GD - General Dynamics Is Poised For Growth And Way Too Cheap

2023-07-09 12:31:20 ET

Summary

- General Dynamics is well-positioned for growth due to demand for its defense hardware and expected growth in munitions and supply chain improvements.

- The company anticipates cash conversion rates above 100% beyond 2023, with free cash flow allocated to dividends and share repurchases.

- Thanks to its current undervaluation, General Dynamics stock presents a compelling investment opportunity due to its growth potential and commitment to shareholder returns.

Introduction

It's time to talk about General Dynamics ( GD ) , a stock I've had on my radar for many years and one of the few defense contractors that's not a part of my portfolio.

As most readers know, I have more than 20% defense exposure, which is based on the importance of this industry and its ability to generate consistent dividend growth and capital gains. It's an innovation play, not a play to benefit from future wars.

Having said that, in May, I made the case that General Dynamics is Too Good To Be This Cheap . Since then, the stock has started to form what looks like a bottom.

Not only that, as we'll discuss in this article, a lot of tailwinds are starting to strengthen. This includes demand for its defense hardware like military vehicles and private jets and expected growth acceleration in munition and supply chain improvements.

From a dividend (growth) investor's point of view, I have to say that I remain extremely pleased with this company.

Not only do I believe that GD shares remain undervalued and in a good spot to accelerate shareholder returns, but I also believe that the next rotation from growth to value will be highly beneficial for GD stockholders.

So, let's dive into the details!

Well-Positioned For Growth

General Dynamics is a well-diversified defense contractor with exposure in a number of highly attractive segments. This is also the reason why I do not own GD shares because my other four defense contractors also cover these areas. Not buying GD was solely based on diversification.

| USD in Million | 2021 | Weight | 2022 | Weight |

|---|---|---|---|---|

| Technologies | ||||

| 12,457 | ||||

| 32.4 % | ||||

| 12,492 | ||||

| 31.7 % | ||||

| Marine Systems | ||||

| 10,526 | ||||

| 27.4 % | ||||

| 11,040 | ||||

| 28.0 % | ||||

| Aerospace | ||||

| 8,135 | ||||

| 21.1 % | ||||

| 8,567 | ||||

| 21.7 % | ||||

| Combat Systems | ||||

| 7,351 | ||||

| 19.1 % | ||||

| 7,308 | ||||

| 18.5 % |

In its Marine Systems segment, the company builds large combat ships, submarines, and other ships that form the backbone of the mighty US Navy.

General Dynamics

In Aerospace, the company mainly builds private jets under its Gulfstream brand. This segment is also the reason why 70% of the company's sales are government sales. Most major competitors have much higher government sales.

General Dynamics

In Combat Systems, the company builds major defense vehicles like the Abrams Main Battle Tank, the Stryker, and various other armored vehicles that are used by NATO defense forces.

General Dynamics

This brings me to the core of this article.

While the company's hardware-focused business was somewhat lagging behind its peers with more next-gen defense capabilities (like Northrop Grumman ( NOC )), General Dynamics is now in a fantastic spot to grow all of its segments.

During this year's annual Bernstein Strategic Decisions Conference , the company highlighted a number of tailwinds and how it expects to grow its business over time.

Gulfstream & Strong Cyclical Demand

Starting with its Gulfstream (Aerospace) segment, the company is mainly focused on profitability instead of market share. In the second half of this year, the company expects certification of its G700 jet, which should allow the company to achieve its goal of pushing aerospace margins to 20%.

With regard to demand, General Dynamics anticipates a book-to-bill ratio of 1, reflecting strong demand from North American public and private companies, moderate demand from Europe, and strong demand from the Mideast and parts of Asia (excluding China).

GD believes that its broad portfolio of airplanes caters well to corporate customers with diverse missions, and high net-worth individuals also contribute to demand.

The company does not believe that a mild recession will damage demand. I agree with that, as we're witnessing that the recession (so far) is mainly in the lower-income groups. Needless to say, as this segment is prone to cyclical demand, steeper recessions will likely lead to an adjustment in expected demand.

Defense Tailwinds & Targeted Spending

As the overwhelming majority of GD's revenue comes from anti-cyclical government orders, the budget is key.

{kind=link}

The FY2024 Defense Bill seeks to boost defense spending by almost 4%.

The Defense bill funds agencies and programs under the jurisdiction of the Department of Defense ("DOD") and Intelligence Community, including the Military Services, Central Intelligence Agency, and the National Security Agency. For Fiscal Year 2024, the bill provides $826.45 billion in new discretionary spending, which is $285.87 million over the President’s Budget Request and $28.71 billion – or 3.6% – over the FY23 enacted level.

