GD - General Dynamics: Too Good To Be This Cheap

2023-05-08 14:11:37 ET

Summary

- The General Dynamics stock price is off to a bad start this year, falling more than 15% in light of debt ceiling talks and recession fears.

- While GD was negatively impacted by recent banking woes, it is expected to accelerate growth in the years ahead, thanks to improving orders and easing supply chain issues.

- Given its stock price performance and improving fundamentals, I believe that GD is attractively valued and an attractive dividend growth investment.

Introduction

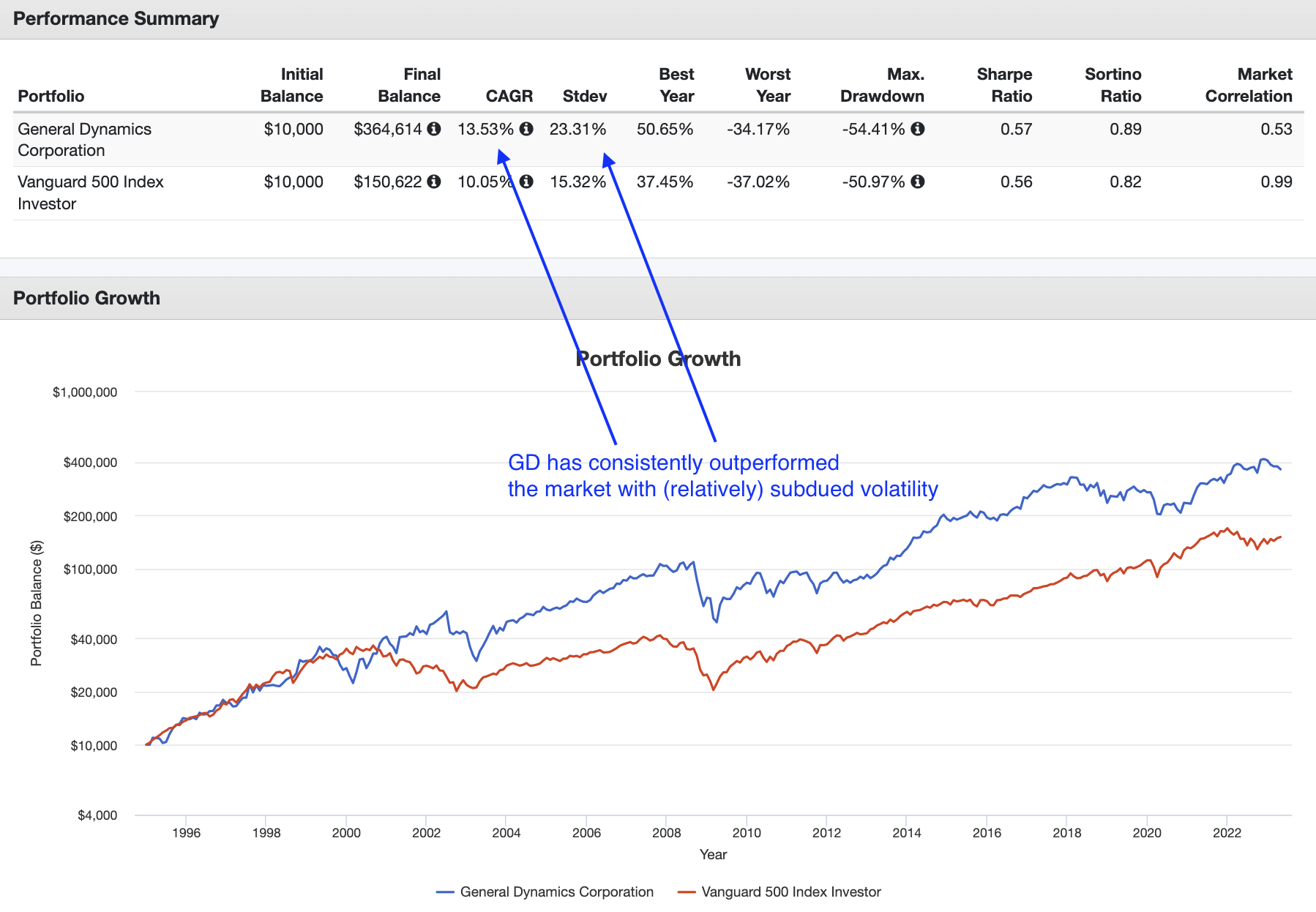

While every (dividend) portfolio is unique, I feel that a lot of my readers own shares in General Dynamics Corporation ( GD ) . I have covered this company a few times in the past as it is a pillar of the United States and NATO defense forces. On top of that, it is an excellent dividend growth stock with a track record of low-volatility outperformance.

