GD - General Dynamics: Price Is Still Sky High

2023-03-07 07:40:51 ET

Summary

- General Dynamics has established itself as a major player in the defense industry driven by an impressive track record of profitability.

- GD stock is expected to benefit from an increase in the US government's larger defense budget driven partially by Russia's invasion of Ukraine.

- Investors should be cautious about paying too high a premium for their shares.

Intro

National security is undoubtedly crucial for any country's prosperity, and it has led to the emergence of a profitable defense industry aimed at safeguarding against external threats. Defense contractors are the companies that operate within this industry. Due to the critical nature of their work and the relationships they build with countries, they enjoy a competitive advantage that is challenging to replace.

Recently, defense contractors have faced intense scrutiny over accusations that they profit from war, leading to questions about the necessity of the US government's substantial defense budget. This has created pressure on companies like General Dynamics ( GD ). In this article, we will analyze GD's business models, its historical performance, and its future prospects in order to determine the company's intrinsic value.

The Business

General Dynamics Corporation is a global company that specializes in aerospace and defense. Founded in 1899, GD is headquartered in Reston, Virginia. Its operations are divided into four segments: Aerospace, Marine Systems, Combat Systems, and Technologies.

The Aerospace segment focuses on designing, manufacturing, and selling business jets. Additionally, it offers services such as aircraft maintenance, repair, management, and staffing.

The Marine Systems segment specializes in building nuclear-powered submarines, surface combatants, and auxiliary ships for the United States Navy. It also constructs crude oil and product tankers, container and cargo ships, and provides navy ship maintenance and modernization services.

The Combat Systems segment's primary focus is on the production of land combat solutions, including vehicles, weapons systems, and munitions. This segment also offers modernization programs, engineering, and support services.

Lastly, the Technologies segment provides information technology solutions and mission support services, including cloud computing, artificial intelligence, and unmanned undersea vehicle manufacturing and assembly services.

Performance

During the last decade, the company has experienced consistent revenue growth, but has not been growing fast. In the most recent fiscal year, it reported sales of $39.4 billion. This figure reflects a just a 27% increase in sales over the last ten years.

GD hasn't been able to achieve consistent free cash flow growth either as the company reported four years of free cash flow declines over the last decade. Overall, the company only managed to grow its free cash flows by just 24% during the period.

GD is a slow growing company but there are some bright spots for investors. First, the company has established a nice track record of profitability. During the previous decade, GD averaged a return on equity of 23% without a single year less than 18%. A consistently high ROE indicates that the company is effectively utilizing its assets to generate profits, and it also suggests that the company has a strong competitive advantage in its industry.

Data by Stock Analysis

Another positive for the company is how share holder friendly it has become. During the previous ten years GD raised its dividend by 195%. In fact, GD has raised its dividend 28 years in a row. The company has also built an impressive track record of buying back shares, purchasing 22% of the company's shares during the last decade.

Data by Stock Analysis

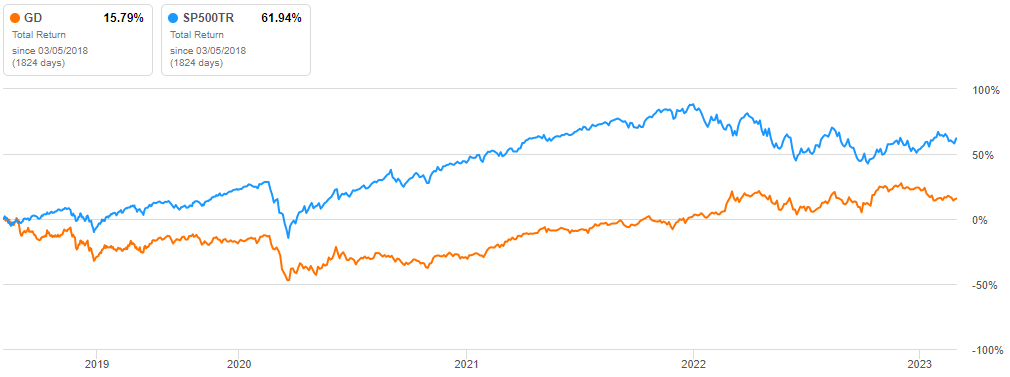

Despite the company's outstanding track record of profitability and how well it's taken care of its shareholders over the years, GD has underperformed the total return of the S&P 500 by a substantial margin over the past five years leaving many shareholders feeling frustrated.

{kind=link}

Outlook

GD's success is determined by its ability to meet government's needs for defense and security products and services which it has historically done really well as it has established itself as a leading defense contractor for the US government. Roughly 70% of its revenue comes from the U.S. government, which means that the company's financial performance is heavily affected by government spending levels, especially in the defense sector.

The fiscal year (FY) 2023 defense appropriations bill, signed into law on December 29, 2022, amounted to roughly $798 billion. This represents an increase of approximately 10% compared to the spending level for FY 2022 that was enacted which will be a tail wind for GD moving forward.