While this is below what some market participants may have hoped for, General Dynamics is quite optimistic, as it expects continued support, given the relevance of its major defense programs and the ongoing threats in the world.

While there is some uncertainty related to spending discussions, General Dynamics believes it is well-positioned to fare well based on the strength of its programs.

For example (emphasis added):

- Growth in the Marine group is driven by the national imperative for Navy surface ships and the increasing importance of submarines, particularly the Columbia class. General Dynamics aims to stabilize the industrial base and improve material delivery, throughput, and productivity for the Virginia program . According to the company, as challenges are overcome, considerable growth is expected , especially with the progress of the Columbia program. Furthermore, margin expansion is a key focus for the Marine group, and as they work through challenges, they anticipate achieving the 9% to 10% margin range, which is considered a goal for the business.

Furthermore, GD is making tremendous progress when it comes to hiring and using efficiency gains to offset certain inflation-related pricing headwinds.

{kind=link}

- The war in Ukraine is turning into a massive tailwind for General Electric's Combat Systems segment. Prior to the invasion, the company had anticipated flat to occasional negative growth in combat. However, due to the increased threat environment, there is now an expected low single-digit growth in combat systems. There is improved demand in Europe for combat vehicles, both tracked and wheeled, as well as munitions and bridges. General Dynamics sees potential for further growth depending on the speed of contract acquisition and increased funding.

While I am no geopolitical conflict expert, I believe that Ukraine's efforts to retake lost ground will turn into an even bigger growth engine for armored vehicles. After all, before the war, armies didn't lose combat vehicles. The horrors of the war in Ukraine have unveiled how important this segment is.

Furthermore, General Dynamics is the primary supplier of tactical bridges and expects increasing growth in this area. Additionally, there is demand for combat vehicles like Mobile Protected Firepower ("MPF"), Abrams, and Stryker. The Army's MPF program is expected to receive full funding, and Abrams tanks have become a strategic asset for many allies.

- Related to that, the munitions business is an area of focus for General Dynamics, particularly in the context of the war in Ukraine. The company has been working closely with the army and the administration to secure funding and contracts for munitions production. While the Biden budget showed a decrease in the munition budget, GD is confident that the administration is supportive and will provide additional funding as needed .

Given what I'm hearing from people familiar with defense procurement, I believe that munition growth is also turning into a bigger tailwind than initially expected.

{kind=link}

- General Dynamics' Technologies business, including GDIT (General Dynamics Information Technology) and Mission Systems, has faced supply chain challenges that have impacted its growth. While GDIT has continued to experience profitable low single-digit growth, Mission Systems has seen a decline in revenue due to these challenges. However, the company believes that the impact on the Technologies group is largely behind them and expects both segments to grow in the future .

With all of this in mind, there's more good news for shareholders.

Shareholder Returns & Valuation

On top of new emerging tailwinds, General Dynamics anticipates cash conversion rates around or above 100% beyond 2023. This means that the company will generate more cash than net income, which is a sign of high-quality earnings.

In light of that, the company's capital deployment will focus on sustaining the business, R&D, and reducing debt, with free cash flow allocated to dividends and share repurchases.

