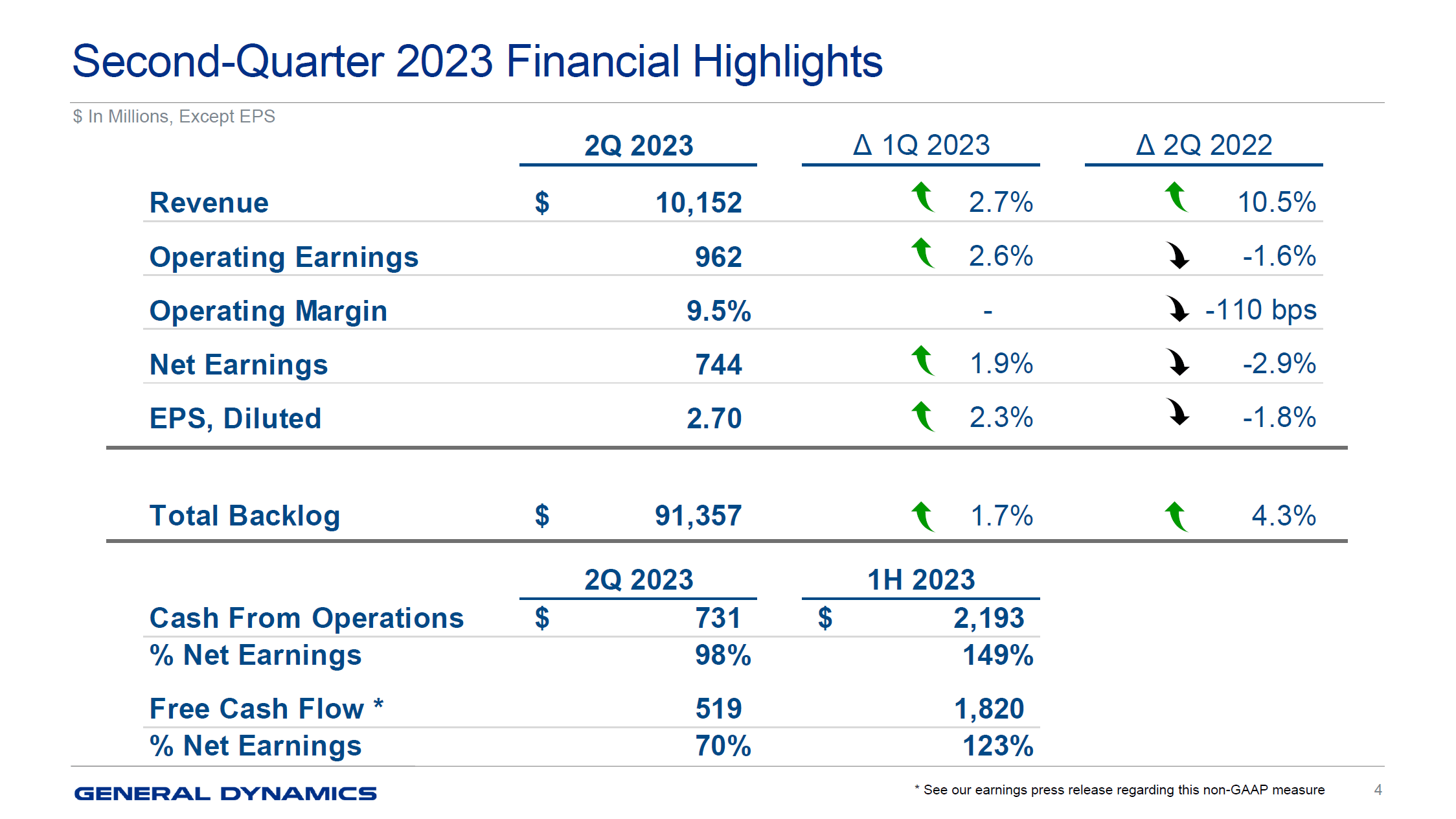

While we do see quite some green arrows in the slide above, I would say that the overall performance has not been favorable. Compared to the first quarter, we see low single-digit growth in revenues and earnings, but year-over-year we see that a 10.5% higher revenue did not translate into higher earnings. In fact, earnings were lower, driven by a 110 bps margin contraction due to supply chain challenges and revenue mix.