{kind=link}

Portfolio Visualizer (Author Annotations)

Unfortunately, GD shares aren't in a good place right now. While we aren't dealing with a massive sell-off, shares are down 18% from their 52-week high and down 15% year-to-date. This happened despite the ongoing war in Ukraine, Chinese threats towards Taiwan, easing supply chain issues, and favorable defense budget developments .

Hence, in this article, we'll focus on this sell-off and assess if this might be a good spot to add some exposure or initiate a position for (dividend-focused) long-term investors.

So, let's get to it!

What To Make Of General Dynamics

A well-diversified defense contractor with fantastic dividend growth characteristics.

As I know I'm going to get questions in the comment section, let me start by explaining why I do not own General Dynamics.

I have more than 20% defense exposure, which is extremely high. I own Lockheed Martin ( LMT ), Northrop Grumman ( NOC ), L3Harris Technologies ( LHX ), and Raytheon Technologies ( RTX ).

As much as I like GD - as you will find out in this article - I did not buy it because a stock portfolio with fewer than 25 single stocks doesn't need five defense stocks. Also, I have all of GD's bases covered. Roughly 32% of GD revenues are generated in its Technology segment. I have technologies covered through other holdings, especially technologies that incorporate space and multi-domain warfare. 28% of GD's revenue comes from Marine Systems. While I do not own direct Navy exposure anymore, Lockheed has minor Navy exposure, while all of my holdings are major Navy suppliers.

Furthermore, 22% of GD's revenues come from its Aerospace segment, which is dominated by sales of various Gulfstream models. That's commercial aerospace, which I have covered via Raytheon's Collins and P&W segments.

18% of GD sales come from its Combat Systems segment. This includes heavy machinery like the mighty Abrams tank. While I do not own tank exposure, both Lockheed and Northrop produce heavy equipment and supply critical parts to others.

In other words, I have all bases covered.

