CRM - General Dynamics: The Best War Coupon For 2023

Summary

- General Dynamics is our most preferred Aerospace and Defense stock given the availability of near-term catalysts and the financial impact on near-term 12-month financial results.

- We anticipate General Dynamics will surprise on revenue and earnings over the course of 2023 given the rising threat environment of the Ukrainian War.

- We expect significant consequences tied to the Ukrainian War, but as investors we have to be mindful of the risks in this environment and hedge those risks in the portfolio.

- We recommend General Dynamics at Strong Buy and anticipate +25% upside at 16.24x FY '25 dil. EPS (estimate).

- We expect General Dynamics to perform better than some of its peers in the defense sector despite political headwinds and view the stock as a hedge to Asia supply chain risks, which could impact stocks like AAPL, TSM and TSLA.

General Dynamics ( GD ) stock hasn’t recovered to its all-time high of $258, as it continues to hover at about $229 despite the changing threat environment in the Ukrainian War. We believe some of the narrative shift happened towards the end of the year, as markets started to weigh the impact of a split Congress on the ability to pass any real meaningful spending legislation with much of the debate and lost momentum happening in the lower house of Congress. We believe experts and markets expected that Congress would pass an 10% increase to defense spending in 2023, but ultimately settled on an 8% increase to defense spending given the mismatch in political differences between both the Republican and Democratic Party.

We believe the differences in anticipated military budgets had a negative impact on the stock price of the sector though we believe General Dynamics is the best positioned defense stock in the sector given its heightened concentration of military revenue, and broadness of portfolio. Also we like the underlying narrative of military ground systems (M1 Abrams tanks) and added munitions sales growth when compared to some of the other peers, which have promising timelines but difficulties with reaching near-term revenue goals. Hence, we turn to General Dynamics as the one stock in Aerospace with the most near-term potential to surprise on production, revenue, and expectations, which is exactly what investors need in order to hedge the counter-cyclical rotation out of bad performing tech stocks.

We recommend General Dynamics at Strong Buy and offer a price target of $290, as we value General Dynamics at 16x - 16.5x FY ‘25 earnings, which is extremely conservative for a valuation in the technology and defense sector. When compared to other stocks that are trading on the assumption that war contagion risks exist in a vacuum like tech stocks the obvious hedge would be a company like General Dynamics. Given the risks of the environment we also own some other defense names, as they have performed very strongly as a group, but in particular, we find the +25% upside in General Dynamics stock relatively compelling given the risk/reward.

Why invest into Aerospace and Defense stocks?

Amazon ( AMZN ), Intel ( INTC ) and Microsoft ( MSFT ) or the AIM group reported below expectations in the past quarter. We call it the triple “data-center blues” where inevitably the comparison to dinosaur IBM ( IBM ) becomes more apparent, but not exactly. You could include IBM. Suppose you could call it the “quadruple data center blues” to emphasize how bad IT sector stocks are performing currently. Cisco ( CSCO ) and Oracle ( ORCL ) being the usual non-performers and also enterprise software stocks like Salesforce ( CRM ) struggling and digital advertising stocks like Angi ( ANGI ) and Zillow ( Z ) caught naked in this environment.

We think IT stocks should be exchanged for war stocks quite frankly, as we’ve been hedging against war risk, as none of these tech stocks hedge against the impact of inflation very effectively, or benefit from any disruptions tied to the Ukrainian War as they are tech companies with an emphasis on hardware, which could also be disrupted due to any added instability in the China South Sea where the Chinese Government has been dredging and building islands as miniature military bases.

We think Chinese provocations and on-going risk of manmade and natural disasters tied to the Asia supply chain are astronomical and could be hedged with alternatives like aerospace, particularly we like General Dynamics, which we discuss primarily in this report.

Also, when compared to our research on Raytheon ( RTX ), which we discuss here separately, we like General Dynamics more as we expect more upside when compared to the more limited upside on RTX stock and likely $100 resistance level keeping traders contained. Hence, our neutral rating. Poor missile segment results due to production delays, and on-going engine issues tied to the Pratt & Whitney F135 engine, which is part of the F-35 program keeps the stock’s upside limited near-term. We only expect +15% upside as we offer a $110 price target at 21x earnings on RTX stock currently. But, we also like the fact that expectations are so low, and the order backlog for missiles and rockets are quite high across the RMS (Raytheon Missile Systems) segment, it’s just that production is really struggling, because the rockets and missiles that Raytheon produces are guided systems, which take longer to procure.