General Dynamics has four reporting segments, namely Aerospace, Combat Systems, Marine Systems and Technologies. In the Aerospace segment, revenues increased by $86 million to $1.953 billion or a 4.6% increase. However, due to supply chain challenges, none of the top line growth translated into higher earnings. In fact, earnings were down 0.8%. Overall, supply chain issues do pressure the top line, but also affect the cost efficiency as more out of station work is required which reduces the manufacturing efficiency.

In Combat Systems, sales grew 15.5% while profits grew 2.4%. So, also in combat systems, we saw most of the top line growth being offset by lower margins. Revenues increased by higher Land Systems sales and higher artillery program volume. These programs are not accretive to margins in the current phase of the program, resulting in margins to drop from 14.7% to 13%.

For Marine Systems, we did see strength, with sales growing by 15.4% to $3.059 billion and profits increasing 11.4%, with margins dropping from 8% to 7.7% due to ongoing supply chain challenges that are primarily affecting the Virginia-class submarines.

The Technologies segment saw 7% sales growth, but its profits were 7% lower due to a margin decline from 10.1% to 9.5%. This was driven by new programs boosting the revenues but not bringing the solid margin performance to the bottom line yet.

Overall, the story for the second quarter results from General Dynamics was in some way similar to the prior quarter. We did see revenue growth, but supply chain issues and mix continue to put a damper on results.