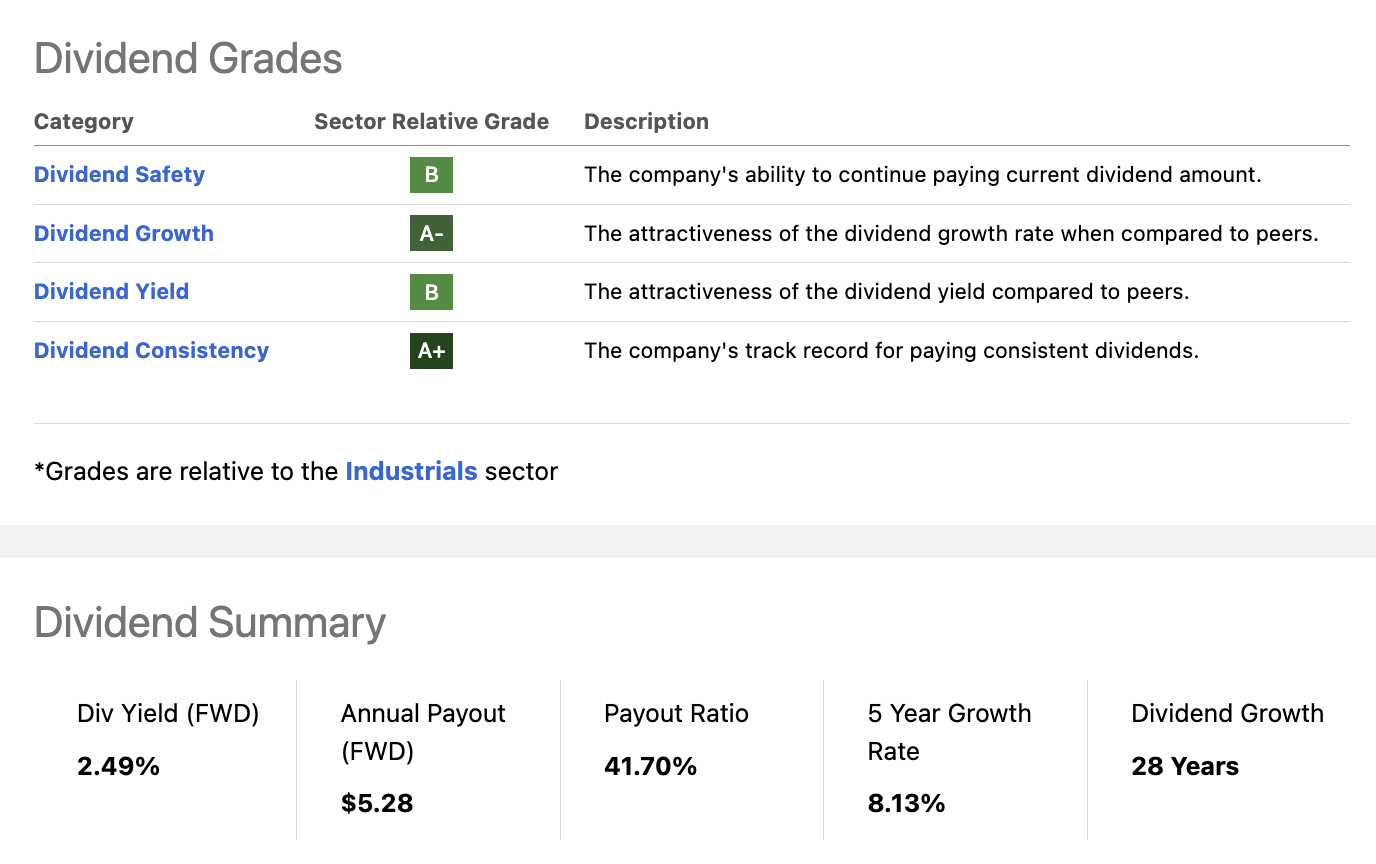

With that in mind, if I had a portfolio with more companies, I would likely buy GD at some point. After all, it has a wide-moat business and a fantastic dividend scorecard. As we can see below, the company scores high on dividend growth and dividend consistency. It has highly satisfying scores in the safety and yield departments.

{kind=link}

Seeking Alpha

- The company pays a $1.32 per share per quarter dividend, which translates to a yield of 2.5%.

- GD has hiked its dividend for 28 consecutive years, making the stock a member of the elite dividend aristocrats club.

- Over the past five years, the average annual dividend growth rate was 8.1%. The most recent hike was 4.8%, which was announced on March 9, 2023.

- The company has a payout ratio of 41.7%, which is supportive of continuing dividend hikes, but above the sector median of 28%. Please note that the median dividend yield in the sector is 1.6%. In other words, while GD has a higher payout ratio, it also has a significantly higher yield.

On top of that, the company engages in buybacks. Over the past ten years, GD has bought back 22% of its shares, which has added to its ability to outperform the market.

With that in mind, GD is down almost 20%. In other words, we need to assess why that is to avoid buying a bull trap or a stock that could turn into a pet rock. After all, paying and consistently growing a dividend isn't enough to satisfy investors.

What To Make Of The GD Share Price Decline?

GD's business remains stellar, with strong demand and easing supply chain issues.

If there's one thing, I've learned from defense contractors in 1Q23, it's that tailwinds are rather strong. Essentially, it boils down to this:

- Global defense demand remains very strong as nations continue to prioritize defense spending in light of new global threats and the fact that some neglected spending for multiple decades.

- Supply chain bottlenecks are easing. While most supply chains have completely normalized, certain high-tech supply chains are lagging. Most defense companies expect things to normalize going into next year.

For example, certain electrical items still experience shortages, according to S&P Global ( SPGI ) data.