When looking long-term we like Textron ( TXT ) $105 price target at 22x FY’ 25 EPS, which we discuss here . Mainly tied to the Bell-Valor V280 program, as it’s a game changer with a tilt-rotor design or the miniaturized V-22 Osprey used primarily by the Marines and Special Operations. We believe the Army version or the V280 craft and mass production drives the strongest long-term growth narrative in the segment given the outstanding value of the Apache and Black Hawk helicopters in the US Army; we estimate the total value of the contract at $3.3 trillion spread over 70 years or $47 billion in value annually assuming a combination of inflation, production, maintenance, and retrofit figures. Yes the numbers start to spiral like the US budget, but we expect revenue to reach ridiculous levels assuming 3,300 vehicles get produced for the U.S. Army, costing $100 million per unit and have on-going sustainment contracts. However, we expect even more units to be built, likely 10,000+ units total, which could be sold to foreign G-20 NATO ally countries or through manufacturing agreements to other countries with a strong military manufacturing base like Japan, South Korea, Germany, Canada, Saudi Arabia, and UK. Keep in mind we’re talking lifetime figures over the course of 70-years.

War and the political situation room gives us room to expect more this year

Military executives were anticipating a tax credit tied to research and defense spending , and absent the tax credit, the corporate tax rate outlook for General Dynamics went up to 17% for FY ‘23 based on management’s outlook versus 15.9% tax rate for FY ‘22. We think defense executives tried their best to persuade Congress, but ironically the Omnibus spending bill unveiled no provision for on-going tax credits tied to military R&D spending, which put somewhat of a negative tilt on defense sector stocks forcing investors to be more selective in this environment.

Phoebe Novakovic CEO and Chairwomen of General Dynamics mentioned on the Q4 ‘23 earnings call:

“Forecast comes from our operating plan. It is conservative as it must be in this environment of unpredictable financing of the government. However, the threat environment suggests increases in defense spending. In short, I see more opportunity than risk in our forecast.”

The War Situation Room in Ukraine has gotten bad, and at least based on the most recent news reporting, there’s a likelihood that 500,000 additional Russian troops will be deployed to the front lines of Ukraine in March. However, in the fog of war, we think satellite imagery is somewhat foreboding as it’s suggesting an even larger offensive than the initial 150,000 troops that were initially deployed at the border as part of the “Special Military Operation” back in March of 2022.

We’re not certain if 31 M1 Abrams tanks (pertinent to the discussion) provided by the Biden Administration will be sufficient in addressing the present threat environment. Despite what Phoebe Novakovic repeatedly mentioned as being conservative growth guidance on Q4 ‘22 earnings call, where she reiterates a conservative growth figure of 5% for total top line revenue for 2023, but also leaves a lot of room for speculation on military deliveries.

Currently, 90 Stryker Armored Fighting Vehicles and 31 M1 Abrams sent to Ukraine won’t move the needle enough and it will inevitably lead to more requests for support from Volodymyr Zelenskyy. We think Ukraine is going to need more Stryker Fighting Vehicles and M1 Abrams tanks to win the war based on the substantial increase in the reported number of Russian soldiers gathering at the border.

Ultimately, the difficulty of the threat environment and also the need for more military resources determines not only the number of vehicles sold, but also the amount of sales General Dynamics will generate from servicing the Stryker and Abrams. We anticipate that the war will become even more protracted, thus demanding the need for a greater number of tank battalions and also a greater number of Stryker Assault Vehicles.

Figure 1. Stryker M-Shorad (Maneuver Short Range Air Defense)

Stryker Anti Air Configuration (Stryker)

We find ourselves optimistic on this outcome however, as the Stryker provides added mobility and has a number of combat uses that far exceeds the value of APCs (Light Armored Vehicles) such as air defense (image above), mortar, cannon, minesweeping, medical, transportation, and can substantially improve the outcome of the war by simply offering more transportation for mechanized infantry units on the front lines that are stagnating in a trench war.