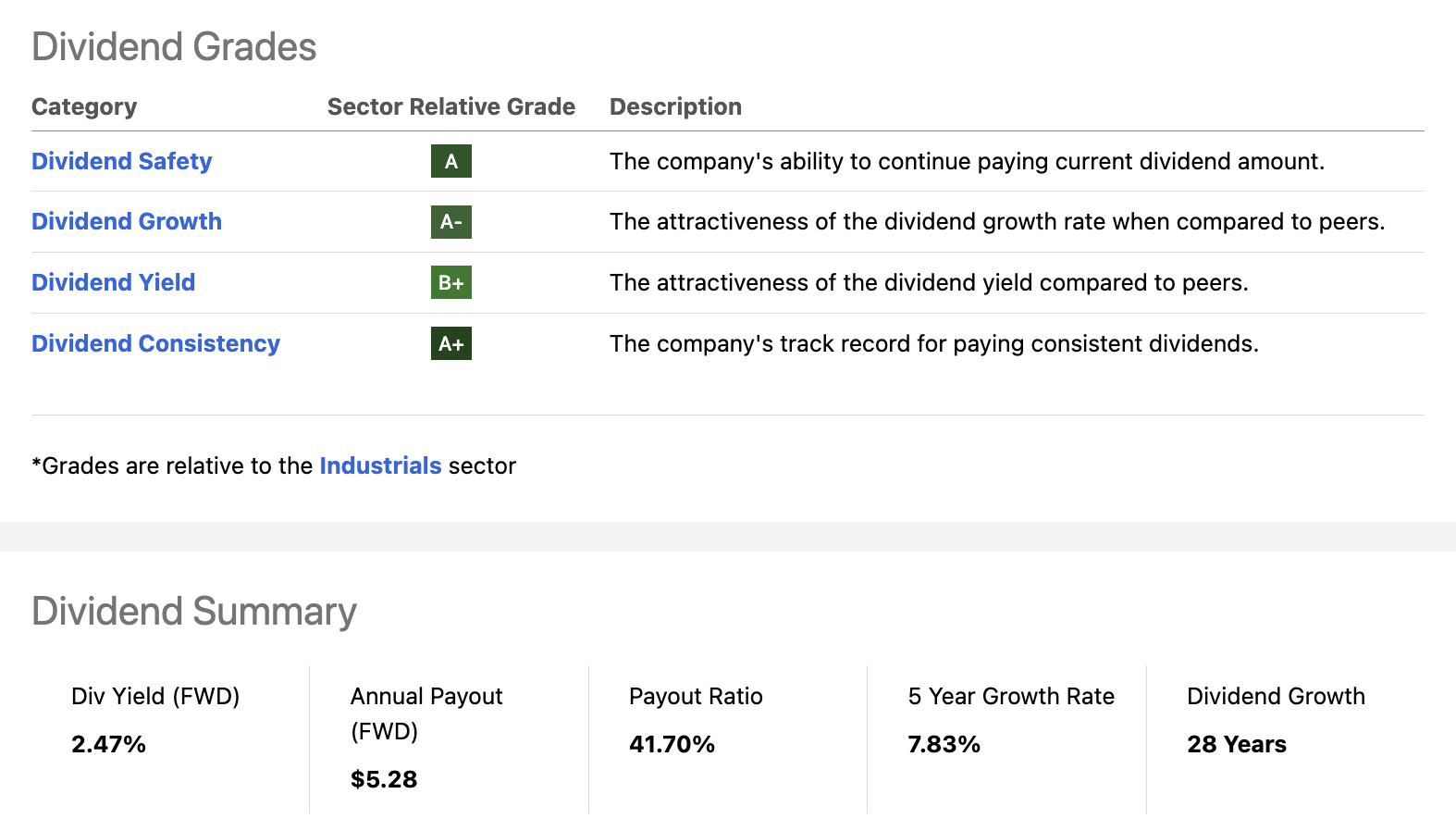

This dividend aristocrat with more than 25 consecutive annual dividend hikes has a dividend scorecard to write home about. The company has a 2.5% yield, a sub-45% payout ratio, and a 7.8% average annual dividend growth rate over the past five years.

{kind=link}

The most recent hike was 4.8%, which was announced on March 9. Going forward, I expect dividend growth to pick up, boosted by higher growth.