S&P Global

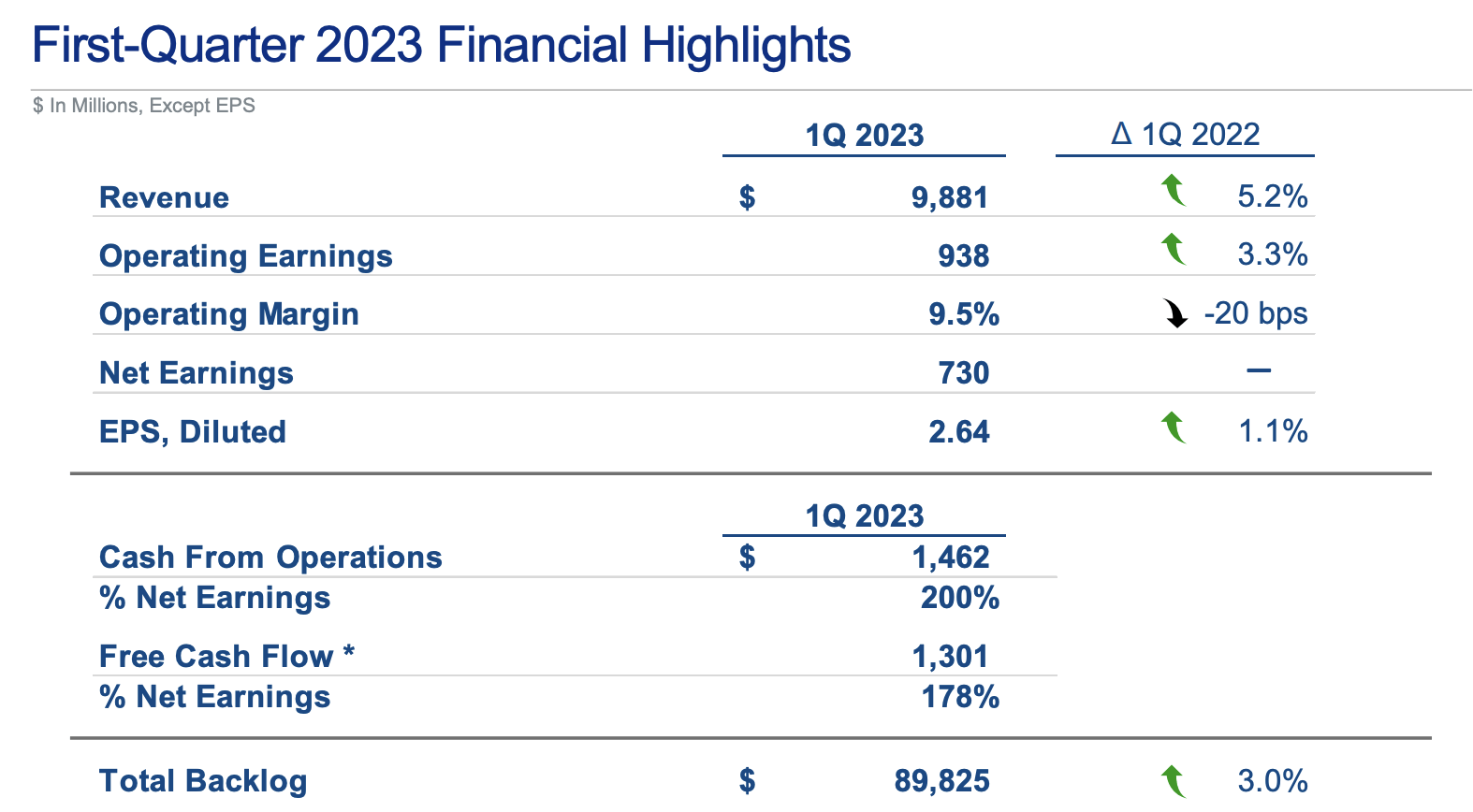

At the end of April, GD reported its earnings, which were quite good. The company grew its revenue by 5.3% to $9.9 billion, beating analyst estimates by $600 million. It allowed the company to generate $2.64 in GAAP EPS, beating estimates by $0.06.

{kind=link}

General Dynamics

The company had a 3% higher backlog of orders, which now stands at $89.8 billion. This number is down 1.4% quarter-on-quarter. Furthermore, according to the company (emphasis added):

We had a solid quarter from an orders perspective with an overall book-to-bill ratio of 0.9:1 for the company. Order activity was particularly strong in the Combat Systems group, which had a book-to-bill of 1.5x.

Essentially, this means that for every $1 in completed backlog, the company got $0.90 in new orders. That's indicative of slower growth down the road. However, it's not a disaster.