This 10% increase in US defense spending can be partially attributed to Russia's invasion of Ukraine . During fiscal 2022 the United States had given a total of $28 billion in defense assistance to Ukraine to provide financial support, training, equipment, and guidance to Ukrainian forces. It is likely that Congress will continue to provide extra emergency funding for Ukraine in the foreseeable future as more needs and expenses arise over time.

As the US defense budget is set to increase by 10%, GD is projecting that the Aerospace segment's revenue will increase to around $10.4 billion in 2023, up from $8.56 billion, mainly due to the delivery of 145 new aircraft. However, it is expected that the revenue for the other segments will remain mostly flat in 2023.

It should be noted that although the US defense budget is expected to increase, defense contractors such as GD have faced significant criticism for allegedly profiting from war. Additionally, the US government has been under intense scrutiny as many question whether allocating such vast resources to the defense budget is necessary. This criticism and scrutiny have been and will continue to be a head wind for GD moving forward.

Despite this, investors will be reassured to know that the company is continuing to prioritize them. As of December 31, 2022, the company has 6.7 million remaining shares that are authorized to be repurchase, representing 2.4% of the total outstanding shares. Also, on March 2, 2022, the board of directors announced an increase in the quarterly dividend to $1.26 per share from $1.19.

Valuation

To start with the valuation section, we will utilize a DCF analysis to reverse engineer GD's present stock price and determine the growth rate required in the next decade to validate the company's current share price. Afterward, we'll discuss if that growth rate is reasonable.

We'll start with GD's average free cash flows for the past five years, which comes out to be $2.63B. We'll leave the growth rate over the first ten years blank for now because this is what we are solving for. Following the 10th year, we'll use a 2.5% growth rate to determine the terminal value.

To discount the cash flows, we'll use a 10% discount rate, which is based on the long-term annualized S&P 500 return with dividends reinvested. With these inputs, we will find that a 10.35% annual growth rate over the next ten years is needed to justify GD's current share price of $232.26 at the time of writing this article.

{kind=link}

The 10.35% annualized free cash flow growth rate implied by GD's current share price, far exceeds the growth rate that GD was able to achieve over the previous ten years. However, analyst do estimate GD's earnings to grow by 9.32% annualized over the next five years which is materially higher than its growth rate over the previous five years of just 2.77%.

While I think that the rise in defense spending by the US will benefit GD in the coming years, I find it difficult to believe that GD can maintain a 10.35% yearly growth rate of free cash flows for the next ten years. Therefore, my assessment of GD using the DCF analysis suggests that it may be slightly overvalued.

When evaluating a stock, it's important to use multiple valuation techniques because no single method can provide a complete and accurate picture of a company's financial health or future prospects. Therefore, we will also run a comparative analysis on GD to estimate its intrinsic value.

The comparative analysis will examine the company's highest, lowest, and median price-to-earnings ratios that the market has used for GD over the past five years, as well as the sector median P/E ratio of 20.81 . We will then utilize these ratios to evaluate CNI's projected 2023 EPS estimate of $ 12.77 per share.

| Scenario |

| P/E |

| Next Year Earnings Estimate |

| Intrinsic Value Estimate |

| % Change |

| Bear Case |

| 8.898 |

| $12.77 |

| $113.63 |

| -50.99% |

| 5Y Median P/E |

| 16.9 |

| $12.77 |

| $215.81 |

| -6.92% |

| Bull Case |

| 24.08 |

| $12.77 |

| $307.50 |

| 32.63% |

| Sector Median Valuation |

| 20.81 |

| $12.77 |

| $265.74 |

| 14.62% |

The comparative analysis of GD reveals multiple potential outcomes. In an optimistic scenario, if the market applies the 24.08 multiple observed in March, 2018, to the average earnings estimate of GD for the next year, investors could potentially gain up to 32.63% if those estimates are met. Conversely, in a pessimistic scenario, if GD is valued at the low P/E ratio observed in 2020, investors could potentially lose up to 50.99%.

According to the 5-year median P/E ratio, the most probable outcome for GD is its base case scenario, which is considered to be the most important. If this scenario becomes a reality, investors might be able to receive a modest loss of 6.92%.

In the event that GD is valued at the sector median multiple, the outcome would be a slight return of 14.62%. All in all, the comparative analysis implies that GD is a little overvalued, and investors should expect to see a modest pull back to GD's current price and should only see a satisfactory return or substantial loss if the extreme cases were to play out.

Takeaway

GD has established itself as a major player in the defense industry driven by an impressive track record of profitability as it has consistently produced excellent returns on equity over the last decade. Despite this, GD has struggled to achieve outstanding revenue or free cash flow growth in recent years. However, the company is expected to benefit from an increase in the US government's larger defense budget driven partially by Russia's invasion of Ukraine.

That being said, investors should note that GD's stock is slightly overvalued at its current prices based on a discounted cash flow and comparative analysis. While the company's strong position in the defense sector and its ability to win high-profile contracts make it an attractive investment, investors should be cautious about paying too high a premium for its shares.

For further details see:

General Dynamics: Price Is Still Sky High