This creates the possibility of attacking the lines with flanking maneuvers, or to break the weaker points of the front line and then flank the opposing military units. We anticipate that the number of tanks needed to beat the Russian military will increase, as initial reports of tank casualties might not take into consideration the fog of war, and also the likelihood that the Russians are retrofitting, repairing, and likely to deploy a greater number of tanks in conjunction with the reported 500,000 additional reserve soldiers gathering at the border. I think it's inevitable that the Russians will deploy more tanks on the battlefield regardless of casualties, and will eventually deploy newer variants of various tanks as the conflict rages on as they’re still manufacturing vehicles despite on-going shortages.

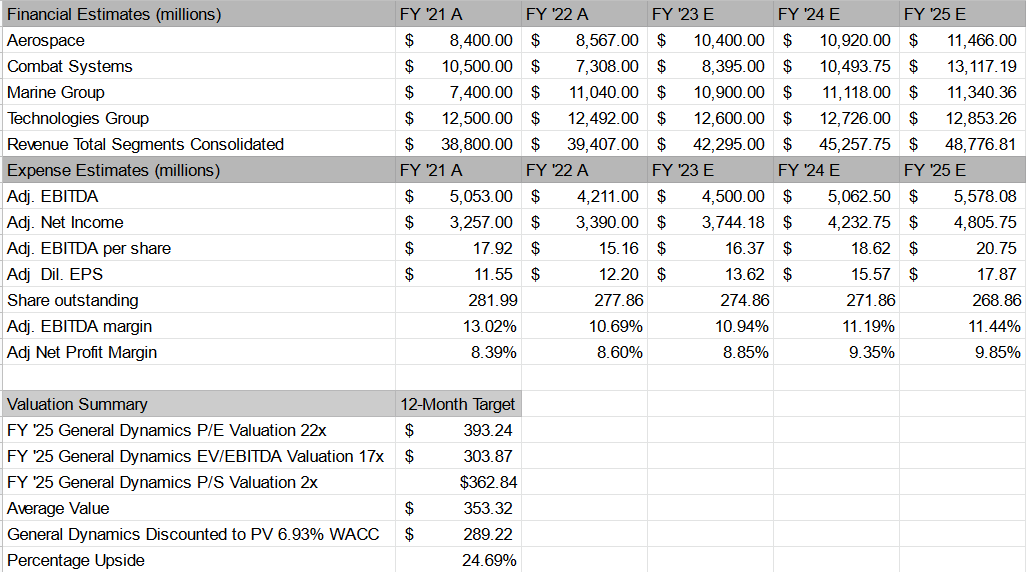

General Dynamics financial model and price target valuation

We expect much stronger revenue from the ground systems business, General Dynamics has the spare production capacity as indicated on the Q4 ‘22 earnings call, as CEO and Chairman, Phoebe Novakovic mentions:

“Staffing is not an issue here, plenty of capacity on the combat system side, both tracked and wheeled. So to the extent that the US Government intends to execute any current contract with some of these bilateral agreements that they are developing, we can – it’s well within the capacity of the industrial base to accommodate.”

Much of the upside on FY ‘23 results in our financial model stems from the results tied to the ground systems business unit, which will primarily benefit from the additional sales of M1 Abrams tanks to various NATO members along with the on-going support and sustainment contracts tied to the deployment of M1 Abrams tanks and Stryker combat vehicles in Ukraine.

Given the added scope of upside tied to maintenance, and delivery of M1 Abrams tanks with the addition of more of these modern marvels added to the arsenals of European allies, we expect revenue to surprise consensus estimates. We forecast sales of $42.295 billion FY '23 versus $41.17 billion FY '23 consensus. The difference in estimates (+$1.125 billion) being made up entirely of M1 Abrams and Stryker related revenue, which would translate to a significant beat on financial results for FY ‘23 from where the stock is currently, and would drive the stock price materially higher on stronger results tied to Combat Systems, and an eventual uptick in Aerospace related revenue driven by G700 and G800 deliveries over the next couple years.