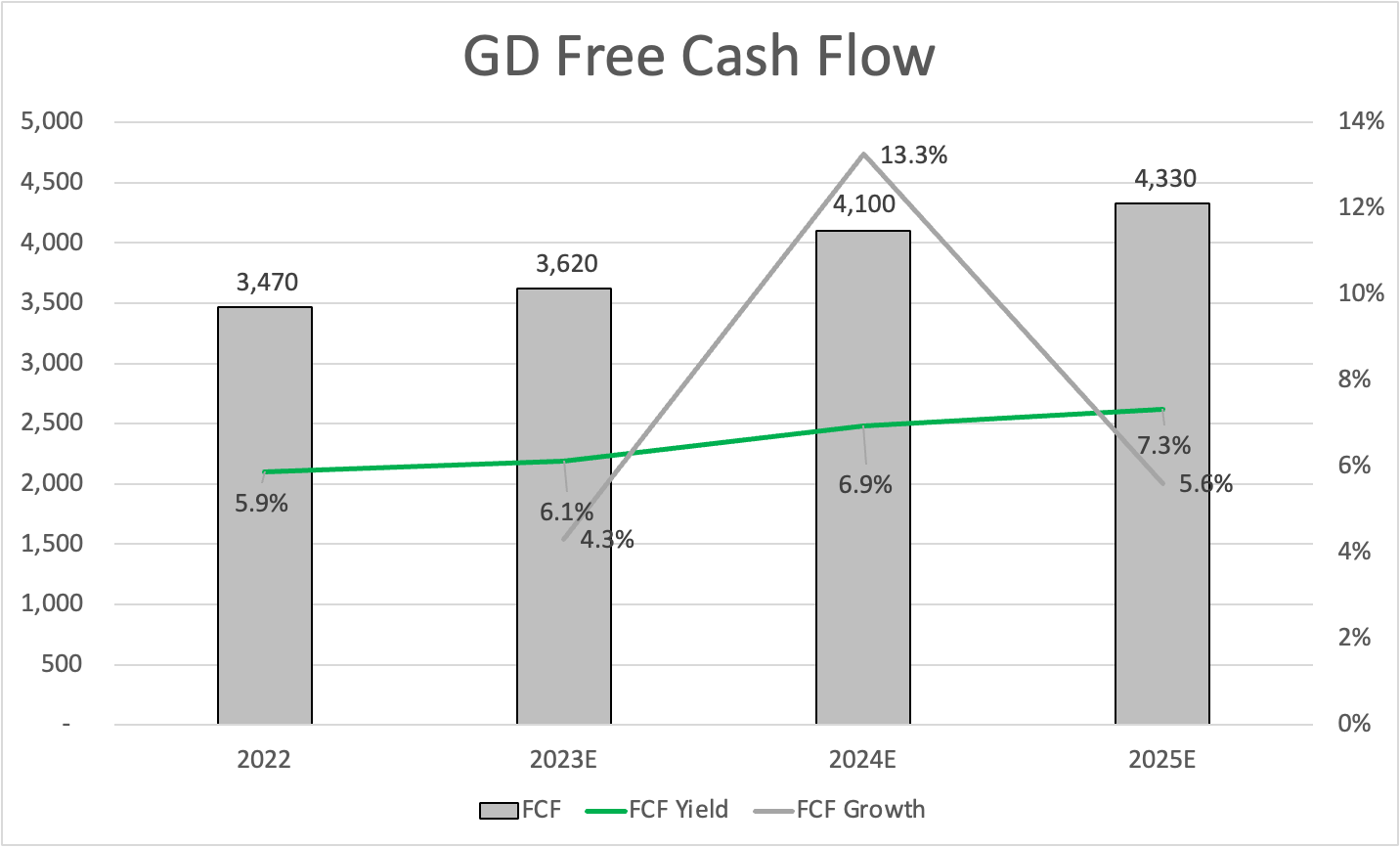

Looking at the chart below, we see that after 2023, free cash flow is expected to accelerate, which could result in a 7% free cash flow yield. This is one of the highest numbers I've seen in this industry.

{kind=link}

Not only does a 7% free cash flow yield protect a 2.5% dividend yield, but it also paves the road for higher growth in the future.

Furthermore, because the company has a 1.5x 2023E net leverage ratio and an A- credit rating, it does not need to prioritize financial health. This allows for aggressive buybacks.

Over the past ten years, the company has bought back more than a fifth of its shares. I expect this trend to continue, as the company is generating too much cash to not buy back its own shares.

I also need to say that the current valuation warrants rather aggressive buybacks.

Using the aforementioned free cash flow estimates, GD is trading at 14x 2024E free cash flow. That's a great deal, as I believe that GD should trade close to 20x free cash flow. The same goes for EV/EBITDA, which is now back at its long-term median. However, note that free cash flow conversion is stronger.

Analysts seem to agree with me. The consensus price target is $261, which is 22% above the current price.

FINVIZ

I agree that GD shouldn't trade below that target.

However, the market hasn't recognized GD's potential yet.

We shouldn't blame this on GD but on the market in general.

