GD - General Dynamics Is A Buy Despite Uncertain Pentagon Spending

2023-10-16 02:22:56 ET

Summary

- General Dynamics shares have rallied due to the Israelis-Hamas conflict and have returned about 11% since my buy recommendation.

- The company's earnings were down from last year due to margin pressures and ongoing supply chain challenges that should reverse and provide a tailwind to growth.

- GD has a strong backlog and is less sensitive to political gridlock, making it relatively immune to certain political risks.

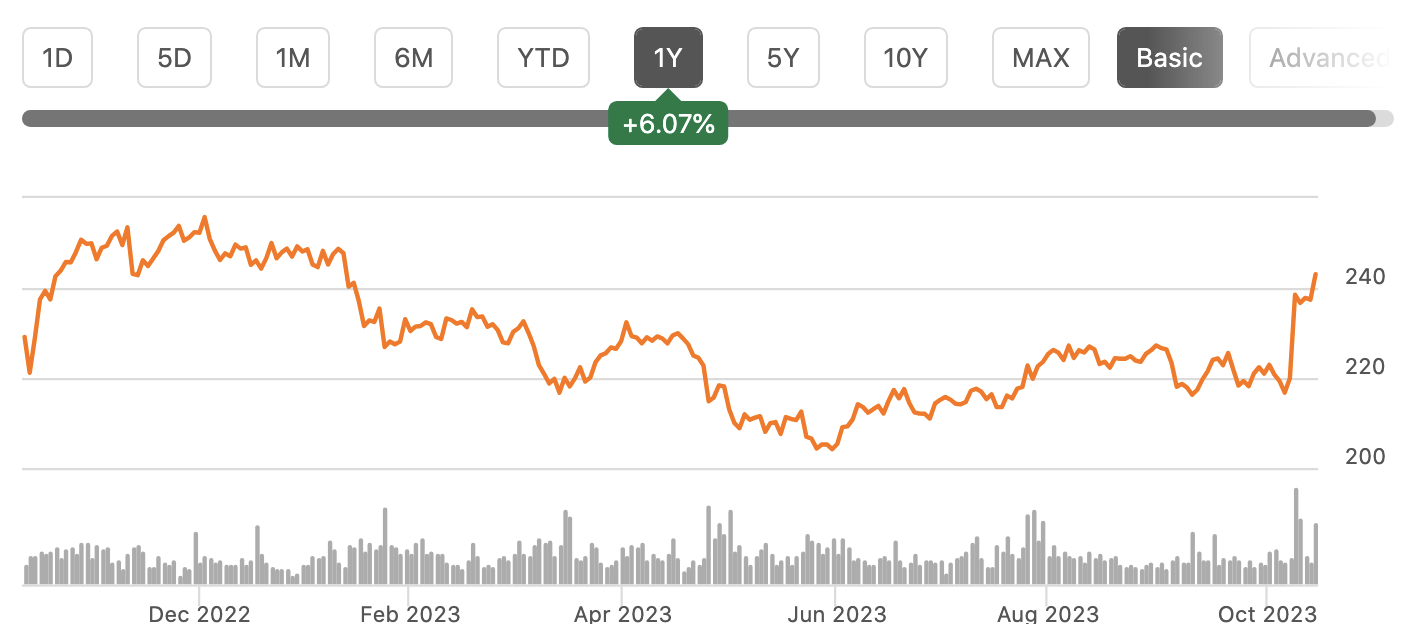

Shares of General Dynamics ( GD ) have rallied in recent days towards 12-month highs in the wake of the Israelis-Hamas conflict. Since recommending shares last October , they have returned about 11%, aided by the recent rally. While the defense spending outlook is more uncertain than I expected it to be a year ago, this conflict is a reminder of how events can force spending higher. Additionally with the nature of its backlog, GD is about as immune from political gridlock as a defense contractor can be. While shares are not "cheap," its premium valuation is deserved.

{kind=link}

In the company's second quarter , General Dynamics earned $2.70, which was down from $2.75 last year even as revenue increased by 10.5% to $10.2 billion. This is because the company has continued to face margin pressures due to higher R&D spending and primarily ongoing supply chain challenges. As such, operating margins fell by 110bp to 9.5%.