A big part of the new orders' weakness was caused by the recent bank failures and the impact this had on its Aerospace segment (Gulfstream private jets). According to the company, the banking stress created a pause in the market that lasted about three weeks. However, the company reported a return to normal demand, although it needs to be said that it's now clear how careful buyers of private jets are when it comes to potential market risks.

Going forward, the company anticipates a rebound in demand, leading to a >1x book-to-bill ratio.

[...] we had anticipated a book-to-bill -- full book-to-bill of 1:1 on at that point, higher deliveries. So, on a going-forward basis, it's our working assumption that we will continue to see 1:1 . And at the moment, we see no reason why that can't be achieved.

Furthermore, the company's non-Aerospace book-to-bill ratios were fine.

- Aerospace: 0.9x (book-to-bill).

- Combat Systems: 1.5x.

- Technology: 1.5x.

Furthermore, the Aerospace segment missed its first airplane delivery due to supply chain issues; however, the company expects the supply chain issue to be resolved in early Q3, which is a bit earlier than I expected. The company also noted that it was building a considerable number of G700s in the third and fourth quarters and would incur some period costs without the related revenue.

In Land Systems, the company saw increased revenue from the MPF ramp-up, Stryker SHORAD, and new international vehicle programs for Poland and Australia. At European Land Systems, the company had higher Parana volumes, and OTS enjoyed higher artillery program volume. The company also saw strong order performance, with orders at their highest level in more than eight years, which underlines the ramp-up in global defense spending.

The Marine Systems division continued to demonstrate impressive revenue growth, with a growth rate of 12.9% YoY, led by Columbia class construction and engineering, DDG-51 construction, and Submarine Construction. The company also noted that it had made progress on its Columbia-class submarine program, which it said remained on track to deliver the first boat to the Navy in 2027. It also delivered its 100th Virginia-class submarine and has nine under construction.

The company's Mission Systems unit had revenue of $1.32 billion, up 7.4% over the year-ago quarter, with earnings of $200 million, up 13.6% Y/Y. The unit's earnings benefited from higher volume across multiple product lines, increased manufacturing productivity, and the absence of COVID-related expenses from the prior year.

Furthermore, this business unit secured several key contract wins during the quarter, including a $1.2 billion contract to provide new satellite payloads for the Space Development Agency.

In light of these developments, the company did NOT update its guidance, which is common, as the company never updates its guidance this early in a business year.

However, the company did say that its second quarter will be weak, followed by a recovery in the quarters after that.

I would say, however, that our quarterly progression differs from prior years and that the second quarter will be our lowest quarter because of mix and volume across the business .

Nonetheless, we look forward to very strong third and fourth quarters . We will give you a comprehensive update at the end of next quarter as is our custom. This concludes my remarks with respect to what was a challenging but, in many respects, rewarding quarter.

In light of the robust fundamentals of the company, I believe the decline in the stock price can be attributed to two factors.

- Investors are selling cyclical stocks. While defense stocks are not cyclical, they account for 20% of the industrial sector. So, investors dumping cyclical stocks often leads to weakness in the defense industry.

- Debt ceiling risks aren't helping. While the ceiling will be raised and the US will continue to pay all of its debts, it's not helping that both parties in Washington are looking to gain from debt ceiling talks. This is making investors nervous that spending cuts could impact defense spending.

Democrats, who control the Senate, have insisted on a stand-alone bill, while Republicans, who control the House of Representatives, say any proposal to raise the country’s borrowing must include spending cuts and policy changes. - Wall Street Journal

While these uncertainties aren't helping, I do not expect defense spending to be hit by any cuts - both Republicans and Democrats have made it clear that defense spending is key. The worst case is that Republicans will go after what they consider to be non-relevant defense spending, which would not hurt GD or any of its major peers.

So, what about its valuation?