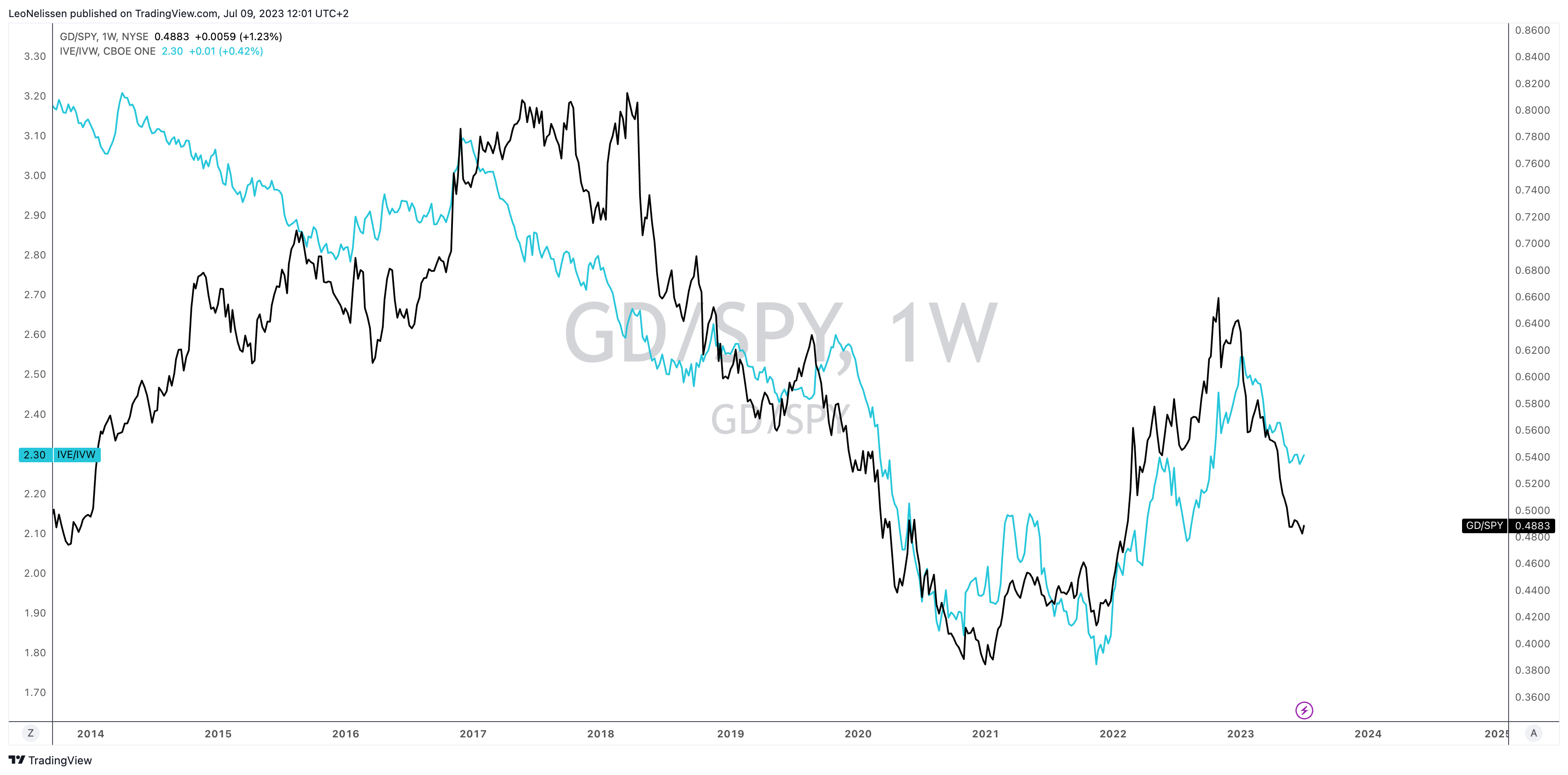

The chart below compares the ratio between GD and the S&P 500 ( SPY ) to the ratio between value ( IVE ) and growth ( IVW ) stocks. Over the past few years, GD has traded like a value stock. Given the strong performance of tech since last year, the market wasn't willing to bet on undervalued industrials.

{kind=link}

While that may be annoying for the time being, I believe that these developments come with a lot of opportunities - especially if inflation turns out to be sticky, which could give the Fed more reasons to keep rates elevated on a prolonged basis.

If I didn't have any defense exposure, I would be a buyer at current levels, as I not only consider GD to be too cheap, but I also believe that the stock has the ability to outperform the market on a prolonged basis.

Takeaway

General Dynamics presents a compelling investment opportunity with its well-positioned growth potential and attractive valuation.

The company's diversified defense segments, including Technologies, Marine Systems, Aerospace, and Combat Systems, offer a strong foundation for expansion.

With anticipated demand for defense hardware like military vehicles and private jets, as well as growth in munitions and supply chain improvements, GD is poised for success.

Furthermore, GD's focus on profitability and strong cyclical demand in its Gulfstream segment, along with increased defense spending, provide additional tailwinds.

The company's commitment to shareholder returns through dividends and share buybacks, backed by its high-quality earnings and cash generation, adds to its appeal.

Current undervaluation and a potential shift from growth to value stocks make GD an attractive dividend play.

For further details see:

General Dynamics Is Poised For Growth And Way Too Cheap