General Dynamics Updates Guidance To Reflect Lower Margin

{kind=link}

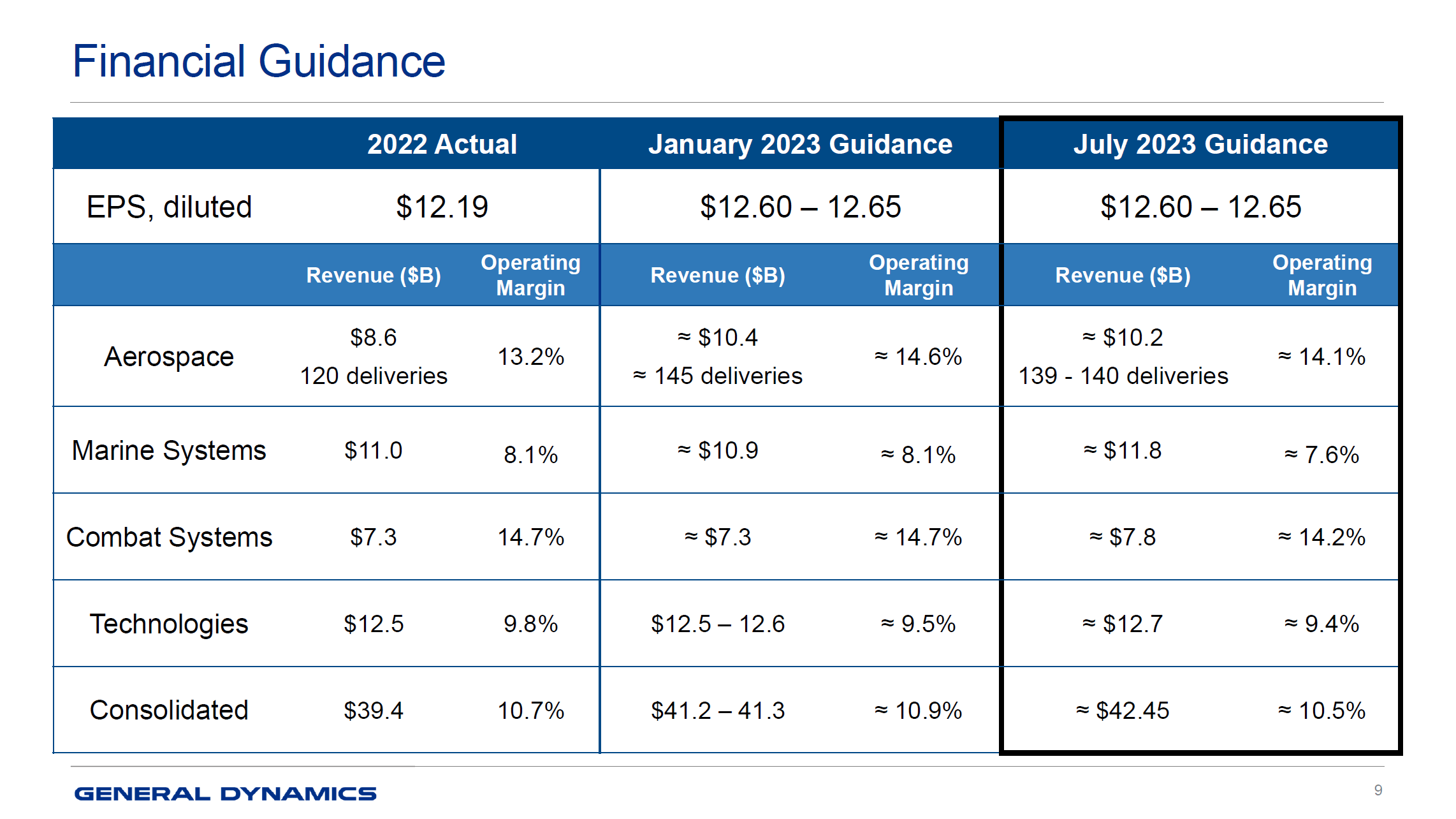

The second quarter results triggered General Dynamics to also update its guidance. For Aerospace, the continued supply chain issues are pushing the certification of the G700 into the fourth quarter, of which some could spill over into 2024, resulting in a $0.2 billion decrease in forecast revenues and a 0.5 percentage point margin headwind. Marine systems will be $0.9 billion higher than previously guided, while Combat Systems will be $0.5 billion higher on lower margins driven by mix. Technologies will be up $0.1 billion on lower margins as well. So, with the exception of Aerospace, we see that revenues will grow, but margins will be lowered, leading to a guidance that indicates 5% growth in operating earnings compared to 2022, but a modest decline in operating earnings compared to what was guided for earlier.

Is GD Stock A Buy?

With the margin pressure and supply chain issues, one can wonder whether General Dynamics is still a buy. For proper context placement, I think it is important to realize that the Q1 performance is not to be projected forward. For instance, in the first two quarters, G700 jets will be built that won’t be delivered from Q4 onward and the supply chain challenges are easing according to General Dynamics. That indicates to improvement in the remainder of the year. Furthermore, General Dynamics has a streak of 27 years of dividend increases, and while its 2.35% yield might not be juicy, coupled with a strong history of dividend increases it is a strong pointer that a very nice yield-on-cost can be built over time. So, I wouldn’t want to look at quarterly results to tell anyone to not hold this stock because its history shows strong return to shareholders via dividends.