Valuation

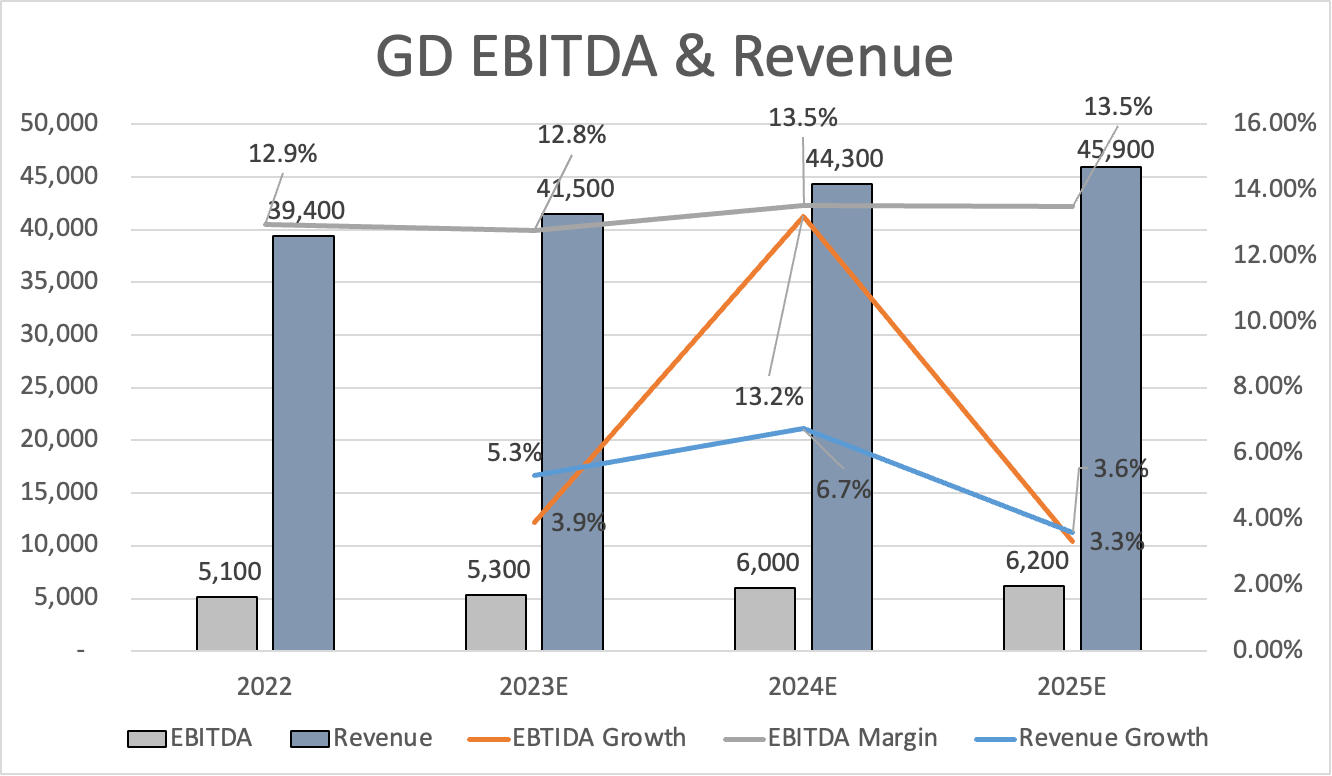

General Dynamics' revenue is expected to consistently grow to $45.9 billion in 2025. EBITDA margins are expected to gradually improve to 13.5%, backed by normalizing supply chains and easing inflation.