Figure 2. General Dynamics Financial Mode

{kind=link}

General Dynamics Financial Model (Trade Theory)

We expect net profitability to improve very gradually in-line with management commentary with an eventual goal of reaching 10% average net profitability for the entire company sometime over the next couple of years. Of course, the management discusses profits by segment, but basically we expect about +125 bps of net profit improvement driven by a number of factors like the reduction in R&D tied spending for the G700 and G800 following launch over the next 12-months for both model variants tied with the ramping mix towards combat systems revenue and ammunition driving a stronger net profit narrative and exiting our financial model at 9.85% net profit margin, which we use to compute the diluted EPS figure for FY ‘25 or $17.87 diluted EPS.

Furthermore, we expect very modest capital returns over the next 3-year period, though we could imagine that if profitability starts to improve the share buybacks from the $1.2 billion spent on buybacks this past year will trend higher as well. We expect revenue surprises driven by a combination of Aerospace and Combat systems results, which contributes to the divergence in our expectations from consensus, as our FY ‘24 revenue of $45.25 billion and diluted EPS of $15.57 is better than the expected results from consensus at $43.48 billion, and $14.75 diluted EPS, which conforms with analyst estimates. This is mainly because we expect the addition of next-generation Gulfstream Private jets (fastest in business class) reaching new heights in terms of revenue contribution.

We expect Combat Systems to return to 2021 revenue levels by 2024. Prior to the troop withdrawals from the Middle East in December 2021, the Combat Systems segment reported $10.5 billion in sales; we anticipate that those levels will be reached by end of FY ‘24 in our financial model. We anticipate that revenue from Combat Systems will return following what has been a weak FY ‘22 due to absence of ground presence in the Middle East offset by the overwhelming need for Main Battle Tanks or MBTs (for short) in 2023 and 2024 in Eastern Europe where sales from combat systems translates to 16% growth CAGR over the next 3-years in our financial model. This might sound out of the ordinary, but given the historical levels of the business, and the need for MBTs and Stryker vehicles on the battlefield, we feel very confident that the forecast can be met, and the stock price will continue to appreciate by our forecasted amount of +25% over the next 12-months.

We arrive at our General Dynamics price target after applying a 22x earnings, 17x EV/EBITDA multiple, and 2x sales multiple to FY ‘25 results. We then discount our average value for the stock, and use the firm’s WACC of 6.93% to arrive at our prevent value estimate of $290 for General Dynamics. We believe our estimate is extremely conservative, as it computes to just a 16.24x forward earnings multiple on FY ‘25 estimates in our model meaning we’re paying just 16x earnings to buy the stock’s projected FY ‘25 dil. EPS assuming there’s a demand surprise over the next 12-months for Combat Systems.

General Dynamics investor thesis summary

The temporary weakness in the stock price might leave some in disbelief regarding our bullish take on the stock, but we believe the stock will start to trade at new all-time highs by year end, as we expect trends in military spending to continue trending higher globally, as the scale of the Russian offensive is expected to increase based on numerous news briefings tied to the war, and what’s been made public by the US, Ukrainian, and Russian Governments.

The upside tied to Abrams deliveries in Ukraine isn’t fully priced into the stock, and many experts will agree that the war casualties will likely trend higher even with the inclusion of modern armor. We expect investors can hedge much of the war-themed risks in their portfolio by carefully selecting certain aerospace stocks out of the group.

We in particular like General Dynamics over the next 12-months, as we anticipate a solid string of beat and raise quarters with a competent CEO at the head of the company making all the necessary moves needed to generate shareholder value.

We recommend General Dynamics at strong buy, and we expect +25% upside from where the stock is trading at the time of writing, which is $231 per share currently. We think there’s a very straightforward path to $290, and we expect very limited downside risk with the exception of politically themed spending cuts to the military causing downside to the stock, or if the world's Governments actually finds a way to end the Ukrainian War within 12-months, which seems extremely unlikely, which diminishes risks from pacifism to the long thesis on GD.

For further details see:

General Dynamics: The Best War Coupon For 2023