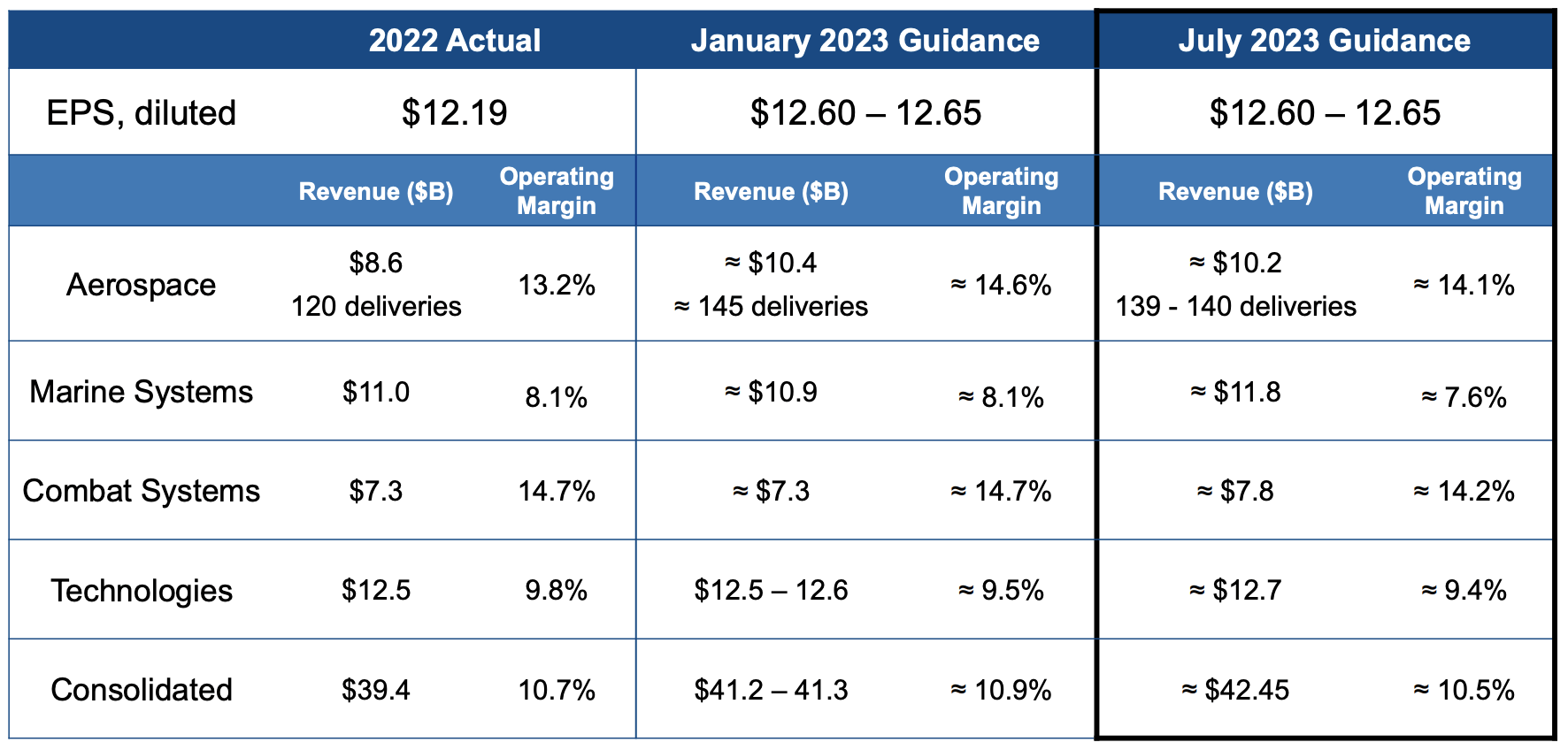

COVID disruptions have taken a long time to resolve, in part because many workers require security clearances, lengthening the time to bring manufacturing production of parts across the entire supply chain back to normal. Importantly, management expects to see incremental and steady margin growth from here, particularly out of its marine unit as supply chains are getting better. As you can see below, GD raised its revenue guidance by over $1 billion in July while holding its EPS guidance flat, as it assumes a slower trajectory of margin recovery.