{kind=link}

Leo Nelissen

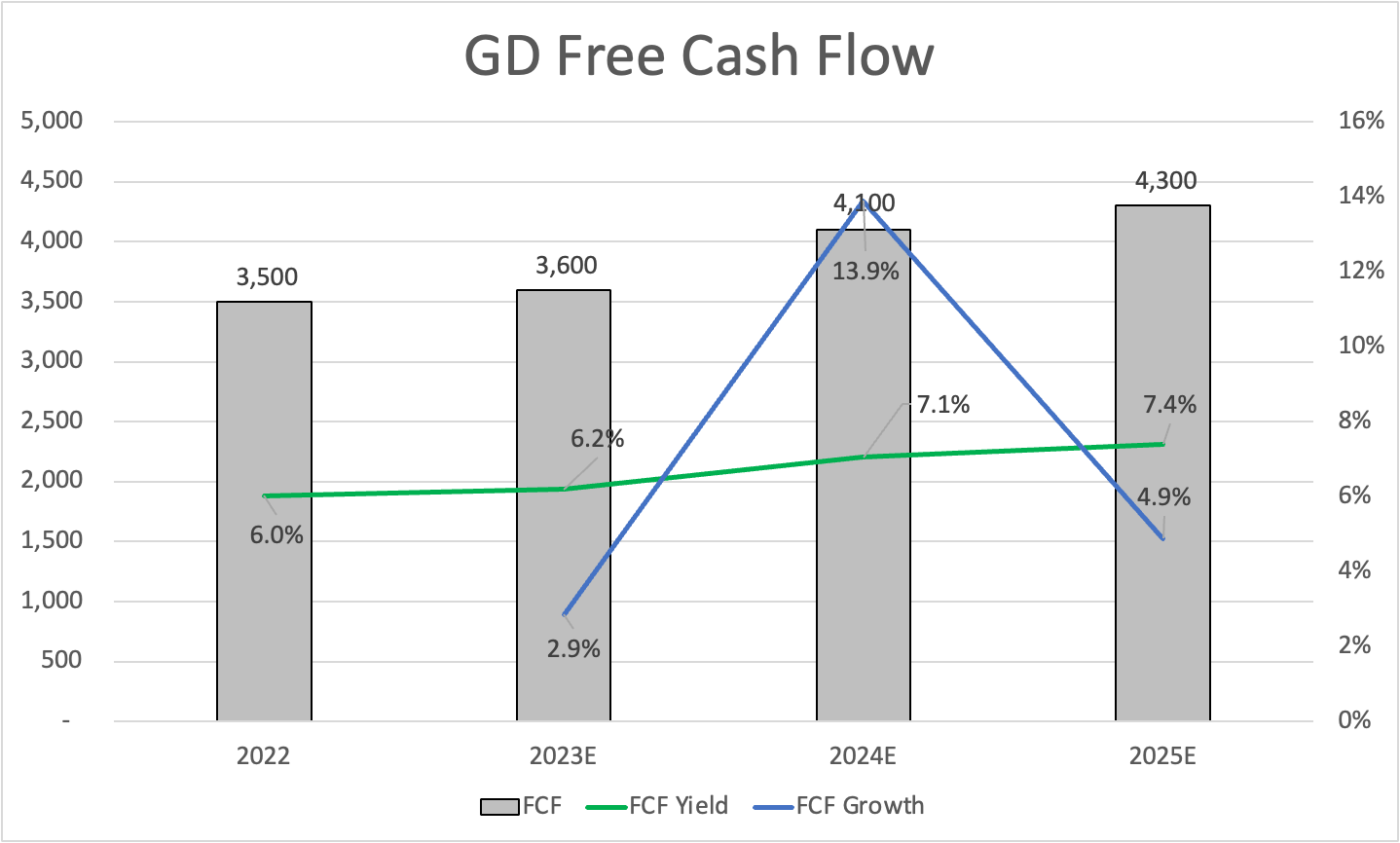

Free cash flow is expected to accelerate after 2023, which is in line with expectations for its peers. This is mainly based on a mix of the aforementioned easing supply chain issues and strong orders.

{kind=link}

Leo Nelissen

Hence, GD could end up with a free cash flow yield of more than 7% next year, supporting high dividend growth and buybacks. It also makes the valuation attractive.

Using 2024E data, GD is trading at 11.3x EBITDA.

The company is trading at 14.2x 2024E free cash flow.

Based on the company's fundamentals and future expectations, backed by demand and supply chain improvements, the company's valuation is attractive. In October 2022, I wrote that GD is a good buy whenever it drops 10%. The stock has fallen 15% since then, which reinforces my buy rating.

Takeaway

The General Dynamics stock price isn't doing too well this year, dropping roughly 15%. However, its core business remains strong. While banking woes temporarily hurt its order flow in the first quarter, the company is expected to end up with a >1x book-to-bill ratio in all segments, backed by strong defense and commercial demand.

Furthermore, easing supply chain issues are expected to boost margins and growth after 2023, allowing the company to boost dividend growth and fuel opportunistic buyback programs.

While the debt ceiling and recession-related headlines could keep a lid on the GD stock price for a few more months, I believe that GD is attractively valued, offering buying opportunities for conservative dividend growth investors looking for defense exposure.

For further details see:

General Dynamics: Too Good To Be This Cheap