{kind=link}

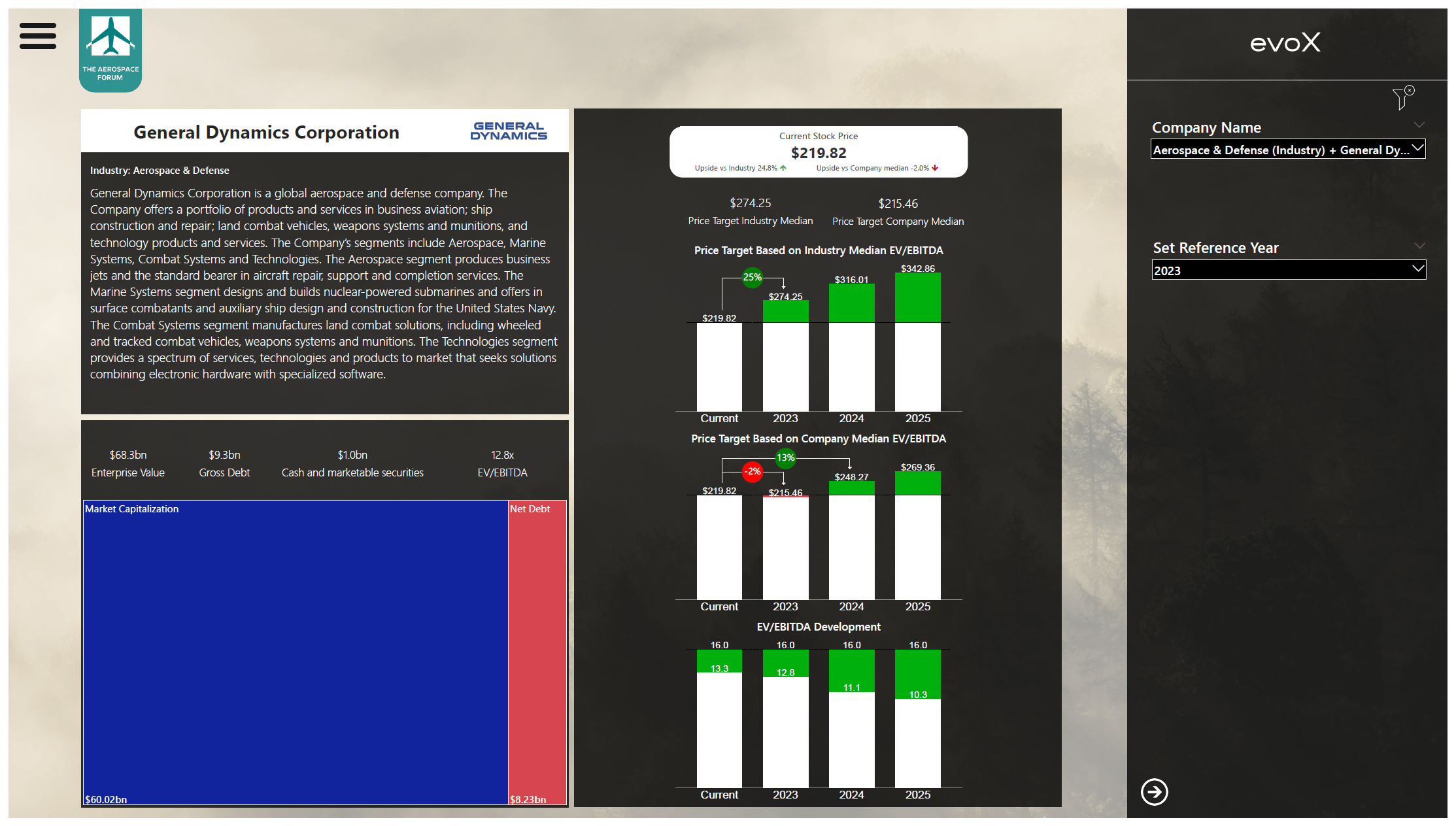

Utilizing the evoX Financial Analytics tool, we see that General Dynamics is undervalued compared to its peers. Using its own usual enterprise to EBITDA multiple, we see that the stock is more or less fairly valued with 2023 performance in mind, or said differently: 2023 earnings are already factored in. However, compared to the industry multiple, there is around 25% upside to $274 per share, which is higher than the $264 per share price target that Wall Street has for the stock. It seems that General Dynamics tends to trade with the current year projections in mind.

As we transition to the next year, that would indicate at least 13% upside for the stock, which layers on top of buybacks and dividend increases to make the stock more attractive. So, valued in line with its peers 25% upside exists compared to the current year financial results and valued one year ahead against its own EV/EBITDA multiple 13%, upside exists for General Dynamics Corporation stock.

So, I do believe that with the forward projections in mind, General Dynamics is a buy.

Conclusion: General Dynamics Is For The Long-Term Investor

The General Dynamics Corporation second quarter results were pressured by supply chain issues and negative mix, but this year we will already see some improvements, as pre-built G700s will start delivering and supply chain challenges will ease modestly. Overall, General Dynamics Corporation is for the long-term investor, in my view. The company has a solid track record of increasing its dividends, and its forward earnings show upside to the stock price for all years, excluding one scenario, whether you value the company in line with its peers or to its median enterprise-to-EBITDA multiple. So, I do believe that General Dynamics Corporation is a more than solid stock for shareholders to buy and hold.

For further details see:

General Dynamics: Cheap Stock On Growth Fundamentals