{kind=link}

In my recommendation last October, I suggested GD would earn about $12.20 over the next twelve months as I have been taking a "wait and see" approach to margin improvement, and GD is poised to exceed this target on the back of its strong revenue growth of 8% alongside modest share count reduction from its buyback program. 3% EPS growth in the face of margin deterioration is a very favorable outcome and points to the potential for meaningful earnings acceleration as the supply chain continues to repair.

Across units, if we first address Aerospace, this is GD's only unit that is primarily nondefense, as it manufactures the popular Gulfstream jet (a market leader in the private/corporate jet sector). Revenue was up about 5%, but that should accelerate as deliveries ramp. As you can above, deliveries will run 5 short of prior guidance; this is due to supply chain issues, not a demand problem. In fact, there are more Gulfstreams in the backlog than at any time in the past decade.

Elsewhere, combat systems were a standout revenue-wise, up 15% to $1.9 billion, aided by increased ammunition and tactical systems sales, which are somewhat lower margins. This unit is a prime beneficiary of emergency funding to assist Ukraine in its war with Russia. It would also be the unit likely to see the most incremental demand from aid for Israel, should a package materialize.

Marine systems revenue was also up about 15% to $3.1 billion. This is the unit with the most compelling secular growth story as GD is manufacturing the new class of nuclear submarines, the Columbia. Critically, its Columbia submarine is on track with the first boat 36% complete. This unit has a $44 billion backlog, driven by Columbia. China is expanding and advancing its submarine fleet dramatically , posing a long-term security challenge that we will want to match with equally advanced submarines. Ultimately, I expect Columbia to be to General Dynamics what the F-35 has been for Lockheed Martin ( LMT ), a cornerstone program generating cash flow and growth for well over a decade, given multiyear build times.

With these solid results, GD has generated $1.8 billion in H1 free cash flow. With that cash flow, it has repaid $750 million in debt last quarter and $1.7 billion the past year. Alongside that, it has bought back $288 million of stock. With just $9.7 billion of gross debt, GD's balance sheet is strong, and its debt reduction has helped to largely immunize the business from higher interest rates.

GD still has $1.2 billion in cash on hand, and with its buyback, share count is down about 1.5% from last year. Over the next two years, I expect to see GD pivot from debt reduction and toward share repurchases with its ~$3+ billion in free cash flow generation, which should lead to somewhat faster share count reduction. General Dynamics also raised its dividend by 5% this past year, and I would expect ongoing mid-single digit increases.

Now last year, given the need to invest more to deter a rising China, alongside the ongoing war in Ukraine, I felt we would likely see sustained Pentagon spending growth, which would buoy the entire defense sector. However, one must recognize the spending outlook is far more uncertain today. Political support for further Ukraine funding is less strong than 12 months ago, though potential Israel needs could lead to a broad, compromise package. It is unclear.

Additionally, this year's debt ceiling deal capped Pentagon spending at up 3.3% or $886 billion for fiscal 2024, though it could pass emergency aid for Ukraine/Israel outside of this limit. However, if Congress cannot pass an appropriations bill for all 12 agencies by January 1; there would be an automatic 1% budget cut based on the debt ceiling agreement. Given the uncertainty in Washington and the fact there is not a Speaker of the House, there is definitely a risk that this automatic 1% spending cut will happen. Government funding expires on November 17th, and January 1 is quickly approaching. We simply cannot be sure where the Pentagon budget will be, or if it will grow.

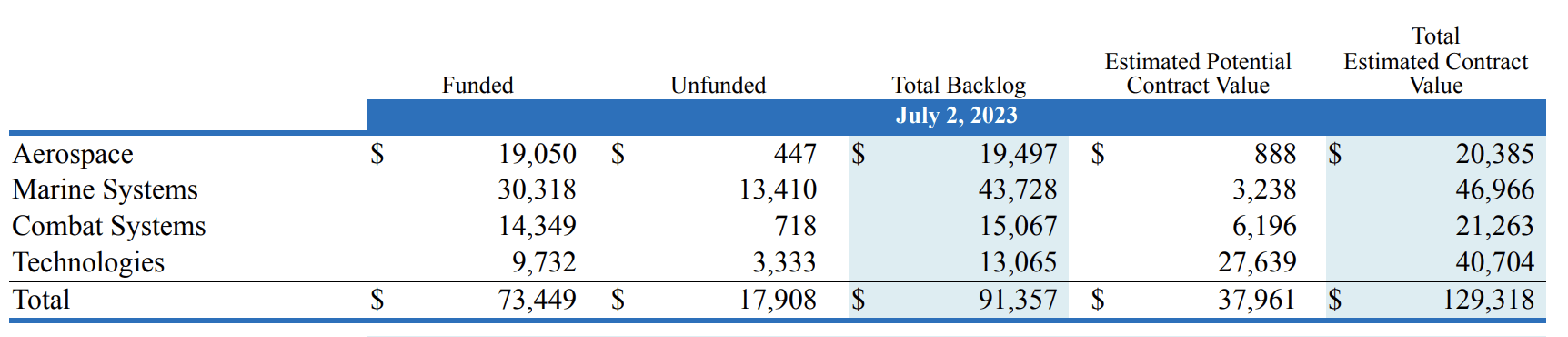

That is not good news for any defense contractor. Importantly, GD is less sensitive to this trend. It has a $91.4 billion backlog, which has been growing. In the last quarter, it had a 1.2x book-to-bill ratio with $11.9 billion in orders. Not all backlog dollars are the same though, as some are funded and some are subject to eventual appropriation of funds from Congress, which may or may not materialize. For General Dynamics, this is less of a concern as over 80% of its backlog is funded.

{kind=link}

While lower Pentagon spending could hit its unfunded backlog or reduce the estimated potential of contracts, that funded backlog provides an important, predictable base of business. This is because when Congress passes appropriations bills; it can allocate money for "advanced procurement ((AP))" for multiyear projects that authorize the Pentagon to spend money in future years. This is essential for a project like Columbia where the submarines take several years to build, so some continuity is required.

Indeed, if we look at Columbia funding as an example, in fiscal 2023 , congress authorized about $5.8 billion in spending for Columbia Class submarines, of which $3.4 billion was AP. The 2024 Senate Appropriations bill (which has yet to become law) authorized another $5.8 billion with $2.8 billion of AP and $3 billion of in-year spending. Some of that $3.4 billion in 2023 AP will be spent in 2024, 2025, etc. This pot of advanced funds provides a trajectory for steady spending and growth.

Defense contractors' primary customer is the US Government, and so there will always be political risk in the revenue outlook, but the nature of GD's backlog helps to reduce this over the short-term given multiyear funding mechanisms. Lower spending will never be a positive for any defense contractor, but it will impact those with shorter-term projects more than GD. Additionally, I do continue to view the medium-term outlook as positive for defense spending, looking past near-term political uncertainty given what appears to be an increasingly dangerous world and a rising China.

Over the next twelve months, I would expect revenue growth to slow somewhat given slower Pentagon spending and tougher comps in aerospace but to see some margin improvement. ~3% revenue growth and a return to just 2022 margins could lead to about $13.20 in EPS over the next twelve months. With another 1.5-2% share count reduction, ~$13.35 is a reasonable target.

That gives shares an 18.2x forward multiple. This is a bit below the market's forward 19.1x multiple.

Given GD's potential for growth to accelerate as Columbia fully ramps in several years and margins are recaptured, alongside its noncyclical business, and medium-term outlook for increased defense spending, I think shares should trade at a premium to the market. Ultimately, I see about 10% upside given my target for a 20x multiple, or about $265-270. Additionally, should geopolitical developments worsen, the outlook for GD would improve, which can provide a useful hedge in a portfolio as geopolitical tensions likely weigh on the broader market. I continue to view GD as a buy despite near-term domestic political risks.

For further details see:

General Dynamics Is A Buy Despite Uncertain Pentagon Spending